|

市场调查报告书

商品编码

1693682

託管数位工作场所服务:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Managed Digital Workplace Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

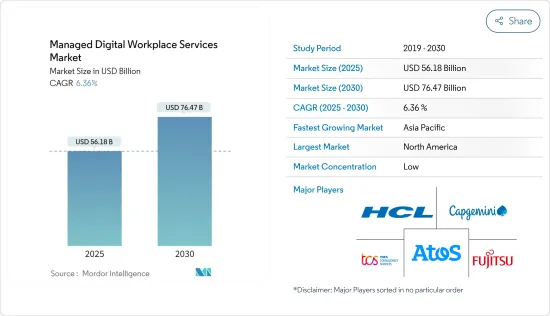

託管数位工作场所服务市场规模预计在 2025 年为 561.8 亿美元,预计到 2030 年将达到 764.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.36%。

託管数位化工作场所服务的驱动因素包括技术进步、劳动力人口结构的变化、新技术和工具的可用性、员工对更多灵活性的渴望以及强大而富有爱心的经营团队培育的积极的公司文化。此外,成功的数位转型取决于有效的变革管理、员工参与度以及对转型目标和目的的清晰理解等因素。

主要亮点

- 在预测期内,各组织越来越多地采用数位化工作场所可能会推动对託管数位化工作场所服务的需求。例如,beautiful.ai 在 2022 年对 3,000 名管理人员进行的一项调查中探讨了数位化工作场所如何影响他们的业务以及远端工作者的未来发展,78% 的受访者同意投入大量财力资源来确保数位化工作场所的成功,80% 的受访者表示他们致力于在数位化财力和工具方面致力于管理人员的企业企业。 81%的人乐观地认为数位化工作将取代办公室工作。即使在数位化职场,66% 的人也感觉联繫更加紧密。

- 此外,IT 技术对託管数位工作场所服务产生了重大影响。随着数位平台和自动化的使用日益增多,工作场所变得更有效率和精简。例如,云端基础的设施管理软体可以让企业领导者保持井然有序和最新状态,从而提高业务绩效。此外,数位化工作场所技术提供更好的工作流程和资料管理,并专注于通讯、资讯管理和网路安全。

- 此外,人工智慧在管理数位化工作场所营运方面变得越来越重要。透过自动化任务和提供智慧洞察,人工智慧使组织能够简化工作流程、提高生产力并改善员工体验。数位化工作场所中的人工智慧应用范例包括知识管理、资料管治、资讯管理、最终使用者体验管理和文件管理。此外,人工智慧可以帮助组织制定有效的工作场所自动化策略并提高员工的工作效率。随着人工智慧技术的不断发展,预计它将在塑造数位化工作场所的未来方面发挥更重要的作用。

- 此外,BFSI 领域的技术和客户格局的变化可能会在预测期内推动对託管数位工作场所服务的需求。许多 BFSI 行业的公司,例如保险公司瑞士再保险公司,已经与市场供应商合作,实现云端基础的数位化工作场所,预计这一趋势将在未来几年加剧,从而增加 BFSI 行业的需求。此外,全球银行和保险公司日益增长的数位转型正在推动数位化工作场所转型的需求,以提高效率和生产力,进一步增强研究市场的成长前景。

- 日益猖獗的网路犯罪为全球託管数位工作场所服务市场带来了重大挑战和限制。保护数位资产、防御网路威胁以及遵守资料保护条例对于组织来说都是具有挑战性的任务。由于网路犯罪对客户信任的影响以及对增加网路安全投资的呼吁,强有力的安全措施和主动的安全管理对于提供託管数位工作场所服务至关重要。

- 疫情过后,混合型和现场工作越来越受欢迎。世界各地的组织必须适应不同实体职场环境中的这种新常态,并改善其企业数位化工作场所。预计这种工作转变将影响对託管数位工作场所服务的需求,以改善工作实践,确保持续的生产力、营运和业务成功。疫情爆发后,各家公司纷纷联合起来,利用数位化工作场所的优势。这种加强的合作可能会促进疫情期间研究市场的成长。

託管数位工作场所服务市场趋势

医疗保健产业预计将出现强劲成长

- 在医疗保健行业,采用新技术已经变得很普遍,以改善患者护理和体验以及职场管理。医疗保健行业的人员配置安排多种多样且复杂,包括大型团队、兼职、全职、随叫随到、季节性、远端和现场工作人员以及具有多种角色和专业的工作人员。这个行业涉及许多协调和特殊性,这就是为什么实施管理解决方案如此重要。

- 此外,降低医院和其他医疗机构的人事费用、提高业务效率和整合部门的需求日益增长,是推动采用此类解决方案的主要因素。此外,预测期内,医疗保健专业人员日益增长的需求以及职场管理解决方案带来的好处(例如职场透明度和灵活排班)也有望增加这些解决方案在医疗保健领域的采用。

- 此外,对医疗服务的需求不断增长,导致对医疗设施建设的投资增加。医疗保健设施市场的成长是由于世界各地人口的成长和老化。这可能会导致医疗保健领域更多地采用託管数位工作场所服务。例如,根据经合组织和世界卫生组织的研究,预计未来五年全球医院数量将稳定成长。数据显示,预计五年内医院数量将达到166,235家。

- 许多医疗保健提供者正在投资扩大和建造新的医疗设施。例如,2022 年 6 月,南卡罗来纳州卫生和环境控制部核准罗珀圣弗朗西斯医疗保健中心在其伯克利县院区增建一座塔楼。预计医疗设施的扩张将增加对数位管理服务的需求,以追踪数据和整体工作场所管理,这反过来又将产生对託管数位工作场所服务的需求。

- 医疗机构需要各种职场管理服务,如废弃物管理、保全服务、餐饮服务、清洁服务、技术支援服务等,而且需求可能很快就会增加。单独管理这些服务很困难。工作场所管理服务提供的云端处理、行动性、实体和知识自动化等协作工具使得同时完成所有工作变得更加容易。快速扩张数位化趋势正在推动对託管数位工作场所服务的需求。

亚太地区将迎来显着成长

- 亚太地区最近经历了快速的技术进步和数位转型。这场数位革命正在大幅改变企业的业务方式,推动对高效、安全的数位化工作场所解决方案的需求。託管数位化工作场所服务对于企业提高生产力、协作能力和员工满意度至关重要。

- 亚太地区的政府和公共部门组织正在经历快速的数位转型,以满足改善公民服务、简化业务和提高效率的需求。许多政府机构正在转向託管数位工作场所服务 (MDWS) 作为实现这些目标的策略解决方案。此外,亚太地区的政府也越来越多地采用数位管道来提供高效率的、以公民为中心的服务。

- 此外,託管数位服务使政府能够创建一个职场环境,让员工能够无缝协作、存取相关资讯并快速回应公民的询问和服务请求。例如,新加坡的智慧国家计画专注于利用服务台透过 MyInfo 服务和 Moments of Life 应用程式等平台提供综合数位服务和个人化公民体验。

- 此外,亚太地区的託管数位工作场所服务 (MDWS) 市场正在经历强劲成长并具有巨大的潜力。随着数位化进程、远距办公采用和业务效率的提高,亚太地区的企业逐渐意识到 MDWS 解决方案的价值。市场对无缝远端协作、改善员工体验和强大资料安全的需求不断增长。

- 此外,随着政府和企业对数位转型计画的投资,MDWS 供应商拥有独特的机会提供满足亚太市场独特需求的客製化解决方案。随着新兴技术的整合和对创新的关注,亚太地区的 MDWS 市场预计将进一步扩大,并在塑造该地区未来工作和数位赋能方面发挥关键作用。

託管数位工作场所服务产业概览

总体而言,竞争对手之间的竞争强度很高,预计在预测期内将保持不变。 Atos Se、富士通有限公司、HCL 和凯捷等市场主要企业不断提供更多、更强大的服务。此外,企业纷纷采取强而有力的竞争策略来维持市场地位和留住客户,这导致竞争对手之间的敌意日益加剧。此外,供应商专注于提供整合服务,使他们能够为客户提供一体化託管数位工作场所服务。

2023 年 4 月,Stefanini 和菲利普莫里斯国际公司 (PMI) 宣布建立工作场所解决方案合作伙伴关係。 Stefanini 提供託管服务,例如服务台支援、服务管理、现场支援和 Workplace Core 服务,例如端点管理、ITAM、M365 等。菲利普莫里斯国际公司的约 79,800 名员工将在 80 个国家、140 个地点(包括办公室、工厂和零售店)获得服务,并使用 29 种语言。

2022 年 9 月,全球科技公司 HCL Technologies (HCL) 和英特尔推出了卓越中心,以加速开发和采用符合业界标准的数位化工作场所 (DWP) 产品。该卓越中心拥有创新技术和主题专家,将利用 HCL 的 DWP 解决方案和英特尔的技术组合共同创建解决方案,以实现无缝、互联和安全的混合工作场所。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 生态系分析

- COVID-19 市场影响

第五章市场动态

- 市场驱动因素

- 服务台采用先进的数位化,解决联络问题

- 作为数位转型倡议的一部分,数位解决方案的采用率不断提高

- 在家工作增多,多家公司考虑将在家工作作为永久选择

- 市场限制

- 网路犯罪的兴起

第六章市场区隔

- 按服务

- 服务台

- 最终用户设备支持

- 数位化工作场所

- 按行业

- BFSI

- 卫生保健

- 製造业

- 能源和公共产业

- 政府和公共机构

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章竞争格局

- 公司简介

- Atos SE

- Fujitsu Ltd

- HCL Technologies

- Capgemini Services SAS

- Tata Consultancy Services Limited

- Wipro Ltd

- IBM Corporation

- DXC Technology

- Cognizant Technology Solutions Corporation

- NTT Data Corporation

- Stefanini Group

第 8 章 供应商排名分析

第九章投资分析

第十章 市场机会与未来展望

The Managed Digital Workplace Services Market size is estimated at USD 56.18 billion in 2025, and is expected to reach USD 76.47 billion by 2030, at a CAGR of 6.36% during the forecast period (2025-2030).

The driving factors that can contribute to managed digital workplace services include technological advancements, changing workforce demographics, availability of new technologies and tools, employee demand for greater flexibility, and a positive company culture facilitated by strong and helpful management. Additionally, successful digital transformations are influenced by factors such as effective change management, employee engagement, and a clear understanding of the goals and objectives of the shift.

Key Highlights

- The rise in adopting digital workplaces by various organizations would drive the demand for managed digital workplace services over the forecasted period. For instance, According to a survey done by beautiful.ai in 2022, which polled 3,000 managers to find out how the digital workplace has affected their businesses and what the future holds for the remote worker, 78% agree that significant financial resources are being directed toward achieving a successful digital workplace, and 80% said their firm is committed to investing financial resources in technology and tools to assist managers in successfully leading and meeting goals in a digital workplace. 81% are optimistic about digital work replacing their in-office setting. In a digital working environment, 66% feel that there is still a strong sense of connection.

- Furthermore, information technology has significantly impacted managed digital workplace services. With the increasing use of digital platforms and automation, workplaces have become more efficient and streamlined. Cloud-based facilities management software, for example, has enabled business leaders to stay organized and up-to-date, resulting in improved business performance. Additionally, digital workplace technologies have focused on communication, information management, and cybersecurity, providing better workflows and data management.

- Furthermore, artificial intelligence is increasingly important in managing digital workplace operations. By automating tasks and providing intelligent insights, AI enables organizations to streamline workflows, increase productivity, and improve employee experience. Some examples of AI applications in the digital workplace include knowledge management, data governance, information management, end-user experience management, and document management. Additionally, AI can help organizations formulate effective workplace automation strategies and increase employee productivity. As AI technology continues to evolve, it is expected to play an even more significant role in shaping the future of the digital workplace.

- Further, the changing technology and customer experience landscape in the BFSI sector will drive the demand for managed digital workplace services over the forecast period. Many BFSI sector companies, such as Swiss Re, an insurance firm, have partnered with market vendors to enable a cloud-based digital workplace, and the trend is expected to strengthen in the coming years, with the demand expected to increase from the BFSI sector. Further, the growing digital transformation in banks and insurance firms worldwide necessitates the need for digital workplace transformation for enhanced efficiency and productivity, thus further providing growth prospects for the studied market.

- For the global market for managed digital workplace services, the rising incidences of cybercrime present significant challenges and constraints. Securing digital assets, defending against cyber threats, and adhering to data protection regulations are challenging for organizations. Strong security measures and proactive security management are crucial in delivering managed digital workplace services due to the impact of cybercrime on customer trust and the requirement for greater investments in cybersecurity.

- Post-pandemic, hybrid work, and on-site work are gaining traction. Organizations worldwide must adapt to this new normal in different physical workplace settings or improvements in the corporate digital workplace. This work shift is analyzed to influence the demand for managed digital workplace services to improve work practices to ensure that productivity, operations, and business success continue. Post-pandemic, various firms have collaborated to use the benefits of the digital workplace; such a rise in collaborations would push the growth of the studied market during the pandemic.

Managed Digital Workplace Services Market Trends

Healthcare Sector Expected to Witness Robust Growth

- Incorporating emerging technologies in the healthcare industry is prevailing, owing to enhanced patient treatment and experience and better workplace management. It has been understood that the healthcare industry presents various staffing complexities, including larger teams, a mix of part-time, full-time, on-call, seasonal, remote, and on-site workers, and workers of multiple roles and specializations. A great deal of coordination and specificity is involved in the industry, making deploying a management solution crucial.

- Moreover, the increasing need to reduce labor costs in hospitals and other health facilities, increased operational efficiency, and consolidation in the sector are some of the primary factors driving the adoption of these solutions. Further, the growing demand for healthcare professionals and benefits associated with workplace management solutions, such as transparency and flexible scheduling of workplaces in the industry, is also expected to increase the adoption of these solutions in the healthcare sector during the forecast period.

- Further, there is an increase in investment in the construction of healthcare facilities due to the increased need for healthcare services. This increase in the market for healthcare facilities is caused due to the rise in population and the growing aging population across various regions worldwide. This will likely expand the healthcare sector's adoption of managed digital workplace services. For instance, as per the survey by OECD and WHO, the number of hospitals worldwide is expected to rise steadily over the next five years. According to the data, the number of hospitals is expected to reach 1,66,235 in five years.

- Many healthcare providers are investing in expanding and constructing new healthcare facilities. For instance, in June 2022, the South Carolina Department of Health and Environmental Control approved Roper St. Francis Healthcare's Certificate of Need's additional tower on the hospital's Berkeley County campus. The expansion of healthcare facilities is anticipated to create augmented demand for digital management services to keep track of the data and overall workplace management, which in turn is projected to generate demand for managed digital workplace services.

- Healthcare establishments require various workplace management services, such as Waste Management, Security Services, Catering Services, Cleaning Services, Technical Support Services, and many more, whose demand will likely increase shortly. These services are difficult to manage individually. Collaboration tools such as cloud computing, mobility, and physical and knowledge automation provided by workplace management services make it easy to handle it all simultaneously. Rapid expansion and digitalization trends have crested demand for managed digital workplace services.

Asia-Pacific Expected to Witness Significant Growth

- The Asia-Pacific region has experienced rapid technological advancements and digital transformation recently. This digital revolution has significantly changed businesses' operations, increasing demand for efficient and secure digital workplace solutions. Managed Digital Workplace Services have emerged as a critical enabler for organizations to enhance productivity, collaboration, and employee satisfaction.

- The Government and Public sector in the Asia-Pacific region are experiencing rapid digital transformation driven by the need to enhance citizen services, streamline operations, and improve efficiency. Many government organizations are turning to Managed Digital Workplace Services (MDWS) as a strategic solution to achieve these goals. Furthermore, governments across the Asia-Pacific are increasingly adopting digital channels to provide efficient and citizen-centric services.

- Moreover, managed digital services enable governments to create work environments that empower employees to collaborate seamlessly, access relevant information, and promptly respond to citizen inquiries and service requests. For instance, Singapore's Smart Nation initiative focuses on leveraging service desks to provide integrated digital services and personalized citizen experiences through platforms like the MyInfo service and the Moments of Life app.

- Furthermore, the managed digital workplace services (MDWS) market in the Asia-Pacific region is experiencing robust growth and holds immense potential. With increasing digitalization efforts, remote work adoption, and the drive for operational efficiency, organizations across the region recognize the value of MDWS solutions. The market is fueled by the growing demand for seamless remote collaboration, enhanced employee experiences, and robust data security.

- Further, as governments and enterprises invest in digital transformation initiatives, MDWS providers have a unique opportunity to offer tailored solutions that cater to the specific needs of the Asia-Pacific market. With the convergence of emerging technologies and a focus on innovation, the MDWS market in the region is poised for further expansion, playing a vital role in shaping the future of work and digital empowerment in the Asia-Pacific.

Managed Digital Workplace Services Industry Overview

Overall, the intensity of competitive rivalry is high and expected to remain the same throughout the forecasted period. Major players in the market, such as Atos Se, Fujitsu Ltd, HCL, and Capgemini, are constantly providing increased and enhanced offerings. Additionally, companies are employing powerful competitive strategies to sustain themselves in the market and retain their clients, thereby intensifying competitive rivalry. Further, the vendors are focusing on offering integrated services to the client where all-in-one managed digital workplace service can be provided to the client.

In April 2023, Stefanini, with workplace solution collaboration, Stefanini and Phillip Morris International (PMI) announced a partnership. Stefanini will provide managed services such as service desk support, service management, onsite support, and workplace core services such as End Point Management, ITAM, and M365. Phillip Morris International's approximately 79,800 employees will be served in 29 languages throughout 80 countries and 140 sites, including offices, factories, and retail stores.

In September 2022, HCL Technologies (HCL), a global technology company, and Intel launched a Center of Excellence to foster the creation and adoption of industry-tailored Digital Workplace (DWP) offerings. Equipped with innovative technologies and experts, the Center of Excellence will leverage HCL's DWP solutions and Intel's technology portfolio to co-create solutions enabling seamless, connected, secure hybrid workplaces.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Ecosystem Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Higher Levels of Digitization in the Service Desk for Contact Resolution

- 5.1.2 Increase in Adoption of Digital Solutions as part of Digital Transformation Initiatives

- 5.1.3 Rise of Work from Home Employees with Several Companies Considering it as a Permanent Alternative

- 5.2 Market Restraints

- 5.2.1 Increasing Incidents of Cybercrime

6 MARKET SEGMENTATION

- 6.1 By Services

- 6.1.1 Service Desk

- 6.1.2 End-user Device Support

- 6.1.3 Digital Workplace

- 6.2 By End-user Vertical

- 6.2.1 BFSI

- 6.2.2 Healthcare

- 6.2.3 Manufacturing

- 6.2.4 Energy and Utility

- 6.2.5 Government and Public Sector

- 6.2.6 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Atos SE

- 7.1.2 Fujitsu Ltd

- 7.1.3 HCL Technologies

- 7.1.4 Capgemini Services SAS

- 7.1.5 Tata Consultancy Services Limited

- 7.1.6 Wipro Ltd

- 7.1.7 IBM Corporation

- 7.1.8 DXC Technology

- 7.1.9 Cognizant Technology Solutions Corporation

- 7.1.10 NTT Data Corporation

- 7.1.11 Stefanini Group

8 VENDOR RANKING ANALYSIS

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

数位化工作场所市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分

数位化工作场所市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分 全球数位化工作场所市场规模、份额、趋势和成长分析报告(2026-2034年)

全球数位化工作场所市场规模、份额、趋势和成长分析报告(2026-2034年) 数位化工作场所市场-全球产业规模、份额、趋势、机会及预测(按组件、部署方式、组织规模、最终用户产业、地区和竞争格局划分,2021-2031年)

数位化工作场所市场-全球产业规模、份额、趋势、机会及预测(按组件、部署方式、组织规模、最终用户产业、地区和竞争格局划分,2021-2031年) 数位化工作场所转型服务市场规模、份额和成长分析(按部署类型、组织规模、应用、产业垂直领域、服务类型和地区划分)-2026-2033年产业预测

数位化工作场所转型服务市场规模、份额和成长分析(按部署类型、组织规模、应用、产业垂直领域、服务类型和地区划分)-2026-2033年产业预测 数位化工作场所市场规模、份额和成长分析(按组件、产业、组织规模和地区划分)-2026-2033年产业预测

数位化工作场所市场规模、份额和成长分析(按组件、产业、组织规模和地区划分)-2026-2033年产业预测 数位化工作场所软体:全球市场份额和排名、总收入和需求预测(2025-2031 年)

数位化工作场所软体:全球市场份额和排名、总收入和需求预测(2025-2031 年) 数位工作场所市场:2025-2030 年全球预测(按产品、应用、产业、组织规模和部署类型)

数位工作场所市场:2025-2030 年全球预测(按产品、应用、产业、组织规模和部署类型) 全球数位化工作场所市场(按类型、部署模式、组织规模、行业垂直领域和地区划分)- 预测至 2030 年全球数位化工作场所转型服务市场规模(按组成部分、公司规模、最终用户、地区和预测):

全球数位化工作场所市场(按类型、部署模式、组织规模、行业垂直领域和地区划分)- 预测至 2030 年全球数位化工作场所转型服务市场规模(按组成部分、公司规模、最终用户、地区和预测): 数位化工作场所市场规模、份额和成长分析(按组件、部署、组织规模、垂直和地区)- 产业预测 2025-2032

数位化工作场所市场规模、份额和成长分析(按组件、部署、组织规模、垂直和地区)- 产业预测 2025-2032