|

市场调查报告书

商品编码

1910887

塑胶射出成型:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Plastics Injection Molding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

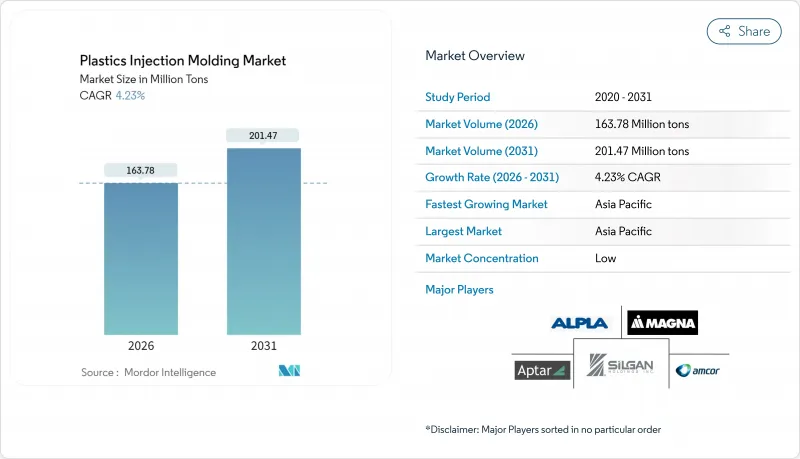

预计到 2025 年,塑胶射出成型市场价值将达到 1.5713 亿吨,并预计从 2026 年的 1.6378 亿吨增长到 2031 年的 2.0147 亿吨,在预测期(2026-2031 年)内以 4.23% 的复合年增长率增长。

这一持续成长表明,该技术在包装、汽车、电子和医疗设备等行业的成本效益型大规模生产中发挥核心作用。电子商务的成长、电动车 (EV) 生产的加速以及监管部门推动循环经济,这些因素共同拓宽了注塑射出成型机和先进的材料配方技术正在帮助生产商抵消不断上涨的原材料成本。亚太电子产业丛集的扩张、北美地区的製造业回流以及欧洲在可再生能源法规方面的先发优势等区域性因素,正在为各地区创造更多机会。同时,与原油价格相关的树脂价格波动以及日益严格的全球塑胶法规正在限制利润率,促使企业加强对再生原料、数位化品管和报废追溯系统的投资。

全球注塑射出成型市场趋势与洞察

电子商务推动包装需求激增

小包裹量的爆炸式增长推动了对耐用且轻巧的保护解决方案的需求。这促使品牌所有者指定使用整体式聚乙烯和聚丙烯包装,以在不牺牲强度的前提下最大限度地减少材料用量。将于2025年生效的欧盟包装和包装废弃物法规(PPWR)要求到2030年,PET食品包装的再生材料含量必须达到30%,这加速了模具和製程参数的重新设计,以适应高再生材料含量。在美国14个州实施的生产者延伸责任制(EPR)计划增加了成本,促进了环保设计,并奖励拥有先进树脂回收生产线的加工商。这些法规的综合影响正在加速注塑射出成型市场的需求成长,尤其是在薄壁容器和瓶盖领域,透过缩短生产週期可以实现材料节约和生产效率提升。先进的射出成型商正在采用套模贴标和数位浮水印技术来简化分类流程,从而提高废弃树脂的可用性,并确保原材料的持续供应。

汽车和电动车的轻量化要求

为了满足日益严格的平均二氧化碳排放目标并最大限度地提高电动车的续航里程,汽车製造商正越来越多地转向塑胶替代品。特斯拉的巨型铸造策略展示了大型铝铸件在减少零件数量方面的优势,同时扩大了对可与射出成型结构整合的注塑成型内外饰件的需求。电池製造商正在探索采用阻燃夹层壁热塑性外壳,与钢製外壳相比,每辆车最多可减轻 40 公斤的重量。恩格尔公司的高压电池机壳原型就是这项转变的例证。 ISO 14040 生命週期评估正日益影响材料选择,可再生树脂优先于复合金属零件。这些趋势正在推动对工程级聚合物(例如聚酰胺、聚碳酸酯和再生聚丙烯)的需求,由于每辆车用量增加以及对新型电动车平台模具的持续需求,塑胶射出成型市场的价值基础正在扩大。

树脂价格波动与原油价格相关

受原油价格受地缘政治动盪影响,现货聚乙烯和聚丙烯价格上涨。美国将于2025年实施的关税将使部分树脂等级的到岸成本增加10-15%,而中国约500万吨的供应过剩则压低了亚洲的价格,并扩大了区域套利价差。树脂经销商表示,市场存在前所未有的不确定性,82%的加工商正在采取多通路采购策略,以应对价格飙升。利润率波动抑制了长期模具投资,提高了注塑射出成型市场产能扩张的门槛,并促使加工商转向避险工具和公式定价合约。

细分市场分析

预计到2025年,聚乙烯将占据射出成型塑胶市场36.05%的主导份额,并在2031年之前保持5.02%的复合年增长率,这主要得益于对再生材料含量要求的提高,从而增强了其可回收性优势。聚乙烯的主导地位得益于薄壁包装、盖子与封口装置系统以及新兴的汽车燃料电池组件,这些应用都充分利用了聚乙烯树脂的耐化学腐蚀性。聚丙烯紧随其后,凭藉其高耐热变形温度和优异的刚度重量比,在汽车内饰、暖通空调外壳和家用电器组件等领域占据重要地位。丙烯腈-丁二烯-苯乙烯共聚物(ABS)将在家用电子电器机壳保持一定的市场份额,而聚苯乙烯由于监管日益严格,在一次性刀叉餐具的市场份额正在下降。

先进的回收设施能够进行解聚和溶剂精炼,从而提升消费后聚乙烯的质量,使其能够直接取代原生树脂,并帮助加工商减少范围3排放。聚碳酸酯在车头灯镜片和透明防护罩领域的应用日益广泛,并在某些汽车车型中被用作薄壁玻璃的替代品。源自蓖麻油的生物基聚酰胺因其固有的阻燃性和低碳强度,在引擎室零件领域越来越受欢迎。这些材料层面的变化有助于塑胶射出成型市场的多元化,同时也有助于客户实现其环境、社会和管治(ESG)目标。

塑胶射出成型报告按原料类型(聚丙烯、丙烯腈丁二烯苯乙烯、聚苯乙烯、聚乙烯、聚氯乙烯等)、应用领域(包装、建筑、消费品、电子产品、汽车和运输、医疗、其他应用)和地区(亚太地区、北美、欧洲、南美、中东和非洲)进行细分。

区域分析

到2025年,亚太地区将占据全球注塑射出成型市场34.10%的份额,并在2031年之前以5.24%的复合年增长率持续增长,这主要得益于中国、印度和东南亚电子及汽车製造业的扩张。政府激励措施、低廉的人事费用以及接近性下游组装厂的优势,都为产能扩张提供了支撑。日本超过80%的工厂已实施数位双胞胎和碳足迹管理工具,以提高生产效率和永续性。北美地区正在进行製造业回流和近岸外包,预计墨西哥将在2023年吸引439亿美元的外国直接投资(FDI),这将推动汽车内装件模具进口和承包工程单元的建设。

在美国,一项耗资1.4兆美元的再工业化计画预计将提升半导体、电动车电池和医疗设备的产能,推动国内对树脂的需求。加拿大安大略省的模具製造群继续为消费品包装项目供应高腔模具,但工资溢价正在推动自动化程度的提高。

欧洲加工商正投资于解聚製程和溶剂精炼厂,以符合PPWR法规的要求。该法规要求到2030年,PET包装中必须含有30%的再生材料。德国的工程技术支援豪华汽车的多成分注塑成型,而法国则顺应消费者日益增长的环保意识,扩大生物基化妆品包装的生产。南美洲依赖巴西的汽车需求,在地采购法规正在鼓励增加塑胶零件的国内产量。

中东和非洲地区正经历快速扩张,这主要得益于沙乌地阿拉伯对下游聚合物产业的投资,以及南非旨在促进本地零件生产的模具津贴计画。这些不同的区域趋势正在汇聚,共同扩大射出射出成型市场的地域覆盖范围。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务激增?推动包装需求

- 汽车和电动车的轻量化要求

- 抛弃式产品的需求不断增长

- 亚太地区电子製造业的产业化

- OEM厂商采用射出成型电动汽车电池外壳

- 市场限制

- 树脂价格波动与原油价格相关

- 全球塑胶法规日益收紧

- 全电动大吨位压平机的资本投资与技能短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依原料类型

- 聚丙烯

- 丙烯腈丁二烯苯乙烯(ABS)

- 聚苯乙烯

- 聚乙烯

- 聚氯乙烯(PVC)

- 聚碳酸酯

- 聚酰胺

- 其他成分

- 透过使用

- 包装

- 建筑/施工

- 消费品

- 电子设备

- 汽车/运输设备

- 卫生保健

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ALPLA

- Amcor PLC

- Antolin

- AptarGroup, Inc.

- BERICAP

- CVA Plastics

- EVCO Plastics

- FORVIA Faurecia

- HTI Plastics

- Husky Technologies

- IAC Group

- Magna International Inc.

- Marelli Holdings Co. Ltd

- Naber Plastics BV

- Quantum Plastics

- SCHAUENBURG Industrietechnik

- SEKISUI CHEMICAL CO., LTD.

- Silgan Holdings Inc.

- The Rodon Group

- TOYOTA BOSHOKU CORPORATION

第七章 市场机会与未来展望

The Plastics Injection Molding Market was valued at USD 157.13 million tons in 2025 and estimated to grow from USD 163.78 million tons in 2026 to reach USD 201.47 million tons by 2031, at a CAGR of 4.23% during the forecast period (2026-2031).

This sustained expansion underscores the technology's centrality to cost-effective, large-volume manufacturing in packaging, automotive, electronics and medical devices. E-commerce growth, accelerating electric-vehicle (EV) production and regulatory pushes for circularity collectively widen the application base of the plastics injection molding market, while energy-efficient all-electric machines and advanced material formulations help producers offset rising input costs. Asia-Pacific's growing electronics clusters, North American reshoring initiatives and Europe's first-mover stance on recyclability regulations all amplify regional opportunities. At the same time, volatile crude-oil-linked resin pricing and tightening global anti-plastic rules temper profit margins and compel investments in recycled feedstocks, digital quality control and end-of-life traceability systems.

Global Plastics Injection Molding Market Trends and Insights

Surge in E-commerce-Driven Packaging Demand

Explosive parcel volumes have heightened requirements for durable yet lightweight protective solutions, prompting brand owners to specify mono-material polyethylene and polypropylene packages that minimize material use without compromising strength. The EU Packaging and Packaging Waste Regulation (PPWR), effective 2025, mandates 30% recycled content in PET food packaging by 2030, accelerating redesign of tooling and process parameters to handle higher-recycled blends. U.S. Extended Producer Responsibility (EPR) fees across 14 states create an additional cost signal that rewards eco-modulated designs and favors converters with advanced resin reclamation lines. These converging mandates bolster volume growth in the plastics injection molding market, particularly in thin-wall container and closure segments where cycle-time reductions deliver material savings and higher throughput. Progressive molders are adopting in-mold labeling and digital watermarking to streamline sorting, increasing the likelihood of post-consumer resin availability and ensuring feedstock continuity.

Lightweighting Requirements in Automotive and EVs

Automotive OEMs have intensified plastics substitution to achieve stringent fleet-average CO2 targets and maximize EV range. Tesla's gigacasting strategy showcases how large aluminum castings reduce part counts, but it simultaneously expands demand for injection-molded interior and exterior trims that integrate with cast structures. Battery manufacturers are exploring thermoplastic housings with flame-retardant sandwich walls that cut up to 40 kg per vehicle compared with steel alternatives, a shift exemplified by Engel's high-voltage battery enclosure prototype. ISO 14040 life-cycle assessments increasingly influence material choices, favoring recyclable resins over multi-material metal assemblies. These trends elevate engineering-grade polymers such as polyamide, polycarbonate and recycled polypropylene, widening the value pool of the plastics injection molding market through higher content per vehicle and sustained tooling demand for new EV platforms.

Volatile Crude-Oil-Linked Resin Pricing

Polyethylene and polypropylene spot prices rose as crude benchmarks responded to geopolitical disruptions. U.S. tariffs introduced in 2025 raised landed costs of some resin grades by 10-15%, while Chinese oversupply, estimated at an additional 5 million tons of capacity, depressed Asian quotes and widened inter-regional arbitrage spreads. Resin distributors cite unprecedented uncertainty, with 82% of converters pursuing multisourcing strategies to guard against price spikes. Margin volatility discourages long-term tooling commitments, raising the hurdle rate for capacity additions across the plastics injection molding market and nudging processors toward hedging instruments and formula-pricing contracts.

Other drivers and restraints analyzed in the detailed report include:

- Growing Need for Single-Use Medical Disposables

- OEM Adoption of Injection-Molded EV Battery Housings

- Tightening Global Anti-Plastic Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene secured a commanding 36.05% share of the plastics injection molding market in 2025 and is on track for a 5.02% CAGR through 2031 as recycled-content mandates reinforce its recyclability advantage. This leadership is fueled by thin-wall packaging, cap-and-closure systems and emerging automotive fuel-cell components that capitalize on the resin's chemical resistance. Polypropylene follows closely in interior automotive trims, HVAC housings and appliance parts, leveraging high heat deflection and stiffness-to-weight ratios. Acrylonitrile butadiene styrene retains niche in consumer electronics casings, while polystyrene faces structural decline in single-use cutlery amid regulatory crackdowns.

Advanced recycling facilities capable of depolymerization and solvent-based purification are improving the quality of post-consumer polyethylene, enabling drop-in replacement for virgin resin and lowering scope-3 emissions for converters. Polycarbonate uptake advances steadily in headlamp lenses and transparent protective shields, with thin-gauge glazing options replacing heavier glass in certain automotive models. Bio-based polyamides produced from castor-bean oil are gaining interest in under-hood parts due to inherent flame retardancy and lower carbon intensity. These material-level shifts deepen the diversification of the plastics injection molding market while supporting clients' environmental, social and governance (ESG) objectives.

The Plastics Injection Molding Report is Segmented by Raw Material Type (Polypropylene, Acrylonitrile Butadiene Styrene, Polystyrene, Polyethylene, Polyvinyl Chloride, and More), Application (Packaging, Building and Construction, Consumer Goods, Electronics, Automotive and Transportation, Healthcare, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific held 34.10% of the plastics injection molding market in 2025 and is expanding at a 5.24% CAGR to 2031 as China, India, and Southeast Asia scale electronics and automotive output. Government incentives, lower labor costs, and proximity to downstream assembly plants underpin capacity additions. Japan is leveraging digital twins and carbon-footprint dashboards across more than 80% of factories to heighten productivity and sustainability. North America benefits from reshoring and nearshoring, with Mexico securing USD 43.9 billion in FDI during 2023 that spurs tooling imports and turnkey cell installations for automotive interiors.

The United States' USD 1.4 trillion reindustrialization plan supports semiconductor, EV battery and medical-device capacity that will boost domestic resin offtake. Canada's mold-making clusters in Ontario continue to supply high-cavitation tools for consumer-packaging programs, though wage premiums encourage higher degrees of automation.

European converters are investing in depolymerization and solvent-based purification plants to meet PPWR requirements for 30% recycled content in PET packaging by 2030. Germany's engineering prowess underpins advanced multi-component molding for premium vehicles, while France scales bio-based cosmetic packaging aligned with consumer eco-preferences. South America depends on Brazilian automotive demand, with localized content rules compelling higher domestic plastic part production.

The Middle East and Africa are expanding through Saudi Arabia's polymer downstream investments and South Africa's tooling grant scheme aimed at stimulating localized part production. These diverse regional dynamics collectively broaden the geographic footprint of the plastics injection molding market.

- ALPLA

- Amcor PLC

- Antolin

- AptarGroup, Inc.

- BERICAP

- CVA Plastics

- EVCO Plastics

- FORVIA Faurecia

- HTI Plastics

- Husky Technologies

- IAC Group

- Magna International Inc.

- Marelli Holdings Co. Ltd

- Naber Plastics BV

- Quantum Plastics

- SCHAUENBURG Industrietechnik

- SEKISUI CHEMICAL CO., LTD.

- Silgan Holdings Inc.

- The Rodon Group

- TOYOTA BOSHOKU CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-Commerce?Driven Packaging Demand

- 4.2.2 Lightweighting Requirements in Automotive and EVs

- 4.2.3 Growing Need for Single-Use Medical Disposables

- 4.2.4 Industrialisation in APAC Electronics Manufacturing

- 4.2.5 OEM Adoption of Injection-Molded EV Battery Housings

- 4.3 Market Restraints

- 4.3.1 Volatile Crude-Oil-Linked Resin Pricing

- 4.3.2 Tightening Global Anti-Plastic Regulations

- 4.3.3 Cap-Ex and Skills Gap for All-Electric High-Tonnage Presses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material Type

- 5.1.1 Polypropylene

- 5.1.2 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.3 Polystyrene

- 5.1.4 Polyethylene

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Polycarbonate

- 5.1.7 Polyamide

- 5.1.8 Other Raw Materials

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Building and Construction

- 5.2.3 Consumer Goods

- 5.2.4 Electronics

- 5.2.5 Automotive and Transportation

- 5.2.6 Healthcare

- 5.2.7 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ALPLA

- 6.4.2 Amcor PLC

- 6.4.3 Antolin

- 6.4.4 AptarGroup, Inc.

- 6.4.5 BERICAP

- 6.4.6 CVA Plastics

- 6.4.7 EVCO Plastics

- 6.4.8 FORVIA Faurecia

- 6.4.9 HTI Plastics

- 6.4.10 Husky Technologies

- 6.4.11 IAC Group

- 6.4.12 Magna International Inc.

- 6.4.13 Marelli Holdings Co. Ltd

- 6.4.14 Naber Plastics BV

- 6.4.15 Quantum Plastics

- 6.4.16 SCHAUENBURG Industrietechnik

- 6.4.17 SEKISUI CHEMICAL CO., LTD.

- 6.4.18 Silgan Holdings Inc.

- 6.4.19 The Rodon Group

- 6.4.20 TOYOTA BOSHOKU CORPORATION

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

工业模具市场:依模具类型、模具材料、最终用途产业及销售管道划分-2026-2032年全球预测橡胶转注成型机市场:按型腔类型、自动化程度、机器类型、材料类型、终端用户产业划分,全球预测,2026-2032年

工业模具市场:依模具类型、模具材料、最终用途产业及销售管道划分-2026-2032年全球预测橡胶转注成型机市场:按型腔类型、自动化程度、机器类型、材料类型、终端用户产业划分,全球预测,2026-2032年 网格铸造机市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、製程、最终用户及功能划分

网格铸造机市场分析及预测(至2035年):依类型、产品类型、技术、组件、应用、材质、製程、最终用户及功能划分 2026年全球工业模具市场报告

2026年全球工业模具市场报告 挤出塑胶市场-全球产业规模、份额、趋势、机会及预测(依材料、最终用户、地区及竞争格局划分,2021-2031年)塑胶射出成型市场:依最终用途产业、材料类型、机器类型和扣夹力-全球预测,2025-2032年

挤出塑胶市场-全球产业规模、份额、趋势、机会及预测(依材料、最终用户、地区及竞争格局划分,2021-2031年)塑胶射出成型市场:依最终用途产业、材料类型、机器类型和扣夹力-全球预测,2025-2032年 全球金属模具市场全球聚合物微射出成形市场

全球金属模具市场全球聚合物微射出成形市场 吹塑成型机市场:按机器类型、应用、材料类型和地区划分,2026-2032 年全球工业模具市场:2034 年的机会与策略

吹塑成型机市场:按机器类型、应用、材料类型和地区划分,2026-2032 年全球工业模具市场:2034 年的机会与策略