|

市场调查报告书

商品编码

1690864

卫星通讯:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Satellite Communications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

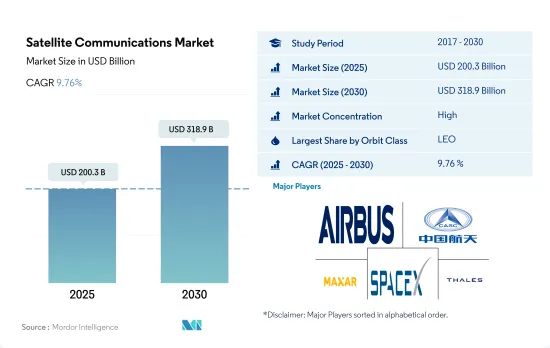

卫星通讯市场规模预计在 2025 年达到 2,003 亿美元,到 2030 年将达到 3,189 亿美元,预测期内(2025-2030 年)的复合年增长率为 9.76%。

低地球轨道卫星有望占据该领域的主导地位

- 卫星和太空船通常被放置在围绕地球的许多特殊轨道之一中。地球轨道有三种:地球静止轨道(GEO)、中地球轨道(MEO)和低地球轨道(LEO)。许多气象和通讯往往在距离地球表面最远的高地球轨道上运行。中地球轨道卫星包括导航卫星和用于监测特定区域的专用卫星。大多数科学卫星,包括美国太空总署的地球观测系统,都在低地球轨道上运行。

- 小型卫星的快速发展及其因附加优势而在低地球轨道的部署正在推动低地球轨道领域成长。 2017年至2019年,GEO卫星占据了市场的大部分份额。低地球轨道卫星在 2020 年发展势头强劲,预计在预测期内将继续保持成长轨迹。到 2029 年,低地球轨道 (LEO) 预计将占据 79.5% 的市场占有率,其次是地球静止轨道 (GEO),占有 18% 的份额。

- 每颗製造和发射的卫星的用途各不相同。 2017年至2022年期间,MEO发射的57颗卫星中,有8颗用于通讯目的。同样,在 GEO 中,147 颗卫星中有 105 颗用于通讯目的。目前,全球约有 4,131 颗低地球轨道卫星已经建造并发射,由世界各地的各个组织拥有。其中约2976颗是用于通讯目的的卫星。

通讯应用需求不断成长,推动全球市场

- 卫星通讯市场是一个全球性产业,通讯、军事和国防以及广播等多个领域提供关键基础设施。卫星发射方面,2017年至2022年间,约80%的通讯将在北美製造和发射,其次是欧洲(15%)、中国(3%)、其他国家(2%)。

- 北美拥有强大的军事和国防部门,在卫星技术方面投入了大量资金,同时也拥有重要的商业部门,SpaceX、MDA、HughesNet 和 Telesat 等公司经营大型卫星编队,用于宽频网路、电视广播和其他服务。

- 主要卫星製造商包括泰雷兹阿莱尼亚航太公司和空中巴士防务与航太公司。欧洲太空总署(ESA)大力投资太空技术,以支持国家安全和国防倡议。商业卫星通讯市场也十分重要,欧洲通讯卫星组织和 SES 等公司经营大量卫星编队,用于通讯、广播和其他服务。

- 受高速资料传输需求成长和卫星技术投资增加的推动,亚太地区卫星通讯市场预计将快速成长。中国和印度是该地区最大的两个市场,两国都在大力投资太空技术,以支持其国家安全和防御倡议并促进经济成长。

全球卫星通讯市场趋势

全球对小型卫星的需求不断增加

- 小型卫星能够提供传统卫星的几乎所有功能,而成本却仅为传统卫星的一小部分,这使得建造、发射和操作小型卫星星系变得越来越可行。北美的需求主要由美国推动,美国每年生产的小型卫星最多。 2017 年至 2022 年间,北美地区的各参与者总合596 颗奈米卫星发射入轨道。美国宇航局目前参与了多个旨在开发这些卫星的计划。

- 欧洲拥有多家知名卫星製造营业单位,如萨里卫星技术有限公司和GomSpace Group AB,是奈米卫星製造的中心。 2018 年 11 月,欧空局宣布参与设计一款低成本 35 公斤月球通讯任务,称为 DoT-4,计画于 2021 年发射。 DoT-4 的设计目的是利用 Goonhilly 深空网路将通讯传递到地球并与月球表面的探测车建立连接。

- 亚太地区的需求主要受到中国、日本和印度的推动,这三个国家每年生产的小型卫星最多。 2017年至2022年期间,该地区各参与者已将190多颗奈米卫星发射入轨道。中国正投入大量资源来增强其太空能力。中国是迄今为止亚太地区发射微型卫星最多的国家。

增加市场投资机会

- 2021年,北美政府在太空开发上的支出达到约370亿美元。该地区是太空创新和研究的中心,也是全球最大的航太机构美国太空总署的所在地。 2022年,美国政府将在太空计画上投入约620亿美元,成为全球在太空计画上投入最多的国家。在美国,联邦机构每年从国会获得 323.3 亿美元的资金,也就是预算。

- 英国政府计画投入 75 亿美元升级军方的卫星通讯能力。 2020 年 7 月,英国国防部授予空中巴士防务与航太公司一份价值 6.3 亿美元的合同,用于建造新的通讯,作为增强其军事能力的权宜之计。 2022年11月,欧空局提案在未来三年内增加25%的太空资金,以维持欧洲在地球观测领域的领先地位,扩大导航服务,并继续作为美国的探勘伙伴。欧空局已要求22个国家提交2023年至2025年约185亿欧元的预算。

- 鑑于亚太地区太空相关活动的增加,日本的预算提案估计其2022年的太空预算将超过14亿美元,其中包括H3火箭、工程测试卫星-9和情报收集卫星(IGS)计画的研发。印度2022财年的太空预算为18.3亿美元。韩国科学技术通讯通讯部宣布,2022 年太空预算为 6.19 亿美元,用于生产卫星、火箭和其他主要太空设备。

卫星通讯产业概况

卫星通讯市场格局较为集中,前五大公司占98.46%的市占率。该市场的主要企业是:空中巴士公司、中国航太科技集团公司(CASC)、麦克萨技术公司、太空探索技术公司和泰雷兹公司(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第 3 章 简介

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 卫星小型化

- 卫星质量

- 空间支出

- 法律规范

- 世界

- 澳洲

- 巴西

- 加拿大

- 中国

- 法国

- 德国

- 印度

- 伊朗

- 日本

- 纽西兰

- 俄罗斯

- 新加坡

- 韩国

- 阿拉伯聯合大公国

- 英国

- 美国

- 价值链与通路分析

第五章 市场区隔

- 卫星质量

- 10-100kg

- 100-500kg

- 500-1000kg

- 10公斤以下

- 1000kg以上

- 轨道级

- GEO

- LEO

- MEO

- 最终用户

- 商业的

- 军事和政府

- 其他的

- 地区

- 亚太地区

- 欧洲

- 北美洲

- 世界其他地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 业务状况

- 公司简介.

- Airbus SE

- China Aerospace Science and Technology Corporation(CASC)

- Cobham Limited

- EchoStar Corporation

- Intelsat

- L3Harris Technologies Inc.

- Maxar Technologies Inc.

- SES SA

- SKY Perfect JSAT Corporation

- Space Exploration Technologies Corp.

- Swarm Technologies, Inc.

- Thales

- Thuraya Telecommunications Company

- Viasat, Inc.

第七章:执行长的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源和进一步阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 72146

The Satellite Communications Market size is estimated at 200.3 billion USD in 2025, and is expected to reach 318.9 billion USD by 2030, growing at a CAGR of 9.76% during the forecast period (2025-2030).

LEO satellites are expected to comprise the leading segment

- A satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. There are three types of Earth orbits: geostationary orbit (GEO), medium Earth orbit (MEO), and low Earth orbit (LEO). Many weather and communications satellites tend to have high Earth orbits, which are farthest from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- The rapid development of small satellites and their deployment in low Earth orbit because of their added advantages are driving the growth of the LEO segment. During 2017-2019, the majority share of the market was occupied by GEO satellites. In 2020, LEO satellites gained momentum, and they are expected to continue their growth trajectory during the forecast period as well. The LEO segment is expected to occupy a market share of 79.5% in 2029, followed by GEO, with a share of 18%.

- The different satellites manufactured and launched have different applications. During 2017-2022, of the 57 satellites launched in MEO, eight were built for communication purposes. Similarly, of the 147 satellites in GEO, 105 were deployed for communication purposes. Around 4,131 LEO satellites manufactured and launched were owned by various organizations across the world. Of that, nearly 2,976 satellites were designed for communication purposes.

Rising demand for communication application is driving the demand in the market globally

- The satellite communications market is a global industry that provides critical infrastructure for various sectors, including telecommunications, military and defence, and broadcasting. Regarding satellite launches, during 2017-2022, approximately 80% of the communication satellites were manufactured and launched by North America, followed by Europe with 15%, China with 3%, and the rest with 2%, respectively.

- North America has a strong military and defence sector that invests heavily in satellite technology, and the commercial sector is also significant, with companies like SpaceX, MDA, HughesNet, and Telesat operating large fleets of satellites for broadband internet, TV broadcasting, and other services.

- Europe is another significant player in the global satellite communications market, and it is home to several leading satellite manufacturers, including Thales Alenia Space and Airbus Defence and Space. The European Space Agency (ESA) invests heavily in space technology to support national security and defence initiatives. The commercial satellite communications market is also significant, with companies like Eutelsat and SES operating large fleets of satellites for communication, broadcasting, and other services.

- The Asia-Pacific region is expected to be the fastest-growing market for satellite communications, driven by increasing demand for high-speed data transmission and rising investments in satellite technology. China and India are two of the largest markets in the region, with both countries investing heavily in space technology to support national security and defence initiatives and drive economic growth.

Global Satellite Communications Market Trends

The global demand for satellite miniaturization is rising

- The ability of small satellites to perform nearly all of the functions of a traditional satellite at a fraction of its cost has increased the viability of building, launching, and operating small satellite constellations. The demand from North America is primarily driven by the United States, which manufactures the most small satellites each year. In North America, during 2017-2022, a total of 596 nanosatellites were placed in orbit by various players in the region. NASA is currently involved in several projects aimed at developing these satellites.

- Europe has become the hub for nano and microsatellite manufacturing due to the presence of several prominent satellite manufacturing entities in the region, including Surrey Satellite Technology Ltd and GomSpace Group AB. In November 2018, ESA announced its participation in designing a low-cost 35 kg lunar communications satellite mission called DoT-4, which was targeted for a 2021 launch. DoT-4 was designed to provide the communications relay back to Earth using the Goonhilly Deep Space Network and link up with a rover on the surface of the Moon.

- The demand from Asia-Pacific is primarily driven by China, Japan, and India, which manufacture the largest number of small satellites annually. During 2017-2022, more than 190 nano and microsatellites were placed into orbit by various players in the region. China is investing significant resources in augmenting its space-based capabilities. The country has launched the most significant number of nano and microsatellites in Asia-Pacific to date.

Investment opportunities are increasing in the market

- Government expenditure for space programs in North America reached approximately 37 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space programs in the world. In the United States, federal agencies receive funding of USD 32.33 billion from Congress every year, known as budgetary resources, for their subsidiaries.

- The UK government has planned an upgradation, worth USD 7.5 billion, of the satellite telecommunication capabilities of the armed forces. In July 2020, the UK Ministry of Defence (MoD) awarded a contract worth USD 630 million to Airbus Defence and Space for constructing a new telecommunications satellite as a stopgap to bolster military capabilities. In November 2022, ESA announced that it proposed a 25% boost in space funding over the next three years to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. ESA asked its 22 nations to back a budget of around EUR 18.5 billion for 2023-2025.

- Considering the increase in space-related activities in the Asia-Pacific region, in 2022, according to the draft budget of Japan, the space budget amounted to over USD 1.4 billion, which included the development of the H3 rocket, Engineering Test Satellite-9, and the nation's Information Gathering Satellite (IGS) program. The proposed budget for India's space programs for FY22 was USD 1.83 billion. In 2022, South Korea's Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment.

Satellite Communications Industry Overview

The Satellite Communications Market is fairly consolidated, with the top five companies occupying 98.46%. The major players in this market are Airbus SE, China Aerospace Science and Technology Corporation (CASC), Maxar Technologies Inc., Space Exploration Technologies Corp. and Thales (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Global

- 4.4.2 Australia

- 4.4.3 Brazil

- 4.4.4 Canada

- 4.4.5 China

- 4.4.6 France

- 4.4.7 Germany

- 4.4.8 India

- 4.4.9 Iran

- 4.4.10 Japan

- 4.4.11 New Zealand

- 4.4.12 Russia

- 4.4.13 Singapore

- 4.4.14 South Korea

- 4.4.15 United Arab Emirates

- 4.4.16 United Kingdom

- 4.4.17 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Satellite Mass

- 5.1.1 10-100kg

- 5.1.2 100-500kg

- 5.1.3 500-1000kg

- 5.1.4 Below 10 Kg

- 5.1.5 above 1000kg

- 5.2 Orbit Class

- 5.2.1 GEO

- 5.2.2 LEO

- 5.2.3 MEO

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Military & Government

- 5.3.3 Other

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.2 Europe

- 5.4.3 North America

- 5.4.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Airbus SE

- 6.4.2 China Aerospace Science and Technology Corporation (CASC)

- 6.4.3 Cobham Limited

- 6.4.4 EchoStar Corporation

- 6.4.5 Intelsat

- 6.4.6 L3Harris Technologies Inc.

- 6.4.7 Maxar Technologies Inc.

- 6.4.8 SES S.A.

- 6.4.9 SKY Perfect JSAT Corporation

- 6.4.10 Space Exploration Technologies Corp.

- 6.4.11 Swarm Technologies, Inc.

- 6.4.12 Thales

- 6.4.13 Thuraya Telecommunications Company

- 6.4.14 Viasat, Inc.

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

基于半导体的防伪系统市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形式、材质类型、设备和最终用户划分

基于半导体的防伪系统市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、形式、材质类型、设备和最终用户划分 军用商业卫星通讯:趋势与预测(2024-2034)

军用商业卫星通讯:趋势与预测(2024-2034) 卫星通讯市场-全球产业规模、份额、趋势、机会及预测(按组件、应用、垂直产业、地区及竞争格局划分,2021-2031年)

卫星通讯市场-全球产业规模、份额、趋势、机会及预测(按组件、应用、垂直产业、地区及竞争格局划分,2021-2031年) 卫星通讯市场规模、份额和趋势分析报告:按组件、卫星星系、频宽、应用、产业、地区和细分市场预测(2026-2033 年)卫星通讯:物联网应用及合约市场数据概览:2025 年第四季

卫星通讯市场规模、份额和趋势分析报告:按组件、卫星星系、频宽、应用、产业、地区和细分市场预测(2026-2033 年)卫星通讯:物联网应用及合约市场数据概览:2025 年第四季 5G非地面网路(NTN)服务市场按组件、平台类型、频宽、应用和最终用户划分-2026-2032年全球预测NTN商业服务市场:按服务类型、部署模式、产业和组织规模分類的全球预测(2026-2032年)卫星通讯单元市场按服务类型、平台类型、频段、最终用户和应用划分-全球预测,2026-2032年

5G非地面网路(NTN)服务市场按组件、平台类型、频宽、应用和最终用户划分-2026-2032年全球预测NTN商业服务市场:按服务类型、部署模式、产业和组织规模分類的全球预测(2026-2032年)卫星通讯单元市场按服务类型、平台类型、频段、最终用户和应用划分-全球预测,2026-2032年 中东卫星通讯市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

中东卫星通讯市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年) 全球卫星通讯(SATCOM)市场预测至2032年:按组件、轨道等级、频段、平台、最终用户和地区划分

全球卫星通讯(SATCOM)市场预测至2032年:按组件、轨道等级、频段、平台、最终用户和地区划分

▼