|

市场调查报告书

商品编码

1692584

北美汽车黏合剂和密封剂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)North America Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

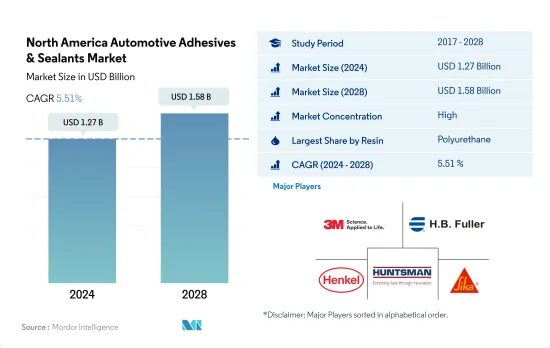

北美汽车黏合剂和密封剂市场规模预计在 2024 年达到 12.7 亿美元,预计到 2028 年将达到 15.8 亿美元,预测期内(2024-2028 年)的复合年增长率为 5.51%。

汽车产业采用永续性将推动市场成长

- 聚氨酯树脂占据北美汽车黏合剂和密封剂市场的最大份额。北美聚氨酯接着剂的使用量高于任何其他树脂。主要原因是该地区拥有大量生产设施。 2017年至2019年,因汽车产量下降,消费成长率稳定下降,达-3%左右。疫情过后,消费将成长3%。聚氨酯接着剂预计在 2022 年至 2028 年期间达到 3.1% 的复合年增长率。

- 同时,环氧胶黏剂和丙烯酸胶黏剂在汽车胶黏剂市场也占有重要地位。然而,明年对环氧树脂来说可能是一个重大挑战,因为用于製造环氧黏合剂的原料本质上是危险的,因此受到美国政府的监管。环氧树脂胶黏剂将成为第二大消费材料,2022 年至 2028 年的复合年增长率约为 3.14%。紧随其后的是丙烯酸胶黏剂,2022 年至 2028 年的复合年增长率约为 3.01%。

- 氰基丙烯酸酯和硅胶密封胶等黏合剂正在蓬勃发展。汽车产业广泛采用永续性概念,电动车产量正在大幅增加。这导致这些黏合剂在组装电子元件中的使用增加,这可能会导致未来几年的需求增加。在预测期(2022-2028 年),氰基丙烯酸酯和硅胶黏合剂的产量复合年增长率超过 2.5%。

「以胶粘代替焊接」趋势日益增长,显着促进了汽车胶粘剂的需求

- 由于美国拥有巨大的汽车製造能力,北美汽车黏合剂和密封剂市场以美国为主导。美国是世界第二大汽车生产国,2021 年生产了 917 万辆汽车,而墨西哥和加拿大分别生产了 310 万辆和 110 万辆。

- 「以胶黏代替焊接」的日益流行,极大地促进了该地区对汽车黏合剂和密封剂的需求。随着汽车製造商不断创新,使汽车更轻,从而节省燃料并减少二氧化碳排放,塑胶车顶、保险桿或碰撞相关部件的黏合剂黏合已成为螺丝、铆钉和焊接等传统连接方法的有效替代方案。

- 聚氨酯基黏合剂和密封剂因其灵活性(包括宽工作温度范围、热湿固化和涂漆性)而成为北美汽车行业最常用的材料,预计到 2021 年将占据 26.3% 的份额。环氧黏合剂和密封剂是其他树脂类型中第二大使用材料,到 2021 年将占 21.5% 的份额。

- 到2028年,北美丙烯酸黏合剂的份额预计将从2021年的16%扩大到20%。这是因为它能够与塑胶和复合材料结合以减轻车辆重量,并可用于电池组装操作。

北美汽车胶合剂和密封剂市场趋势

政府推出电动车措施支持汽车生产

- 北美汽车产业是贡献其经济3%以上份额的重要产业之一。在这三个国家中,美国是最大的汽车生产国,市占率超过65%,其次是墨西哥,市占率23%,加拿大为8%。

- 该地区的汽车销售量大幅降低了整体产量,从而影响了黏合剂的使用。 2017-18 年和 2018-19 年的变化范围为 -0.2% 至 -3.7%。此外,2019-20年,该地区的生产因新冠疫情而受到严重影响。由于製造工厂关闭和供应链中断而导致的汽车零件短缺可能会限制生产水准。从波动来看,该地区的降幅约为20%。然而,2021 年汽车需求的成长可能会导致全部区域的黏合剂使用量增加。

- 北美电动车市场也为黏合剂带来了成长机会。电动车和混合动力汽车的产量和采用率的不断提高将推动汽车电子元件组装中黏合剂的使用量增加。美国不仅是全部区域,也是世界上最大的电动车生产国之一。美国联邦政府的目标是到2030年电动车占新车和轻型卡车销售的50%。同时,许多州也宣布了更积极的目标。这些因素可能会增加对黏合剂的需求,从而导致预测期内更好的成长。

北美汽车胶合剂和密封剂产业概况

北美汽车黏合剂和密封剂市场相当集中,前五大公司占据了66.62%的市场份额。该市场的主要企业有:3M、HB Fuller Company、Henkel AG & Co. KGaA、Huntsman International LLC 和 Sika AG(按字母顺序排列)

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 车

- 法律规范

- 加拿大

- 墨西哥

- 美国

- 价值炼和通路分析

第五章市场区隔

- 树脂

- 丙烯酸纤维

- 氰基丙烯酸酯

- 环氧树脂

- 聚氨酯

- 硅胶

- VAE・EVA

- 其他树脂

- 科技

- 热熔胶

- 反应性

- 密封剂

- 溶剂型

- 紫外线固化胶合剂

- 水性

- 国家

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介.

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- Dow

- DuPont

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Sika AG

第七章:CEO面临的关键策略问题

第 8 章 附录

- 全球黏合剂和密封剂产业概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 驱动因素、阻碍因素和机会

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

The North America Automotive Adhesives & Sealants Market size is estimated at 1.27 billion USD in 2024, and is expected to reach 1.58 billion USD by 2028, growing at a CAGR of 5.51% during the forecast period (2024-2028).

Adoption of sustainability in the automotive industry to create upswings for the market growth

- In the North American automotive adhesives and sealants market, polyurethane resins cover the largest share. The usage of polyurethane adhesive in North America is higher than other resins. The main reason behind this factor is that the region includes production facilities to a large extent. From 2017 to 2019, the consumption growth rate reduced steadily and recorded about -3%, and this is due to the reduction in automotive production. After the pandemic, consumption leads to a growth of 3%. Polyurethane adhesives are registering a CAGR of 3.1% between 2022 to 2028.

- On the other hand, epoxy and acrylic adhesives also show their great presence in the automotive adhesives market. However, for epoxy, the upcoming year could be a great challenge as the raw materials used to produce epoxy adhesives are hazardous in nature and, thus, are getting regulated by the US government. Epoxy adhesive is the second largest consumed material, with a CAGR of about 3.14% from 2022 to 2028. Epoxy adhesives are followed by acrylic adhesives, which register a CAGR of about 3.01% between 2022 to 2028.

- Adhesives, such as cyanoacrylate and silicone sealants, are on a booming trend. The adoption of sustainability in the automotive industry is getting increased widely, and EV production is increasing to a large extent. Owing to this, the usage of these adhesives for electronic component assembly is increasing, which, as a result, may lead to increased demand in the coming years. Cyanoacrylate and silicone adhesives recorded a CAGR of above 2.5% in terms of volume during the forecast period (2022-2028).

Growing trend of 'bonding instead of welding' to significantly contribute to the demand for automotive adhesives

- The North American automotive adhesives and sealants market is dominated by the United States due to the huge automotive production capacity of the country. The United States ranks 2nd globally in automotive production, with 9.17 million produced in 2021, whereas Mexico produced 3.1 million units and Canada produced 1.1 million units.

- The growing trend of 'bonding instead of welding' has significantly contributed to the demand generated for automotive adhesives and sealants in the region. As automakers are always innovating to make vehicles lighter to save fuel and reduce CO2 emissions, usage of adhesives for plastic roofs, bumpers, or crash-relevant parts - bonded joints became an effective alternative to traditional joining procedures, such as screws, rivets, or welding.

- Polyurethane-based adhesives and sealants are most commonly used in the automotive industry in the North American region occupying a share of 26.3% in 2021 due to their flexibility, like wide operating temperature range, heat cured and moisture cured, and paintability. Epoxy adhesives and sealants are the second most commonly used among other resin types, with a share of 21.5% in 2021 because of the stronger metal-to-metal bonding property.

- In 2028, the share of acrylic adhesives in the North American region is expected to grow up to 20% from 16% in 2021 due to their ability to bind to plastic and composite materials to lighten the weight of vehicles and applicability in battery assembly operations.

North America Automotive Adhesives & Sealants Market Trends

Government initiatives for electric vehicles to support the automotive production

- North American automotive is one of the prominent sectors which helps to generate above 3% of its economy. Among all the 3 countries, the United States is the largest automotive producer, covering more than 65% of shares, followed by Mexico with 23% of shares and Canada with 8% of shares.

- Vehicle sales in the region have majorly declined its overall production, owing to which the utilization of adhesives is impacted. In 2017-18 and 2018-19, the variation change has been recorded from -0.2% to -3.7%. Moreover, in 2019-20, due to the COVID-19 pandemic, regional production has been largely impacted. The shutdown of manufacturing facilities and the shortage of vehicle components due to disruption in the supply chain tend to constrain the production level. In terms of variation, the region has recorded about a 20% decline. However, in 2021, the demand for automotive is rising, which, on the other hand, may increase the utilization of adhesives across the region.

- The EV market in North America is another opportunity for adhesives to grow. The rising production and adoption of EVs and Hybrid vehicles tend to raise the usage of adhesives for electronic component assembly in the vehicles. The United States is one of the largest producers of EVs globally as well as across the region. The federal government's goal in the United States is for EVs to account for 50% of new passenger vehicles and light truck sales by 2030. Simultaneously, a number of particular states have announced more aggressive targets. These factors tend to increase the demand for adhesives and will result in better growth in the forecast period.

North America Automotive Adhesives & Sealants Industry Overview

The North America Automotive Adhesives & Sealants Market is fairly consolidated, with the top five companies occupying 66.62%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Automotive

- 4.2 Regulatory Framework

- 4.2.1 Canada

- 4.2.2 Mexico

- 4.2.3 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Dow

- 6.4.5 DuPont

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Huntsman International LLC

- 6.4.9 Illinois Tool Works Inc.

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

全球汽车黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球汽车黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球汽车黏合剂市场报告

2026年全球汽车黏合剂市场报告 汽车黏合剂和密封剂市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、树脂、技术、地区和竞争格局划分,2021-2031年

汽车黏合剂和密封剂市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、树脂、技术、地区和竞争格局划分,2021-2031年 汽车外饰轻质黏合剂市场按产品类型、技术、基材类型、应用和最终用途划分,全球预测(2026-2032年)汽车车身黏合剂市场按产品类型、车辆类型、应用方法、用途和分销管道划分,全球预测(2026-2032年)

汽车外饰轻质黏合剂市场按产品类型、技术、基材类型、应用和最终用途划分,全球预测(2026-2032年)汽车车身黏合剂市场按产品类型、车辆类型、应用方法、用途和分销管道划分,全球预测(2026-2032年) 日本汽车黏合剂市场报告(按技术、树脂类型、车辆类型、应用(白车身、动力总成、涂装车间、组装)和地区划分,2026-2034 年)

日本汽车黏合剂市场报告(按技术、树脂类型、车辆类型、应用(白车身、动力总成、涂装车间、组装)和地区划分,2026-2034 年) 轮胎密封剂市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

轮胎密封剂市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测 汽车黏合剂和密封剂市场规模、份额和成长分析(按技术、功能、产品、应用、车辆类型和地区划分)—产业预测(2026-2033 年)汽车胶合剂市场(按产品、形式、车型、应用、分销管道和最终用户划分)—2025-2030 年全球预测空气滤清器胶黏剂市场(按胶黏剂类型、材料类型、应用、最终用户产业和销售管道)——2025-2030 年全球预测

汽车黏合剂和密封剂市场规模、份额和成长分析(按技术、功能、产品、应用、车辆类型和地区划分)—产业预测(2026-2033 年)汽车胶合剂市场(按产品、形式、车型、应用、分销管道和最终用户划分)—2025-2030 年全球预测空气滤清器胶黏剂市场(按胶黏剂类型、材料类型、应用、最终用户产业和销售管道)——2025-2030 年全球预测