|

市场调查报告书

商品编码

1689976

乙太网路控制器:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Ethernet Controller - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

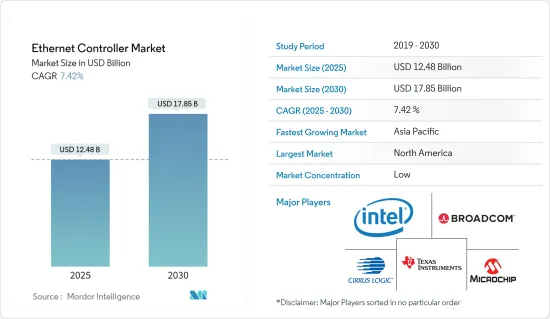

乙太网路控制器市场规模预计在 2025 年为 124.8 亿美元,预计到 2030 年将达到 178.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.42%。

现代数位经济中资料中心和云端运算的日益普及推动了市场的发展。从科学发现到人工智慧 (AI),现代资料中心对于解决世界上最大的挑战至关重要。这些现代资料中心正在进行转型,以增加网路频宽并优化人工智慧等工作负载。

资料量的增加推动了对乙太网路控制器的需求,从而促进了市场成长。根据爱立信行动报告,资料封包价格的下降和智慧型手机使用量的增加正在加速印度的资料流量。报告预测到2025年,行动资料流量将达到每月Exabyte以上。

控制自动化技术乙太网路(EtherCAT)基于 CANopen通讯协定和乙太网路。但与互联网或网路通讯不同的是,它针对工业自动化控制进行了最佳化。利用 OSI 网路模型,乙太网路和 EtherCAT 依赖相同的实体层和资料链结层。不仅如此,这两个网路针对不同的任务进行了最佳化,因此在设计上有所不同。

USB 转乙太网路转换器在多种情况下都很有用。例如,您可能会发现使用者笔记型电脑上的 Wi-Fi 选项遇到技术问题,或者使用者需要存取互联网,但发现出于安全原因某些位置已停用 Wi-Fi。在这些情况下,一个乙太网路连接埠和一个简单的适配器就足够了。

此类长期延期合约预计会使市场饱和并影响成长,从而为市场快速实施技术更新带来障碍。产业趋势要求解决方案和服务供应商应该使用乙太网路控制器等新兴技术,而长期合约可能会对市场产生反效果。此外,市场竞争加剧将影响现有供应商的利润率和成长。供应商之间的竞争水平非常激烈,乙太网路控制器产品在全球范围内正变得商品化。

由于需求出现意外波动,加上供应减少,一些零件製造商已加大产量,但仍不够。成长的主要动力是对全球经济数位化的持续投资、5G技术的推出以及对资料中心和云端服务的大力投资。随着 5G 智慧型手机的快速普及和云端运算的持续增强对高速连接的需求不断增加,预计未来几年市场将会成长。爱立信预计,2019 年至 2028 年间,全球整体5G 用户数将大幅成长,从 1,200 多万增至 45 亿多。

乙太网路控制器市场趋势

伺服器占最大市场占有率

- 大多数企业需要储存资料,例如电子邮件、网站、线上交易等,而这通常在伺服器上完成。伺服器是连接到公司本地网路或在大多数情况下连接到互联网的专用电脑。如果您的公司规模较小,您甚至可以将伺服器保留在公司内部并自行操作。但随着组织及其需求的成长,会产生更多的资料,需要更多的伺服器和储存空间。典型的资料中心基础设施包含许多伺服器,它们是功能强大的电脑。

- 伺服器为资料中心提供动力并支援云端环境,使伺服器产业成为无数关键任务企业和客户端运算业务的支柱。随着企业努力满足巨量资料和进阶工作负载要求,对更强大伺服器的需求持续成长。随着云端处理、人工智慧、巨量资料和资料中心的兴起,伺服器的需求也将大幅增加。随着伺服器需求的增加,乙太网路控制器的数量也随之增加。

- 基板管理控制器 (BMC) 监控大多数现代伺服器中的温度、电压和风扇。如果系统中某些事情需要管理员注意(例如 CPU 过热),BMC 通常会设定为传送通知(以电子邮件和/或 SNMP 警报的形式)。

- 英特尔乙太网路 800 系列控制器包括应用装置伫列 (ADQ)、动态装置个人化 (DDP) 以及对 iWARP 和 RoCEv2 远端直接记忆体存取 (RDMA) 的支援。它提供工作负载最佳化的效能和灵活性,以满足不断变化的网路需求。对于 NFV、储存、HPC-AI 和混合云端等高效能伺服器应用,800 系列控制器可提供高达 100GbE 的速度。

- 此外,NetXtreme-E系列BCM57414 50G PCIe 3.0乙太网路控制器基于Broadcom的可扩充10/25/50/100/200G乙太网路控制器架构。该架构旨在为企业和云端规模的网路和储存应用程式在伺服器中建构高度扩充性、功能丰富的网路解决方案,包括高效能运算、通讯、机器学习、储存分解和资料分析。

- 爱立信表示,到2030年,资料流量预计将成长两倍。到2023年,全球智慧型手机每月平均使用的行动资料将达到20.37千兆字节,高于前一年的15.93千兆位元组。预计这一数字将在 2024 年达到 25.17 GB,并在 2028 年达到 47.27 GB。因此,分散式云端将变得实用化,并提供轻鬆实现这种规模连接所需的低延迟和高频宽。一些科技巨头在管理其伺服器和运算需求时面临重大挑战。密集化的关键驱动因素是人工智慧资料分析的普及。

北美占有最大市场占有率

- 为了充分发挥5G的潜力,它需要灵活的网路和传输基础设施。随着乙太网路成为最有效的传输技术,通讯业者路由器和交换器被要求透过共用基础设施来支援各种使用案例,从而导致乙太网路设备的部署增加。

- 据爱立信称,预计2019年至2028年间,北美5G用户数将从107万多大幅成长至4.054亿多。随着美国5G产业的快速发展,市场对乙太网路控制器的需求也有望增加。

- 乙太网路控制器允许有线连接到电脑网络,因此任何需要高速互联网连接的设备都必须使用乙太网路控制器来实现高速互联网连接。云端基础设施网路就是一个例子。随着云端功能的发展和企业将业务转移到云端,美国对云端应用程式的需求正在迅速增长。

- 低成本、减少维护、资料安全和几乎无限的扩充性可能会导致未来几年更多企业选择云端储存解决方案。因此,云端运算和储存的成长也可能引发乙太网路控制器市场的激增。

- 加拿大先进的通讯研究中心通讯研究中心(CRC)致力于采用5G技术,让加拿大人能够使用尖端的通讯系统、技术和应用。根据 GSMA 预测,到 2030 年,5G 连线将占加拿大所有行动连线的 95%。

乙太网路控制器产业概览

乙太网路控制器市场高度分散,既有全球参与者,也有中小型企业。主要参与企业包括英特尔公司、博通公司、微晶片科技公司、Cirrus Logic 公司和德州仪器公司。市场参与企业正在采取联盟和收购等策略来加强其产品供应并获得永续的竞争优势。

2024 年 4 月,Microchip 收购 ADAS 和数位驾驶座连接领域的先驱 VSI,扩大了其车载网路足迹。此次市场收购将为 Microchip 广泛的乙太网路和 PCIe 车载网路产品系列添加 ASA Motion Link 技术,从而支援下一代软体定义汽车。

2024年3月,Marvell Technology Inc.与台积电合作推出业界领先的2奈米半导体技术平台,以满足高速基础设施需求。 Marvell 2 nm 平台提供了广泛的 IP 套件来满足许多基础设施需求。这包括超过 200Gbps 的高速长距离 SerDes、处理器子系统、加密引擎、系统晶片到晶片互连以及用于计算、记忆体、网路和储存的高频宽物理层介面。这些进步为开发客製化的云端优化运算加速器、乙太网路交换器、用于光学和铜互连的数位讯号处理器以及对人工智慧丛集、云端资料中心和类似高效能基础设施至关重要的其他设备奠定了基础。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 评估主要宏观经济趋势的影响

第五章 市场动态

- 市场驱动因素

- 采用EtherCat即时网路进行机器控制

- 采用USB乙太网路控制器

- 市场限制

- 受新冠疫情影响,需求下降

- 由于定价竞争激烈,利润空间较小

第六章 市场细分

- 频宽类型

- 快速以太网

- Gigabit乙太网

- 交换器以太网

- 按功能

- PHY(物理层)

- 一体化

- 按最终用户

- 伺服器

- 路由器/交换机

- 消费性电子应用

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 亚洲

- 印度

- 中国

- 日本

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Intel Corporation

- Broadcom Inc.

- Microchip Technology Inc.

- Cirrus Logic Inc.

- Texas Instruments Incorporated

- Silicon Laboratories Inc.

- Marvell Technology Group

- Realtek Semiconductor Corp.

- Cadence Design Systems Inc.

- Futurlec Inc.

第八章投资分析

第九章 市场机会与未来趋势

The Ethernet Controller Market size is estimated at USD 12.48 billion in 2025, and is expected to reach USD 17.85 billion by 2030, at a CAGR of 7.42% during the forecast period (2025-2030).

The increasing adoption of data centers and cloud computing in the modern digital economy drives the market. From scientific discoveries to artificial intelligence (AI), modern data centers are crucial to solving some of the world's most important challenges. These modern data centers are transforming to increase networking bandwidth and optimize workloads, like AI.

The increasing data volume heightened the need for Ethernet controllers, thereby driving the market's growth. According to the Ericsson Mobility Report, the decline in data packet charges and increased smartphone usage accelerated data traffic across India. The report estimates that the volume of mobile data traffic is expected to reach over 21 exabytes per month by 2025.

Ethernet for Control Automation Technology (EtherCAT) is based on the CANopen protocol and Ethernet. However, it differs from Internet or network communications in that it is specifically optimized for industrial automation control. Utilizing the OSI network model, Ethernet and EtherCAT rely on the same physical and data link layers. Beyond that, the two networks diverge by design as they are optimized for different tasks.

A USB-to-ethernet converter is useful in various circumstances. For example, a user's laptop's Wi-Fi option may be experiencing technical difficulties, or the user may discover that the Wi-Fi is disabled for security reasons in specific locations despite users requiring internet access. An Ethernet port and a simple adapter should suffice in such circumstances, as a cable will provide a faster and more consistent connection.

The market is expected to create a roadblock for itself to update faster on technology, as such long-duration contracts with extensions saturate the market, thus impacting its growth. When the industry trends indicate that the solution and service providers should use new and emerging technology, such as Ethernet controllers, long-term contracts can be counterproductive in the market. Moreover, the growing competition in the market impacts the profit margins and growth of the existing vendors. The level of competition between suppliers is so high that Ethernet controller products are transitioning to be commoditized in the world.

The unanticipated swing in demand with reduced supply led to the ramping of production by several component manufacturers, which still fell short. The primary drivers behind the growth are the continued investments in digitizing global economies, the deployment of 5G technologies, and the robust investments in data centers and cloud services. The market is expected to witness growth in the coming years, owing to the increase in the demand for high-speed connectivity, driven by the ongoing 5G smartphone ramp-up and the continued strength of the cloud. According to Ericsson, 5G subscriptions are forecast to increase drastically from 2019 to 2028 globally, from over 12 million to over 4.5 billion subscriptions, respectively.

Ethernet Controller Market Trends

Servers to Hold the Largest Market Share

- Most businesses require data storage, whether for their email, website, or online transactions, and this may be done on a server. Servers are specialized computers linked to a company's local network and, in most cases, the Internet. If a company is small enough, it may keep its servers in-house and run them independently. However, as organizations and their demands expand, more servers and storage space are required as more data is generated. A typical data center infrastructure includes many servers, which are powerful computers.

- As servers power data centers and support cloud environments, the server industry is the backbone of innumerable mission-critical and client-side corporate computing operations. As businesses seek to power big data and advanced workload requirements, demand for higher-performing servers continues to climb. With the increasing cloud computation, AI, big data, and data centers, the need for servers will also grow significantly. With this growing demand for servers, Ethernet controllers will also increase.

- A baseboard management controller (BMC) monitors most modern servers' temperature, voltages, and fans. When something in the system requires an administrator's attention (such as the CPU overheating), the BMC may generally be set to send out notifications (in the form of emails and SNMP alerts).

- Application device queues (ADQ), dynamic device personalization (DDP), and support for both iWARP and RoCEv2 Remote Direct Memory Access (RDMA) are included in Intel Ethernet 800 Series controllers. It provides workload-optimized performance and the flexibility to meet changing network requirements. For high-performance server applications, including NFV, storage, HPC-AI, and hybrid cloud, the 800 Series controllers provide speeds up to 100GbE.

- Further, the NetXtreme-E Series BCM57414 50G PCIe 3.0 Ethernet controller is based on Broadcom's scalable 10/25/50/100/200G Ethernet controller architecture. This architecture is designed to build highly scalable, feature-rich networking solutions in servers for enterprise and cloud-scale networking and storage applications, such as high-performance computing, telco, machine learning, storage disaggregation, and data analytics.

- According to Ericsson, the data traffic is expected to triple by 2030. In 2023, smartphones across the globe used an average of 20.37 gigabytes of mobile data per month, up from 15.93 gigabytes the previous year. This figure is expected to reach 25.17 gigabytes in 2024 and 47.27 gigabytes by 2028. Thus, the distributed cloud that can secure the low latency and high bandwidth required to connect such scale easily is coming into action. Several technology giants are addressing the critical challenges while managing their servers and computational needs. A major factor responsible for the rising densities is the rapid rise of data-crunching for AI.

North America Holds Largest Market Share

- 5G requires a flexible networking and transportation infrastructure to reach its full potential. As Ethernet becomes the most efficient transport technology, carrier routers and switches are being charged with supporting a range of use cases over shared infrastructure, increasing Ethernet gear installations.

- According to Ericsson, 5G subscriptions are predicted to increase drastically in North America from 2019 to 2028, from over 1.07 million to over 405.4 million. With such massive growth in the 5G industry in the United States, the market will also see demand for Ethernet controllers.

- As an Ethernet controller allows wired connections to a computer network, any device requiring a high-speed internet connection has to use Ethernet controllers for fast internet connections. Such is the case with cloud infrastructure networks. With developing cloud capabilities and enterprises shifting their work to the cloud, the demand for cloud applications is increasing rapidly in the United States.

- Due to low costs, less maintenance, data security, and almost unlimited scalability, more businesses will opt for cloud storage solutions in the coming years. Therefore, this rise in cloud computing and storage will also surge in the ethernet controller market.

- The Communications Research Centre (CRC), Canada's leading advanced telecommunications research center, is dedicated to bringing 5G technology to Canadians to ensure they can use state-of-the-art telecommunications systems, technologies, and applications. According to GSMA, by 2030, 5G connections are predicted to account for 95% of all mobile connections in Canada.

Ethernet Controller Industry Overview

The ethernet controller market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Intel Corporation, Broadcom Inc., Microchip Technology Inc., Cirrus Logic Inc., and Texas Instruments Incorporated. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In April 2024, Microchip acquired ADAS and Digital Cockpit Connectivity Pioneer VSI Co. Ltd to extend automotive networking. The market acquisition adds ASA Motion Link technology to Microchip's broad Ethernet and PCIe automotive networking portfolio to enable next-generation software-defined vehicles.

In March 2024, Marvell Technology Inc., in partnership with TSMC, unveiled the industry's pioneering 2 nm semiconductor technology platform, tailored for high-speed infrastructure demands. The Marvell 2 nm platform, an extensive IP suite, addresses many infrastructure needs. It includes high-speed long-reach SerDes exceeding 200 Gbps, processor subsystems, encryption engines, system-on-chip fabrics, chip-to-chip interconnects, and high-bandwidth physical layer interfaces for computing, memory, networking, and storage. These advancements form the cornerstone for developing bespoke cloud-optimized compute accelerators, Ethernet switches, digital signal processors for optical and copper interconnects, and other devices crucial for fueling AI clusters, cloud data centers, and similar high-performance infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of EtherCat for Realtime Network for Machine Control

- 5.1.2 Adoption of USB Ethernet Controllers

- 5.2 Market Restraints

- 5.2.1 Low Demand Due to Impact of COVID-19

- 5.2.2 Competitive Prices Led to Stiff Profit Margins

6 MARKET SEGMENTATION

- 6.1 By Bandwidth Type

- 6.1.1 Fast Ethernet

- 6.1.2 Gigabit Ethernet

- 6.1.3 Switch Ethernet

- 6.2 By Function

- 6.2.1 PHY (Physical Layer)

- 6.2.2 Integrated

- 6.3 By End Users

- 6.3.1 Servers

- 6.3.2 Routers and Switches

- 6.3.3 Consumer Applications

- 6.3.4 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Broadcom Inc.

- 7.1.3 Microchip Technology Inc.

- 7.1.4 Cirrus Logic Inc.

- 7.1.5 Texas Instruments Incorporated

- 7.1.6 Silicon Laboratories Inc.

- 7.1.7 Marvell Technology Group

- 7.1.8 Realtek Semiconductor Corp.

- 7.1.9 Cadence Design Systems Inc.

- 7.1.10 Futurlec Inc.