|

市场调查报告书

商品编码

1690760

IT 外包 (ITO):市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)IT Outsourcing (ITO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

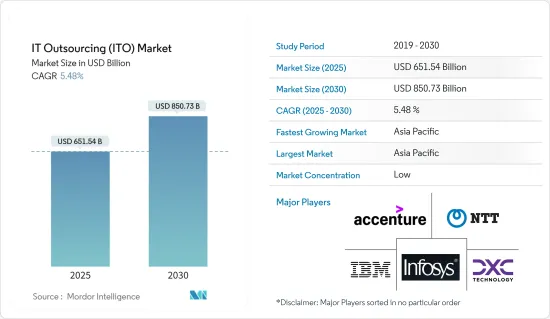

2025 年 IT 外包 (ITO) 市场规模预计为 6,515.4 亿美元,预计到 2030 年将达到 8,507.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.48%。

主要亮点

- 资讯科技已成为大多数组织的竞争优势。随着云端迁移和云端服务选项的出现,IT 外包已不再只是一个削减成本的过程。因此,这种新形式主要由客户体验、业务成长和竞争颠覆等组织动机所驱动。

- 更重要的是,新兴和小型组织日益增长的这种偏好使得市场上领先的供应商越来越注重寻找将其离岸团队与现场团队整合在一起的方法。小型供应商的另一个重要方面是其所提供服务的灵活性。

- 随着企业对简化业务营运和专注于推动收益的关键活动的需求不断增加,他们正在外包 IT 服务以获得能够保护资料的安全IT基础设施。企业正在利用 IT 服务市场参与者的专业知识来降低整个组织内与资料相关的风险。由于招募高技能专业人才需要时间,BFSI 产业正在推动市场发展。为了降低整体成本,企业正在投资外包解决方案。

- 然而,云端和基于伺服器的服务缺乏资料安全性正在阻碍市场的成长。云端基础的服务存在许多独特的安全问题和挑战。资料通常储存在第三方供应商处,并可透过网际网路在云端存取。这限制了资料的可见性和控制力。然而,对高效、扩充性基础设施的需求不断增长,以及向云端的迁移不断增加,正在推动市场的发展。

IT外包(ITO)市场的趋势

按行业划分,BFSI 是最大的

- 银行、金融服务和保险 (BFSI) 是主要的终端用户产业之一,其技术采用发生了重大转变,这主要是由于疫情和不断变化的竞争格局所带来的情况。

- 金融机构越来越多地将流程和服务外包给第三方。银行可以将从邮寄宣传活动到付款处理的所有事务外包。银行只有拥有强大而全面的内部 IT 部门或值得信赖的外部合作伙伴才能生存并吸引客户。例如,2023 年 3 月,数位和产品开发公司 Orion Innovation 宣布收购金融机构银行实施合作伙伴 Banktec Software Services Limited。 BankTech 将补充 Orion 的金融服务专业知识、开放银行解决方案和实施能力。

- BFSI 产业也正向云端转移,带来新的市场机会。根据 Google Cloud 最近进行的一项调查,全球约 41.4% 的技术人员和商业领袖计划投资云端基础的服务来管理他们的工作负载。此外,根据 Flexera 软体的资料,IT 支出将在 2022 年和 2023 年成长,其中软体产业的支出将成长 18%,其次是云端服务的支出,2023 年将成长 16%。

- 现今的客户要求更加个人化、更加简化的银行服务。您的 IT 外包商可以帮助您过渡到全通路平台,以便在任何装置上提供无缝存取。此外,这些平台还促进即时资料收集和分析,使金融机构能够改善客户体验。因此,这些发展正在推动银行的 IT 外包。

- 总体而言,BFSI 行业对 IT 外包服务的需求将受到先进的网路安全、数位转型、日益增长的监管合规性以及对创新解决方案的需求的推动,以满足不断变化的客户期望和行业趋势。

亚太地区可望主导市场

- 中国是亚太地区主要外包目的地之一。外包产业正在寻找大多数美国公司认为有吸引力的好处。降低开发成本对于保留外包的真正好处起着关键作用。

- 中国做出了巨大努力,透过数位化和工业化,从(廉价)劳动力製造向高端工业生产转型。商务部资料显示,2023年中国服务外包产业成长,企业签订服务外包合约金额达4,040亿美元,比去年成长17.6%。

- 印度是一个相当成熟的全球IT外包目的地,拥有广泛的选择。由于对熟练软体开发人员的需求不断增长,中国的 IT 外包公司正在全球迅速扩张。成本和强大的技术人才队伍对该国的市场优势发挥关键作用。

- 基于近年来IT技术的进步,日本正在扩大国内商业领域的IT外包范围,其中包括云端处理、资料保护和网路安全等。云端处理服务的使用正在增加,因为它们不需要大量的基础设施投资来提供业务能力。

- 总体而言,随着市场的持续发展,该地区各国预计未来几年将大幅成长。此外,该地区的资料中心建设正在推动强劲的需求。此外,随着资料中心市场不断成熟,基础设施升级带来的大量收益将推动该地区的 IT 外包发展。

IT外包(ITO)市场概况

IT外包市场的主要企业包括IBM Corporation、DXC Technologies、埃森哲PLC、NTT Corporation和Infosys Limited。这些市场参与企业正在采取各种策略,包括建立伙伴关係和收购,以加强产品系列建立永续的竞争优势。

- 2023 年 11 月,全球技术和服务公司 DXC Technology 与数位工作流程公司 ServiceNow 宣布建立策略合作伙伴关係,以在全球范围内转变客户服务和工作流程管理。两家公司将把 ServiceNow 的 ITSM Pro 和 Process Mining 解决方案的高级分析和 AI 整合到 DXC 平台 X 中,以推动共同客户的创新。

- 2023年7月,全球领先的数位业务和IT服务公司NTT 资料宣布将推出安全管理外包服务,旨在预防网路攻击事件并在发生时将损害降至最低。该服务于 2023 年 7 月在日本推出,并在本财年(2024 年 3 月)内扩展到全球。

- 2023 年 6 月,印孚瑟斯公司收购了丹麦银行在印度的 IT 业务,这是一项为期五年、价值 4.54 亿美元的 IT 外包协议的一部分,旨在专注于数位转型。透过这笔交易,该公司将人工智慧引入其服务中。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 对高效、扩充性IT基础设施的需求不断增加

- 越来越多的组织开始强调 IT 是依靠外包供应商来脱颖而出的一种手段

- 日益增长的云端迁移和虚拟基础设施的采用

- 市场挑战

- 市场分化与资料外洩增多

- IT架构的动态需求影响最终用户的客製化成本

- COVID-19 对 IT 外包产业的影响

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场分析

- 在岸和境外外包趋势

- 外包产业细分 - BPO 与 IT 外包的比较

- IT 解决方案商品化的影响

- IT 外包与管理服务产业分析

- 关键 IT 外包细分市场 - 应用程式和基础设施

- 数位转型的影响与「即服务」模式的出现

第六章 市场细分

- 按组织规模

- 中小型企业

- 大型企业

- 按最终用户产业

- BFSI

- 卫生保健

- 媒体与通讯

- 零售与电子商务

- 製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 波兰

- 比利时

- 荷兰

- 卢森堡

- 瑞典

- 丹麦

- 挪威

- 芬兰

- 冰岛

- 亚洲

- 中国

- 印度

- 日本

- 印尼

- 越南

- 马来西亚

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 哥伦比亚

- 中东和非洲

- GCC

- 南非

- 土耳其

- 北美洲

第七章 竞争格局

- 公司简介

- IBM Corporation

- DXC Technologies

- Accenture PLC

- NTT Corporation

- Infosys Limited

- Tata Consultancy Services

- Cognizant Technology Solutions Corporation

- Capgemini SE

- Wipro Limited

- Andela Inc.

- Wns Holding Ltd

- Pointwest Technologies

- ATOS SE

- Amadeus IT Group

- Specialist Computer Centres(SCC)

- HCL Technologies Ltd

第八章 全球主要IT外包公司企业发展排名分析

第九章 市场展望

The IT Outsourcing Market size is estimated at USD 651.54 billion in 2025, and is expected to reach USD 850.73 billion by 2030, at a CAGR of 5.48% during the forecast period (2025-2030).

Key Highlights

- Information technology has become a competitive edge for most organizations. IT outsourcing has become more than a simple cost-reduction process with cloud migrations and cloud service options. Therefore, this new form is mainly driven by organizational motivations in terms of customer experience, business growth, and competitive disruption.

- More importantly, such a rise in preference among the newer and smaller organizations has led the key vendors of the market to increasingly concentrate on finding a way to integrate the offshore team with the on-site. Another critical aspect driven by small-scale players is the agility in vendor offerings, which refers to the time-to-market.

- There is a rise in demand by businesses to streamline business operations and focus on crucial activities that are revenue drivers, and outsource IT services for secure IT infrastructure enabling data protection. The businesses deploy market players' expertise in IT services to reduce organization-wide data-related risks. The BFSI sector is driving the market since recruiting specialists with advanced skills is time-consuming. To reduce the overall cost involved, the companies invest in outsourcing solutions.

- However, the lack of data security in cloud and server-based services is hindering the market's growth. Cloud-based services pose many specific security issues and challenges. Data is usually stored with a third-party provider and can be accessed over the internet in the cloud. This indicates that visibility and control over that data are limited. Nevertheless, growing demand for efficiency and scalable infrastructure and increasing cloud migration are driving the market.

IT Outsourcing (ITO) Market Trends

BFSI to be the Largest End-user Vertical

- Banking, financial services, and insurance (BFSI) is one of the major end-user verticals experiencing significant change in technology adoption, mainly due to the conditions brought on by the pandemic and the evolving competitive landscape.

- Financial organizations are increasingly outsourcing their process and services to third parties. Banks are capable of outsourcing everything from mailing campaigns to payment processing. Banks can only survive and attract customers with a robust and comprehensive in-house IT department or trusted outside partners. For instance, in March 2023, Orion Innovation, a digital and product development firm, announced the acquisition of Banktech Software Services Ltd, a banking implementation partner for financial institutions that will complement Orion's financial services for expertise, open banking solutions, and implementation capabilities to Banktech.

- The BFSI industry is also shifting toward the cloud, which presents new market opportunities. According to a recent survey by Google Cloud, around 41.4% of global tech and business leaders planned to invest in cloud-based services to manage their workloads. Also, as per data by Flexera software, there was growth in IT spending in 2022 and 2023, and the software industry experienced 18% spending, followed by cloud services with 16% spending in 2023.

- Modern customers need more personalized and streamlined access to banks' services. The transition to omnichannel platforms, which provide seamless access for all devices, can be carried out by IT outsourcers. Moreover, such platforms facilitate real-time data collection and analysis so that financial institutions can improve customers' experience. Hence, such developments are driving IT outsourcing in the banks.

- Overall, the BFSI industry's demand for IT outsourcing services will be fueled by the need for advanced cybersecurity, digital transformation, growing regulatory compliance, and innovative solutions to meet evolving customer expectations and industry trends.

Asia-Pacific is Expected to Dominate the Market

- China is one of the significant outsourcing destinations in the Asia-Pacific. The outsourcing industry considers benefits that the majority of the companies in the United States find attractive. Reduction in development costs plays a critical role in retaining the actual benefits of outsourcing.

- China has made significant efforts to transition from (cheap) employment manufacturing to high-end industrial production through digitization and industrialization. According to data from the Ministry of Commerce, China's outsourcing industry grew in 2023. The firms signed outsourcing contracts of USD 404 billion, a 17.6% growth from last year.

- India is a considerably mature global IT outsourcing destination with a vast range of options. IT outsourcing companies in the country are rapidly expanding operations worldwide due to an increasing demand for skilled software developers. The cost aspect and talented skill pool have played a critical role in ensuring the nation's dominance in the market.

- In Japan, based on recent technological advancements in IT, the scope of IT outsourcing in the country's business sector has expanded to include cloud computing, data protection, and cybersecurity. Owing to the ability to provide business functionality without the need for substantial infrastructure investment, cloud-computing services are increasingly being utilized.

- Overall, the countries in the region are expected to gain significantly in the coming years as the market continues to develop. In addition, the data center buildings in the region have fueled a significant demand. Also, with the data center market on the verge of maturing, significant revenues in upgrading infrastructure have been poised to develop IT outsourcing in the region.

IT Outsourcing (ITO) Market Overview

The IT outsourcing market exhibits significant fragmentation, featuring key industry players such as IBM Corporation, DXC Technologies, Accenture PLC, NTT Corporation, and Infosys Limited. These market participants employ various strategies, such as forming partnerships and pursuing acquisitions, to bolster their product portfolios and establish sustainable competitive advantages.

- In November 2023, DXC Technology, a global technology service company, and ServiceNow, a digital workflow company, announced a strategic partnership to transform customer service and workflow management globally. They aim to integrate ServiceNow's advanced analytics and AI from its ITSM Pro and process mining solutions into DXC platform X to drive innovation for joint customers.

- In July 2023, NTT DATA (global digital business and IT service leader) announced the launch of an outsourcing service for security management to prevent cyber attack incidents and minimize damage when incidents occur. The service was launched in Japan in July 2023 and expanded worldwide within the fiscal year (March 2024).

- In June 2023, Infosys acquired Danske Bank's IT operation in India, part of an IT outsourcing contract worth USD 454 million over five years, to focus on its digital transformation. Through this contract, the company introduced generative artificial intelligence into the services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Efficiency and Scalable IT Infrastructure

- 4.2.2 Organizations are Increasingly Focusing on IT as a means to Gain Differentiation by Relying on Outsourced Vendors

- 4.2.3 Ongoing Migration Toward the Cloud and Adoption of Virtualized Infrastructure

- 4.3 Market Challenges

- 4.3.1 Fragmented Nature of the Market And Growing Incidence of Data Breaches

- 4.3.2 Dynamic Needs of IT Structure Impacts the Cost of Customization for End Users

- 4.4 Impact of COVID-19 on the IT Outsourcing Industry

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET ANALYSIS

- 5.1 Trends Related to Onshoring and Offshoring

- 5.2 Breakdown of Outsourcing Industry - BPO vs IT-based Outsourcing

- 5.3 Impact of the Ongoing Commodification of IT Solutions

- 5.4 Analysis of IT Outsourcing and Managed Service Industry

- 5.5 Breakdown of the Major IT Outsourcing Segments - Application and Infrastructure

- 5.6 Impact of Digital Transformation and Emergence of "As-a-Service" Model

6 MARKET SEGMENTATION

- 6.1 By Organization Size

- 6.1.1 Small and Medium Enterprises

- 6.1.2 Large Enterprises

- 6.2 By End-user Vertical

- 6.2.1 BFSI

- 6.2.2 Healthcare

- 6.2.3 Media and Telecommunications

- 6.2.4 Retail and E-commerce

- 6.2.5 Manufacturing

- 6.2.6 Other End-user verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Poland

- 6.3.2.7 Belgium

- 6.3.2.8 Netherlands

- 6.3.2.9 Luxembourg

- 6.3.2.10 Sweden

- 6.3.2.11 Denmark

- 6.3.2.12 Norway

- 6.3.2.13 Finland

- 6.3.2.14 Iceland

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Indonesia

- 6.3.3.5 Vietnam

- 6.3.3.6 Malaysia

- 6.3.3.7 South Korea

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Colombia

- 6.3.5 Middle East and Africa

- 6.3.5.1 GCC

- 6.3.5.2 South Africa

- 6.3.5.3 Turkey

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 DXC Technologies

- 7.1.3 Accenture PLC

- 7.1.4 NTT Corporation

- 7.1.5 Infosys Limited

- 7.1.6 Tata Consultancy Services

- 7.1.7 Cognizant Technology Solutions Corporation

- 7.1.8 Capgemini SE

- 7.1.9 Wipro Limited

- 7.1.10 Andela Inc.

- 7.1.11 Wns Holding Ltd

- 7.1.12 Pointwest Technologies

- 7.1.13 ATOS SE

- 7.1.14 Amadeus IT Group

- 7.1.15 Specialist Computer Centres (SCC)

- 7.1.16 HCL Technologies Ltd