|

市场调查报告书

商品编码

1692581

中东和非洲建筑胶合剂和密封剂市场占有率分析、行业趋势、统计数据、成长预测(2025-2030 年)Middle East & Africa Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

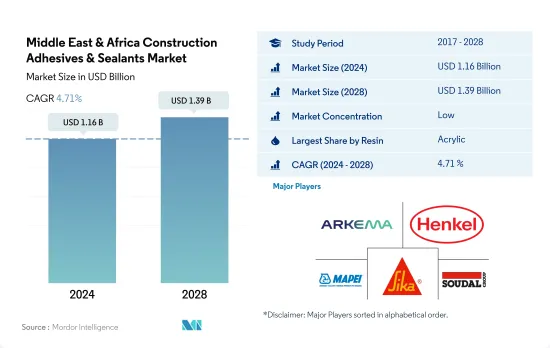

中东和非洲建筑胶合剂和密封剂市场规模预计在 2024 年达到 11.6 亿美元,预计到 2028 年将达到 13.9 亿美元,预测期内(2024-2028 年)的复合年增长率为 4.71%。

沙乌地阿拉伯的黏合剂和密封剂消费量正在成长,推动其在未来几年继续保持最大消费量地位

- 2017 年至 2021 年期间,聚氨酯和丙烯酸树脂基黏合剂和密封剂是所有其他树脂类型中使用最多的。这些树脂具有很强的黏合强度,非常适合用作结构性黏着剂,预计在预测期内(2022-2028 年)仍将是使用最广泛的树脂类型。在中东和非洲,67% 的丙烯酸建筑胶合剂采用水性技术生产,而聚氨酯系统主要采用密封胶技术生产。

- 在中东和非洲,2020 年建筑胶合剂和密封剂需求整体下降,可归因于该地区整体经济放缓,而中东和北非地区疫情导致全国封锁、供应链中断、强制性社交隔离规定等。结果,2020 年建筑胶合剂和密封剂需求萎缩了 7.04%。 2021 年,需求回升了 5.22%。

- 在中东和非洲,在历史时期(2017-2021 年)内,建筑黏合剂和密封剂的需求在预测期(2022-2028 年)内以 4% 的复合年增长率增长。预计需求将以6%的速度成长。在所有树脂类型中,预计预测期内(2022-2028 年)硅胶树脂基黏合剂和密封剂的复合年增长率最高,约为 6%。

- 沙乌地阿拉伯占全球建筑胶黏剂和密封剂需求的最大份额。 2021年,沙乌地阿拉伯的需求量为8,160万公斤。预计2028年将达到1.006亿公斤,复合年增长率为6.9%。预计到2022年,聚氨酯、丙烯酸和硅树脂基黏合剂和密封剂产品将占沙乌地阿拉伯建筑业总需求的50%以上。

该地区绿色建筑建设活动的兴起预计将显着推动成长

- 2020 年建筑业产量下降 4.4% 是由于新冠疫情,导致全国停工、供应链中断和强制性的社交距离规定。这些因素减少了2020年建筑所需的黏合剂和密封剂的需求。由于建筑市场的疲软,南非的降幅最大。

- 由于中东和非洲建设活动的活性化,2021 年对建筑黏合剂和密封剂的需求增加。沙乌地阿拉伯正在进行各种建设项目,包括耗资 5000 亿美元的未来特大城市Neom计划、红海计划(第一期工程,计划于 2022 年完工)、分布在五个岛屿上、拥有 3000 间客房的豪华和超豪华酒店、两个内陆度假村、Qiddiya 娱乐城和超豪华健康目的地 Amaala。预计这些计划将在预测期内推动建筑黏合剂和密封剂的需求。

- 预计中东和非洲也将在未来几年全球绿建筑成长中发挥关键作用。中东和非洲绿色建筑委员会网络应对当地的挑战和机会,确保该地区的建筑为人们提供高品质的生活,最大限度地减少负面环境影响,并最大限度地提高经济效益。因此,由于绿色建筑建设活动的兴起,预计在 2022-2028 年预测期内,中东和非洲的黏合剂和密封剂市场销量将以 3.4% 的复合年增长率增长,以金额为准。

中东和非洲建筑胶合剂和密封剂市场趋势

强劲的人口和有利的政府政策推动建筑业发展

- 建筑业正成为非洲经济的主要驱动力,贡献 GDP 的 10-15%。该地区的发展吸引了来自世界各地的投资,为住宅、商业、机构和工业建筑的建设创造了更多机会,促进了劳动力的成长。

- 2018年建筑业成长率为2.38%,2019年成长率为2.32%。然而,由于新冠疫情对沙乌地阿拉伯和阿联酋等国的建设活动造成限制,建筑市场在2020年萎缩了6.81%。 2021年,随着中东和北非国家成功控制新冠疫情,建筑市场恢復了成长率。因此,核心建筑产业实现了温和成长,而其他可比市场则出现缓慢甚至负成长。

- 中东和北非(MENA)地区目前拥有超过3.5亿人口,其人口成长的特征是快速都市化。预计这一趋势将持续下去,2010 年至 2050 年间,城市人口预计将翻一番,从 2 亿增加到近 4 亿。这意味着巨大的建设需求,而衝突导致的人口流离失所问题则使这项需求雪上加霜。因此,预计预测期内(2022-2028 年)中东和非洲的建筑业将以 2.7% 的复合年增长率成长。

中东和非洲建筑胶合剂和密封剂产业概况

中东和非洲建筑胶合剂和密封剂市场分散,前五大公司占据18.51%的市场份额。该市场的主要企业包括阿科玛集团、汉高股份公司、马贝集团、西卡股份公司和 Soudal Holding NV。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 建筑与施工

- 法律规范

- 沙乌地阿拉伯

- 南非

- 价值炼和通路分析

第五章市场区隔

- 树脂

- 丙烯酸纤维

- 氰基丙烯酸酯

- 环氧树脂

- 聚氨酯

- 硅胶

- VAE・EVA

- 其他的

- 科技

- 热熔胶

- 反应性

- 密封剂

- 溶剂型

- 水性

- 国家

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- Arkema Group

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- MAPEI SpA

- Sika AG

- Soudal Holding NV

- Wacker Chemie AG

第七章:CEO面临的关键策略问题

第 8 章 附录

- 全球黏合剂和密封剂产业概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 驱动因素、限制因素和机会

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 92418

The Middle East & Africa Construction Adhesives & Sealants Market size is estimated at 1.16 billion USD in 2024, and is expected to reach 1.39 billion USD by 2028, growing at a CAGR of 4.71% during the forecast period (2024-2028).

Saudi Arabia's growing consumption of adhesives & sealants to maintain its position at the top in terms of consumption even for the next few years

- Polyurethane and acrylic resin-based adhesives and sealants were the most used among other resin types in 2017-2021. They are expected to be the most used resin types during the forecast period (2022-2028) because of their strong bonds and their applicability as structural adhesives. In the Middle East and Africa, 67% of acrylic-based construction adhesives are manufactured in water-borne technology, and polyurethane-based products are manufactured majorly in sealant technology.

- In the Middle East & Africa region, the decrease in overall demand for construction adhesives and sealants in 2020 can be attributed to the overall economic slowdown in the region caused due to COVID-19 pandemic, which led to nationwide lockdowns, supply chain disruption, mandatory social distancing regulations, etc. Thus, the construction adhesives and sealants contracted by 7.04%% in 2020. It was restored by 5.22% in 2021.

- In the Middle East and Africa, during the historic period (2017-2021), demand for construction adhesives and sealants increased by a CAGR of 4% during the forecast period (2022-2028). The demand is expected to increase at a rate of 6%. Among all the resin types, silicone resin-based adhesives and sealants are expected to register the largest CAGR of around 6% during the forecast period (2022-2028).

- Saudi Arabia occupied the largest share of the global demand for construction adhesives and sealants. In 2021, the demand generated from Saudi Arabia was 81.6 million kilograms. In 2028, the demand is expected to reach 100.6 million kilograms with a CAGR of 6.9%. Polyurethane, acrylic, and silicon resin-based adhesives and sealants products are expected to occupy more than 50% of the total demand generated by the Saudi Arabian construction industry in 2022.

A major boost to the growth forecasted to be contributed by the rising green building construction activities in the region

- In 2020, the decline in construction output by 4.4% was due to the COVID-19 pandemic, which led to nationwide lockdowns, supply chain disruption, mandatory social distancing regulations, etc. These factors led to declining demand for adhesives and sealants required for construction in 2020. The decline was the highest in South Africa because of the country's construction market decline.

- The demand for construction adhesives and sealants grew in 2021 because of the rising construction activities in Middle East & Africa. Saudi Arabia has implemented various construction projects, including a USD 500 billion futuristic mega-city 'Neom' project, the Red Sea Project - Phase 1, which is due to be completed in 2022, and luxury and hyper-luxury hotels that may comprise 3,000 rooms across five islands, and two inland resorts, Qiddiya Entertainment City, and Amaala - the uber-luxury wellness tourism destination. Such projects are likely to drive the demand for construction adhesives and sealants over the forecast period.

- The Middle East & Africa region is also set to be critical for the growth of green buildings globally over the next few years. Green Building Councils in the MENA Regional Network are responding to challenges and opportunities on the ground, ensuring that the region's buildings provide a high quality of life for people, minimize negative impacts on the environment, and maximize economic benefits. Thus, due to rising green building construction activities, the Middle East & African adhesives and sealants market is projected to record a CAGR of 3.4% by volume and 5.01% by value during the forecast period 2022-2028.

Middle East & Africa Construction Adhesives & Sealants Market Trends

Robust population and favorable government policies to boost the construction industry

- The construction industry is becoming a key driver for African economies, accounting for 10-15% of GDP. Development in the region is attracting investment from all over the world, which is further creating opportunities and boosting the workforce in the construction of residential, commercial, institutional, and industrial buildings.

- The construction industry registered a growth rate of 2.38% and 2.32% in 2018 and 2019, respectively. However, in 2020, the construction market contracted by 6.81% compared to the same period in 2019, as the COVID-19 pandemic negatively affected the construction market by restricting construction activities in countries like Saudi Arabia and the United Arab Emirates. In 2021, the construction market regained growth rate as the Middle East and African nations have done well in controlling the COVID-19 outbreak. As a result, key construction sectors recorded moderate growth, unlike other comparable markets which have witnessed low to negative growth.

- The Middle East and North Africa (MENA) is currently home to over 350 million people, and its population growth has been characterized by rapid urbanization. This is projected to continue, with the urban population expected to double from 2010 to 2050, from 200 million to nearly 400 million. This means a large demand for buildings, complicated by the challenges of conflict-induced displacement of people. Thus, the Middle East & Africa Construction industry is expected to increase at a CAGR of 2.7% during the forecast period (2022-2028).

Middle East & Africa Construction Adhesives & Sealants Industry Overview

The Middle East & Africa Construction Adhesives & Sealants Market is fragmented, with the top five companies occupying 18.51%. The major players in this market are Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Saudi Arabia

- 4.2.2 South Africa

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 South Africa

- 5.3.3 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Arkema Group

- 6.4.2 Dow

- 6.4.3 H.B. Fuller Company

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Huntsman International LLC

- 6.4.6 Illinois Tool Works Inc.

- 6.4.7 MAPEI S.p.A.

- 6.4.8 Sika AG

- 6.4.9 Soudal Holding N.V.

- 6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

建筑黏合剂市场:全球市场按产品类型、应用和销售管道分類的预测 - 2026-2032 年建筑密封胶市场:产品类型、技术、应用、最终用途 - 2026-2032年全球市场预测

建筑黏合剂市场:全球市场按产品类型、应用和销售管道分類的预测 - 2026-2032 年建筑密封胶市场:产品类型、技术、应用、最终用途 - 2026-2032年全球市场预测 全球建筑黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球建筑黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球建筑黏合剂市场报告

2026年全球建筑黏合剂市场报告 建筑黏合剂市场-全球产业规模、份额、趋势、机会及预测(按树脂类型、技术、最终用途产业、地区和竞争格局划分,2021-2031年)地板黏合剂市场按类型、形态、基材、应用方法、包装、最终用途和通路划分-2026-2032年全球预测

建筑黏合剂市场-全球产业规模、份额、趋势、机会及预测(按树脂类型、技术、最终用途产业、地区和竞争格局划分,2021-2031年)地板黏合剂市场按类型、形态、基材、应用方法、包装、最终用途和通路划分-2026-2032年全球预测 建筑密封胶市场规模、份额和成长分析(按树脂类型、技术、功能、应用、最终用途产业和地区划分)-产业预测,2026-2033年

建筑密封胶市场规模、份额和成长分析(按树脂类型、技术、功能、应用、最终用途产业和地区划分)-产业预测,2026-2033年 建筑黏合剂市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测全球建筑胶合剂和密封剂市场(2024-2031)

建筑黏合剂市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测全球建筑胶合剂和密封剂市场(2024-2031) 建设用黏剂市场,规模,占有率,产业分析报告:类别树脂,各技术,各用途,各地区,2025年~2034年的市场预测

建设用黏剂市场,规模,占有率,产业分析报告:类别树脂,各技术,各用途,各地区,2025年~2034年的市场预测

▼