|

市场调查报告书

商品编码

1692583

欧洲汽车黏合剂和密封剂:市场占有率分析、产业趋势和成长预测(2025-2030 年)Europe Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

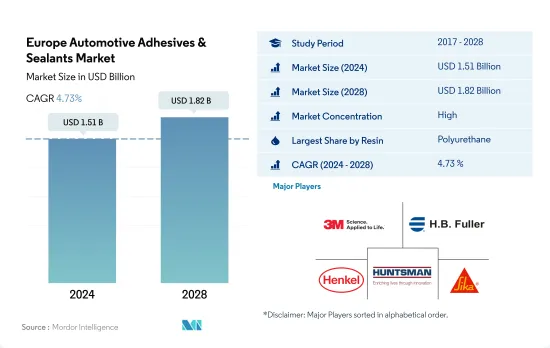

预计 2024 年欧洲汽车黏合剂和密封剂市场规模将达到 15.1 亿美元,预计到 2028 年将达到 18.2 亿美元,预测期内(2024-2028 年)的复合年增长率为 4.73%。

汽车製造商向汽车电气化的转变将推动市场成长

- 在欧洲汽车胶合剂和密封剂市场中,聚氨酯树脂、环氧树脂和丙烯酸树脂占了巨大的市场份额。聚氨酯树脂所占份额较高,是因为它们在汽车工业中最常用于製造轻型商用车、汽车和电动车的高回弹泡棉座椅、硬质泡棉隔热板、B柱、车顶内衬、悬吊绝缘体、保险桿和其他内装零件。

- 在欧洲,德国、俄罗斯、波兰、法国、英国、比利时和义大利等国对环氧树脂的使用正在增加。这些国家的汽车生产能力正在不断提高,汽车零件中轻质塑胶的使用也不断增加。 2021年轻型商用车产量增加至210万辆,较2020年成长1%。这导致该地区丙烯酸、硅胶和其他树脂基黏合剂和密封剂的使用增加。

- 该地区政府实施的严格排放法规以及汽车製造商向汽车电气化的转变预计将在预测期内推动欧洲汽车黏合剂市场的成长。由于汽车黏合剂相对于传统金属焊接具有优势,预计市场将显着成长。据称,汽车黏合剂还可以降低汽车噪音、震动和声振,带来更舒适的驾驶体验。因此,考虑到这些因素,预计预测期内(2022-2028 年)市场复合年增长率为 4.57%。

政府减少二氧化碳排放的法规将促进电动车製造并刺激市场需求

- 由于全球汽车标准的变化、西欧需求减弱以及国际贸易紧张局势,2018年和2019年欧洲对汽车黏合剂和密封剂的需求略有下降。 2020年,欧洲对汽车黏合剂和密封剂的需求将下降20%,因为由于COVID-19疫情造成的营运和供应链限制,汽车产量将从2019年的2156万辆下降到2020年的1,690万辆。

- 由于德国拥有一体化的价值链和由研发基础设施支援的强大製造能力,德国占据欧洲国家中汽车黏合剂和密封剂需求的最大份额。 2021年,德国生产了330万辆汽车,占欧洲汽车产量的20%。

- 聚氨酯和环氧基黏合剂和密封剂是该地区最常用的黏合剂和密封剂,因为它们可以用作结构性黏着剂,以增加车辆的承载能力。除了电绝缘性能外,它还具有耐热性和耐化学性,使其成为 PCB(印刷基板)应用的理想选择。预计2021年聚氨酯产品消费量将达8,500万公斤,到2028年将达到1.056亿公斤,复合年增长率为3.16%。

- 《Fit for 55》法案是欧盟委员会气候变迁目标的一部分,旨在到 2030 年将温室气体排放减少至少 55%。 《Fit for 55》法案设定的目标是到 2030 年将汽车的二氧化碳排放排放55%,货车的二氧化碳排放量减少 50%。这项法规将刺激对电动车的需求,预计在预测期内将刺激对聚氨酯、丙烯酸和硅胶产品的需求,这些产品也可用于汽车电子产品。

欧洲汽车胶合剂和密封剂市场趋势

政府推广电动车的支持措施将扩大电动车产业

- 欧洲人均GDP为34,230美元,2022与前一年同期比较成长1.6%。汽车工业部门约占GDP总量的2%。 2021年,欧洲汽车产量将占乘用车81%,商用车17%,其他2%。

- 2020年,德国、义大利、西班牙、俄罗斯、英国等多个欧洲国家都受到新冠疫情影响。疫情扰乱了供应链,导致各国工厂关闭,并造成晶片短缺,影响了欧洲的汽车生产。汽车产量与2019年相比大幅下降22%。

- 美国25.3%的汽车进口来自欧洲,其中德国和英国是主要进口国,2021年分别占10.3%和4.7%。 2022年初,俄罗斯入侵乌克兰导致新车销售下降20.5%,也反映在汽车产量上。 2022年第一季欧洲汽车市场与去年同期相比下降了10.6%。

- 由于许多欧洲国家正在对电动车进行新的投资,因此在 2022-2027 年期间,汽车产量的复合年增长率可能达到 2.25%。例如,西班牙计划投资51亿美元用于电动车生产。

欧洲汽车胶合剂和密封剂产业概况

欧洲汽车黏合剂和密封剂市场相当集中,前五大公司占据了66.71%的市场。该市场的主要企业包括 3M、HB Fuller Company、Henkel AG & Co. KGaA、Huntsman International LLC、Sika AG 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 车

- 法律规范

- EU

- 俄罗斯

- 价值炼和通路分析

第五章市场区隔

- 树脂

- 丙烯酸纤维

- 氰基丙烯酸酯

- 环氧树脂

- 聚氨酯

- 硅胶

- VAE・EVA

- 其他的

- 科技

- 热熔胶

- 反应性

- 密封剂

- 溶剂型

- 紫外线固化胶合剂

- 水性

- 国家

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 英国

- 其他欧洲国家

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Sika AG

第七章:CEO面临的关键策略问题

第 8 章 附录

- 全球黏合剂和密封剂产业概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 驱动因素、限制因素和机会

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 92420

The Europe Automotive Adhesives & Sealants Market size is estimated at 1.51 billion USD in 2024, and is expected to reach 1.82 billion USD by 2028, growing at a CAGR of 4.73% during the forecast period (2024-2028).

Increasing shift toward vehicle electrification by automobile players to propel market growth

- Polyurethane, epoxy, and acrylic resins account for a large share of the European automotive adhesives and sealants market. The share of polyurethane resins is higher as they are most commonly used in the automotive industry to manufacture high-resilience foam seating, rigid foam insulation panels, B-pillars, headliners, suspension insulators, bumpers and other interior parts of light commercial vehicles, cars, and electric vehicles.

- In Europe, the usage of epoxy resins is increasing in countries like Germany, Russia, Poland, France, the United Kingdom, Belgium, and Italy. The use of lightweight resins in automotive vehicle parts increased along with automotive vehicle production capacities in these countries. In 2021, the production of light commercial vehicles increased to 2.1 million units, an increase of 1% over 2020. Thus, the usage of acrylic, silicone, and other resin-based adhesives and sealants increased in the region.

- The stringent emission norms implemented by governments in the region and the shift toward vehicle electrification by players are expected to boost the growth of the European automotive adhesives market over the forecast period. The market is expected to witness significant growth owing to the benefits offered by automotive adhesives over traditional metal welding. Automotive adhesives also reduce the noise, harshness, and vibration of the vehicle and provide comfortable driving. Hence, owing to such factors, the market is estimated to register a CAGR of 4.57% during the forecast period (2022-028).

Government legislations to reduce Co2 emissions to boost electric vehicle manufacturing in turn boosting market demand

- Europe's automotive adhesives and sealants demand declined slightly in 2018 and 2019 due to changes in global vehicle standards and demand falls in western Europe and international trade conflicts. In 2020, Europe's automotive adhesives and sealants demand decreased by 20% as vehicle production fell from 21.56 million units in 2019 to 16.9 million units in 2020 due to operational and supply chain restrictions caused by the COVID-19 pandemic.

- Germany has the largest share of the demand for automotive adhesives and sealants among European countries due to its large manufacturing capacity, which is supported by the integrated value chain and R&D infrastructure of the country. In 2021, Germany manufactured 3.3 million units which constitute up to 20% of the total vehicles manufactured in Europe.

- Polyurethane and epoxy-based adhesives and sealants are most commonly used in the region because they can be used as structural adhesives to enhance the load-bearing capacity of the vehicle. They also offer heat and chemical resistance along with electric insulation, which makes them ideal for PCB (Printed Circuit Board) applications. In 2021, 85 million kilograms of polyurethane-based products were consumed, and by 2028 this is expected to reach 105.6 million kilograms with a CAGR of 3.16%.

- As part of the European commission's climate goals to reduce greenhouse house emissions by at least 55% by 2030. The legislation 'Fit for 55' sets targets to reduce CO2 emissions from cars by 55% and vans by 50% by 2030. This regulation has boosted the demand for electric vehicles, which in turn is expected to boost the demand for PU, acrylic, and silicone-based products in the forecast period, as they can also be used in automotive electronics.

Europe Automotive Adhesives & Sealants Market Trends

Supportive government initiatives to promote electric vehicles will raise the industry size

- Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

- In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

- The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

- Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Europe Automotive Adhesives & Sealants Industry Overview

The Europe Automotive Adhesives & Sealants Market is fairly consolidated, with the top five companies occupying 66.71%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Automotive

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 Illinois Tool Works Inc.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球汽车黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球汽车黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球汽车黏合剂市场报告

2026年全球汽车黏合剂市场报告 汽车密封剂市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年汽车黏合剂和密封剂市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、树脂、技术、地区和竞争格局划分,2021-2031年

汽车密封剂市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年汽车黏合剂和密封剂市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、树脂、技术、地区和竞争格局划分,2021-2031年 汽车外饰轻质黏合剂市场按产品类型、技术、基材类型、应用和最终用途划分,全球预测(2026-2032年)汽车车身黏合剂市场按产品类型、车辆类型、应用方法、用途和分销管道划分,全球预测(2026-2032年)

汽车外饰轻质黏合剂市场按产品类型、技术、基材类型、应用和最终用途划分,全球预测(2026-2032年)汽车车身黏合剂市场按产品类型、车辆类型、应用方法、用途和分销管道划分,全球预测(2026-2032年) 日本汽车黏合剂市场报告(按技术、树脂类型、车辆类型、应用(白车身、动力总成、涂装车间、组装)和地区划分,2026-2034 年)

日本汽车黏合剂市场报告(按技术、树脂类型、车辆类型、应用(白车身、动力总成、涂装车间、组装)和地区划分,2026-2034 年) 轮胎密封剂市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

轮胎密封剂市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测 汽车黏合剂和密封剂市场规模、份额和成长分析(按技术、功能、产品、应用、车辆类型和地区划分)—产业预测(2026-2033 年)空气滤清器胶黏剂市场(按胶黏剂类型、材料类型、应用、最终用户产业和销售管道)——2025-2030 年全球预测

汽车黏合剂和密封剂市场规模、份额和成长分析(按技术、功能、产品、应用、车辆类型和地区划分)—产业预测(2026-2033 年)空气滤清器胶黏剂市场(按胶黏剂类型、材料类型、应用、最终用户产业和销售管道)——2025-2030 年全球预测

▼