|

市场调查报告书

商品编码

1690073

汽车声学材料:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Automotive Acoustic Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

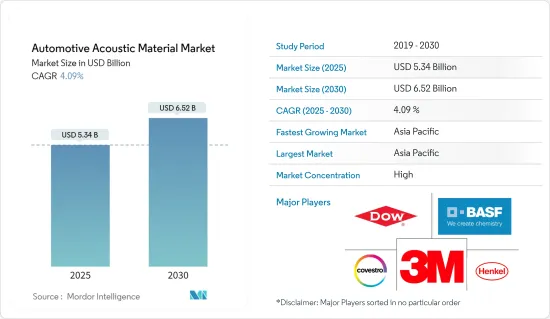

预计2025年汽车声学材料市场规模为53.4亿美元,到2030年预计将达到65.2亿美元,预测期内(2025-2030年)的复合年增长率为4.09%。

由于新冠疫情导致早期供应和生产中断,汽车产业正在经历需求衝击,且恢復期尚不清楚。一些OEM 的流动收入很差,因为他们无力降低固定成本。市值短缺和整合已经持续了相当长一段时间,削弱了某些参与者的实力,因为如果无法吸引新的投资,他们就面临破产的风险。

由于客製化和自动驾驶等趋势,汽车内装正在改变。业内公司正努力开发融合众多创新功能的汽车内装设计。

汽车音响作为现代汽车的品质元素正逐渐受到青睐,汽车製造商对此表现出浓厚的兴趣。在销售汽车时,乘客的舒适度是首要考虑因素之一。这些组件必须占用尽可能少的空间,同时仍提供最佳的舒适度。因此,这个领域正在不断进步。

由于它们通常用于行驶时受到振动的部件,例如引擎盖和仪表板绝缘体,因此汽车声学材料的售后市场预计会扩大。人们对跑车和豪华车的需求不断增长,以及改装古董车的日益流行,可能为汽车声学材料开闢巨大的市场。

除了经济放缓之外,声学材料和其他物品的进口税以及 COVID-19 疫情预计也会阻碍市场扩张。另一方面,声学材料价格波动和因环保问题导致的电动车需求增加预计将推动该行业的发展。

汽车声学材料市场趋势

高檔汽车的需求不断增加

随着豪华汽车需求的不断增长,豪华性和舒适性已成为製造商关注的重点。主要目标是将汽车的噪音水平保持在可接受的范围内。这样的噪音法规要求人们更加重视车辆音响系统。因此,预计未来几年汽车声学材料市场将会成长。

高檔汽车的扩张可能会推动全球对汽车声学材料的需求,因为它们可以改善内装外观并最大限度地减少车舱内的噪音、振动和声振粗糙度 (NVH)。

易于安装、能够完全填充车辆内部空腔的汽车吸音材料的出现预计将推动汽车吸音材料市场的需求。政府对公共交通的投资预计将推动汽车声学材料的需求。

製造商不断增加研发支出,以提高噪音吸收水平,推动了汽车声学材料市场的发展。具有吸收低频声音能力的复合材料越来越受欢迎。此外,製造商越来越注重为车辆的内部和外部提供卓越的颜色饰面,预计这将在整个预测期内促进市场成长。

许多製造商正在投资研发,以开发具有增强性能的材料。例如

- 2021 年 11 月,Autoneum 推出了一项以毛毡为基础的新技术:Flexi-Loft。 Flexi-Loft 是再生棉和功能纤维的独特混合物,可减轻产品重量并使其精确贴合复杂的形状。 Autoneum 已在全球范围内使用 Flexiloft 作为基于 Prime Light 技术的一系列地毯、内仪表板和其他声学组件的隔热材料。

亚太地区占主要市场占有率

亚太地区正成为最大的声学材料市场。 2021年,亚太地区占全球汽车产量的最大份额。该地区预计是汽车声学材料数量和金额最大的市场。该地区庞大的汽车产量为声学材料市场提供了巨大的成长机会。

中国是世界上最大的汽车市场。但近年来销量一直在下降。根据中国工业协会(CAAM)的数据,全球最大汽车市场 12 月销量年增 3.8%,2021 年总销量达 2,628 万辆。

过去几年里,中国各公司纷纷扩大生产设施并开设新生产设施。例如:

- 2021年10月,戴姆勒在北京正式启用全新的「戴姆勒中国研发技术中心」。工程总投资11亿元,研发技术中心总占地面积5.5万平方公尺。测试大楼内设有七个测试设施,包括 eDrive 实验室、充电实验室、挥发性有机化合物 (VOC) 实验室、底盘实验室、噪音、振动和声振粗糙度 (NVH) 实验室、引擎实验室和环境实验室。新测试大楼可同时容纳300余辆测试车辆。

欧洲是第二大乘用车市场,尤其是高级车市场。预计预测期内高檔汽车销量将呈线性增长,从而增加欧洲对声学材料的需求。

汽车声学材料产业概况

随着市场竞争日益激烈,各家公司纷纷建立新的策略伙伴关係,大力投资研发计划,并向市场推出新产品,以在竞争中脱颖而出。例如

- 2021年3月,帝人株式会社宣布,其聚酯三维成型吸音材料被丰田汽车公司的燃料电池车(FCV)「MIRAI」采用。它是一种用于降低燃料电池组内部氢气和空气发生化学反应时产生的噪音的材料,反应产生的水会从燃料电池组或排水管排放到车外。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 市场限制

- 波特五力分析

- 新进入者的威胁

- 购买者和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 材料

- 聚氨酯

- 纺织品

- 玻璃纤维

- 其他材料

- 车辆类型

- 搭乘用车

- 商用车

- 应用

- 阀罩衬里

- 车门饰件

- 其他用途

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 巴西

- 阿拉伯聯合大公国

- 其他国家

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- Dow Chemicals

- 3M Acoustics

- BASF SE

- Covestro

- Henkel Adhesive Technologies

- Lyondellbasell

- Sumitomo Riko

- Sika

- Toray Industries

- Huntsman

- Freudenberg Group

第七章 市场机会与未来趋势

The Automotive Acoustic Material Market size is estimated at USD 5.34 billion in 2025, and is expected to reach USD 6.52 billion by 2030, at a CAGR of 4.09% during the forecast period (2025-2030).

Following early supply and production interruptions as a result of the COVID-19 pandemic, the auto industry is undergoing a demand shock, with an unknown recovery period. Some OEMs have poor liquidity revenues due to a lack of room to minimize fixed expenses. Decreases in power due to a significant period of time of lacking in market capitalization and consolidation and without acquiring fresh investment, some players may risk going out of business.

Vehicle interiors are changing as a result of trends like customization and autonomous driving, in which the driver is increasingly becoming a passenger. Industry players are hard at work developing designs for car interiors that include a number of innovative features.

Car acoustics is slowly gaining popularity as a quality factor in current automobiles, and automakers are expressing a lot of interest in it. Passenger comfort has risen to the top of the priority list when it comes to selling a car. Components must occupy as little space as possible while providing optimal comfort. As a result, continuous progress is being made in this area.

Since they are used in numerous components such as the engine cover, dash insulator, and other components that are regularly vibrated when the car is driving, the aftermarket for automotive acoustic materials is expected to expand. The ever-increasing demand for sports and luxury vehicles and the growing popularity of modified antique cars may open up a large market for automotive acoustic materials.

The slowing economy, combined with taxes on importing acoustic materials and other items, and the COVID-19 pandemic are projected to hinder the market's expansion. On the other hand, price fluctuations in acoustic materials and the increased demand for electric vehicles due to environmental concerns are expected to drive the industry.

Automotive Acoustic Material Market Trends

Growing Demand for Premium Cars

Luxury and comfort have been a significant focus area for manufacturers, as the demand for premium cars has grown. The primary goal is to keep the vehicle's sound within acceptable limits. These noise restrictions need greater attention in the automobile acoustic system. As a result, the market for automotive acoustic materials is expected to grow in the future years.

As automotive acoustic materials provide the interior appearance and minimize noise, vibration, and harshness (NVH) in the cabin, the expansion of the premium cars is likely to fuel the demand for automotive acoustic materials globally.

The advent of automotive acoustic materials that are easy to install and extend to completely fill interior cavities in vehicles is projected to enhance the demand in the automotive acoustic material market. The government's investment in public transportation is expected to boost the demand for vehicle acoustic materials.

The growth in constant R&D spending by manufacturers to enhance noise-absorbing levels is driving the automotive acoustic materials market. Composite materials with the ability to absorb low-frequency sounds are gaining popularity. Furthermore, manufacturers' attention to providing exceptional color finishes for the interior and exterior appearance of cars is expected to contribute to market growth throughout the forecast period.

Many manufacturers are investing in R&D to develop materials with enhanced properties. For instance:

- In November 2021, Autoneum announced a new felt-based technology Flexi-Loft, which due to a unique blend of recycled cotton and functional fibers, reduces product weight and allows for accurate adaptation even to complex shapes. Autoneum is already using Flexi-Loft worldwide as an insulator for various carpets, inner dashes, and other acoustic components based on its Prime-Light technology.

Asia-Pacific Captures the Major Market Share

The Asia-Pacific region has emerged as the largest market for acoustic materials. Asia-Pacific accounted for the largest global vehicle production in 2021. The region is estimated to be the largest market for automotive acoustic materials, by volume and value. The huge vehicle production in the region offers a tremendous growth opportunity for the acoustic materials market.

China is the largest automobile market in the world. However, for the past few years, the country has been witnessing a decline in sales. Overall sales in the world's largest auto market increased by 3.8% year-on-year in December, bringing the total sales for 2021 to 26.28 million, according to figures from the China Association of Automobile Manufacturers (CAAM).

In the past few years, the country has seen various companies expanding their production facilities and opening new facilities. For instance:

- In October 2021, Daimler opened its new 'Daimler R&D Tech Center China' officially in Beijing. With a total investment of CNY 1.1 billion, the R&D tech center has a gross floor area of 55,000 m2. The test building is home to seven testing facilities, including an eDrive lab, a charging lab, a volatile organic compounds (VOC) lab, a chassis lab, a noise, vibration and harshness (NVH) lab, an engine lab, and an environmental lab. The new test building can accommodate more than 300 test vehicles at the same time.

Europe is the second-largest market for passenger cars, particularly for premium cars. The sale of premium cars is projected to show linear growth during the forecast period, thereby increasing the demand for acoustic materials in Europe.

Automotive Acoustic Material Industry Overview

The competition in the market is increasing as the companies are making new strategic partnerships, investing majorly in R&D projects, and launching new products in the market to be ahead of their rivals. For instance:

- In March 2021, Teijin Limited announced that its polyester three-dimensional molded sound-absorbing material had been adopted for Toyota Motor Corporation's fuel cell vehicle (FCV) "Mirai." It will be used as a material to reduce noise when hydrogen and air chemically react in the FC stack, and the generated water is discharged from the FC stack or drain pipe outside the vehicle.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Polyurethane

- 5.1.2 Textile

- 5.1.3 Fiberglass

- 5.1.4 Other Materials

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Application

- 5.3.1 Bonnet Liner

- 5.3.2 Door Trim

- 5.3.3 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Dow Chemicals

- 6.2.2 3M Acoustics

- 6.2.3 BASF SE

- 6.2.4 Covestro

- 6.2.5 Henkel Adhesive Technologies

- 6.2.6 Lyondellbasell

- 6.2.7 Sumitomo Riko

- 6.2.8 Sika

- 6.2.9 Toray Industries

- 6.2.10 Huntsman

- 6.2.11 Freudenberg Group