|

市场调查报告书

商品编码

1690197

工程木材:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Engineered Wood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

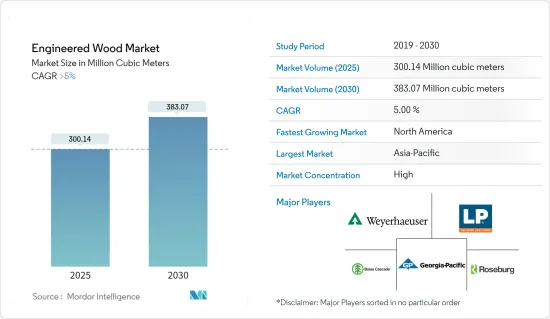

预计 2025 年工程木材市场规模为 3.0014 亿立方米,到 2030 年将达到 3.8307 亿立方米,预测期内(2025-2030 年)的复合年增长率将超过 5%。

COVID-19疫情对市场产生了负面影响。然而,由于疫情后建筑和装修活动的增加,工程木材市场目前预计将达到疫情前的水平。

主要亮点

- 从中期来看,非住宅领域的需求不断增长以及 CLT(交叉层压木材)作为建筑材料的使用不断增加可能会在预测期内推动市场发展。

- 另一方面,对甲醛排放的严格环境问题可能会阻碍市场成长。

- 预计印度和中国住宅的兴起将在预测期内带来机会。

- 亚太地区可能主导全球市场,而北美预计在预测期内工程木材的消费速度最快。

工程木材市场趋势

住宅领域占据市场主导地位

- 工程木材用途广泛,包括家具、墙壁、地板、门、屋顶、橱柜、柱子、横樑和楼梯。

- 复合板的用途正在迅速扩大。对于低层建筑,CLT 墙板的承重能力增强,比传统的框架墙具有更大的优势。

- CLT 已成为欧洲和北美中层住宅领域的成熟体系。此外,交叉层压木材在建造150公尺以上的高层建筑时也得到越来越多的应用。

- 预计 OSB 在墙壁、地板和屋顶等各种住宅应用中的使用日益增加将推动市场的发展。

- 各种工程木材被广泛应用于住宅领域,用于各种用途。欧洲有 73% 的人口居住在都市区,预计到 2050 年都市区将达到 80% 以上。

- 欧洲家具公司非常成功且富有创新精神。德国、义大利和斯堪的纳维亚的家具公司是奢华设计领域的标竿。

- 根据美国人口普查局公布的资料,2023年美国私人建筑年度总价值与前一年同期比较增长4.7%。

- 2023年的总建筑预算为19,787亿美元,比2022年的总建筑预算高出7%。

- 2023 年 12 月,建筑支出预计为 2.096 兆美元,而 2022 年为 1.8409 兆美元,成长 13.9%。

- 因此,由于上述方面,预计住宅领域将在预测期内推动市场发展。

亚太地区占市场主导地位

- 亚太地区包括中国、印度、东协、日本等主要国家。

- 中国经济成长的动力主要来自发达的住宅和商业建筑业。在中国,香港住宅委员会已推出多项倡议,推动经济适用住宅建设。当局的目标是到 2030 年提供 301,000 套公共住宅。

- 此外,预计到 2025 年将建成 7,000 多个购物中心。

- 在印度,预计2024年经济适用住宅将增加约70%。据Invest India称,到2025年,印度建筑业规模预计将达到1.4兆美元。

- 此外,预计到 2030 年,印度将有超过 30% 的人口居住在都市区,这将带来对额外 2,500 万套中檔和经济适用住宅的需求,从而在预测期内推动对工程木製品的需求。

- 在亚太地区,日本和中国占了OSB市场的很大份额。 Norbond 在日本销售 OSB 板已有 20 多年,并在广大最终用户的建筑项目中取得了优异的成绩。

- 因此,预计亚太地区将主导全球市场。

工程木材产业概况

工程木材市场部分整合,大多数公司占有较小的市场占有率。市场的主要企业(不分先后顺序)包括 Weyerhaeuser Company、Boise 连锁、 乔治亚-Pacific、Roseburg Forest Products 和 Louisiana-Pacific Corporation。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 非住宅领域的需求不断增加

- 越来越多地使用复合板(CLT)作为建筑材料

- 其他机会

- 限制因素

- 甲醛排放引发的严重环境问题

- 其他阻碍因素

- 产业价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 类型

- 合板

- 定向纤维板(OSB)

- 古拉姆

- 交叉层压木材(CLT)

- 层压单板木材(LVL)

- 塑合板

- 其他(纤维板、平行股线等)

- 应用

- 非住宅

- 住宅

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 土耳其

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Binderholz GmbH

- Boise Cascade

- Georgia-Pacific(Georgia-Pacific Wood Products LLC)

- HASSLACHER Holding GmbH

- Havwoods India Pvt. Ltd

- Huber Engineered Woods LLC

- KLH Massivholz Wiesenau GmbH

- Kronoplus Limited

- Louisiana-Pacific Corporation

- Mayr-Melnhof Holz Holding AG

- Nordic Structures

- Pacific Woodtech Corporation

- Resolute Forest Products

- Roseburg

- Stora Enso

- West Fraser

- Weyerhaeuser Company

第七章 市场机会与未来趋势

- 印度和中国的住宅建设成长

- 其他机会

The Engineered Wood Market size is estimated at 300.14 million cubic meters in 2025, and is expected to reach 383.07 million cubic meters by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic had a negative impact on the market. However, the market for engineered wood has now been close to reaching pre-pandemic levels because of increasing construction and restoration activities in the post-pandemic period.

Key Highlights

- Over the medium term, growing demand from the non-residential sector and increasing use of cross-laminated timber (CLT) as a construction material are likely to drive the market during the forecast period.

- On the flip side, stringent environmental concerns related to formaldehyde emissions are likely to hinder market growth.

- The growing residential construction in India and China is expected to act as an opportunity in the forecast period.

- Asia-Pacific is likely to dominate the global market, while North America is expected to witness the fastest consumption of engineered wood during the forecast period.

Engineered Wood Market Trends

The Residential Segment to Dominate the Market

- Engineered wood is used for a wide range of applications, including furniture, walls, flooring, doors, roofs, cabinets, columns, beams, and staircases.

- The application of cross-laminated wood has been increasing rapidly. For low-rise construction, the increased loadbearing capacity of CLT wall panels adds further benefits over conventional stud-framed walls.

- Cross-laminated timber is now an established system in the mid-rise residential sector in Europe and North America. In addition, there are increasing examples of cross-laminated timber being used to construct skyscrapers for buildings over 150 meters tall.

- The growing application of OSB in various residential applications, such as walls, flooring, and roofs, is estimated to drive the market.

- All types of engineered woods are significantly used in various applications in the residential sector. With 73% of its population living in urban areas, Europe is expected to be over 80% urban by 2050.

- European furniture companies are very successful and innovative. The German, Italian, and Nordic furniture companies act as benchmarks in the field of high-class design.

- According to the data released by the United States Census Bureau, the total annual value of private construction in the country increased by 4.7% in 2023 compared to the previous year.

- The total value of construction in 2023 was USD 1,978.7 billion, which was 7% above the total value of construction in 2022.

- In December 2023, a total of USD 2,096 billion was spent compared to USD 1,840.9 billion in 2022, registering a 13.9% rise in construction spending.

- Thus, based on the aforementioned aspects, the residential segment is expected to drive the market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific has several major countries, such as China, India, ASEAN, and Japan.

- China has been majorly driven by ample developments in the residential and commercial construction sectors and is supported by a growing economy. In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030.

- China is also likely to witness the construction of 7,000 more shopping centers, which are estimated to start functioning by 2025.

- In India, the availability of affordable housing is expected to rise by around 70% by 2024. By 2025, India's construction industry is expected to reach USD 1.4 trillion, as per Invest India.

- Also, by 2030, more than 30% of the population is expected to live in urban India, creating a demand for 25 million additional mid-end and affordable units, thus bolstering the demand for engineered wood products during the forecast period.

- In Asia-Pacific, Japan and China have a considerable share of the OSB market. Norbond has been marketing its OSB panels in Japan for over 20 years, and it has established a track record of high performance in a variety of end-user construction.

- Hence, Asia-Pacific is expected to dominate the global market.

Engineered Wood Industry Overview

The engineered wood market is partially consolidated, with most players accounting for a marginal market share. Major companies in the market (in no particular order) include Weyerhaeuser Company, Boise Cascade, Georgia-Pacific, Roseburg Forest Products, and Louisiana-Pacific Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Non-residential Sector

- 4.1.2 Increasing Use of Cross-laminated Timber (CLT) as Construction Materials

- 4.1.3 Other Opportunities

- 4.2 Restraints

- 4.2.1 Stringent Environmental Concerns Related to Formaldehyde Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Plywood

- 5.1.2 Oriented Strand Board (OSB)

- 5.1.3 Glulam

- 5.1.4 Cross-laminated Timber (CLT)

- 5.1.5 Laminated Veneer Lumber (LVL)

- 5.1.6 Particleboard

- 5.1.7 Other Types (Fiber Board, Parallel Strand, Others)

- 5.2 Application

- 5.2.1 Non-residential

- 5.2.2 Residential

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Binderholz GmbH

- 6.4.2 Boise Cascade

- 6.4.3 Georgia-Pacific (Georgia-Pacific Wood Products LLC)

- 6.4.4 HASSLACHER Holding GmbH

- 6.4.5 Havwoods India Pvt. Ltd

- 6.4.6 Huber Engineered Woods LLC

- 6.4.7 KLH Massivholz Wiesenau GmbH

- 6.4.8 Kronoplus Limited

- 6.4.9 Louisiana-Pacific Corporation

- 6.4.10 Mayr-Melnhof Holz Holding AG

- 6.4.11 Nordic Structures

- 6.4.12 Pacific Woodtech Corporation

- 6.4.13 Resolute Forest Products

- 6.4.14 Roseburg

- 6.4.15 Stora Enso

- 6.4.16 West Fraser

- 6.4.17 Weyerhaeuser Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Residential Construction in India and China

- 7.2 Other Opportunities

工程木材市场:2026-2032年全球市场预测(依产品类型、木材种类、通路、应用及最终用户划分)

工程木材市场:2026-2032年全球市场预测(依产品类型、木材种类、通路、应用及最终用户划分) 2026-2034年全球工程木材市场规模、份额、趋势和成长分析报告

2026-2034年全球工程木材市场规模、份额、趋势和成长分析报告 2026年全球中密度纤维板和刨花板市场报告2026年全球再生白纸板市场报告2026年全球工程木材市场报告

2026年全球中密度纤维板和刨花板市场报告2026年全球再生白纸板市场报告2026年全球工程木材市场报告 全球工程木材市场(至 2035 年):按产品类型、黏合剂类型、应用、最终用户、地区、产业趋势和预测

全球工程木材市场(至 2035 年):按产品类型、黏合剂类型、应用、最终用户、地区、产业趋势和预测 工程木材市场规模、份额及成长分析(按类型、应用、最终用户和地区划分)-2026-2033年产业预测

工程木材市场规模、份额及成长分析(按类型、应用、最终用户和地区划分)-2026-2033年产业预测 竹工程木材市场-全球产业规模、份额、趋势、机会和预测(按产品类型、按应用、按最终用户、按配销通路、按地区、按竞争)2020-2030F

竹工程木材市场-全球产业规模、份额、趋势、机会和预测(按产品类型、按应用、按最终用户、按配销通路、按地区、按竞争)2020-2030F 全球工程木材市场:需求分析、区域、应用及 2034 年预测

全球工程木材市场:需求分析、区域、应用及 2034 年预测 2025-2029年全球工程木製品市场

2025-2029年全球工程木製品市场