|

市场调查报告书

商品编码

1692453

交流 (AC)马达-市场占有率分析、行业趋势与统计、成长预测(2025-2030 年)Alternating Current (AC) Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

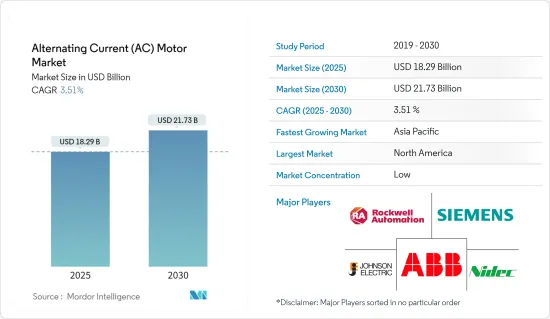

交流马达市场规模预计在 2025 年为 182.9 亿美元,预计到 2030 年将达到 217.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.51%。

主要亮点

- AC马达AC马达一种利用电磁感应现象将交流电转换为机械动力的马达。交流电驱动此马达。定子和转子是AC马达最重要的部件。定子是马达的静止部分,转子是马达的旋转部分。AC马达有单相和三相。

- 三相交流马达主要用于工业中将大量电能转换为机械能。单相交流AC马达主要用于小功率的转换。单相交流AC马达大多体积较小,在家庭、办公室、商业关係、工厂等提供各种服务。大多数电器产品,如冰箱、电风扇、洗衣机、烘干机和搅拌机,都使用单相交流AC马达。

- 预计在预测期内,电动车的普及将支持市场成长。多年来,汽车产业的日产量显着增加。根据国际汽车工业组织(OICA)的数据显示,去年全球汽车产量约8,500万辆,与前一年同期比较增加6%。去年,中国、日本和德国是最大的轿车和商用车生产国。

- AC马达将各种其他组件组合成一个物理单元。标准配置包括引擎和驱动器、整合式编码器、控制器、电缆和通讯连接埠。这增加了整个系统的成本。AC马达所需的资本投资高于其他传统马达,这对市场成长构成了挑战。

- 新冠疫情对全球市场的影响巨大,多个国家政府实施的防控措施对工业部门的成长产生了重大影响。结果,所研究的市场由于供应链问题而经历了放缓,尤其是在初始阶段。不过,随着主要终端用户产业全面恢復运营,智慧AC马达的需求预计将会增加。

交流马达市场趋势

石油和天然气产业预计将占据主要市场份额

- 石油和天然气产业在推动市场成长方面发挥关键作用。AC马达因其简单、可靠且价格实惠而广泛应用于该行业。AC马达为钻机系统和设备提供可靠、稳定的电力,在石油和天然气行业中发挥至关重要的作用。这些马达产生的能量为原油、天然气和石油等宝贵资源的开采、加工、储存和运输提供动力。感应马达和同步发电机用于为陆上和海上钻井作业的各种应用提供动力。

- 石油和天然气产业对AC马达的需求不断增长,这是由于人们越来越重视在恶劣运作环境下的能源效率和可靠性。此外,交流马达还具有卓越的速度控制和监控能力。由于交流电动机能够在各种环境条件下有效运行,并且与其他类型的电动马达相比具有更长的使用寿命,因此在陆上石油和天然气工业过程中对交流马达的采用显着增加。

- 额定电压低于 1 千伏特 (kV) 的交流电机经常用于石油和天然气设施中的较小设备,例如泵浦、风扇、鼓风机和小型压缩机。额定电压在1kV至6.6kV之间以及6.6kV以上的交流电机广泛应用于石油和天然气行业的中高功率应用。这些马达通常用于大型压缩机、发电机、泵浦和其他重型设备。额定电压高于 6.6kV 的交流马达具有几个值得注意的特点,包括提高功率输出、提高效率和提高过载能力。

- 根据国际能源总署(IEA)的最新预测,即使在目前的政策环境下,全球石油和天然气需求也将在未来几年达到高峰。国际能源总署预测,到本世纪末,全球石油需求将成长约 800 万桶/日,从而增加对海上活动的需求。由于海上作业和投资的增加,预计AC马达的需求将激增。这些马达用于各种海上应用,包括钻井钻机、生产平台、浮式生产储油卸油设备油船 (FPSO)、海底系统和其他海上设备。

- 此外,欧佩克报告称,近期全球原油消费量(包括生质燃料)为每天9,957万桶。预计未来几年这数字将增加至1.0189亿桶/日,最终达到1.098亿桶/日。预计轻质油和柴油的需求将从每天 2,760 万桶增至每天 3,010 万桶。预计这些因素将推动业界对AC马达的需求。

预计亚太地区市场将显着成长

- 中国正经历快速工业化进程,製造业、汽车业、电子业等各领域都在快速发展。AC马达广泛应用于泵浦、压缩机、输送机和风扇等工业机械设备,这推动了对AC马达的需求。

- 中国专注于高端製造业、电力事业以及石油和天然气工业,中国同时使用低压和中压驱动器。例如,中国政府雄心勃勃的「中国製造2025」倡议,部分受到德国工业4.0的启发,旨在提高中国在製造业的竞争力。

- 预计印度将占据全球AC马达市场的巨大份额。该国市场的发展受到製造业对马达日益增长的需求以及能源效率意识不断增强的推动。此外,预计能源成本的上升将加速各行各业对同步马达的采用。由于印度拥有大量马达製造商,预计该国在预测期内将占据相当大的市场占有率。

- 日本政府积极主动减少碳排放,并推出了鼓励工业界采用节能解决方案的支持政策。这推动了AC马达在交通运输和工业自动化等广泛行业的进一步应用。

- 日本透过工业4.0策略在亚太地区向自动化工业经济转型中取得了长足进步,并已成为向亚太地区其他区域市场供应工厂自动化产品的製造业中心。

- 据国土交通省称,截至 2023 年 5 月,电动车 (EV) 约占韩国汽车市场的 1.8%。韩国政府设定目标,在未来几年内将电动和氢动力汽车在新车销售的比例提高到33%。电动车领域的这些发展可能为供应商投资製造设施创造重大机会,从而推动市场发展。

交流马达市场概况

交流 (AC)马达市场高度分散,主要参与者包括罗克韦尔自动化公司、西门子股份公司、德昌电机、日本电产株式会社和 ABB 有限公司。市场上的公司正在采用联盟和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2024 年 5 月 - ABB 推出配备 AMXE250马达和 HES580 逆变器的电动公车先进套件。此整合式推进系统旨在提高效率、可靠性和可用性,为永续运输解决方案树立新标准。

- 2024 年 5 月 - KPS Capital Partners LP 透过一家新成立的附属公司达成最终协议,以 35 亿欧元的企业价值从西门子股份公司收购 Innomotics GmbH。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

- 新冠疫情及其他宏观经济因素对市场的影响

第五章市场动态

- 市场驱动因素

- 能源效率需求日益增长

- 工业自动化的兴起

- 市场挑战

- 初始成本高

第六章市场区隔

- 透过感应交流AC马达

- 单相

- 变形怪

- 采用同步交流AC马达

- 直流励磁转子

- 永久磁铁

- 磁滞马达

- 磁阻马达

- 按最终用户产业

- 石油和天然气

- 化工和石化

- 发电

- 用水和污水

- 金属与矿业

- 食品和饮料

- 离散製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 义大利

- 法国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 北美洲

第七章:供应商排名分析

第八章竞争格局

- 公司简介

- Rockwell Automation Inc.

- Siemens AG

- Johnson Electric

- Nidec Corporation

- ABB Ltd

- Franklin Electric Co.Inc.

- WEG Electric Corporation

- Yaskawa Electric Corporation

- Kirloskar Electric Co. Ltd

- Bosch Rexroth AG(ROBERT Bosch GmbH)

- Regal Rexnord Corporation

- SEVA-tec GmbH

第九章投资分析

第十章:投资分析市场的未来

The Alternating Current Motor Market size is estimated at USD 18.29 billion in 2025, and is expected to reach USD 21.73 billion by 2030, at a CAGR of 3.51% during the forecast period (2025-2030).

Key Highlights

- An AC motor is an electric motor that converts the alternating current into mechanical power using an electromagnetic induction phenomenon called an AC motor. An alternating current drives this motor. The stator and the rotor are the two most essential parts of an AC motor. The stator is the stationary part of the motor, and the rotor is the rotating part of the motor. The AC motor may be single-phase or three-phase.

- Three-phase AC motors are primarily applied in the industry for bulk power conversion from electrical to mechanical. Single-phase AC motors are mainly used for small power conversion. Single-phase AC motors are nearly small and provide various services in the home, office, business concerns, factories, etc. Almost all domestic appliances, such as refrigerators, fans, washing machines, hair dryers, and mixers, use single-phase AC motors.

- The growing adoption of electric vehicles is expected to support the market's growth during the forecast period. The automotive sector witnessed a significant increase in daily units produced over the years. According to the International Organization of Motor Vehicle Manufacturers (OICA), in the previous year, approximately 85 million motor vehicles were produced across the world, an increase of 6% compared to the year before it. China, Japan, and Germany were the largest producers of cars and commercial vehicles last year.

- AC motor integrates various other components into one physical unit. Standard configurations include the engine and drive, integrated encoders, controllers, cabling, and communication ports. This increases the overall cost of the system. The capital investment required for AC motors is greater than that required for other traditional motors, posing a challenge to the market's growth.

- A notable impact of the global outbreak of the COVID-19 pandemic has been observed on the market as various containment measures taken by governments across multiple countries, such as the implementation of lockdown, significantly impacted the growth of the industrial sector. As a result, a slowdown was witnessed in the studied market, especially during the initial phase, due to supply chain issues. However, with significant end-user industries resuming operations at total capacity, the demand for smart AC motors is anticipated to increase.

Alternating Current (AC) Motor Market Trends

The Oil and Gas Industry is Expected to Hold a Major Share in the Market

- The oil and gas industry plays a significant role in driving market growth. AC motors are extensively utilized within this industry due to their simplicity, reliability, and affordability. Electric AC motors play a crucial role in the oil and gas industry by delivering dependable and steady power to drill rig systems and equipment. These motors generate the necessary energy to facilitate the extraction, processing, storage, and transportation of valuable resources such as crude oil, natural gas, and petroleum. Induction motors and synchronous generators are employed to supply power for a wide range of applications in both onshore and offshore drilling operations.

- The rising demand for AC motors in the oil and gas sectors can be attributed to the growing emphasis on energy efficiency and reliability in challenging operational environments. Moreover, AC electric motors provide exceptional speed control and monitoring capabilities. The adoption of AC electric motors in onshore oil and gas industrial processes has witnessed a substantial increase owing to their ability to operate effectively in diverse environmental conditions and exhibit longer life cycles compared to alternative motor types.

- AC electric motors with a voltage rating below 1 kilovolt (kV) are frequently utilized in smaller equipment such as pumps, fans, blowers, and smaller compressors within oil and gas facilities. AC electric motors with a voltage rating ranging from 1 kV to 6.6 kV, as well as those exceeding 6.6 kV, are extensively employed in medium to high-power applications within the oil and gas industry. These motors are commonly found in larger compressors, generators, pumps, and other heavy-duty equipment. AC electric motors with a voltage rating exceeding 6.6 kV possess several notable characteristics, including increased power output, enhanced efficiency, and improved overload capacity.

- According to the International Energy Agency (IEA), the latest projections indicate that global demand for oil and gas will reach its peak in the coming years, even with the current policy settings in place. The IEA anticipates that global demand will rise by approximately eight million barrels per day (bpd) by the end of the decade, leading to an increased need for offshore activities. As a result of this growth in offshore operations and investments, there is an expected surge in demand for AC motors. These motors are utilized in various offshore applications, such as drilling rigs, production platforms, floating production storage and offloading (FPSO) vessels, subsea systems, and other offshore equipment.

- Furthermore, as per OPEC's report, the global consumption of crude oil (including biofuels) recently stood at 99.57 million barrels per day. It is estimated to rise to 101.89 million barrels per day in the coming years and eventually reach 109.8 million barrels per day. The demand for diesel and gas oil is forecasted to amount to 30.1 million barrels per day, up from 27.6 million barrels. Such factors will encourage the demand for AC motors in the industry.

Asia-Pacific is Expected to Witness a Significant Growth in the Market

- China has been witnessing rapid industrialization and development across various sectors, such as manufacturing, automotive, and electronics. AC motors are widely used in industrial machinery and equipment for applications such as pumps, compressors, conveyors, and fans, driving the demand for AC motors.

- China has been focusing on high-end manufacturing industries, power utilities, and oil and gas industries, boosting the usage of both low and medium-voltage drives in the country. For instance, the Chinese government's ambitious 'Made in China 2025' initiative, partially inspired by Germany for Industry 4.0, aims to boost the country's competitiveness in the manufacturing sector.

- India is expected to hold a significant global AC Motor Market share. The country's market is driven by rising demand for electric motors in manufacturing industries and rising awareness about energy efficiency. Also, the rising energy costs are expected to accelerate the adoption of synchronous electric motors in various industries. Due to the presence of many electric motor manufacturers in India, the country is expected to maintain a considerable market share during the forecast period.

- Japanese government's proactive approach to reducing carbon emissions has led to supportive policies that encourage industries to embrace energy-efficient solutions. This has further increased the adoption of AC motors in a wide range of industries, including transportation and industrial automation.

- Japan has been significantly transforming into an automated industrial economy in Asia-Pacific through its Industrial version 4.0 strategies, and the country has emerged as a manufacturing hub for factory automation products and supplies to other regional markets in Asia-Pacific.

- As of May 2023, according to the Ministry of Land, Infrastructure, and Transport, electric vehicles (EVs) represented approximately 1.8% of the South Korean automobile market. The government of South Korea has set a target to raise the proportion of electric and hydrogen vehicles in new vehicle sales to 33% in the coming years. Such developments in the EV sector will create significant opportunities for the vendor to invest in manufacturing facilities, thereby driving the market.

Alternating Current (AC) Motor Market Overview

The alternating current (AC) motor market is highly fragmented, with major players like Rockwell Automation Inc., Siemens AG, Johnson Electric, Nidec Corporation, and ABB Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- May 2024 - ABB unveiled an advanced package for electric buses featuring the AMXE250 motor and HES580 inverter. This integrated propulsion system is engineered to enhance efficiency, reliability, and availability, setting a new standard for sustainable transportation solutions.

- May 2024 - KPS Capital Partners LP, through a newly established affiliate, entered into a definitive agreement to acquire Innomotics GmbH from Siemens AG for an enterprise value of EUR 3.5 billion.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of the COVID-19 pandemic and other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for High Energy Efficiency

- 5.1.2 Rise in Industrial Automation

- 5.2 Market Challenges

- 5.2.1 High Initial Costs

6 MARKET SEGMENTATION

- 6.1 By Induction AC Motors

- 6.1.1 Single Phase

- 6.1.2 Poly Phase

- 6.2 By Synchronous AC Motors

- 6.2.1 DC Excited Rotor

- 6.2.2 Permanent Magnet

- 6.2.3 Hysteresis Motor

- 6.2.4 Reluctance Motor

- 6.3 By End-user Industry

- 6.3.1 Oil and Gas

- 6.3.2 Chemical and Petrochemical

- 6.3.3 Power Generation

- 6.3.4 Water and Wastewater

- 6.3.5 Metal and Mining

- 6.3.6 Food and Beverage

- 6.3.7 Discrete Industries

- 6.3.8 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Italy

- 6.4.2.4 France

- 6.4.2.5 Russia

- 6.4.2.6 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 South Korea

- 6.4.3.5 Australia and New Zealand

- 6.4.3.6 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.6 Saudi Arabia

- 6.4.7 United Arab Emirates

- 6.4.8 South Africa

- 6.4.9 Rest of Middle East and Africa

- 6.4.1 North America

7 VENDOR RANKING ANALYSIS

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Rockwell Automation Inc.

- 8.1.2 Siemens AG

- 8.1.3 Johnson Electric

- 8.1.4 Nidec Corporation

- 8.1.5 ABB Ltd

- 8.1.6 Franklin Electric Co.Inc.

- 8.1.7 WEG Electric Corporation

- 8.1.8 Yaskawa Electric Corporation

- 8.1.9 Kirloskar Electric Co. Ltd

- 8.1.10 Bosch Rexroth AG (ROBERT Bosch GmbH)

- 8.1.11 Regal Rexnord Corporation

- 8.1.12 SEVA-tec GmbH

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

全球交流马达市场规模、占有率、成长及产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测低压马达市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测全封闭式马达市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察,以及2024-2032年预测

全球交流马达市场规模、占有率、成长及产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测低压马达市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测全封闭式马达市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察,以及2024-2032年预测 中电压马达:全球市占率及排名、总收入及需求预测(2025-2031年)全球汽油动力舷外机市场-市场份额和排名、总收入和需求预测(2025-2031 年)

中电压马达:全球市占率及排名、总收入及需求预测(2025-2031年)全球汽油动力舷外机市场-市场份额和排名、总收入和需求预测(2025-2031 年) 中高功率马达市场(按类型、电压、额定功率、效率等级、工业用途划分)-2025-2032年全球预测工业马达汇流排市场按汇流排类型、终端用户产业、额定电压、绝缘材料和应用划分-2025年至2032年全球预测整合式高功率马达市场(依马达类型、功率范围、终端用户产业及通路划分)-2025-2032年全球预测气动马达市场按产品类型、压力范围、应用、产业和分销管道划分-2025-2032年全球预测石油天然气交流电机市场按类型、应用、额定功率、转速、外壳、冷却方式、绝缘等级、认证和最终用途划分-全球预测,2025-2032年

中高功率马达市场(按类型、电压、额定功率、效率等级、工业用途划分)-2025-2032年全球预测工业马达汇流排市场按汇流排类型、终端用户产业、额定电压、绝缘材料和应用划分-2025年至2032年全球预测整合式高功率马达市场(依马达类型、功率范围、终端用户产业及通路划分)-2025-2032年全球预测气动马达市场按产品类型、压力范围、应用、产业和分销管道划分-2025-2032年全球预测石油天然气交流电机市场按类型、应用、额定功率、转速、外壳、冷却方式、绝缘等级、认证和最终用途划分-全球预测,2025-2032年