|

市场调查报告书

商品编码

1692477

水泥 -市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

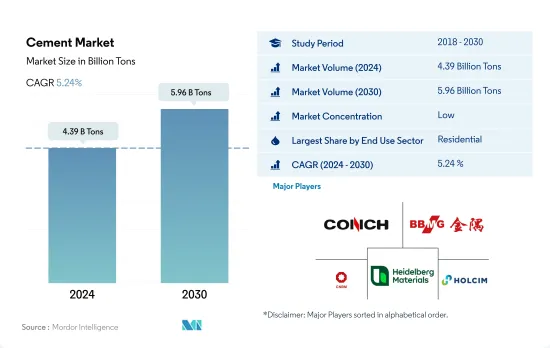

预计 2024 年水泥市场规模为 43.9 亿吨,到 2030 年将达到 59.6 亿吨,预测期内(2024-2030 年)的复合年增长率为 5.24%。

商业领域的快速成长将导致水泥需求增加

- 2022年各产业水泥需求均低于2021年,导致全球整体需求下降近3.83%。预计 2023 年所有产业的需求都将增加,整体增幅将比 2022 年高出 0.70%。

- 住宅产业是世界上最大的水泥消费产业,大多数国家都建造混凝土住宅,这直接导致该产业对水泥的需求量很大。亚太地区是水泥市场需求最高的地区。由于人口众多,该地区到2022年将占全球水泥需求的67%。

- 基础设施是大多数国家利用大量水泥库存的领域。水泥是混凝土的主要成分,对于道路、水坝和港口等各种基础设施的建设至关重要。亚太地区占该领域消费量,主要是中国、印度、韩国和日本。这些国家占2022年基础建设领域水泥需求的90%。

- 预计商业领域的建设活动将成长最快。例如,在所有产业中,商业领域的新增占地面积预计将以最快的速度成长,预测期内(2023-2030 年)的复合年增长率约为 4.56%。因此,预计全球商业领域的水泥需求将成长最快,预测期内复合年增长率为 6.18%,到 2030 年达到 7.646 亿美元。

建筑投资推动中东和非洲水泥需求

- 2022年,全球水泥需求预计将较2021年下降3.83%,主要原因是亚太地区下降6.37%。预计2023年水泥需求将保持相对强劲,亚太地区将进一步下降。

- 亚太地区继续在建筑计划数量方面领先,其中印度位居榜首,截至 2022 年 5 月,印度计划建设价值 2500 万美元的基础设施计划。中国和澳洲紧追在后,分别位居第三和第四位。因此,亚太地区已成为全球水泥消费的中心。

- 继亚太地区之后,中东和非洲正成为重要的水泥消费地区。沙乌地阿拉伯和阿拉伯联合大公国处于领先地位,其政府继续投资于基础设施和产业倡议。其中,阿联酋的基础设施投资在2021年至2022年期间激增了82%。到2022年,沙乌地阿拉伯和阿联酋将分别占全球水泥产量的12%和3%。

- 根据预测数据,中东和非洲的水泥需求成长最高,预测期内(2023-2030 年)水泥需求量的复合年增长率为 7.07%。尤其是沙乌地阿拉伯近期签署了总额约26.6亿美元的协议和谅解备忘录,并致力于建立投资基金,以加强商业、旅游和住宅计划,进一步推动该地区对水泥的需求。

全球水泥市场趋势

亚太地区大型办公大楼建设计划激增,将推动全球专用商业占地面积成长

- 2022年,全球占地面积将与前一年同期比较去年小幅成长0.15%。欧洲表现突出,增幅达 12.70%,这得益于欧洲大力推行节能办公大楼,以实现 2030 年二氧化碳排放目标。随着员工重返办公室,欧洲公司正在重新签订租约,刺激 2022 年新办公大楼建设面积达到 450 万平方英尺。预计这一势头将在 2023 年持续下去,全球成长率预计为 4.26%。

- 新冠疫情造成劳动力和材料短缺,导致商业建筑计划取消和延迟。然而,随着停工缓解和建设活动恢復,2021 年全球新增商业占地面积飙升 11.11%,其中亚太地区以 20.98% 的成长率领先。

- 展望未来,全球新增商业占地面积的复合年增长率将达到4.56%。预计亚太地区的复合年增长率将达到 5.16%,超过其他地区。这一增长背后的驱动力是中国、印度、韩国和日本商业建筑计划的活性化。尤其北京、上海、香港、台北等中国主要城市的甲级办公室建设正在加速。此外,印度计划于 2023 年至 2025 年间在七大城市开设约 60 家购物中心,总面积约 2,325 万平方英尺。总合到 2030 年,亚太地区的这些措施将比 2022 年增加 15.6 亿平方英尺的新零售占地面积。

预计南美洲的住宅将出现最快的成长,这得益于政府加大对经济适用住宅计画的投资,这将推动全球住宅产业的发展。

- 2022年,全球新建住宅占地面积与2021年相比减少了约2.89亿平方英尺。这是由于土地稀缺、劳动力短缺以及建筑材料价格不可持续的高企造成的住宅危机。这场危机对亚太地区造成了严重影响,2022 年新占地面积与 2021 年相比下降了 5.39%。不过,2023 年的前景更加光明,预计全球新建占地面积将比 2022 年增长 3.31%,这要归功于政府投资,这些投资可以为 2030 年之前 30 亿人建造新的经济适用住宅提供资金。

- 新冠疫情造成经济放缓,导致大量住宅建设计划取消或延后,2020年全球新建占地面积较2019年下降4.79%。随着2021年限制措施的解除,住宅计划被压抑的需求得到释放,2021年全球新建占地面积较2020年增长11.22%,其中欧洲增幅最高,为18.28%,其次是南美洲,2021年较2020年增长17.36%。

- 预测期内,全球住宅新占地面积预计复合年增长率为 3.81%,其中南美洲的增长速度最快,为 4.05%。巴西宣布将于 2023 年实施「Minha Casa Minha Vida」等计划和倡议,同时还将进行多项监管改革,政府计划投资 19.8 亿美元为低收入家庭提供经济适用住宅;智利也宣布将于 2023 年实施「FOGAES」等计划和倡议,旨在为家庭提供经济适用住宅房屋抵押贷款,这些计划和建设倡议将刺激新住宅的建设倡议。

水泥业概况

水泥市场分散,前五大企业市占率为32.78%。该市场的主要企业有:安徽海螺水泥股份有限公司、北京金隅集团、中国建筑材料集团公司、海德堡材料和霍尔希姆(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 终端使用领域的趋势

- 商业

- 工业/设施

- 基础设施

- 住宅

- 重大基础设施计划(目前和已宣布)

- 法律规范

- 价值炼和通路分析

第五章市场区隔

- 最终使用区域

- 商业

- 工业/设施

- 基础设施

- 住宅

- 产品

- 混合水泥

- 纤维水泥

- 普通波特兰水泥

- 白水泥

- 其他的

- 地区

- 亚太地区

- 按国家

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 韩国

- 泰国

- 越南

- 其他亚太地区

- 欧洲

- 按国家

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 英国

- 其他欧洲国家

- 中东和非洲

- 按国家

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 北美洲

- 按国家

- 加拿大

- 墨西哥

- 美国

- 南美洲

- 按国家

- 阿根廷

- 巴西

- 南美洲其他地区

- 亚太地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Adani Group

- Anhui Conch Cement Company Limited

- BBMG Corporation

- CEMEX, SAB de CV

- Cemros

- China National Building Material Group Corporation

- China Resource Cement Holdings

- CRH

- Dangote Cement Plc.

- Heidelberg Materials

- Holcim

- SIG

- TAIWAN CEMENT LTD.

- UltraTech Cement Ltd.

- Votorantim Cimentos

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 91436

The Cement Market size is estimated at 4.39 billion Tons in 2024, and is expected to reach 5.96 billion Tons by 2030, growing at a CAGR of 5.24% during the forecast period (2024-2030).

The commercial sector's fast-paced growth is leading to higher cement demand

- The demand for cement across the sectors was reduced in 2022 over 2021, resulting in a nearly 3.83% lower demand worldwide due to very low growth and even declines in the new floor area under construction. As the demand across sectors was projected to rise in 2023, the overall increase was estimated to be 0.70% higher than in 2022.

- The residential sector is the largest consumer of cement in the world, as most countries have concrete homes that directly convert to a large volume of cement demand from this sector. The cement market experiences the highest demand from Asia-Pacific. The region accounted for 67% of the world's total cement demand in 2022, owing to its vast population.

- Infrastructure is the sector in which most countries utilize a significant portion of their cement stock. Cement is among the primary raw materials of concrete, which is essential for all types of infrastructure construction, such as roads, dams, ports, etc. Asia-Pacific accounts for the largest cement consumption in this sector, primarily due to China, India, South Korea, and Japan. These countries together constituted 90% of the region's infrastructure sector's cement demand in 2022.

- Construction activities are expected to rise the fastest in the commercial sector. For instance, the new floor area of the commercial sector among all the sectors is poised to grow with the fastest CAGR of around 4.56% during the forecast period (2023-2030). Hence, the cement demand from the commercial sector is expected to increase the fastest globally at a CAGR of 6.18% during the forecast period and is expected to reach USD 764.6 million by 2030.

The demand for cement to rise in the Middle East & Africa owing to investments in construction

- In 2022, global cement demand saw a 3.83% decline in volume compared to 2021, largely driven by a 6.37% drop in the Asia-Pacific region. Projections suggested that cement demand in 2023 would remain relatively steady, with the Asia-Pacific expected to witness a further decline.

- The Asia-Pacific consistently leads in construction project volumes, exemplified by India's dominance with over USD 25 million worth of infrastructure projects in the pipeline as of May 2022, surpassing other nations. China and Australia followed closely in the third and fourth positions, respectively. Consequently, the Asia-Pacific stands as the global cement consumption hub.

- Following the Asia-Pacific, the Middle East & Africa emerge as a significant consumer of cement. Saudi Arabia and the United Arab Emirates take the lead, buoyed by their governments' consistent investments in infrastructure and sector initiatives. Notably, infrastructure investments in the United Arab Emirates surged by 82% from 2021 to 2022. In 2022, Saudi Arabia and the United Arab Emirates accounted for 12% and 3% of the global cement volume, respectively.

- Anticipated data indicates that the Middle East & Africa will witness the highest cement demand growth, registering a CAGR of 7.07% in volume during the forecast period (2023-2030). Notably, Saudi Arabia's recent agreements and MoUs, totaling nearly USD 2.66 billion, focus on establishing investment funds to bolster commercial, tourism, and residential projects, further fueling the cement demand in the region.

Global Cement Market Trends

Asia-Pacific's surge in large-scale office building projects is set to elevate the global floor area dedicated to commercial construction

- In 2022, the global new floor area for commercial construction witnessed a modest growth of 0.15% from the previous year. Europe stood out with a significant surge of 12.70%, driven by a push for high-energy-efficient office buildings to align with its 2030 carbon emission targets. As employees returned to offices, European companies, resuming lease decisions, spurred the construction of 4.5 million square feet of new office space in 2022. This momentum is poised to persist in 2023, with a projected global growth rate of 4.26%.

- The COVID-19 pandemic caused labor and material shortages, leading to cancellations and delays in commercial construction projects. However, as lockdowns eased and construction activities resumed, the global new floor area for commercial construction surged by 11.11% in 2021, with Asia-Pacific taking the lead with a growth rate of 20.98%.

- Looking ahead, the global new floor area for commercial construction is set to achieve a CAGR of 4.56%. Asia-Pacific is anticipated to outpace other regions, with a projected CAGR of 5.16%. This growth is fueled by a flurry of commercial construction projects in China, India, South Korea, and Japan. Notably, major Chinese cities like Beijing, Shanghai, Hong Kong, and Taipei are gearing up for an uptick in Grade A office space construction. Additionally, India is set to witness the opening of approximately 60 shopping malls, spanning 23.25 million square feet, in its top seven cities between 2023 and 2025. Collectively, these endeavors across Asia-Pacific are expected to add a staggering 1.56 billion square feet to the new floor area for commercial construction by 2030, compared to 2022.

South America's estimated fastest growth in residential constructions due to increasing government investments in schemes for affordable housing to boost the global residential sector

- In 2022, the global new floor area for residential construction declined by around 289 million square feet compared to 2021. This can be attributed to the housing crisis generated due to the shortage of land, labor, and unsustainably high construction materials prices. This crisis severely impacted Asia-Pacific, where the new floor area declined 5.39% in 2022 compared to 2021. However, a more positive outlook is expected in 2023 as the global new floor area is predicted to grow by 3.31% compared to 2022, owing to government investments that can finance the construction of new affordable homes capable of accommodating 3 billion people by 2030.

- The COVID-19 pandemic caused an economic slowdown, due to which many residential construction projects got canceled or delayed, and the global new floor area declined by 4.79% in 2020 compared to 2019. As the restrictions were lifted in 2021 and pent-up demand for housing projects was released, new floor area grew 11.22% compared to 2020, with Europe having the highest growth of 18.28%, followed by South America, which rose 17.36% in 2021 compared to 2020.

- The global new floor area for residential construction is expected to register a CAGR of 3.81% during the forecast period, with South America predicted to develop at the fastest CAGR of 4.05%. Schemes and initiatives like the Minha Casa Minha Vida in Brazil announced in 2023 with a few regulatory changes, for which the government plans an investment of USD 1.98 billion to provide affordable housing units for low-income families, and the FOGAES in Chile also publicized in 2023, with an initial investment of USD 50 million, are aimed at providing mortgage loans to families for affordable housing and will encourage the construction of new residential units.

Cement Industry Overview

The Cement Market is fragmented, with the top five companies occupying 32.78%. The major players in this market are Anhui Conch Cement Company Limited, BBMG Corporation, China National Building Material Group Corporation, Heidelberg Materials and Holcim (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Blended Cement

- 5.2.2 Fiber Cement

- 5.2.3 Ordinary Portland Cement

- 5.2.4 White Cement

- 5.2.5 Other Types

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 By Country

- 5.3.1.1.1 Australia

- 5.3.1.1.2 China

- 5.3.1.1.3 India

- 5.3.1.1.4 Indonesia

- 5.3.1.1.5 Japan

- 5.3.1.1.6 Malaysia

- 5.3.1.1.7 South Korea

- 5.3.1.1.8 Thailand

- 5.3.1.1.9 Vietnam

- 5.3.1.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 By Country

- 5.3.2.1.1 France

- 5.3.2.1.2 Germany

- 5.3.2.1.3 Italy

- 5.3.2.1.4 Russia

- 5.3.2.1.5 Spain

- 5.3.2.1.6 United Kingdom

- 5.3.2.1.7 Rest of Europe

- 5.3.3 Middle East and Africa

- 5.3.3.1 By Country

- 5.3.3.1.1 Saudi Arabia

- 5.3.3.1.2 United Arab Emirates

- 5.3.3.1.3 Rest of Middle East and Africa

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adani Group

- 6.4.2 Anhui Conch Cement Company Limited

- 6.4.3 BBMG Corporation

- 6.4.4 CEMEX, S.A.B. de C.V.

- 6.4.5 Cemros

- 6.4.6 China National Building Material Group Corporation

- 6.4.7 China Resource Cement Holdings

- 6.4.8 CRH

- 6.4.9 Dangote Cement Plc.

- 6.4.10 Heidelberg Materials

- 6.4.11 Holcim

- 6.4.12 SIG

- 6.4.13 TAIWAN CEMENT LTD.

- 6.4.14 UltraTech Cement Ltd.

- 6.4.15 Votorantim Cimentos

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

2025年混合水泥全球市场报告2025年矿渣水泥全球市场报告

2025年混合水泥全球市场报告2025年矿渣水泥全球市场报告 全球碳中和水泥市场预测(至2032年):按类型、原料、通路、技术、应用、最终用户和地区进行分析

全球碳中和水泥市场预测(至2032年):按类型、原料、通路、技术、应用、最终用户和地区进行分析 水泥助磨剂和性能增强剂市场-全球产业规模、份额、趋势、机会和预测(按产品类型、水泥类型、最终用户、地区和竞争细分,2020-2030 年)2025年水泥和混凝土产品全球市场报告2025年水泥胶黏剂全球市场报告

水泥助磨剂和性能增强剂市场-全球产业规模、份额、趋势、机会和预测(按产品类型、水泥类型、最终用户、地区和竞争细分,2020-2030 年)2025年水泥和混凝土产品全球市场报告2025年水泥胶黏剂全球市场报告 全球铝酸钙市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测水泥熟料市场-全球产业规模、份额、趋势、机会和预测,按类型(普通波特兰水泥、混合水泥)、按配销通路、按应用、按地区、按竞争进行细分,2020-2030 年预测

全球铝酸钙市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测水泥熟料市场-全球产业规模、份额、趋势、机会和预测,按类型(普通波特兰水泥、混合水泥)、按配销通路、按应用、按地区、按竞争进行细分,2020-2030 年预测 砂处理设备市场机会、成长动力、产业趋势分析及2025-2034年预测预热器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

砂处理设备市场机会、成长动力、产业趋势分析及2025-2034年预测预热器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

▼