|

市场调查报告书

商品编码

1690142

英国资料中心 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)United Kingdom Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

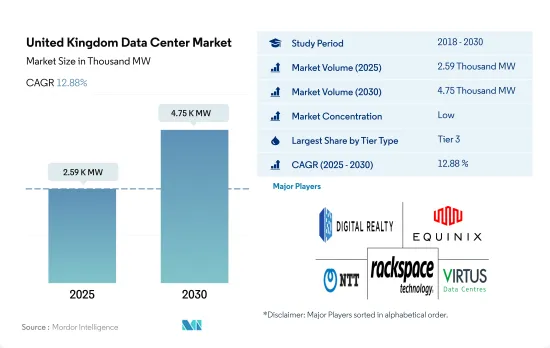

英国资料中心市场规模预计在 2025 年达到 2,590kW,预计到 2030 年将达到 4,750kW,复合年增长率为 12.88%。

预计 2025 年主机託管收益将达到 26.61 亿美元,2030 年将达到 67.995 亿美元,预测期内(2025-2030 年)的复合年增长率为 20.64%。

就容量而言,到 2023 年, 层级 3资料中心将占据大部分份额,预计在预测期内将继续占据主导地位。

- 3层级资料中心因具有现场协助、电力和冷却冗余等特点而最受欢迎。 2022 年, 层级 3 直流市场运作容量为 1,540.98 兆瓦。预测期间的预计容量预计将从 2023 年的 1,813.19 兆瓦成长到 2029 年的 3,369.24 兆瓦,复合年增长率为 10.88%。这些资料中心具有「可同时维护」的特点,其主要区别在于冗余组件。

- 中小型企业通常喜欢至少层级 3 级的系统,因为它提供的冗余保护要好得多。在英国,小型企业占企业总数的99.9%。据估计,到2022年初,英国私人企业数量将达到550万家。层级设施的广泛采用体现在批发和超大规模主机託管主要被 BFSI、电讯和媒体娱乐用户采用。截至 2022 年,全国约有 148 个层级资料中心,约有 28 个层级资料中心正在兴建中。

- 层级 4 因其容错能力强、停机时间短、执行时间高达 99.99% 而成为大型企业的下一个首选资料中心。预计云端运算和通讯领域的主要终端用户采用超大规模主机託管将在预测期内见证市场的成长潜力。英国政府的 G-Cloud 计画正在改变公共部门购买资讯和通讯技术的方式。 2022 年,该国拥有两座层级资料中心,分别由 Exascale Ltd 和 ServerMania 拥有。

- 1 级和 2 级资料中心是最不受欢迎的,因为它们是供电和冷却的单一途径,与 3 级和 4 级设施相比,预期运作为 99.671%(每年停机时间为 28.8 小时)。

英国资料中心市场趋势

智慧型手机普及率的提高以及 4G 和 5G 服务的出现将推动市场成长

- 预计到 2022 年,该国智慧型手机用户数将达到 6,346 万,到 2029 年将达到 6,800 万,预测期内的复合年增长率为 1.01%。

- 英国智慧型手机普及率逐年上升,预计2022年将达到93%。在16-24岁族群中,2022年的智慧型手机拥有率为99%。英国行动网路用户数已达6,230万,预计随着4G和5G的出现,这一数字将成长约286万,到2026年将超过6,500万。此外,自新冠疫情爆发以来,人们增加了智慧型手机的使用,并在网路游戏和媒体串流平台上花费了更多时间。因此,2020年4月,该产业将个人非接触式卡片付款的消费限额从30英镑提高到45英镑,以支持线上付款。这种情况导致智慧型手机的普及率不断提高,并且这种情况持续至今。

- 用户数量的增加带动了资料中心市场的需求。这一成长是由电子商务、媒体娱乐和 BFSI 领域的成长所推动的,这些领域产生了大量资料。智慧型手机需要即时处理大量资料,这需要资料中心进行储存。在智慧型手机普及率从 2017 年的 72% 成长到 2022 年的 90% 以上的历史时期内,资料中心机架的数量从 2017 年的约 215,000 个增加到 2022 年的 388,000 个。预计这一趋势将在预测期内持续下去。

2G 和 3G 的逐步淘汰以及 4G 和 5G 网路的采用,以及行动装置使用量的增加,将推动市场成长

- 英国首个 5G 网路于 2019 年 5 月运作,4G 网路于 2012 年 10 月推出。自运作以来,这两个网路的资料通讯速度都有所提升。 4G通讯速度已从 2012 年的 12Mbps 提升至 2022 年的 36.40Mbps。同样,5G 速度也从 2019 年的 139.5 Mbps 提升至 2022 年的 160.15 Mbps。根据 2022 年 5 月的一项行业调查,在英国(英国),约 67% 的受访者在智慧型手机上使用 4G 服务,约 25% 的受访者正在使用 5G 服务。

- 英国将在2033年前逐步淘汰2G和3G行动服务。所有通讯业者的一项关键策略是关闭其2G和3G网络,并将投资和频谱资源集中在进一步改善4G客户体验,同时推出5G。英国政府承诺支持1.1亿英镑(1.35亿美元)的投资,以加速5G和6G的发展。此外,还与行动网路营运商沃达丰、EE、维珍媒体、O2 和 Three 就 2G 和 3G 转换日期达成了一致。

- 更高的速度和整体改善的连接性也为其他终端用户产业铺平了道路。 2021 年,英国用户平均每天在行动装置上花费四个小时。这比 2020 年增加了 0.3 小时。 2022 年初英国社群媒体用户数量占总人口的 84.3%,2021 年至 2022 年间增加了 460 万人。总体而言,这将提高行动资料速度,增加资料流量,从而增加资料中心存储和处理资料的需求。

英国资料中心产业概况

英国资料中心市场较为分散,前五大公司占34.50%的市占率。该市场的主要企业包括 Digital Realty Trust Inc.、Equinix Inc.、NTT Ltd、Rackspace Technology Inc. 和 Virtus Data Centres Properties Ltd (STT GDC)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 市场展望

- 负载能力

- 占地面积

- 主机代管收入

- 安装的机架数量

- 机架空间利用率

- 海底电缆

第五章 产业主要趋势

- 智慧型手机用户数量

- 每部智慧型手机的资料流量

- 行动资料速度

- 宽频资料速度

- 光纤连接网路

- 法律规范

- 英国

- 价值炼和通路分析

第六章市场区隔

- 热点

- 伦敦

- 其他中东和非洲地区

- 资料中心规模

- 大规模

- 超大规模

- 中等规模

- 超大规模

- 小规模

- 层级类型

- 1层级和2级

- 层级

- 层级

- 吸收量

- 未使用

- 使用

- 按主机託管类型

- 超大规模

- 零售

- 批发的

- 按最终用户

- BFSI

- 云

- 电子商务

- 政府

- 製造业

- 媒体与娱乐

- 电信

- 其他的

第七章竞争格局

- 市场占有率分析

- 商业状况

- 公司简介.

- Colt Technology Services

- CyrusOne Inc.

- Digital Realty Trust Inc.

- Equinix Inc.

- Global Switch Holdings Limited

- Global Technical Realty SARL

- Kao Data Ltd

- NTT Ltd

- Rackspace Technology Inc.

- Telehouse(KDDI Corporation)

- Vantage Data Centers LLC

- Virtus Data Centres Properties Ltd(STT GDC)

第八章:CEO面临的关键策略问题

第九章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 全球市场规模和DRO

- 资讯来源及延伸阅读

- 图表清单

- 关键见解

- 资料包

- 词彙表

The United Kingdom Data Center Market size is estimated at 2.59 thousand MW in 2025, and is expected to reach 4.75 thousand MW by 2030, growing at a CAGR of 12.88%. Further, the market is expected to generate colocation revenue of USD 2,661 Million in 2025 and is projected to reach USD 6,799.5 Million by 2030, growing at a CAGR of 20.64% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, it will continue its dominance during forecast period

- Tier 3 data centers are the most preferred due to features such as onsite assistance, power, and cooling redundancy. The Tier 3 DC market was operating at 1540.98 MW in 2022. The expected capacity during the forecast period is expected to grow from 1813.19 MW in 2023 to 3369.24 MW in 2029 at a CAGR of 10.88%. These data centers are 'concurrently maintainable' with redundant components as a key differentiator.

- SMBs generally prefer to use at least a tier III-rated system for the far superior redundancy protections offered. In the United Kingdom, SMEs account for 99.9% of the business population. At the start of 2022, there were estimated to be 5.5 million businesses in the UK private sector. Major adoption of tier 3 facilities is reflected in BFSI, telecom, and media and entertainment users are majorly adopting wholesale and hyperscale colocation. As of 2022, there are around 148 Tier 3 data centers in the country, and around 28 upcoming data centers are under construction with Tier 3 standards.

- Tier 4 is the next most preferred data centers by large enterprises due to their fault-tolerant functionality, lower downtime, and 99.99% uptime. It is expected that the market will showcase potential growth during the forecast period with the adoption of hyperscale colocation by major end users in the cloud and telecom sectors. The UK government's G-Cloud program is changing the way public sector organizations purchase information and communications technology. In 2022, the country had two Tier 4 data centers owned by Exascale Ltd and ServerMania.

- The Tier 1&2 data centers are the least preferred due to their single path for power and cooling and providing expected uptime of 99.671% (28.8 hours of downtime annually) when compared to Tier 3 and Tier 4 facilities.

United Kingdom Data Center Market Trends

Increase smartphone penetration rate, emergence of 4G and 5G services to boost market growth

- The number of smartphone users in the country was 63.46 million in 2022 and is expected to witness a CAGR of 1.01% during the forecast period to reach a value of 68 million by 2029.

- The smartphone penetration rate in the United Kingdom has increased each year, reaching an overall figure of 93% in 2022. Among the age group of 16-24, the smartphone ownership rate was 99% in 2022. The number of mobile internet users in the United Kingdom reached 62.3 million, a figure which is projected to increase by approximately 2.86 million and amount to over 65 million by 2026 with the emergence of 4G and 5G. Further, since the COVID-19 pandemic hit, people have increased their smartphone usage and spent more time on online gaming or media streaming platforms. As a result, in April 2020, the industry increased the spending limit on individual contactless card payments from GBP 30 to GBP 45 to help with online payments. Such a scenario has increased smartphone penetration and is currently following the same trend.

- The growth of the user base positively boosted the market demand for data centers. The increasing rate has positively upheld its growth in the e-commerce, media and entertainment, and BFSI sectors, where a large chunk of data has been generated. Since smartphones necessitate real-time processing on having a large data chunk, they mostly require a data center for storage. During the historical period, when smartphone usage penetration increased from 72% in 2017 to more than 90% in 2022, the number of racks in the data center increased from around 215k in 2017 to 388k in 2022. This trend is further expected to be witnessed during the forecast period.

Phase out of 2G and 3G and adoption of 4G and 5G network and increase in use of mobile devices to drive market growth

- The United Kingdom's first 5G network was activated in May 2019, and 4G was launched in October 2012. Since being commissioned, both networks have shown an increment in their data speed. 4G speed increased from 12 Mbps in 2012 to 36.40 Mbps in 2022. Similarly, 5G speed increased from 139.5 Mbps in 2019 to 160.15 Mbps in 2022. In May 2022, according to an industry survey, around 67% of respondents in the United Kingdom (UK) had a 4G service on their smartphone, while about 25% had a 5G service.

- The UK will phase out 2G and 3G mobile services by 2033. The major strategy for all the operators is to turn off their 2G and 3G networks, allowing them to focus investments and spectrum resources on further improving the 4G customer experience while rolling out 5G. The UK government has outlined its intentions to invest in driving 5G and 6G development with the support of GBP 110 million (USD 135 million) worth of investment. Moreover, the switch-off date for 2G and 3G has been agreed upon with mobile-network operators Vodafone, EE, Virgin Media, O2, and Three.

- The growth in speed and better overall connectivity is paving the way for other end-user industries. In 2021, users in the United Kingdom spent an average of four hours per day using their mobile devices. This was an increase of 0.3 hours up from 2020. The number of social media users in the United Kingdom at the start of 2022 was equivalent to 84.3% of the total population, and it increased by 4.6 million between 2021 and 2022. Overall, this will increase the mobile data speed, increasing the data traffic, which thereby requires data centers for storing and processing data.

United Kingdom Data Center Industry Overview

The United Kingdom Data Center Market is fragmented, with the top five companies occupying 34.50%. The major players in this market are Digital Realty Trust Inc., Equinix Inc., NTT Ltd, Rackspace Technology Inc. and Virtus Data Centres Properties Ltd (STT GDC) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 MARKET OUTLOOK

- 4.1 It Load Capacity

- 4.2 Raised Floor Space

- 4.3 Colocation Revenue

- 4.4 Installed Racks

- 4.5 Rack Space Utilization

- 4.6 Submarine Cable

5 Key Industry Trends

- 5.1 Smartphone Users

- 5.2 Data Traffic Per Smartphone

- 5.3 Mobile Data Speed

- 5.4 Broadband Data Speed

- 5.5 Fiber Connectivity Network

- 5.6 Regulatory Framework

- 5.6.1 United Kingdom

- 5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

- 6.1 Hotspot

- 6.1.1 London

- 6.1.2 Rest of United Kingdom

- 6.2 Data Center Size

- 6.2.1 Large

- 6.2.2 Massive

- 6.2.3 Medium

- 6.2.4 Mega

- 6.2.5 Small

- 6.3 Tier Type

- 6.3.1 Tier 1 and 2

- 6.3.2 Tier 3

- 6.3.3 Tier 4

- 6.4 Absorption

- 6.4.1 Non-Utilized

- 6.4.2 Utilized

- 6.4.2.1 By Colocation Type

- 6.4.2.1.1 Hyperscale

- 6.4.2.1.2 Retail

- 6.4.2.1.3 Wholesale

- 6.4.2.2 By End User

- 6.4.2.2.1 BFSI

- 6.4.2.2.2 Cloud

- 6.4.2.2.3 E-Commerce

- 6.4.2.2.4 Government

- 6.4.2.2.5 Manufacturing

- 6.4.2.2.6 Media & Entertainment

- 6.4.2.2.7 Telecom

- 6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Landscape

- 7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.3.1 Colt Technology Services

- 7.3.2 CyrusOne Inc.

- 7.3.3 Digital Realty Trust Inc.

- 7.3.4 Equinix Inc.

- 7.3.5 Global Switch Holdings Limited

- 7.3.6 Global Technical Realty SARL

- 7.3.7 Kao Data Ltd

- 7.3.8 NTT Ltd

- 7.3.9 Rackspace Technology Inc.

- 7.3.10 Telehouse (KDDI Corporation)

- 7.3.11 Vantage Data Centers LLC

- 7.3.12 Virtus Data Centres Properties Ltd (STT GDC)

- 7.4 LIST OF COMPANIES STUDIED

8 KEY STRATEGIC QUESTIONS FOR DATA CENTER CEOS

9 APPENDIX

- 9.1 Global Overview

- 9.1.1 Overview

- 9.1.2 Porter's Five Forces Framework

- 9.1.3 Global Value Chain Analysis

- 9.1.4 Global Market Size and DROs

- 9.2 Sources & References

- 9.3 List of Tables & Figures

- 9.4 Primary Insights

- 9.5 Data Pack

- 9.6 Glossary of Terms

2025年资讯中心外包全球市场报告

2025年资讯中心外包全球市场报告 资料中心备用电源 HVO 的全球和区域市场:HVO 製造商、供应商、发电机製造商和资料中心营运商的分析和预测(2025-2034 年)

资料中心备用电源 HVO 的全球和区域市场:HVO 製造商、供应商、发电机製造商和资料中心营运商的分析和预测(2025-2034 年) 资料中心维修市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、模组、安装类型

资料中心维修市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、模组、安装类型 资料中心资产管理的全球市场:各零件,各部署模式,各用途,各终端用户业界,各地区,机会,预测,2018年~2032年

资料中心资产管理的全球市场:各零件,各部署模式,各用途,各终端用户业界,各地区,机会,预测,2018年~2032年 资料中心用水的美国市场:市场趋势,机会,预测(2025年~2030年)AI资料中心的全球市场:各零件,资料中心类别,各部署,各终端用户业界,各地区,机会,预测,2018年~2032年

资料中心用水的美国市场:市场趋势,机会,预测(2025年~2030年)AI资料中心的全球市场:各零件,资料中心类别,各部署,各终端用户业界,各地区,机会,预测,2018年~2032年 全球资料中心部署支出市场:市场规模(按资料中心类型、最终用户和地区划分)、未来预测资讯中心外包市场规模、份额、按服务类型、部署类型、企业规模、最终用途、地区、细分预测的趋势分析,2025 年至 2030 年全球资料中心能源储存市场规模依资料中心类型、最终用户、地区和预测:资料中心市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、模组、功能

全球资料中心部署支出市场:市场规模(按资料中心类型、最终用户和地区划分)、未来预测资讯中心外包市场规模、份额、按服务类型、部署类型、企业规模、最终用途、地区、细分预测的趋势分析,2025 年至 2030 年全球资料中心能源储存市场规模依资料中心类型、最终用户、地区和预测:资料中心市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户、模组、功能