|

市场调查报告书

商品编码

1690854

美国紧急照明:市场占有率分析、行业趋势和成长预测(2025-2030 年)United States Emergency Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

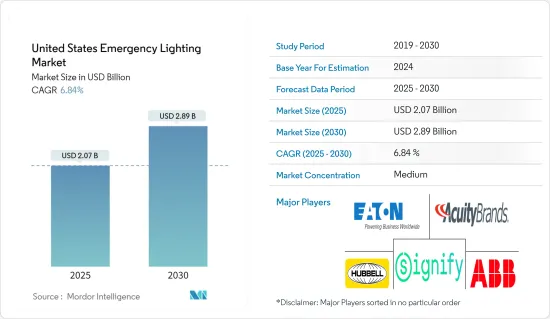

美国紧急照明市场规模预计在 2025 年为 20.7 亿美元,预计到 2030 年将达到 28.9 亿美元,在市场估计和预测期(2025-2030 年)内以 6.84% 的复合年增长率增长。

在新冠疫情爆发期间,市场出现生产停顿和供应链中断,导致工业生产成长放缓,主要製造地的照明製造业产量下降。

关键亮点

- 紧急照明系统是建筑物中最重要的安全系统之一。如果发生紧急情况,您可以按照紧急照明安全地停止事情并疏散建筑物。紧急照明是一种独立的备用系统,不依赖建筑物内一般配电系统的运作。它必须始终可用。

- 美国是最大的紧急照明市场之一,主要受政府法规的推动。在美国,职业安全与健康管理局 (OSHA) 承认国家消防协会 (NFPA) 生命安全规范 (101) 的紧急照明标准,表明雇主如何满足一般职责要求以确保职场的安全。这些标准要求所有逃生路线(包括走廊和通道)都安装紧急照明。

- 根据美国建筑师协会预测,未来五年建筑支出预计将会增加。就近期预测而言,预计到 2020 年底美国非住宅建筑市场将年增与前一年同期比较%(此预测可能受到 COVID-19 情境的影响)。

- 根据美国人口普查局的数据,美国住宅建筑收入从 2010 年 1 月的 3 亿美元增加到 2018 年 1 月的 6 亿美元,而非住宅建筑收入从 2010 年 1 月的 6 亿美元增加到 2018 年 1 月的 8 亿美元。建筑业的这种成长预计将为住宅、商业和工业应用创造市场机会。

美国紧急照明市场趋势

互联繫统和物联网 (IoT) 的发展以及 LED 价格的下降正在推动市场

- 连接系统和物联网 (IoT) 的发展,即整合到系统结构中的中央管理主机,透过为客户提供控制、设施监控和补救服务的应用,对紧急照明市场产生了积极影响。

- 儘管具有用户友好的自我检查功能,但在大型商业建筑中目视检测紧急照明系统仍然容易出现人为错误。物联网技术正在应用于此类应用中,以简化现代紧急照明系统的维护和检查。

- 物联网技术的先决条件包括透过有线连接或无线技术为紧急照明系统添加网路连接。其结果是一个可以远端监控和自我诊断的连接紧急照明系统。这项概念的发展始于20年前,但由于成本和技术复杂性,市场尚未做好准备。随着智慧建筑和完全整合的建筑管理系统逐渐被接受,联网紧急照明的概念在过去三年中重新流行起来。

- 工业环境中的 LED 可节省高达 70% 的能源,相关的紧急照明变得高度可控。此外,LED与安防产业的整合也日益加强。 LED 灯具效率更高,并且透过指示器(显示稳定或闪烁的红色或绿色 LED 来指示系统何时准备就绪)简化了紧急照明的测试。这些是北美标准(例如 CSA C22.2 NO.141)所要求的。

- 专用 LED 驱动器和控制模组的开发为连接的紧急照明和建筑系统提供了额外的可编程性,包括远端维护和监控、调光、电力计量、资料收集和试运行。随着越来越多的建筑业主进行 LED维修以节约能源,使用具有无线通讯的智慧 LED 照明灯具维修是一种经济有效的方法。

商业领域占据主导市场占有率

- 2020年,新冠疫情对商业建筑建设产生了负面影响。然而,随着未来几年疫苗接种的快速推进,该行业有望反弹。

- 根据国家消防协会 (NPFA) 生命安全规范 101,全国所有商业建筑都必须配备紧急和疏散照明。该规范每三年更新一次,旨在保护新建和现有设施中的居住者免受火灾和其他危害。

- 此外,就亮度水平而言,商业建筑的紧急照明在一个半小时内的任何时间都不应低于 6.5 勒克斯。此外,均匀度比率不得超过 40:1。照明系统必须由发电机或电池备用供电。这些规定仿照办公大楼、餐厅、零售店和其他商业建筑的紧急照明要求制定。

- 根据美国能源部 (DOE) 的数据,商业建筑每平方英尺的平均千瓦时用电量约为 22.5 kWh/sq ft。在总消费量中,照明约占 7 kWh/sq ft,仅次于冷藏和冷冻设备(8 kWh/sq ft)。商用照明的高能耗催生了对节能商用紧急照明的需求。

美国紧急照明产业概况

美国紧急照明市场竞争适中,新参与企业较多,主导市场占有率较少。公司不断创新并建立战略伙伴关係以保持市场占有率。

- 2021 年 2 月 - Accuity Brands Inc. 宣布将纽约数位代理商出售给 Illuminations Inc.。透过 Illuminations Inc.,该公司有绝佳的机会在全球最大的照明市场之一加强其品牌影响力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概览

- 技术简介

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 市场驱动因素

- 对节能照明系统和有利的政府法规的需求不断增加

- LED产品价格下跌

- 市场问题

- 前期投资高,替代技术开发

- 法规政策

- COVID-19对紧急照明市场的影响

- 按应用程式对市场进行定性分析(待命与疏散路线 - 恐慌措施和标誌)

第五章市场区隔

- 类型

- 自主型

- 中央供给型

- 最终用户

- 商用

- 工业的

- 教育机构

- 医疗保健

- 其他的

第六章竞争格局

- 公司简介

- Acuity Brands Inc.

- Eaton Corporation PLC

- ABB Ltd

- Hubbell Incorporated

- Signify NV(Including Cooper Lighting Solutions)

- Legrand SA

- Emerson Electric Co.

- Encore Lighting

- Myers Emergency Power Systems

- Larson Electronics

- Cree Inc.

- Digital Lumens Inc.

第七章投资分析

第八章:市场的未来

The United States Emergency Lighting Market size is estimated at USD 2.07 billion in 2025, and is expected to reach USD 2.89 billion by 2030, at a CAGR of 6.84% during the forecast period (2025-2030).

Amid the outbreak of COVID-19, the market was witnessing halting of production and disruption in the supply chain, leading to weakened growth of industrial output and the decline of light-manufacturing output across significant manufacturing hubs.

Key Highlights

- An emergency lighting system is one of the most critical safety systems in a building. It makes it possible to stop things safely and evacuate the building by following the exit lights in case of an emergency. Emergency lighting is a standalone backup system that does not depend on the functionality of the general electrical distribution system in the building. It must always be operational and ready for use.

- The United States is one of the largest markets for emergency lighting, primarily driven by government regulations. In the country, the Occupational Safety and Health Administration (OSHA) recognizes the National Fire Protection Association (NFPA) Life Safety Code (101) standards for emergency lighting as providing instructions for how employers can meet their general duty requirements for ensuring a safe workplace. These standards need all exit routes, including corridors, aisles, and the like, to have emergency lighting.

- As per the American Institute of Architects, construction spending is expected to grow over the next five years. Based on short-term projections, the US non-residential construction market is anticipated to grow to 2.4% by the end of 2020, as compared to the previous year (this forecast may have been affected by the COVID-19 scenario).

- According to the US Census Bureau, in the US residential construction sector, revenue increased from USD 0.3 billion in January 2010 to USD 0.6 billion in January 2018, and non-residential construction revenue increased from USD 0.6 billion in January 2010 to USD 0.8 billion in January 2018. Such growth in the construction sector is expected to create opportunities for the market across residential, commercial, and industrial applications.

US Emergency Lighting Market Trends

Development of Connected Systems and Internet of Things (IoT) and Declining Prices of LED to Drive the Market

- The development of connected systems and the Internet of Things (IoT), a central management console integrated into the system architecture, offers the customers control, the ability to monitor facilities, and apply remediation services, thus actively affecting the emergency lighting market.

- Despite the user-friendly self-testing feature, the task remains prone to human error to visually detect the emergency lighting system in a large commercial building. IoT technology is applied to simplify the maintenance and inspection of modern emergency lighting systems in such applications.

- It is done via wire-connection or wireless technology, with the prerequisite of adding network connectivity to the emergency lighting system. And the resultant is a connected emergency lighting system for remote monitoring and self-test. The concept development was done 20 years back, but the market was not ready due to cost and technology complexity. The growing and gradual acceptance of smart building and fully integrated building management systems has brought the connected emergency lighting concept back in the last three years.

- As LEDs in an industrial environment deliver savings up to 70%, the concerned emergency lights become highly controllable. Additionally, the integration of LEDs with the security industry is growing. LED luminaires are more efficient and simplify emergency lighting testing with indicators to display red or green solid or flashing LEDs for system readiness. These are required by standards such as CSA C22.2 NO. 141 in North America.

- Development of specialty LED drivers and control modules offer additional programmability to connected emergency lighting and building systems such as remote maintenance and monitoring, dimming, power metering, data collection, commissioning, to name a few. With more building owners contracting for LED retrofits to save energy, retrofitting with smart LED luminaires with on-board wireless communications is a cost-effective approach.

Commercial Sector to Dominate Market Share

- The COVID-19 pandemic negatively impacted the construction of commercial buildings in 2020. However, the industry is expected to bounce back in line with the rapid vaccination drive in the coming years.

- According to the National Fire Protection Association's (NPFA) Life Safety Code 101, all commercial buildings in the country must have emergency and exit path lighting. Every three years, the code is updated to ensure new and existing facilities offer protection from fire and other related hazards for occupants.

- In addition, when it comes to brightness levels, the commercial emergency lights must not fall below 6.5 lux at any point of time during the hour and a half mark. Furthermore, the uniformity ratio must not go above 40:1. The lighting system must have a power supply either from a generator or battery backup. Such regulations mold the requirements of emergency lights for office buildings, restaurants, retail stores, and other commercial buildings.

- According to the Department of Energy (DOE), the average number of kilowatt-hours per square foot for a commercial building is approximately 22.5 kWh/square foot. Out of the total consumption, the lighting solely accounts for roughly 7kWh/square foot, which is the second-highest post refrigeration and equipment (8kWh/square foot). The high level of energy consumption by commercial lighting is developing a need for energy-efficient commercial emergency lights.

US Emergency Lighting Industry Overview

The US emergency lighting market is moderately competitive, with new firms entering the market and few firms enjoying a dominant market share. The companies keep on innovating and entering strategic partnerships to retain their market share.

- February 2021 - Accuity Brands Inc. announced that it was selling New York Digital Agency to Illuminations Inc., which aligns with its ongoing transformation strategy to increase customer value and sustainably grow its business significantly. Through Illuminations Inc., the company has a tremendous opportunity to strengthen its brand presence in one of the largest lighting markets in the world.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Technology Snapshot

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Market Drivers

- 4.5.1 Increase in Need for Energy-efficient Lighting Systems and Favorable Government Regulations

- 4.5.2 Declining Prices of LED Products

- 4.6 Market Challenges

- 4.6.1 High Initial Investment and Development of Alternative Technologies

- 4.7 Regulations and Policies

- 4.8 Impact of COVID-19 on the Emergency Lighting Market

- 4.9 Qualitative Analysis of the Market by Application (Stand-by vs Escape Route - Anti-panic and Signage)

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Self-sustained

- 5.1.2 Centrally Supplied

- 5.2 End User

- 5.2.1 Commercial

- 5.2.2 Industrial

- 5.2.3 Educational

- 5.2.4 Healthcare

- 5.2.5 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Acuity Brands Inc.

- 6.1.2 Eaton Corporation PLC

- 6.1.3 ABB Ltd

- 6.1.4 Hubbell Incorporated

- 6.1.5 Signify NV (Including Cooper Lighting Solutions)

- 6.1.6 Legrand SA

- 6.1.7 Emerson Electric Co.

- 6.1.8 Encore Lighting

- 6.1.9 Myers Emergency Power Systems

- 6.1.10 Larson Electronics

- 6.1.11 Cree Inc.

- 6.1.12 Digital Lumens Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

紧急照明电池市场:按最终用途、电池化学成分、应用和分销管道划分-2026-2032年全球市场预测

紧急照明电池市场:按最终用途、电池化学成分、应用和分销管道划分-2026-2032年全球市场预测 全球国防紧急电池市场(2026-2036)商用出口照明灯具市场:依光源、安装类型、电源类型、终端用户和通路划分-全球预测,2026-2032年

全球国防紧急电池市场(2026-2036)商用出口照明灯具市场:依光源、安装类型、电源类型、终端用户和通路划分-全球预测,2026-2032年 紧急照明市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、形状、材料类型和最终用户划分

紧急照明市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、形状、材料类型和最终用户划分 全球紧急照明市场:市场规模、占有率、成长率、依类型和应用划分的产业分析、区域洞察及未来预测(2026-2034)

全球紧急照明市场:市场规模、占有率、成长率、依类型和应用划分的产业分析、区域洞察及未来预测(2026-2034) 2026年全球紧急照明市场报告2026年发光二极体(LED)紧急照明中央电池供电全球市场报告可充电LED紧急照明市场按类型、电池类型、功率等级、最终用途和分销管道划分-2026-2032年全球预测紧急警告照明市场:按光源、产品、通路、应用、最终用户和安装类型划分-2026-2032年全球预测

2026年全球紧急照明市场报告2026年发光二极体(LED)紧急照明中央电池供电全球市场报告可充电LED紧急照明市场按类型、电池类型、功率等级、最终用途和分销管道划分-2026-2032年全球预测紧急警告照明市场:按光源、产品、通路、应用、最终用户和安装类型划分-2026-2032年全球预测 紧急照明市场规模、份额和成长分析(按组件、电源系统、电池类型、光源、应用和地区划分)—产业预测(2026-2033 年)

紧急照明市场规模、份额和成长分析(按组件、电源系统、电池类型、光源、应用和地区划分)—产业预测(2026-2033 年)