|

市场调查报告书

商品编码

1690194

车载充电器:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Automotive On-board Charger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

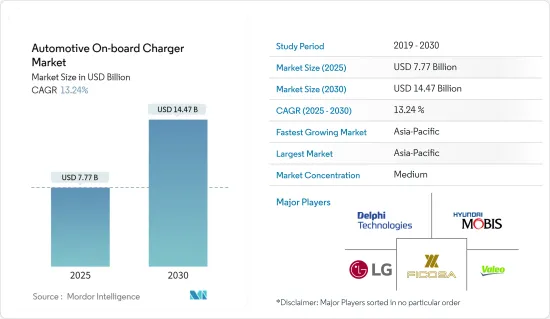

预计 2025 年汽车车载充电器市场规模为 77.7 亿美元,到 2030 年将达到 144.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 13.24%。

从长远来看,电动车的快速销售、电池技术的进步、充电基础设施的改善以及严格的排放法规预计将推动车载充电器的需求。电动车在已开发国家越来越受欢迎。电动车行业领导者和新兴企业计划在未来几年推出新的电动车车型。

根据国际能源总署(IEA)的数据,2022 年全球电池式电动车销量将达到 730 万辆,而 2021 年为 460 万辆,2022与前一年同期比较增 30.3%。

美国政府承诺在2030年将温室气体排放在2005年的基础上减少50-52%。政府已宣布2050年实现净零经济的目标。

随着高功率商用车投入市场,适合整合到这些车辆中的先进车载充电器的需求激增。因此,一些製造商采用了加入双车载充电器的策略来提高这些车辆的效率并有助于降低车载充电器的成本。随着电动车推进技术日益普及,全球对车载充电器的需求预计将会增加。

然而,车载充电器成本较高,对市场参与者构成了重大挑战。为了解决高成本的问题,市场上的各种参与者正在开发先进的技术来降低这些充电器的成本。为了满足电动车买家的大量需求,一些OEM正在推出配备快速充电技术的汽车以缩短充电时间,预计这将在预测期内对车载充电器的需求产生积极影响。未来几年,由于都市化进程加快、人均可支配收入增加以及消费者偏好转向新能源汽车,预计亚太地区将呈现快速成长。

汽车车用充电器市场趋势

乘用车领域引领车用充电器市场

在政府积极推动交通运输业脱碳以及消费者对新能源汽车偏好转变的推动下,电动乘用车的普及近年来迅速增长。随着越来越多的消费者倾向于使用乘用车,对整合到乘用车中以提高其充电效率的组件(例如先进的车载充电器)的需求将显着增加。

根据印度电动车製造商协会 (SMEV) 的数据,印度 2024 财年的电动四轮车销量预计将达到 88,114 辆,而 2023 财年为 47,499与前一年同期比较,2023 财年和 2024 财年的年成长率为 85.5%。

2023 年第一季度,美国电池式电动车销量为 258,800 辆,而 2022 年第一季为 226,700 辆,与 2022 年第四季相比,2023 年第一季环比成长 14.1%。

在全球范围内,对开发电动车充电基础设施的投资不断增加,以帮助促进从汽油/柴油汽车到电动车的平稳过渡。消费者需要大量的公共电动车充电站,以确保他们的旅行不会因汽车电量不足而受到影响。因此,世界各国政府都在投资建造电动车充电网络,这将有助于未来几年乘用车车载充电器的快速成长。

美国政府于 2024 年 1 月宣布计划投资 6.23 亿美元,加速在全国推出一系列电动车充电站,以补充交通运输部门的脱碳努力。该政府表示,将透过向全国 22 个州提供津贴金的方式,改善充电基础设施,包括在奥勒冈州部署快速充电器,在德克萨斯州为货运卡车部署氢燃料充电器。

例如,英国计划在2040年之前禁止销售所有汽油和柴油汽车。印度政府计划在2027年之前考虑在所有城市禁止柴油汽车。挪威等其他欧洲国家已经建立了框架,到2025年只销售零燃烧汽车。各国政府正在製定全面的策略来推动二氧化碳排放,这将导致电动乘用车销量增加,对车载充电器市场的需求产生正面影响。

亚太地区可望引领汽车车用充电器市场

亚太地区是电动车产业的中心,由于原材料低成本,预计将引领车载充电器市场。

电动车製造商数量众多,人口不断成长,政府也参与其中。因此,随着中国、印度和日本等国家的电动乘用车和商用车产业的扩张,预计未来几年亚太地区的车载充电器市场将快速成长。

根据中国工业协会(CAAM)的数据,2023 年 7 月商用纯电动车(BEV)月销量达到 38,000 辆,而 2023 年 6 月为 33,000 辆,6 月至 7 月环比增长 15.1%。

根据日本汽车检查登记资讯协会的数据,2023 年日本投入使用的纯电动车数量将达到 162,390 辆,而 2022 年为 138,330 辆, 与前一年同期比较同比增长 17.3%。

该地区有多家汽车製造商提供相容的电动车,例如比亚迪和塔塔汽车,这也有助于扩大电动车市场并推动车载充电器的需求。该地区的商业车队营运商,例如物流和最后一哩配送服务公司,越来越倾向于在其车队中部署电动货车和卡车,以配合政府减少碳排放的努力。预计未来几年将部署大量卡车和货车,这可能会增加亚太地区对车载充电器的需求。

由于电动车持有的不断增加和建立电动车製造中心的优惠政策,中国有望主导亚太车载充电器市场。该国可选的电动车充电基础设施也有望促进电动车的普及,这将对未来几年车载充电器的需求产生积极影响。

汽车车用充电器产业概况

由于生态系统中存在多家国际製造商,车载充电器市场分散且竞争激烈。主要参与者包括德尔福科技 (BorgWarner Inc)、现代摩比斯、LG 公司、意法半导体、Ficosa International SA、法雷奥 SE、丰田自动织机公司和 Bel Fuse Inc. 随着各种新型电动车型进入市场,车载充电器製造商正在透过与其他参与者建立战略联盟并推出新的车载充电器来扩大其影响力。

2023 年 11 月,博格华纳宣布与目标商标产品製造商 (OEM) 建立合作伙伴关係,为该OEM生产的乘用车型供应双向 800V 车载充电器 (OBC)。该公司表示,其车用充电器采用碳化硅电源开关,以提高车辆效率并改善电源转换和安全合规性。

2023 年 6 月,雷诺和 Mobilize 宣布合作,为雷诺生产的 Model 5 车款配备 R5 双向车用充电器。 Mobilize 表示,其双向充电器、双向充电站和 V2G 服务将帮助客户降低充电成本,因为该技术有助于将电力送回电网。

车载充电器市场预计将见证大量研发投入,以整合先进技术,提高电动车的效率并缩短电动乘用车和商用车的充电时间。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 政府大力推广电动车,推动市场成长

- 市场限制

- 车载充电器高成本阻碍因素市场成长

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 按车型

- 搭乘用车

- 商用车

- 按动力传动系统

- 纯电动车 (BEV)

- 插电式混合动力汽车(PHEV)

- 按额定输出

- 小于 3.3 千瓦

- 3.3~11 kW

- 11kW 或以上

- 按销售管道

- 目的地设备製造商(OEM)

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 巴西

- 墨西哥

- 阿拉伯聯合大公国

- 其他国家

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 公司简介

- Delphi Technologies(BorgWarner Inc.)

- Hyundai Mobis

- LG Corporation

- STMicroelectronics

- Ficosa International SA

- Valeo SE

- Delta Energy Systems AG

- Toyota Industries Corporation

- Brusa Elektronik AG

- VisIC Technologies Ltd

- Bel Fuse Inc.

第七章 市场机会与未来趋势

- 车载充电器技术的快速改进推动市场需求

第八章 供应商资讯

The Automotive On-board Charger Market size is estimated at USD 7.77 billion in 2025, and is expected to reach USD 14.47 billion by 2030, at a CAGR of 13.24% during the forecast period (2025-2030).

Over the long term, rapid sales of electric vehicles, advancements in battery technology, improving charging infrastructure, and stringent emission regulations are expected to fuel the demand for automotive on board chargers. The market has been witnessing the adaptation of electric passenger vehicles in developed countries. Major players and new start-ups in the EV industry plan to introduce new electric models in the coming years.

As per the International Energy Agency (IEA), battery electric vehicle sales worldwide touched 7.3 million units in 2022 compared to 4.6 million units in 2021, representing a Y-o-Y growth of 30.3% between 2021 and 2022.

The US government committed to reducing greenhouse gas emissions 50-52% below 2005 levels in 2030. The government announced its target to achieve a net-zero economy by 2050.

With the introduction of high-power commercial vehicles in the market, there is a massive demand for advanced on board chargers suitable for integration into these vehicles. Thus, several manufacturers are strategizing to incorporate dual on board chargers that improve the efficiency of these vehicles and help reduce the cost of the on board chargers. With the growing electric vehicle propulsion technology penetration in the coming years, the demand for on board chargers worldwide will increase.

However, the high cost of on board chargers imposes a significant challenge for players in the market. To tackle the issue of high costs, various players in the market are developing advanced technologies to reduce the cost of these chargers. To keep up with the high demand from buyers for electric vehicles, several OEMs are introducing cars with fast charging technologies to reduce the charging time, which will positively impact the demand for on board chargers during the forecast period. In the coming years, Asia-Pacific is expected to showcase surging growth owing to the rapid urbanization rate, increasing per capita disposable income, and the consumer preference shifting toward the adoption of new-energy vehicles.

Automotive On-board Charger Market Trends

The Passenger Cars Segment is Leading the On Board Charger Market

The penetration of electric passenger cars rapidly increased in recent years, owing to the government's aggressive push toward decarbonizing the transportation sector and consumers' shifting preference toward the adoption of new-energy vehicles. As more consumers are inclined to adopting passenger cars, the demand for components integrated into these cars, such as advanced on board chargers, to improve the charging efficiency of these cars will significantly increase.

As per the Society of Manufacturers of Electric Vehicles (SMEV), the electric four-wheeler sales in India touched 88,114 units in FY 2024 compared to 47,499 units in FY 2023, representing a Y-o-Y growth of 85.5% between FY 2023 and FY 2024.

The battery electric vehicle sales in the United States touched 258.8 thousand units in Q1 2023 compared to 226.7 thousand units in Q4 2022, recording a Q-o-Q growth of 14.1% between Q4 2022 and Q1 2023.

The rising investments in developing EV charging infrastructure globally are assisting the smooth transition from gasoline/diesel cars to electric cars. Consumers need to deploy many public EV charging stations so that their travel is not impacted due to the lack of charge in their vehicles. Hence, governments worldwide are investing in funding to develop the EV charging network, which, in turn, will contribute to the surging growth of on board chargers for passenger cars in the coming years.

In January 2024, the US government announced its plan to invest USD 623 million to foster the deployment of various electric vehicle charging points across the country, complementing its effort to decarbonize the transportation sector. The government stated that this funding will be disbursed through grants to 22 states nationwide to improve charging infrastructure, such as the deployment of rapid chargers in Oregon and hydrogen fuel chargers for freight trucks in Texas.

Globally, governments of many countries plan to promote green mobility by banning diesel vehicles and providing incentives to EV buyers; for instance, the United Kingdom plans to ban sales of all types of gasoline and diesel engine cars by 2040. The Government of India plans to consider a proposal to ban diesel vehicles from all Indian cities by 2027. Other European countries, such as Norway, are already establishing a framework to sell only zero-combustion cars by 2025. The comprehensive strategies being established by the governments to promote the reduction of carbon emissions are leading to increasing sales of electric passenger cars, which, in turn, is positively contributing to the demand for on board chargers in the market.

Asia-Pacific Is Expected to Lead the Automotive On Board Charger Market

Asia-Pacific is expected to lead the automotive on board charger market as it is the hub of the electric vehicle industry owing to the availability of lower-priced raw materials,

numerous electric vehicle manufacturers, growing population, and government participation. Therefore, with the expanding electric passenger cars and commercial vehicles industry in countries such as China, India, and Japan, the market for on board chargers is expected to showcase a rapid surge in the coming years across the Asia-Pacific.

As per the China Association of Automobile Manufacturers (CAAM), the monthly sales of commercial battery electric vehicles (BEVs) touched 38.000 in July 2023 compared to 33,000 units in June 2023, representing an M-o-M growth of 15.1% between June and July 2023.

According to the Japanese Automobile Inspection & Registration Information Association, the number of battery electric cars in use in Japan stood at 162.39 thousand units in 2023 compared to 138.33 thousand units in 2022, recording a Y-o-Y growth of 17.3% between 2022 and 2023.

The presence of several auto manufacturers in the region, such as BYD and Tata Motors, among others, involved in offering compatible electric vehicles is also leading in expanding the EV market, thereby fuelling the demand for on board chargers. Commercial fleet operators in the region, such as logistics and last-mile delivery service companies, are increasingly preferring to deploy electric vans and trucks in their fleet to complement the government's effort in reducing carbon emissions. With the deployment of a large number of trucks and vans expected in the coming years, the demand for on board chargers across the Asia-Pacific will increase during the forest period.

China is expected to dominate the on board chargers market in Asia-Pacific, owing to its growing electric vehicle parc and favorable policies toward establishing an EV manufacturing hub. The country's optional EV charging infrastructure is also expected to contribute to a greater adoption of EVs, which, in turn, will positively impact the demand for on board chargers in the coming years.

Automotive On-board Charger Industry Overview

The on board charger market is fragmented and highly competitive due to the presence of various international manufacturers operating in the ecosystem. Some of the major players include Delphi Technologies (BorgWarner Inc.), Hyundai Mobis, LG Corporation, STMicroelectronics, Ficosa International S.A., Valeo SE, Toyota Industries Corporation, and Bel Fuse Inc., among others. With the entry of various new electric models in the market, on board charger companies are expanding their presence by forming strategic alliances with other players and launching new automotive on board chargers.

In November 2023, BorgWarner announced its partnership with a North American-based original equipment manufacturer (OEM) to supply its bi-directional 800V Onboard Charger (OBC) for the passenger vehicle models manufactured by the OEM. The company stated that its on board chargers are equipped with silicon carbide power switches to enhance the efficiency of the vehicle and improve power conversion and safety compliance.

In June 2023, Renault and Mobilize announced its partnership to incorporate the R5's bi-directional onboard chargers into the model 5 manufactured by Renault. Mobilize stated that its bi-directional chargers, bidirectional charging station, and V2G service will assist customers reduce their charging costs since this technology helps send back electricity to the power grid.

The on board charger market is anticipated to witness massive investments in research and development to integrate advanced technology to improve the efficiency of electric vehicles and reduce the time to charge electric passenger cars or commercial vehicles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Aggressive Government Focus to Promote the Adoption of Electric Vehicles Fosters the Growth of the Market

- 4.2 Market Restraints

- 4.2.1 High Cost of On Board Chargers Hampers the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD and Volume - Units)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Powertrain Type

- 5.2.1 Battery Electric Vehicles (BEVs)

- 5.2.2 Plug-In Hybrid Electric Vehicles (PHEVs)

- 5.3 By Power Rating

- 5.3.1 Less than 3.3 kW

- 5.3.2 3.3-11 kW

- 5.3.3 More than 11 kW

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Delphi Technologies (BorgWarner Inc.)

- 6.2.2 Hyundai Mobis

- 6.2.3 LG Corporation

- 6.2.4 STMicroelectronics

- 6.2.5 Ficosa International S.A.

- 6.2.6 Valeo SE

- 6.2.7 Delta Energy Systems AG

- 6.2.8 Toyota Industries Corporation

- 6.2.9 Brusa Elektronik AG

- 6.2.10 VisIC Technologies Ltd

- 6.2.11 Bel Fuse Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Enhancement in On Board Charger Technology to Fuel the Market Demand

8 SUPPLIER INFORMATION

2025年双向车用电池充电器市场报告

2025年双向车用电池充电器市场报告 电动汽车车载充电器:全球市场份额和排名、总收入和需求预测(2025-2031 年)

电动汽车车载充电器:全球市场份额和排名、总收入和需求预测(2025-2031 年) 交流电电动车载充电器市场分析与预测(至2034年):类型、产品、技术、组件、应用、安装类型、最终用户、功能、设备和解决方案

交流电电动车载充电器市场分析与预测(至2034年):类型、产品、技术、组件、应用、安装类型、最终用户、功能、设备和解决方案 全球双向充电市场(至2035年):按应用(V2G、V2H、V2L)、动力类型(纯电动车、插电式混合动力车)、车辆类型(乘用车、轻型商用车)、充电型(交流电充电、直流充电)、最终用户和地区划分

全球双向充电市场(至2035年):按应用(V2G、V2H、V2L)、动力类型(纯电动车、插电式混合动力车)、车辆类型(乘用车、轻型商用车)、充电型(交流电充电、直流充电)、最终用户和地区划分 2032 年车用充电器市场预测:按车辆类型、推进类型、充电器类型、输出功率、最终用户和地区进行的全球分析

2032 年车用充电器市场预测:按车辆类型、推进类型、充电器类型、输出功率、最终用户和地区进行的全球分析 车载充电器市场:2025-2032年全球预测(依车辆类型、电压、输出功率及通路划分)2025年全球车用充电器市场报告

车载充电器市场:2025-2032年全球预测(依车辆类型、电压、输出功率及通路划分)2025年全球车用充电器市场报告 全球交流纯电动汽车车用充电器市场全球电动汽车车用充电器市场全球车用充电器市场

全球交流纯电动汽车车用充电器市场全球电动汽车车用充电器市场全球车用充电器市场