|

市场调查报告书

商品编码

1693424

汽车黏合剂和密封剂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Automotive Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

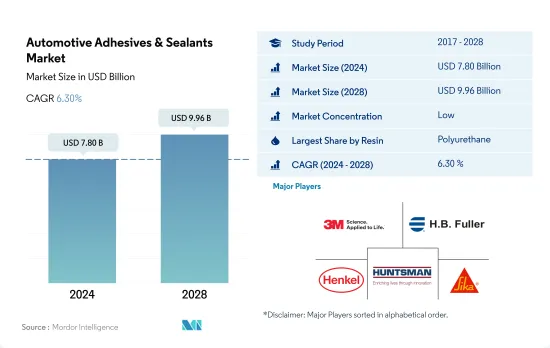

汽车黏合剂和密封剂市场规模预计在 2024 年达到 78 亿美元,预计到 2028 年将达到 99.6 亿美元,预测期内(2024-2028 年)的复合年增长率为 6.30%。

汽车技术进步推动市场需求

- 全球汽车市场的车辆数量预计将以每年 2% 的复合年增长率增长,预计这将在 2022-2028 年预测期内推动对汽车黏合剂和密封剂的需求。

- 全球主要企业都在致力于减轻车辆重量,以提高燃油效率并降低成本。为了实现这一目标,汽车公司正在使用汽车黏合剂和密封剂来代替笨重的金属框架和连接部件,例如焊接接头。预计这些技术发展将在预测期内增加对汽车黏合剂和密封剂的需求。

- 基于聚氨酯、环氧树脂和丙烯酸树脂的黏合剂和密封剂主要用于汽车,因为它们广泛应用于各种基材,如玻璃、塑胶、陶瓷、金属和复合材料,这些基材是汽车製造的主要结构材料。由于这些材料的采用,黏合剂和密封剂也已成为汽车製造不可或缺的一部分。

- 2021 年,VAE/EVA 树脂基汽车胶合剂和密封剂占据了近 8% 的市场份额,这得益于效用在汽车製造中用作热熔胶,用于座椅和内饰、汽车电子元件的紧固以及汽车售后市场,尤其是座椅和内饰。热熔胶对皮革、织物、玻璃和聚合物表面具有良好的黏合性。

「以胶黏代替焊接」的日益普及对市场需求做出了巨大贡献。

- 亚太地区是世界上最大的汽车生产区,其中中国、印度和日本等国家是全球主要的汽车生产国。该地区的汽车产量预计将从 2021 年的 4,790 万辆增长到 2022 年的 5.9%。 2020 年,包括中国、印度、马来西亚、日本和印尼在内的许多国家都受到了新冠疫情的影响。由于生产设施关闭、国际边境关闭以及多个国家原材料短缺,汽车黏合剂和密封剂的消费量与 2019 年相比下降了近 13.3%。

- 美国凭藉其庞大的汽车生产能力,在北美汽车胶合剂市场占据主导地位。美国是世界第二大汽车生产国,2021年生产汽车917万辆,墨西哥生产310万辆,加拿大生产110万辆。

- 「以胶黏代替焊接」的日益普及对该地区汽车黏合剂和密封剂的需求产生了巨大影响。由于汽车製造商不断创新,使汽车更轻,从而提高燃油效率并减少二氧化碳排放,在塑胶车顶、保险桿或碰撞相关部件中使用黏合剂,使黏合剂黏合成为螺丝、铆钉或焊接等传统连接方法的有效替代方案。

- 作为欧盟委员会气候变迁目标的一部分,即到 2030 年将温室气体排放减少至少 55%,《Fit for 55》法规设定了到 2030 年将汽车二氧化碳排放减少 55%,排放二氧化碳排放量减少 50% 的目标。预计该法规将刺激对电动车的需求,从而预计在 2022-2028 年预测期内增加对汽车黏合剂和密封剂的需求。

全球汽车胶合剂和密封剂市场趋势

政府推行的电动车优惠政策将推动汽车产业

- 预计自2021年起全球汽车产业将稳定成长,但随着消费者对拥有个人汽车的偏好下降并越来越偏好共用出行方式,成长速度正在放缓。预计预测期内全球汽车产业将以每年 2% 的速度成长,总收益增加价值将达到 1.5 兆美元。

- 2020年,受新冠疫情影响,汽车销量下滑,但2021年却迅速回升。汽车市场通常对GDP贡献巨大,因此世界各国政府纷纷推出措施支持经济。汽车销量从2019年的9000万辆下降到2020年的7800万辆。

- 由于电动车能源成本低廉、环境友善且移动性高效,其在全球范围内的普及对全球汽车市场的总收益做出了重大贡献。各种政府政策和标准也在推动电动车产量的成长。例如,欧盟二氧化碳排放标准在2021年增加了对电动车的需求。根据国际能源总署的永续情景,到2030年将需要2.3亿辆电动车取代燃油汽车。 2021年,最大的电动车製造商特斯拉的电动车产量增加了157%。预计预测期内(2022-2028 年),消费者对电动车的偏好将进一步成长。

汽车胶合剂和密封剂产业概况

汽车胶合剂和密封剂市场分散,前五大公司占34.49%的市场。该市场的主要企业有:3M、HB Fuller Company、Henkel AG & Co. KGaA、Huntsman International LLC 和 Sika AG(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 车

- 法律规范

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中国

- EU

- 印度

- 印尼

- 日本

- 马来西亚

- 墨西哥

- 俄罗斯

- 沙乌地阿拉伯

- 新加坡

- 南非

- 韩国

- 泰国

- 美国

- 价值炼和通路分析

第五章市场区隔

- 树脂

- 丙烯酸纤维

- 氰基丙烯酸酯

- 环氧树脂

- 聚氨酯

- 硅胶

- VAE・EVA

- 其他树脂

- 科技

- 热熔胶

- 反应性

- 密封剂

- 溶剂型

- 紫外线固化胶合剂

- 水

- 地区

- 亚太地区

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 新加坡

- 韩国

- 泰国

- 其他亚太地区

- 欧洲

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 英国

- 其他欧洲国家

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

- 加拿大

- 墨西哥

- 美国

- 北美其他地区

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地区

- 亚太地区

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介.

- 3M

- Arkema Group

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dow

- DuPont

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Huntsman International LLC

- Illinois Tool Works Inc.

- PPG Industries, Inc.

- SHINSUNG PETROCHEMICAL

- Sika AG

- ThreeBond Holdings Co., Ltd.

第七章:CEO面临的关键策略问题

第 8 章 附录

- 全球黏合剂和密封剂产业概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 驱动因素、阻碍因素和机会

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 92483

The Automotive Adhesives & Sealants Market size is estimated at 7.80 billion USD in 2024, and is expected to reach 9.96 billion USD by 2028, growing at a CAGR of 6.30% during the forecast period (2024-2028).

Growing technological advancements in automobiles to augment market demand

- The number of vehicles in the global automotive market is expected to record a CAGR of 2% annually, which is expected to lead to an increase in the demand for adhesives and sealants required for the automotive industry in the forecast period 2022-2028.

- The major companies worldwide are working on making vehicles lighter in weight for better fuel efficiency and as cost-cutting measures. To achieve this, automotive companies are using automotive adhesives and sealants to replace bulkier metal frames and joinery components, such as weld joints. These technological developments are expected to increase demand for automotive adhesives and sealants in the forecast period.

- Polyurethane, epoxy, and acrylic resin-based adhesives and sealants are majorly used in automobiles because of their wide-ranging applicability to different substrates, such as glass, plastic, ceramics, metals, and composites, which are major materials of construction in the industry for the production of automobiles. Adhesives and sealants have also become integral parts of automobile manufacturing with the adoption of these materials.

- VAE/EVA resin-based automotive sealants and adhesives accounted for nearly 8% of the market value share in 2021 because of their utility as hot melt adhesives in the manufacturing of automobiles for applications, such as seats and interior, automobile electronic components fixation, and in the automotive aftermarket, specifically for seats and interiors. The hot melt adhesives offer good adhesion for leather, fabric, glass, and polymer-based surfaces.

The growing trend of 'bonding instead of welding' has significantly contributed to the market demand

- The Asia-Pacific is the largest producer of vehicles in the world, as countries like China, India, and Japan are some of the major vehicle producers across the globe. Vehicle production in the region was expected to grow by 5.9% in 2022 from 47.9 million units in 2021. In 2020, many countries, including China, India, Malaysia, Japan, and Indonesia, were impacted by the COVID-19 pandemic. The consumption of automotive adhesives and sealants declined by nearly 13.3% compared to 2019 due to the shutdown of production facilities, the closing of international borders, and raw material shortages in several countries.

- The United States dominates the North American automotive adhesives market due to its huge automotive production capacity. The United States ranks second globally in automotive production, with 9.17 million units produced in 2021, whereas Mexico made 3.1 million units and Canada made 1.1 million units.

- The growing trend of 'bonding instead of welding' has significantly contributed to the region's demand for automotive adhesives and sealants. As automakers are always innovating to make vehicles lighter to improve fuel efficiency and reduce CO2 emissions, usage of adhesives for plastic roofs, bumpers, or crash-relevant parts - bonded joints have become an effective alternative to traditional joining procedures such as screws, rivets, or welding.

- As part of the European Commission's climate goals to reduce greenhouse house emissions by at least 55% by 2030, The legislation 'Fit for 55' sets targets to reduce CO2 emissions from cars by 55% and vans by 50% by 2030. This regulation is expected to boost the demand for electric vehicles, which, in turn, is expected to increase the demand for automotive adhesives and sealants over the forecast period 2022-2028.

Global Automotive Adhesives & Sealants Market Trends

Favorable government policies to promote electric vehicles will propel automotive industry

- Since 2021, the global automotive industry has been expected to grow steadily but at a slower pace because of the decline in consumers' preferences for individual ownership of passenger vehicles and their increased preference for shared mobility in transportation. The global automotive industry is expected to experience a growth rate of 2% annually, with an expected value addition of USD 1.5 trillion in total revenue during the forecast period.

- In 2020, due to the impact of the COVID-19 pandemic, vehicle sales declined but recovered rapidly in 2021 because the governments of various countries took measures to support their economies, as automotive markets usually contribute majorly to their GDP. Vehicle sales declined from 90 million units of passenger vehicles in 2019 to 78 million units in 2020.

- The introduction of electric vehicles worldwide has contributed significantly to the overall revenue of the global automotive market because of their cheaper energy costs, environmentally benign nature, and efficient mobility features. Various government policies and standards also work as driving factors to increase EV production. For instance, the EU standards for CO2 emissions increased the demand for electric vehicles in 2021. As per the IEA's Sustainable Scenario, 230 million electric vehicles are required to replace combustion fuel-based vehicles by 2030. In 2021, Tesla, the largest EV manufacturer, recorded a rise of 157% in the number of electric vehicles manufactured. This growing trend of consumers preferring electric vehicles is expected to rise further during the forecast period (2022-2028).

Automotive Adhesives & Sealants Industry Overview

The Automotive Adhesives & Sealants Market is fragmented, with the top five companies occupying 34.49%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Automotive

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Sealants

- 5.2.4 Solvent-borne

- 5.2.5 UV Cured Adhesives

- 5.2.6 Water-borne

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.5 Dow

- 6.4.6 DuPont

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hubei Huitian New Materials Co. Ltd

- 6.4.10 Huntsman International LLC

- 6.4.11 Illinois Tool Works Inc.

- 6.4.12 PPG Industries, Inc.

- 6.4.13 SHINSUNG PETROCHEMICAL

- 6.4.14 Sika AG

- 6.4.15 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

全球汽车黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球汽车黏合剂市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球汽车黏合剂市场报告

2026年全球汽车黏合剂市场报告 汽车黏合剂和密封剂市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、树脂、技术、地区和竞争格局划分,2021-2031年

汽车黏合剂和密封剂市场-全球产业规模、份额、趋势、机会、预测:按车辆类型、树脂、技术、地区和竞争格局划分,2021-2031年 汽车外饰轻质黏合剂市场按产品类型、技术、基材类型、应用和最终用途划分,全球预测(2026-2032年)汽车车身黏合剂市场按产品类型、车辆类型、应用方法、用途和分销管道划分,全球预测(2026-2032年)

汽车外饰轻质黏合剂市场按产品类型、技术、基材类型、应用和最终用途划分,全球预测(2026-2032年)汽车车身黏合剂市场按产品类型、车辆类型、应用方法、用途和分销管道划分,全球预测(2026-2032年) 日本汽车黏合剂市场报告(按技术、树脂类型、车辆类型、应用(白车身、动力总成、涂装车间、组装)和地区划分,2026-2034 年)

日本汽车黏合剂市场报告(按技术、树脂类型、车辆类型、应用(白车身、动力总成、涂装车间、组装)和地区划分,2026-2034 年) 轮胎密封剂市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

轮胎密封剂市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测 汽车黏合剂和密封剂市场规模、份额和成长分析(按技术、功能、产品、应用、车辆类型和地区划分)—产业预测(2026-2033 年)汽车胶合剂市场(按产品、形式、车型、应用、分销管道和最终用户划分)—2025-2030 年全球预测空气滤清器胶黏剂市场(按胶黏剂类型、材料类型、应用、最终用户产业和销售管道)——2025-2030 年全球预测

汽车黏合剂和密封剂市场规模、份额和成长分析(按技术、功能、产品、应用、车辆类型和地区划分)—产业预测(2026-2033 年)汽车胶合剂市场(按产品、形式、车型、应用、分销管道和最终用户划分)—2025-2030 年全球预测空气滤清器胶黏剂市场(按胶黏剂类型、材料类型、应用、最终用户产业和销售管道)——2025-2030 年全球预测

▼