|

市场调查报告书

商品编码

1910897

北美电池能源储存系统(BESS)-市场份额分析、产业趋势与统计、成长预测(2026-2031)North America Battery Energy Storage System (BESS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

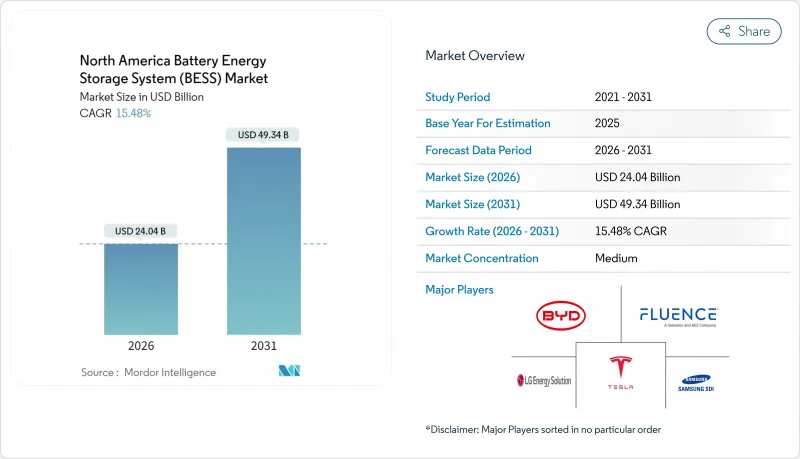

2025年北美电池能源储存系统係统市值为208.2亿美元,预计到2031年将达到493.4亿美元,高于2026年的240.4亿美元。

预测期(2026-2031 年)的复合年增长率预计为 15.48%。

联邦税额扣抵、国内电池製造以及由可再生能源併网、资料中心扩张和电网拥堵推动的电网级需求激增,共同支撑了这一增长。 《通膨控制法案》扩大了独立储能专案30%的投资税额扣抵后,公共产业的采购活动加速,提高了计划的内部报酬率,并刺激了商业市场的发展。同时,密西根州、乔治亚和亚利桑那州的超级工厂已将磷酸锂铁电池(LFP)的在地采购成本降低了20-30%,缩小了与燃气调峰设备的成本差距,并缩短了前置作业时间。开发人员目前正致力于开发能够连续运作数小时的资产,即使在批发电力价格波动的情况下,也能透过频率调节、容量支付和能源套利获得收益。随着特斯拉、Fluence和LG能源解决方案等垂直整合型领导企业与纯粹的整合商和自主开发计划的公共产业竞争,竞争日益激烈。同时,钒液流电池和铁空气电池等长期储能技术正在挑战锂离子电池在 8-12 小时和季节性运作週期中的现有地位。

北美电池能源储存系统(BESS)市场趋势与洞察

各州可再生能源强制性规定的快速扩展

加州SB100法案的目标是到2045年实现100%清洁电力,该法案规定采购11.5吉瓦的储能容量。公用事业公司在2024年中期就超额完成了这一目标,确保了未来几年开发案的稳定成长。纽约州强制要求到2030年达到6吉瓦的储能容量,并提供奖励以弥补市场收入缺口。同时,由于电力短缺期间电价上涨以及燃煤发电的逐步淘汰,储能的经济效益显着提升,ERCOT在2024年达到了5吉瓦的併网申请量。明确的采购目标降低了资本风险,吸引了机构投资者,并透过使计划设计与IEEE 2030.2互通性标准保持一致,提高了计划的整体效率。强制性规定还提供了长期的市场可见性,使製造商能够实现供应链本地化,并使贷款机构能够建立反向槓桿债务。随着越来越多的州从仅关注可再生的目标转向明确包含储能的清洁能源标准,对公用事业规模系统的基础设施需求将显着增长。

北美超级工厂降低磷酸铁锂电池成本

包括宁德时代(CATL)和LG能源解决方案公司在内的供应商已开始运作符合先进製造税额扣抵政策的美国磷酸铁锂电池生产线,每千瓦时电池可享受35美元的税收抵免,每千瓦时组件可享受10美元的税收抵免。在地化生产可将公用事业规模储能係统(BESS)的交付成本降低高达30%,并将采购前置作业时间从12-14个月缩短至6-8个月。此外,本地化生产还能帮助开发商规避针对中国进口商品征收的25% 301条款关税的影响。与公用事业公司签订的多年销售协议可确保采购量并降低关税风险,从而稳定企划案融资融资的资本支出(CAPEX)预测。在地采购基地也有助于实现组件标准化和国产化率奖励,进一步提高财务回报。

前期资本投入高,且原物料价格波动较大

储能係统(BESS)的安装成本仍然是联合循环燃气涡轮机(CCGT)容量价格的2.5-3倍,这限制了其在没有碳定价系统的地区的普及。碳酸锂价格从2024年初的每吨8万美元暴跌至年底的每吨1.2万美元,凸显了采购的波动性,这使得固定价格的EPC合约更加复杂。钴和镍的供应地域集中,使NMC化学品面临地缘政治风险。中国在2024年启动的232条款关税规避调查可能导致额外15-25%的关税,进一步加剧了成本预测的不确定性。缺乏长期销售协议的私人开发商难以将成本衝击转嫁给消费者,导致最终投资决策被推迟,尤其是在ERCOT和CAISO等收入波动较大的地区。

细分市场分析

到2025年,锂离子电池技术在储能电池市场仍将占据91.10%的份额,这主要得益于成熟的磷酸锂电池供应链和不断下降的电芯价格。液流电池的市占率为5.35%,正以30.43%的年增长率成长,主要得益于电力公司对8-12小时放电时间且不易发生热失控的储能设备的需求。德克萨斯州一个100兆瓦时的锌电池先导计画实现了1万次循环,且性能劣化极小,凸显了锌电池与磷酸铁锂电池相比在耐久性方面的显着优势。由于太平洋西北地区电力公司在季节性电力供应提案方面优先考虑非锂电池技术,液流电池储能係统的市场规模预计将会扩大。儘管钠离子电池在住宅储能领域的测试已展现出在寒冷气候下的潜力,但由于磷酸铁锂电池成本的快速下降,铅酸电池在电力应用领域的市场份额仍在持续下降。

液流电池的普及应用表明,人们越来越认识到循环寿命经济性以及功率和能量的独立扩展性。奥勒冈州一个21兆瓦时的钒液流电池计划与风力发电相结合,可提供多天的可靠供给能力,避免了四小时锂电池设计所需的300%超额容量。钠离子电池的原料成本更低,因此在对成本敏感的住宅市场,尤其是在加州NEM 3.0收费系统下,更具吸引力。随着电力公司将采购规范转向更长的续航时间,锂电池在四小时供电以外的优势可能会减弱。

2025年,併网系统占总装机量的88.20%,这得益于联邦能源监理委员会(FERC)第841号命令以及企业积极参与批发电力市场。然而,由于矿山、军事基地和偏远离岛对高成本柴油燃料替代品的需求,离网和微电网解决方案正以28.10%的复合年增长率快速增长。加拿大一个矿场微电网(50兆瓦时)减少了70%的柴油消耗,每年节省800万美元,并减少了2.5万吨二氧化碳排放。美国国防部在2024年为独立基地拨款1.5亿美元。阿拉斯加的一个村庄正在将可再生能源与储能结合,以降低柴油成本0.40-0.60美元/千瓦时。混合微电网在加州和德克萨斯州越来越受欢迎,这种微电网既能保持与电网的连接,又能在野火和飓风期间独立运作。

离网经济模式着重降低燃料和输电成本,儘管每千瓦时(kWh)的初始投资较高,但投资回报週期短。加勒比海一家度假村利用一套10兆瓦时(MWh)的系统,光用六年就收回了成本,节省了200万美元的柴油燃料费用。混合模式提高了系统的韧性,同时实现了需量反应的货币化。更新后的IEEE 1547-2018标准要求从併网运行到独立运行的无缝过渡,简化了连接流程,并鼓励工商业用户采用此模式。

北美电池能源储存系统(BESS) 市场报告按电池类型(例如锂离子电池)、连接类型(併网/离网)、组件(例如电池组/支架、能源管理软体)、能量容量范围(例如 10-100 MWh、500 MWh+)、最终用户应用(电力公司、商业/工业、住宅)和地区(美国、加拿大、墨西哥)和地区进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 各州可再生能源强制性规定激增

- 北美超级工厂磷酸铁锂电池成本下降

- 独立式储能设施的税额扣抵

- 资料中心建置规模不断扩大,电力需求量庞大

- 自由市场中利润结构的创新

- 人工智慧优化的储能係统资产管理

- 市场限制

- 与抽水蓄能和LDES的竞争

- 高昂的初始资本投资成本和原物料价格波动

- 位置地方消防安全选址措施

- 关税和贸易问题带来的成本衝击

- 供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章 市场规模与成长预测

- 依电池类型

- 锂离子电池(磷酸锂铁(LFP)、镍锰钴锂(NMC)、钛酸锂(LTO))

- 铅酸电池

- 液流电池(钒氧化还原电池,锌溴电池)

- 钠离子

- 其他电池技术(镍镉电池、混合型超级电容)

- 按连线类型

- 併网(连接到电力公司)

- 离网(微电网、混合电网)

- 按组件

- 电池组支架

- 电源转换系统(PCS)

- 能源管理软体(EMS)

- 工厂相关设备及服务

- 按能量容量范围

- 小于10兆瓦时

- 10~100 MWh

- 100~500 MWh

- 超过500兆瓦时

- 透过最终用户使用

- 对于电力公司

- 商业和工业

- 住宅

- 按地区

- 美国

- 加拿大

- 墨西哥

第六章 竞争情势

- 市场集中度

- 策略性倡议(併购、联盟、购电协议)

- 市场占有率分析(主要企业的市场排名和份额)

- 公司简介

- Tesla Inc.

- Fluence Energy Inc.

- LG Energy Solution Ltd.

- Samsung SDI Co. Ltd.

- BYD Company Ltd.

- Panasonic Holdings Corp.

- Saft(TotalEnergies)

- Contemporary Amperex Technology Ltd.

- AES Corporation

- GE Vernova

- ABB Ltd.

- Siemens Energy

- Schneider Electric SE

- Eos Energy Enterprises

- NEC Energy Solutions

- Enel North America

- NextEra Energy Resources

- Sunverge Energy

- Powin LLC

- Wartsila Corporation

第七章 市场机会与未来展望

The North America Battery Energy Storage System Market was valued at USD 20.82 billion in 2025 and estimated to grow from USD 24.04 billion in 2026 to reach USD 49.34 billion by 2031, at a CAGR of 15.48% during the forecast period (2026-2031).

Federal tax credits, domestic cell manufacturing, and fast-rising grid-scale demand from renewable energy integration, data center build-outs, and transmission congestion underpin this growth. Utility procurement accelerated after the Inflation Reduction Act extended the 30% investment tax credit to stand-alone storage, improving project internal rates of return and unlocking merchant-market development. Meanwhile, Michigan, Georgia, and Arizona gigafactories are reducing the landed costs of lithium-iron-phosphate (LFP) by 20%-30%, thereby narrowing the cost gap with gas peakers and shortening lead times. Developers now pursue multi-hour assets that stack revenues from frequency regulation, capacity payments, and energy arbitrage even as wholesale spreads remain volatile. Competitive intensity is rising as vertically integrated leaders, such as Tesla, Fluence, and LG Energy Solution, vie with pure-play integrators and utilities that self-develop projects. Meanwhile, long-duration alternatives, including vanadium flow and iron-air batteries, challenge lithium-ion incumbency for 8-to-12-hour and seasonal duty cycles.

North America Battery Energy Storage System (BESS) Market Trends and Insights

Surging State-Level Renewable Mandates

California's SB 100 targets 100% clean electricity by 2045 and sets an 11.5 GW storage procurement that utilities exceeded by mid-2024, ensuring a robust multi-year development queue. New York mandates 6 GW by 2030 with incentives that bridge merchant-revenue gaps, while ERCOT registered 5 GW of 2024 interconnection requests as scarcity pricing and coal retirements drove storage economics. Clear procurement targets de-risk capital, attract institutional investors, and align project designs with IEEE 2030.2 interoperability standards, thereby enhancing overall project efficiency. Mandates also signal long-term market visibility, enabling manufacturers to localize supply chains and lenders to structure back-levered debt. As more states shift from renewables-only targets to clean-energy standards that explicitly include storage, the baseline demand for utility-scale systems expands significantly.

Falling LFP Battery Costs from NA Gigafactories

CATL, LG Energy Solution, and other suppliers have commissioned U.S. LFP cell lines subsidized by an advanced-manufacturing credit worth USD 35 per kWh for cells and USD 10 per kWh for modules. Domestic production compresses delivered utility-scale BESS costs by up to 30%, shrinks procurement lead times from 12-14 months to 6-8 months, and shields developers from 25% Section 301 tariffs on Chinese imports. Multi-year offtake deals with utilities lock in volume, while tariff-risk reduction stabilizes CAPEX assumptions for project finance. The localized supply base is also catalyzing component standardization and higher domestic content bonuses, which further improve financial returns.

High Up-Front CAPEX & Raw-Material Swings

Installed BESS costs remain 2.5-3X the capacity price of combined-cycle gas turbines, limiting uptake where carbon pricing is absent. Lithium carbonate prices plummeted from USD 80,000/t in early 2024 to USD 12,000/t by year-end, highlighting procurement volatility that complicates fixed-price EPC contracts. Cobalt and nickel supply is geographically concentrated, exposing NMC chemistries to geopolitical risk. A 2024 Section 232 probe into Chinese tariff circumvention threatens additional 15%-25% duties, further muddying cost forecasts. Merchant developers lacking long-term offtake struggle to pass through cost shocks, slowing final investment decisions, especially in ERCOT and CAISO, where revenue spreads fluctuate.

Other drivers and restraints analyzed in the detailed report include:

- IRA Stand-Alone Storage Tax Credit

- Grid-Hungry Data-Center Build-Out

- Local Fire-Safety Siting Moratoria

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion technologies maintained a 91.10% share of the battery energy storage system market in 2025, driven by mature LFP supply chains and declining cell prices. Flow batteries, although with a 5.35% share, are growing at a 30.43% annual rate as utilities seek 8- to 12-hour discharge assets that are immune to thermal runaway. A 100 MWh zinc-battery pilot in Texas achieved 10,000 cycles with minimal fade, highlighting the longevity gap compared to LFP. The battery energy storage system market size for flow technologies is poised to benefit from Pacific Northwest utility RFPs that favor non-lithium chemistries for seasonal firming. Sodium-ion trials for residential storage show promise in cold climates, while lead-acid continues to lose ground in utility applications due to the rapid decline in LFP costs.

Flow battery adoption indicates a growing recognition of cycle-life economics and the independent scaling of power versus energy. A 21 MWh vanadium project in Oregon, coupled with wind, provides multi-day firm capacity, avoiding the 300% oversizing required by four-hour lithium designs. Sodium-ion's lower raw-material exposure positions it for cost-sensitive residential markets, especially under California's NEM 3.0 tariffs. Shifting utility procurement specs toward long-duration performance will progressively erode lithium's dominance beyond the 4-hour niche.

On-grid systems captured 88.20% of 2025 deployments, supported by FERC Order 841 and robust participation in the wholesale market. However, off-grid and microgrid solutions are expanding at a 28.10% CAGR as mines, military bases, and islands displace expensive diesel. A 50 MWh Canadian mine microgrid reduced diesel use by 70%, saving USD 8 million annually and eliminating 25,000 t CO2. The U.S. Department of Defense earmarked USD 150 million in 2024 for islandable bases, while Alaska villages blend renewables and storage to reduce diesel costs by USD 0.40-0.60 kWh. Hybrid microgrids that retain grid ties but can island during wildfires or hurricanes are proliferating in California and Texas.

Off-grid economics center on avoided fuel and transmission costs, enabling rapid paybacks despite higher per-kWh CAPEX. A Caribbean resort's 10 MWh system eliminated a USD 2 million diesel bill with a six-year payback. Hybrid models also monetize demand-response payments while enhancing resilience. The updated IEEE 1547-2018 standards mandate seamless grid-to-island transitions, simplifying interconnection and fostering broader adoption among commercial and industrial (C&I) users.

The North America Battery Energy Storage System (BESS) Market Report is Segmented by Battery Type (Lithium-Ion, and More), Connection Type (On-Grid and Off-Grid), Component (Battery Pack and Racks, Energy Management Software, and More), Energy Capacity Range (10 To 100 MWh, Above 500 MWh, and More), End-User Application (Utility, Commercial and Industrial, and Residential), and Geography (United States, Canada, and Mexico).

List of Companies Covered in this Report:

- Tesla Inc.

- Fluence Energy Inc.

- LG Energy Solution Ltd.

- Samsung SDI Co. Ltd.

- BYD Company Ltd.

- Panasonic Holdings Corp.

- Saft (TotalEnergies)

- Contemporary Amperex Technology Ltd.

- AES Corporation

- GE Vernova

- ABB Ltd.

- Siemens Energy

- Schneider Electric SE

- Eos Energy Enterprises

- NEC Energy Solutions

- Enel North America

- NextEra Energy Resources

- Sunverge Energy

- Powin LLC

- Wartsila Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging state-level renewable mandates

- 4.2.2 Falling LFP battery costs from NA gigafactories

- 4.2.3 IRA stand-alone storage tax credit

- 4.2.4 Grid-hungry data-centre build-out

- 4.2.5 Merchant-market revenue-stack innovation

- 4.2.6 AI-optimised BESS asset management

- 4.3 Market Restraints

- 4.3.1 Pumped-hydro & LDES competition

- 4.3.2 High up-front CAPEX & raw-material swings

- 4.3.3 Local fire-safety siting moratoria

- 4.3.4 Tariff / trade-case cost shocks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO))

- 5.1.2 Lead-acid

- 5.1.3 Flow Battery (Vanadium Redox, Zinc-Bromine)

- 5.1.4 Sodium-ion

- 5.1.5 Other Battery Technologies (NiCd, Hybrid Super-capacitors)

- 5.2 By Connection Type

- 5.2.1 On-Grid (Utility Interconnected)

- 5.2.2 Off-Grid (Micro-Grid, Hybrid)

- 5.3 By Component

- 5.3.1 Battery Pack and Racks

- 5.3.2 Power Conversion System (PCS)

- 5.3.3 Energy Management Software (EMS)

- 5.3.4 Balance-of-Plant and Services

- 5.4 By Energy Capacity Range

- 5.4.1 Below 10 MWh

- 5.4.2 10 to 100 MWh

- 5.4.3 100 to 500 MWh

- 5.4.4 Above 500 MWh

- 5.5 By End-user Application

- 5.5.1 Utility

- 5.5.2 Commercial and Industrial

- 5.5.3 Residential

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tesla Inc.

- 6.4.2 Fluence Energy Inc.

- 6.4.3 LG Energy Solution Ltd.

- 6.4.4 Samsung SDI Co. Ltd.

- 6.4.5 BYD Company Ltd.

- 6.4.6 Panasonic Holdings Corp.

- 6.4.7 Saft (TotalEnergies)

- 6.4.8 Contemporary Amperex Technology Ltd.

- 6.4.9 AES Corporation

- 6.4.10 GE Vernova

- 6.4.11 ABB Ltd.

- 6.4.12 Siemens Energy

- 6.4.13 Schneider Electric SE

- 6.4.14 Eos Energy Enterprises

- 6.4.15 NEC Energy Solutions

- 6.4.16 Enel North America

- 6.4.17 NextEra Energy Resources

- 6.4.18 Sunverge Energy

- 6.4.19 Powin LLC

- 6.4.20 Wartsila Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球电池能源储存系统市场:按电池类型、应用、所有权/部署模式、连接方式、国家和地区划分-产业分析、市场规模、份额及预测(2025-2032年)

全球电池能源储存系统市场:按电池类型、应用、所有权/部署模式、连接方式、国家和地区划分-产业分析、市场规模、份额及预测(2025-2032年) 全球电池能源储存系统市场规模、份额、趋势和成长分析报告(2026-2034年)

全球电池能源储存系统市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球电池能源储存系统市场报告

2026年全球电池能源储存系统市场报告 电池储能係统市场-全球产业规模、份额、趋势、机会及预测(依电池类型、连接类型、能源容量、应用、区域及竞争格局划分,2021-2031年预测)

电池储能係统市场-全球产业规模、份额、趋势、机会及预测(依电池类型、连接类型、能源容量、应用、区域及竞争格局划分,2021-2031年预测) 电池能源储存系统市场规模、份额和趋势分析报告:按电池类型、应用领域、地区和细分市场预测(2026-2033 年)

电池能源储存系统市场规模、份额和趋势分析报告:按电池类型、应用领域、地区和细分市场预测(2026-2033 年) 全球电池能源储存系统市场按电池类型、连接类型、所有权、能源容量、应用和地区划分-预测至2030年

全球电池能源储存系统市场按电池类型、连接类型、所有权、能源容量、应用和地区划分-预测至2030年 电池能源储存系统市场(按组件、电池类型、能量容量、连接类型、部署和应用)—2025-2030 年全球预测

电池能源储存系统市场(按组件、电池类型、能量容量、连接类型、部署和应用)—2025-2030 年全球预测 2025 年全球电池储能系统整合商排名报告2034年电池能源储存系统係统全球市场机会与策略

2025 年全球电池储能系统整合商排名报告2034年电池能源储存系统係统全球市场机会与策略 电池能源储存系统(BESS) 市场预测(至 2032 年):按电池类型、能量容量、连接类型、所有者、应用、最终用户和地区进行的全球分析

电池能源储存系统(BESS) 市场预测(至 2032 年):按电池类型、能量容量、连接类型、所有者、应用、最终用户和地区进行的全球分析