|

市场调查报告书

商品编码

1690770

太阳能-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

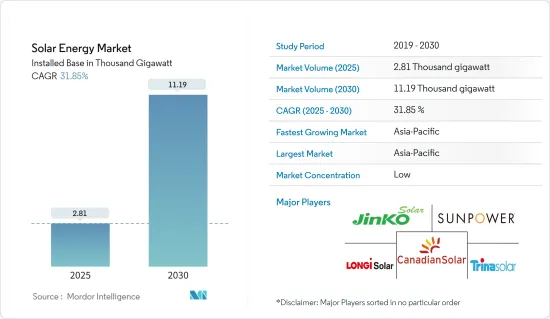

预计太阳能市场安装基数将从 2025 年的 2,810 吉瓦成长到 2030 年的 11,190 吉瓦,预测期间(2025-2030 年)的复合年增长率为 31.85%。

关键亮点

- 从中期来看,预计预测期内,政府的有利措施和太阳能发电系统价格的下降,以及太阳能板价格和安装成本的下降,将支持全球太阳能市场的成长。

- 另一方面,在研究期间,越来越多地采用替代清洁能源(例如燃气发电厂以及陆上和离岸风力发电计划)可能会阻碍市场成长。

- 预计太阳能和能源储存系统的整合将为未来市场创造许多机会。

- 在预测期内,由于中国、印度和其他国家的太阳能发电装置不断增加,亚太地区预计将成为太阳能市场规模最大、成长最快的地区。

太阳能市场趋势

光伏(PV)领域预计将占据市场主导地位

- 光伏系统使用由硅等半导体材料製成的太阳能板将阳光直接转化为电能。当阳光照射到太阳能电池时,它会激发电子并产生直流电 (DC)。然后,这种直流电透过家庭、企业和电网中的逆变器转换为交流电。

- 预计未来五年太阳能光电(PV)领域将占年度再生能源新增产能的最大份额,大大超过水力和风能。根据国际可再生能源机构(IRENA 2024)的数据,太阳能光电装置容量为1,412.093 GW,相对高于2020年的721.989 GW。

- 此外,由于人口成长、都市化以及交通运输等各领域的电气化,全球对电力的需求不断增加。太阳能光电系统提供了一种可扩展的分散式解决方案,以满足日益增长的能源需求,特别是在电网基础设施有限或不可靠的地区。

- 预计2023年全球太阳能光电年安装量将比2022年成长80%以上,併网装置容量将达到417 GWdc。在政府雄心勃勃的目标、政策支持和竞争加剧的推动下,未来对太阳能发电的投资预计将进一步成长。

- 根据国际能源总署 (IEA) 的数据,预计到 2024 年全球太阳能光电产能将达到约 1,000 吉瓦,足以满足 IEA 净零排放情境到 2050 年的年度需求(2030 年约为 650 吉瓦)。

- 美国、欧洲和印度政府都将太阳能供应链多元化作为优先事项,实施印度生产连结奖励计画计划(PLI)和美国通膨削减法案(IRA)等倡议,为国内製造商提供直接财政奖励,以更好地与中国製造商竞争。因此,预计 2022 年至 2023 年间将宣布超过 120% 的新太阳能製造计划,这有可能导致在每个地区建立产能超过 20GW 的国家太阳能供应链。

- 同时,印度在太阳能发电发展方面也取得了长足进展。 2023年,该国的太阳能发电容量将达到971万千瓦,比2022年增加15.4%。随着将竞标太阳能发电容量增加到每年40吉瓦的新目标以及国内供应链的蓬勃发展,预计太阳能成长将很快进一步加速。

- 此外,世界各国政府正在推出支持政策和财政奖励来鼓励采用太阳能。这些措施包括上网电价、税额扣抵、补贴和净计量计划。这些措施将降低前期成本、提高投资收益、促进电网整合,进而促进太阳能光电系统的普及。

- 例如,澳洲设定了2030年82%的电力来自太阳能和风能等可再生能源的目标,预计太阳能将对实现这一目标做出重大贡献。

- 因此,由于上述因素,预计公共产业部门将在预测期内主导太阳能市场。

亚太地区可望主导市场

- 包括中国、印度和日本在内的亚太地区许多国家都制定了雄心勃勃的可再生能源目标和支持政策,以鼓励采用太阳能。这些措施包括上网电价、可再生能源组合标准以及太阳能发电设施补贴。强而有力的政府支持和稳定的政策框架为该地区太阳能市场的成长创造了有利的环境。

- 根据国家能源局统计,2019年,全国风电累积设备容量约292万千瓦,与前一年同期比较增长13.9%,其中太阳能发电装置容量6094万千瓦,与前一年同期比较增长55.2%。此外,根据国家发展和改革委员会(NDRC)和国家能源局(NEA)的新指南,中国计划在2025年将分散式可再生能源容量扩大到500吉瓦。

- 此外,亚太国家正在经历快速人口成长和经济扩张,这也增加了对电力的需求。太阳能为日益增长的能源需求提供了可扩展、可持续的解决方案。因此,该地区太阳能应用的市场潜力巨大。

- 此外,亚太地区的几个国家正在实施雄心勃勃的大规模太阳能计划。例如,中国在公用事业规模的太阳能发电装置方面处于领先地位,拥有大型太阳能发电场和太阳能园区。这些大型计划将增加该地区的累积太阳能光电容量,并使其在全球太阳能光电市场中占据参与企业地位。

- 2024年4月,韦丹塔集团旗下的Serentica Renewables表示,计画投资高达3,000亿印度卢比(约35.9亿美元)。该公司的目标是到 2030 年实现 17 吉瓦的可再生能源。此外,印度跨国集团阿达尼集团宣布,计划在 2030 年之前投资约 23 亿印度卢比(约 275.5 亿美元),用于印度最雄心勃勃的可再生能源扩张以及太阳能和风能发电能力。

- 此外,亚太国家,尤其是中国,也正在成为太阳能光电模组和系统的主要製造地。该地区受益于规模经济、高效的供应链和具有竞争力的生产成本,大大降低了太阳能光电系统的总成本。这种成本优势正在帮助亚太地区主导全球太阳能市场。

- 因此,预计亚太地区将在预测期内主导太阳能市场。

太阳能产业概况

太阳能市场是细分的。市场上的主要企业(不分先后顺序)包括阿特斯太阳能公司、晶科能源控股、天合光能、SunPower Corporation 和隆基绿色能源科技。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章执行摘要

第三章调查方法

第四章 市场概述

- 介绍

- 2029年太阳能装置容量及预测(单位:吉瓦)

- 全球可再生能源结构(2023年)

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 政府奖励和政策

- 太阳能发电系统价格与安装成本下降

- 限制因素

- 越来越多采用替代清洁能源

- 驱动程式

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 技术部门

- 光伏(PV)

- 概述

- 光伏(PV)装置容量及2029年预测

- 2023年太阳能发电出货量(单位:GW)

- 2023年太阳能光电出货量份额(依技术划分)

- 截至2023年太阳能电池组件平均售价(单位:美元/瓦)

- 主要计划资讯

- 聚光型太阳热能发电(CSP)

- 概述

- 聚光型太阳热能发电(CSP)装置容量及2029年预测

- 2023年投入营运的太阳热能发电运作(吉瓦)

- 按集热器类型分類的太阳热能发电装置容量份额(%)(2023年)

- 主要计划资讯

- 光伏(PV)

- 市场分析:按地区分類的市场规模及至2028年的需求预测(按地区划分)

- 北美洲

- 美国

- 墨西哥

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 西班牙

- 义大利

- 英国

- 法国

- 北欧的

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 越南

- 韩国

- 马来西亚

- 泰国

- 印尼

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 奈及利亚

- 南非

- 中东和非洲

- 北美洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd

- Trina Solar Co. Ltd

- SunPower Corporation

- LONGi Green Energy Technology Co. Ltd

- First Solar Inc.

- JA Solar Holding

- Abengoa SA

- Acciona SA

- Brightsource Energy Inc.

- Engie SA

- NextEra Energy Inc.

- ACWA Power

- Sharp Corporation

- REC Solar Holdings AS

- Hanwha Corporation

- 市场排名分析

第七章 市场机会与未来趋势

- 能源储存系统係统集成

简介目录

Product Code: 71528

The Solar Energy Market size in terms of installed base is expected to grow from 2.81 thousand gigawatt in 2025 to 11.19 thousand gigawatt by 2030, at a CAGR of 31.85% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, favorable government policies and declining prices and installation costs of solar PV systems, along with the declining price of solar panels and installation costs, are likely to support the global solar energy market's growth during the forecast period.

- On the other hand, factors such as the rising adoption of alternate clean power sources, such as gas-fired power plants and onshore and offshore wind projects, are likely to hinder the market growth during the study period.

- Nevertheless, the integration of solar energy with energy storage systems is expected to create several opportunities for the market in the future.

- During the forecast period, Asia-Pacific is expected to be the largest and fastest-growing region in the solar energy market due to the increasing solar installations in China, India, and other countries.

Solar Energy Market Trends

Solar Photovoltaic (PV) Segment Expected to Dominate the Market

- Solar PV systems convert sunlight directly into electricity using solar panels made up of semiconductor materials, typically silicon. When sunlight strikes the solar cells, it excites electrons, generating a flow of direct current (DC) electricity. This DC electricity is converted into alternating current (AC) using an inverter in homes, businesses, and the electrical grid.

- The solar photovoltaic (PV) segment is expected to account for the most significant yearly capacity additions for renewables, well above hydro and wind, for the next five years. According to the International Renewable Energy Agency (IRENA 2024), Solar PV installed capacity accounted for 1412.093 GW, comparatively higher than the 721.989 GW installed in 2020.

- Additionally, the global electricity demand is continuously increasing due to population growth, urbanization, and the electrification of various sectors, including transportation. Solar PV systems offer a scalable and decentralized solution to meet this growing energy demand, particularly in regions with limited or unreliable grid infrastructure.

- Global solar PV annual installations grew by over 80% in 2023 compared to 2022, reaching 417 GWdc of grid-connected installed capacity. Due to ambitious government targets, policy support, and increasing competitiveness, investments in PVs are expected to grow further in the coming years.

- According to the International Energy Agency (IEA), global solar PV manufacturing capacity is expected to reach almost 1,000 GW in 2024, adequate to meet the annual demand for IEA Net Zero Emissions by 2050 scenario of almost 650 GW in 2030.

- Governments in the United States, Europe, and India have started to prioritize solar PV supply chain diversification, implementing policies such as India's Production Linked Incentive (PLI) scheme and the US Inflation Reduction Act (IRA) to provide direct financial incentives for domestic manufacturers to increase their competitiveness with Chinese ones. As a result, over 120% more new solar PV manufacturing projects were announced from 2022 to 2023 to potentially create national PV supply chains with over 20 GW of capacity in each region.

- On the other hand, India is witnessing significant developments in solar PV deployments. The country installed 9.71 GW of solar PV in 2023, 15.4% more than in 2022. A new target to increase PV capacity auctioned to 40 GW annually, and the dynamic development of the domestic supply chain is expected to result in a further acceleration in PV growth shortly.

- Moreover, governments worldwide have introduced supportive policies and financial incentives to promote solar PV installations. These measures include feed-in tariffs, tax credits, grants, and net metering programs. Such policies encourage the adoption of solar PV systems by reducing upfront costs, improving investment returns, and facilitating grid integration.

- For instance, Australia has set a goal of generating 82% of its electricity through renewable sources like solar PV and wind by 2030, and solar PV is expected to be a significant contributor to achieving this target.

- Therefore, based on the abovementioned factors, the utility sector is expected to dominate the solar energy market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Many countries in Asia-Pacific, such as China, India, and Japan, have implemented ambitious renewable energy targets and supportive policies to encourage solar energy adoption. These policies include feed-in tariffs, renewable portfolio standards, and subsidies for solar installations. Strong government support and stable policy frameworks have created a conducive environment for the region's solar energy market growth.

- According to the China National Energy Agency, China's cumulative installed power capacity reached approximately 2.92 TW, a 13.9% increase year over year, with solar power accounting for 609.49 GW, a 55.2% jump year over year. Also, according to the new guidelines from the National Development and Reform Commission (NDRC) and the National Energy Administration (NEA), China plans to expand its distributed renewable energy capacity to 500 GW by 2025.

- Furthermore, the countries in Asia-Pacific have a rapidly growing population and expanding economies, leading to an increasing demand for electricity. Solar energy offers a scalable and sustainable solution to this growing energy demand. As a result, there is a strong market potential for solar energy deployment in the region.

- Moreover, several countries in Asia-Pacific have undertaken ambitious large-scale solar energy projects. For instance, China has been a leader in utility-scale solar installations, with extensive solar farms and solar parks. These large-scale projects have boosted the region's cumulative solar capacity and positioned it as a dominant player in the global solar market.

- In April 2024, Serentica Renewables, part of Vedanta Group, announced that it plans to invest up to INR 30,000 crore (~USD 3.59 billion). The company aims to achieve 17 GW of renewable energy by 2030. Also, Adani Group, an Indian multinational conglomerate, announced that it is planning to invest around INR 2.3 lakh crore (~USD 27.55 billion) through 2030 in India's most ambitious renewable energy expansion and solar and wind manufacturing capacity addition.

- Moreover, Asia-Pacific countries, particularly China, have also emerged as major manufacturing hubs for solar PV components and systems. The region benefits from economies of scale, efficient supply chains, and competitive production costs, significantly reducing the overall cost of solar energy systems. This cost advantage has contributed to the dominance of Asia-Pacific in the global solar energy market.

- Therefore, Asia-Pacific is expected to dominate the solar energy market during the forecast period.

Solar Energy Industry Overview

The solar energy market is fragmented. Some of the key players in the market (in no particular order) include Canadian Solar Inc., JinkoSolar Holding Co. Ltd, Trina Solar Co. Ltd, SunPower Corporation, and LONGi Green Energy Technology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Energy Installed Capacity and Forecast in GW, till 2029

- 4.3 Global Renewable Energy Mix, 2023

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Government Incentives and Policies

- 4.6.1.2 Declining Price and Installation Cost of Solar PV Systems

- 4.6.2 Restraints

- 4.6.2.1 Rising Adoption of Alternate Clean Power Sources

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGEMENTATION

- 5.1 Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.1.1 Overview

- 5.1.1.2 Solar Photovoltaic (PV) Installed Capacity and Forecast, till 2029

- 5.1.1.3 Annual Solar PV Shipments, in GW, till 2023

- 5.1.1.4 Share of Solar PV Shipments (%), by Technology, 2023

- 5.1.1.5 Average Selling Price of Solar PV Module, in USD/W, till 2023

- 5.1.1.6 Key Projects Information

- 5.1.2 Concentrated Solar Power (CSP)

- 5.1.2.1 Overview

- 5.1.2.2 Concentrated Solar Power (CSP) Installed Capacity and Forecast, till 2029

- 5.1.2.3 Solar Thermal Capacity in Operation, in GW, till 2023

- 5.1.2.4 Solar Thermal Installed Capacity Share (%), by Collector Type, 2023

- 5.1.2.5 Key Projects Information

- 5.1.1 Solar Photovoltaic (PV)

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Mexico

- 5.2.1.3 Canada

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 Spain

- 5.2.2.3 Italy

- 5.2.2.4 United Kingdom

- 5.2.2.5 France

- 5.2.2.6 NORDIC

- 5.2.2.7 Turkey

- 5.2.2.8 Russia

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Vietnam

- 5.2.3.6 South Korea

- 5.2.3.7 Malaysia

- 5.2.3.8 Thailand

- 5.2.3.9 Indonesia

- 5.2.3.10 Rest of Asia-pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Chile

- 5.2.4.4 Colombia

- 5.2.4.5 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 Nigeria

- 5.2.5.5 South Africa

- 5.2.5.6 Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Canadian Solar Inc.

- 6.3.2 JinkoSolar Holding Co. Ltd

- 6.3.3 Trina Solar Co. Ltd

- 6.3.4 SunPower Corporation

- 6.3.5 LONGi Green Energy Technology Co. Ltd

- 6.3.6 First Solar Inc.

- 6.3.7 JA Solar Holding

- 6.3.8 Abengoa SA

- 6.3.9 Acciona SA

- 6.3.10 Brightsource Energy Inc.

- 6.3.11 Engie SA

- 6.3.12 NextEra Energy Inc.

- 6.3.13 ACWA Power

- 6.3.14 Sharp Corporation

- 6.3.15 REC Solar Holdings AS

- 6.3.16 Hanwha Corporation

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Energy Storage Systems Integration

02-2729-4219

+886-2-2729-4219

2026年全球太阳能市场报告

2026年全球太阳能市场报告 太阳能发电系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、安装类型、最终用户、功能及设备划分

太阳能发电系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、安装类型、最终用户、功能及设备划分 东南亚太阳能:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国太阳能:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙太阳能:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)越南太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

东南亚太阳能:市场占有率分析、产业趋势与统计、成长预测(2026-2031)泰国太阳能:市场占有率分析、产业趋势与统计、成长预测(2026-2031)西班牙太阳能:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)越南太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 太阳能解决方案市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争格局划分,2021-2031年)义大利太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)菲律宾太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

太阳能解决方案市场 - 全球产业规模、份额、趋势、机会及预测(按类型、应用、地区和竞争格局划分,2021-2031年)义大利太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)印尼太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)菲律宾太阳能市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

▼