|

市场调查报告书

商品编码

1689955

气体分离膜:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Gas Separation Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

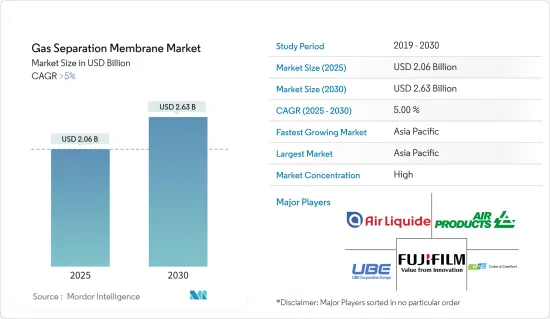

预计 2025 年气体分离膜市场规模为 20.6 亿美元,到 2030 年将达到 26.3 亿美元,预测期内(2025-2030 年)的复合年增长率将超过 5%。

COVID-19疫情对气体分离膜市场产生了负面影响。疫情扰乱了全球供应链,影响了製造气体分离膜所需的原料、零件和设备的供应。生产和运输延迟导致薄膜系统和组件暂时短缺。不过,随着各国逐步解除封锁限制,气体分离膜系统的需求开始恢復。

主要亮点

- 二氧化碳分离过程中对薄膜的需求不断增长以及政府对温室气体排放的严格监管预计将推动气体分离膜市场的发展。

- 然而,高温应用中聚合物膜的塑化、扩大规模和采用新膜预计会阻碍气体分离膜市场的成长。

- 此外,混合基质膜(MMM)和聚合物薄膜的更广泛应用有望为市场发展提供新的机会。

- 按地区划分,亚太地区占据了最大的市场份额。预计中国、印度和日本对气体分离膜的需求不断增长,将使其成为预测期内成长最快的市场。

气体分离膜市场趋势

氮气生成和富氧领域占市场主导地位

- 制氮和富氧是各种工业应用中不可或缺的过程。石油和天然气、化学、电子、食品和饮料以及製药等行业需要氮气覆盖、吹扫、惰性、包装等。同时,富氧对于燃烧、发酵、污水处理等过程也是必要的。

- 利用气体分离膜生成氮气和富氧可以实现现场气体生产,无需运输、储存和处理压缩或液化气体。这可以降低物流成本,提高供应链可靠性并提高工业营运的安全性。

- 氮气在食品和饮料行业中用于替代食品包装中的氧气,以延长保质期并保持新鲜度。它们也用于对桶加压并分配啤酒和苏打水等碳酸饮料。在食品加工业务中,氮气用于惰性、覆盖、冷却和冷冻。

- 中国啤酒产业也是全球成长最快的产业,预计到 2023年终总销售额将达到约 1,315 亿美元。

- 氮气和氧气在电子工业中也有应用。氮气在半导体製造过程中用作载气,以防止污染并维持精确的大气条件。它还用于波峰焊、回流焊接和三防胶工艺,以提高焊料品质并防止氧化。

- 根据半导体产业协会发布的报告显示,2023年11月全球半导体销售额与前一年同期比较增5.3%。

- 富氧用于炼钢、冶炼和非铁金属提炼等冶金工艺,以提高燃烧效率,降低燃料消费量,提高製程生产力。

- 因此,预计气体分离膜的需求将会增加,对市场研究产生正面影响。

亚太地区占市场主导地位

- 亚太地区包括一些成长最快的国家,例如印度、中国、日本、韩国和其他东南亚国家。这些国家正在经历显着的工业成长,推动了石油和天然气、化学品、电子、医疗保健、食品和饮料等各个领域对气体分离膜技术的需求。

- 亚太地区是製造业中心,拥有生产化学品、电子、半导体、汽车和消费品等多元化产业。气体分离膜是许多製造流程中的重要组成部分,因此该地区对其的需求很高。

- 根据世界钢铁组织统计,2023年12月中国钢铁产量为67.4吨。同时,印度已跃升成为全球第二大粗钢生产国。 2022-23财年,该国出口了672万吨成品钢,进口了602万吨。

- 此外,根据半导体协会的数据,2024年1月中国半导体销售额飙升至147.6亿美元,较前一年有显着成长。与 2023 年 1 月的 116.6 亿美元销售额相比,这是一个显着的成长。

- 此外,该地区能源产量的成长预计将刺激该地区酸性气体分离市场对气体分离膜的需求。

气体分离膜产业概况

气体分离膜市场呈现部分整合态势,少数几家大公司占据市场主导地位。市场的主要企业包括空气产品及化学品公司、宇部兴产株式会社、液化空气高级分离公司、DIC 公司和富士胶片株式会社。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 二氧化碳分离过程中对薄膜的需求不断增加

- 政府对温室气体排放制定严格的标准

- 限制因素

- 适用于高温应用的聚合物薄膜的增塑

- 扩大规模并采用新膜

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 材料类型

- 聚酰亚胺和聚酰胺

- 聚砜

- 醋酸纤维素

- 其他材料类型(奈米结构薄膜)

- 应用

- 产氮富氧

- 氢气回收

- 二氧化碳移除

- 硫化氢去除

- 其他用途(碳酸化)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 土耳其

- 俄罗斯

- 北欧的

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Air Liquide Advanced Separations

- Air Products and Chemicals Inc.

- DIC CORPORATION

- Evonik Industries AG

- FUJIFILM Corporation

- GENERON

- Honeywell International Inc.

- Linde PLC

- Membrane Technology and Research Inc.

- Parker Hannifin Corp.

- SLB(schlumberger)

- Toray Industries Inc.

- UBE Corporation

第七章 市场机会与未来趋势

- 混合基质膜(MMM)的开发

- 聚合物薄膜应用领域的开发与拓展

The Gas Separation Membrane Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 2.63 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the gas separation membrane market. The pandemic disrupted the global supply chain, which affected the availability of raw materials, components, and equipment for manufacturing gas separation membranes. Delays in production and shipping led to temporary shortages of membrane systems and components. However, as countries gradually lifted lockdown restrictions, demand for gas separation membrane systems started to rebound.

Key Highlights

- The rising demand for membranes in carbon dioxide separation processes and strict government regulations for GHG emissions are expected to drive the gas separation membrane market.

- However, the plasticization of polymeric membranes in high-temperature applications and the upscaling and adoption of new membranes are expected to hamper the market growth of gas separation membranes.

- Furthermore, developing mixed matrix membranes (MMMs) and polymeric membranes with expanding applications is projected to provide new opportunities for the market studied.

- Asia-Pacific holds the largest share by geography in the market studied. It is expected to be the fastest-growing market over the forecast period due to the rising demand for gas separation membranes in China, India, and Japan.

Gas Separation Membrane Market Trends

The Nitrogen Generation and Oxygen Enrichment Segment to Dominate the Market

- Nitrogen generation and oxygen enrichment are essential processes in various industrial applications. Industries such as oil and gas, chemicals, electronics, food and beverage, and pharmaceuticals require nitrogen for blanketing, purging, inerting, and packaging. At the same time, oxygen enrichment is necessary for processes such as combustion, fermentation, and wastewater treatment.

- Nitrogen generation and oxygen enrichment using gas separation membranes enable onsite gas production, eliminating the need for transportation, storage, and handling of compressed or liquified gases. This reduces logistic costs, enhances supply chain reliability, and improves safety in industrial operations.

- Nitrogen is used in the food and beverage industry to displace oxygen in food packaging to extend the shelf life and preserve freshness. It is used to pressurize kegs and dispense carbonated beverages like beer and soda. In food processing operations, nitrogen is used for inerting, blanketing, cryogenic, and freezing.

- China's beer industry is also experiencing the quickest expansion globally, with its total revenue reaching about USD 131.5 billion by the close of 2023.

- Nitrogen and oxygen find applications in the electronics industry. Nitrogen is used as a carrier gas in semiconductor fabrication processes to prevent contamination and maintain precise atmospheric conditions. It is also used for wave soldering, reflow soldering, and conformal coating processes to improve soldering quality and prevent oxidation.

- According to the report released by the Semiconductor Industry Association, global semiconductor sales increased by 5.3 % year-to-year in November 2023.

- Oxygen enrichment is used in metallurgical processes such as steelmaking, iron smelting, and non-ferrous metal refining to increase combustion efficiency, reduce fuel consumption, and improve process productivity.

- Therefore, the demand for gas separation membranes is expected to increase and thus have a positive impact on the market studied.

Asia-Pacific to Dominate the Market

- Asia-Pacific is home to rapidly growing countries such as India, China, Japan, South Korea, and other Southeast Asian countries. These countries are experiencing significant industrial growth, driving demand for gas separation membrane technologies across various sectors, including oil and gas, chemicals, electronics, healthcare, and food and beverage.

- Asia-Pacific is a central manufacturing hub with a diverse range of industries producing chemicals, electronics, semiconductors, automobiles, and consumer goods. Gas separation membranes are essential components in many manufacturing processes, leading to high demand in the region.

- According to the World Steel Organization, in December 2023, China produced 67.4 metric tons of steel. Meanwhile, India has risen to become the second-largest producer of crude steel globally. The country exported 6.72 million metric tons of finished steel while only importing 6.02 million metric tons in the fiscal year 2022-23.

- Furthermore, according to the Semiconductor Association, in January 2024, China's semiconductor sales soared to USD 14.76 billion, marking a notable rise from the previous year. This is a considerable jump compared to the sales in January 2023, which stood at USD 11.66 billion.

- In addition, the demand for gas separation membranes in the region's acid gas separation market is expected to be stimulated by the rising energy production in this area.

Gas Separation Membrane Industry Overview

The gas separation membrane market is partially consolidated in nature, with a few major players dominating the market. The major companies operating in the market include Air Products and Chemicals Inc., UBE Corporation, Air Liquide Advanced Separations, DIC Corporation, and FUJIFILM Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Membranes in Carbon Dioxide Separation Processes

- 4.1.2 Strict Government Norms Toward GHG Emissions

- 4.2 Restraints

- 4.2.1 Plasticization of Polymeric Membranes in High-temperature Applications

- 4.2.2 Upscaling and Adoption of New Membranes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Polyimide and Polyamide

- 5.1.2 Polysulfone

- 5.1.3 Cellulose Acetate

- 5.1.4 Other Material Types (Nanostructured Membrane)

- 5.2 Application

- 5.2.1 Nitrogen Generation and Oxygen Enrichment

- 5.2.2 Hydrogen Recovery

- 5.2.3 Carbon Dioxide Removal

- 5.2.4 Removal of Hydrogen Sulphide

- 5.2.5 Other Applications (Carbonation)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide Advanced Separations

- 6.4.2 Air Products and Chemicals Inc.

- 6.4.3 DIC CORPORATION

- 6.4.4 Evonik Industries AG

- 6.4.5 FUJIFILM Corporation

- 6.4.6 GENERON

- 6.4.7 Honeywell International Inc.

- 6.4.8 Linde PLC

- 6.4.9 Membrane Technology and Research Inc.

- 6.4.10 Parker Hannifin Corp.

- 6.4.11 SLB (schlumberger)

- 6.4.12 Toray Industries Inc.

- 6.4.13 UBE Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Mixed Matrix Membranes (MMM)

- 7.2 Development in Polymeric Membranes and Expanding Applications

气体分离设备市场规模、份额和成长分析:按产品类型、技术类型、气体类型、产能、应用领域、最终用户和地区划分-2026-2033年产业预测

气体分离设备市场规模、份额和成长分析:按产品类型、技术类型、气体类型、产能、应用领域、最终用户和地区划分-2026-2033年产业预测 全球气体分离膜市场:机会与策略展望(至2034年)

全球气体分离膜市场:机会与策略展望(至2034年) 气体分离膜市场规模、份额及成长分析(依产品类型、材料类型、组件类型、应用、终端用户产业及地区划分)-2026-2033年产业预测

气体分离膜市场规模、份额及成长分析(依产品类型、材料类型、组件类型、应用、终端用户产业及地区划分)-2026-2033年产业预测 2026-2030年全球气体分离膜市场

2026-2030年全球气体分离膜市场 全碳二氧化碳分离膜市场按製程类型、膜配置、应用和最终用户划分,全球预测(2026-2032年)

全碳二氧化碳分离膜市场按製程类型、膜配置、应用和最终用户划分,全球预测(2026-2032年) 全球气体分离膜市场(按组件、材料类型、应用和地区划分)-预测(至2030年)气体分离膜市场:依材料、应用、技术和产业划分-全球预测,2025-2032年

全球气体分离膜市场(按组件、材料类型、应用和地区划分)-预测(至2030年)气体分离膜市场:依材料、应用、技术和产业划分-全球预测,2025-2032年 气体分离膜市场:全球产业分析、规模、份额、成长、趋势及预测(2025-2032)

气体分离膜市场:全球产业分析、规模、份额、成长、趋势及预测(2025-2032) 气体分离膜市场规模、份额、趋势分析报告:按产品、应用、最终用途、地区、细分市场预测,2025-2030 年天然气(气体)分离膜市场,规模,占有率,产业分析报告:各材料,模组,各用途,各地区-2025年~2034年市场预测

气体分离膜市场规模、份额、趋势分析报告:按产品、应用、最终用途、地区、细分市场预测,2025-2030 年天然气(气体)分离膜市场,规模,占有率,产业分析报告:各材料,模组,各用途,各地区-2025年~2034年市场预测