|

市场调查报告书

商品编码

1693722

欧洲生物炭:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe Biochar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

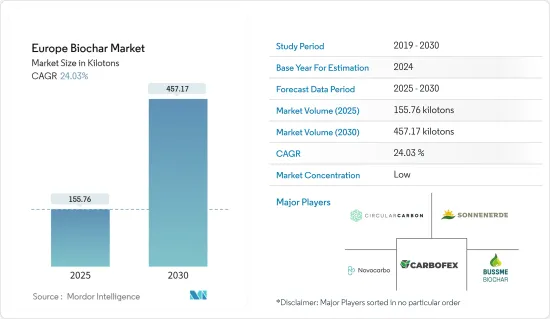

预计 2025 年欧洲生物炭市场规模为 155.76 千吨,2030 年将达到 457.17 千吨,预测期间(2025-2030 年)的复合年增长率为 24.03%。

在新冠疫情期间,门锁等限制措施扰乱了零售的业务,许多市场因担心病毒传播而关闭。然而,随着农业部门逐渐从疫情后復苏,预计未来几年欧洲生物炭市场将实现强劲成长率。

关键亮点

- 从长远来看,农业领域对有机农业的需求不断增长以及对废弃物管理行业的日益关注预计将成为市场的成长引擎。

- 另一方面,未经 EBC 认证的生物炭生产可能会阻碍市场成长。

- 另一方面,用于污水处理和建筑材料的生物炭的研究和开发可能会在预测期内为市场成长提供机会。

- 预计在预测期内,德国将主导欧洲生物炭市场,这得益于全国范围内多个正在进行的生物炭计划。

欧洲生物炭市场趋势

农业领域需求增加

- 生物炭是一种类似木炭的物质,透过受控的热解过程,燃烧废弃物的有机物(称为生物质)製成。使用生物炭作为土壤肥料可以改善土壤质量,提高其运输和循环养分的能力,从而实现长期的碳封存。

- 生物炭还可以修復受污染的土壤,同时带来环境效益。生物炭由于其多孔结构,堆积密度较低,比表面积较高(50-900 m2 g-1),保水能力强。

- 欧洲拥有庞大且不断发展的有机产业和成熟且竞争激烈的农业投入市场。有机食品消费量的增加为有机农业提供了潜在的成长机会。因此,许多符合自愿性欧洲生物炭认证(EBC)标准的新生产商正在进入市场。

- 强劲的市场成长令人鼓舞,但如果欧盟委员会 (2020) 要实现「从农场到餐桌」战略目标,即到 2030 年有机土地面积占比达到 25%,那么有机土地面积的扩张必须继续加速。欧洲消费者购买有机食品的常见原因包括支持当地企业、健康原因以及避免使用杀虫剂和其他喷雾剂。

- 有机农业在整个欧洲正在稳步增长。例如,作为农业重组的一部分,德国计划在2030年将三分之一的农场有机化。但随着通货膨胀的上升,农民呼吁政府提供更多支持。

- 同样,欧盟委员会发布的一份报告称,法国政府计划将在2023年至2027年期间将向有机农业转型的支持增加36%,平均每年达到3.4亿欧元(3.76亿美元)。目标是到2027年将有机农业的覆盖面积增加一倍,并实现联合农业用地(UAA)中18%的土地被有机农业覆盖的目标。

- 此外,根据义大利国家有机农业资讯系统(SINAB)的数据,到2022年,义大利将有约432,000公顷土地用于种植有机饲料,约428,000公顷土地将用于有机牧场和牧场。

- 因此,由于上述因素,预计预测期内有机农业对生物炭的需求将呈指数级增长。

预计德国将主导欧洲市场

- 德国是欧洲积极实施生物炭计划的国家之一。例如,在德国下奥德河谷国家公园的一个示范点,低营养湿地草透过热解和热液碳化(HTC)转化为生物炭。

- 生物炭对农业有显着的好处,因为它可以提高土壤肥力,促进碳固定,利用有机废弃物,提高微生物活性,并可能减少温室气体排放。

- 根据联邦农业资讯中心(BZL)的初步计算,2023年德国农作物产值将达到373亿欧元(405亿美元),年平均成长1.4%。

- 生物炭在德国畜牧业中也被广泛用作饲料。

- 根据德国饲料协会(DVT)预测,2023年德国饲料产量将达1,610万吨。根据德国联邦统计局(Statistisches Bundesamt)预测,2022年德国食品和饲料进口额将成长至646.4亿欧元(701.8亿美元),而2021年为627.9亿欧元(681.7亿美元)。

- 生物炭具有吸附污染物和改善水质的能力,与水净化有关。当添加到水处理系统中时,生物炭充当过滤介质,有效捕获重金属、有机污染物和营养物质等杂质。其多孔结构提供了较大的吸附表面积,使其成为一种有效且可持续的水净化方法。此应用对于解决水污染问题、改善水资源整体品质具有重要意义。

- 生物炭在水处理产业也有广泛的应用。德国的水处理业是欧洲最大的,并且持续大幅成长。该国拥有欧洲最大的工业污水处理(WTP)厂市场。

- 该地区约有3000家处理厂和12,000家排放企业。每年有超过9.2亿立方公尺的工业污水需要经过处理才能安全排放到环境中。

- 根据德国联邦统计局(Statistisches Bundesamt)的数据,2023年德国水收集、处理和供应产业收益价值114.1亿美元,预计2025年将达到117.3亿美元。

- 因此,上述因素显示欧洲生物炭的终端用户应用将成长,从而加强预测期内对生物炭的需求。

欧洲生物炭产业概况

欧洲生物炭市场较为分散,主要企业的市场占有率。市场的主要企业包括(不分先后顺序)Carbofex Ltd、Circular Carbon GmbH、Sonnenerde GmbH、Novocarbo GmbH 和 BussmeEnergy AB。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 农业领域对有机农业的需求不断增加

- 更关注废弃物管理领域

- 其他的

- 限制因素

- 非EBC认证的生物炭生产

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 技术部门

- 热解

- 气化系统

- 其他的

- 应用领域

- 农业

- 畜牧业

- 工业的

- 其他的

- 地区

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 其他欧洲国家

第六章竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- Bussme Energy AB

- Circular Carbon Gmbh

- Carbofex Ltd

- Carbon Centric

- Carbon Finland Oy

- Carbon Gold Ltd

- Carbuna

- Charline Gmbh

- Egos Gmbh

- Eoc Energy Ocean

- Lucrat Gmbh

- Nettenergy BV

- Novocarbo Gmbh

- Sonnenerde Gmbh

- Verora AG

第七章 市场机会与未来趋势

- 污水处理和建筑材料的潜在用途

The Europe Biochar Market size is estimated at 155.76 kilotons in 2025, and is expected to reach 457.17 kilotons by 2030, at a CAGR of 24.03% during the forecast period (2025-2030).

During the COVID-19 pandemic, the operations of retail sellers were disrupted due to the imposition of lockdowns and other restrictions, while many marketplaces were shut down due to fears of spreading the virus. However, the agricultural sector slowly recovered from the aftermath of the pandemic, with the European biochar market anticipated to register strong growth figures in the next several years.

Key Highlights

- In the long term, the increasing demand for organic farming in the agricultural industry and the rising focus on the waste management industry are expected to serve as the growth engines for the market studied.

- On the flip side, the market growth could be hindered by the production of non-EBC-certified biochar.

- Meanwhile, the potential research and development of biochar in wastewater treatment and as a construction material could present future opportunities for market growth during the forecast period.

- Germany is anticipated to dominate the European biochar market during the forecast period, supported by several ongoing biochar projects spread across the country.

Europe Biochar Market Trends

Increasing Demand from the Agricultural Industry

- Biochar is a charcoal-like substance created by burning organic material from agricultural and forest wastes (also known as biomass) in a controlled process known as pyrolysis. Using biochar as a fertilizer for the soil improves the soil's quality and nutrient-carrying and cycling ability, leading to long-term carbon sequestration.

- Biochar can also remediate contaminated soil while providing environmental benefits. Due to its porous structure, biochar includes a low bulk density that helps to achieve a high specific surface area ranging between 50 and 900 m2 g-1 and a high water-holding capacity.

- Europe includes a sophisticated and highly competitive agro-input market with a large and growing organic industry. The rising consumption of organic food presents potential growth opportunities for the organic farming industry. Therefore, many new producers are now entering the market, meeting the voluntary European Biochar Certificate (EBC) standard.

- While strong market growth is encouraging, organic farmland area must continue to expand faster to meet the European Commission's (2020) Farm to Fork strategy goal of 25% organic area share by 2030. Among European consumers, common reasons for buying organic food include supporting local businesses, health reasons, and not using pesticides or other sprays.

- The organic farming industry is witnessing steady growth across Europe. For instance, Germany is aiming to have a third of all farms organic by 2030 as part of an effort to restructure its agriculture. However, with rising inflation, farmers are asking for more government support.

- Similarly, according to a report published by the European Commission, in France, under the government program, 2023-2027 will see a 36% increase in support for conversion to organic farming, reaching an average of EUR 340 million (USD 376 million) per year. The objective is to double the area covered by organic farming and reach the 18% target of the union agricultural area (UAA) covered by organic farming by 2027.

- Furthermore, as per the SINAB (National Information System on Organic Agriculture), in 2022, approximately 432,000 hectares of Italian land were dedicated to the cultivation of organic forage, while roughly 428,000 hectares were allocated for organic meadows and pastures.

- Thus, owing to the factors above, the demand for biochar in organic farming is anticipated to rise exponentially during the forecast period.

Germany is Anticipated to Dominate the European Market

- Germany is among the top countries actively executing several biochar projects in Europe. For instance, in the German demo site at the Unteres Odertal National Park, low-nutritional grass from the wetlands is converted into biochar through pyrolysis or hydrothermal carbonization (HTC).

- Biochar significantly benefits the agriculture industry by enhancing soil fertility, promoting carbon sequestration, utilizing organic waste, improving microbial activity, and potentially reducing greenhouse gas emissions.

- According to preliminary calculations by the Federal Agricultural Information Center (BZL), German crop production was valued at EUR 37.3 billion (USD 40.5 billion) in 2023, up by 1.4% annually.

- Biochar is also widely used as animal feed in livestock farming in Germany.

- As per the German Feed Association (DVT), animal feed production in Germany reached 16.1 million tons in 2023. According to Statistisches Bundesamt (a federal authority of Germany), the Import value of food and animal feed to Germany was EUR 64.64 billion (USD 70.18 billion) in 2022 and registered growth when compared to EUR 62.79 billion (USD 68.17 billion) in 2021.

- Biochar is linked to water purification through its ability to adsorb contaminants and improve water quality. When added to water treatment systems, biochar acts as a filtration medium, effectively capturing impurities such as heavy metals, organic pollutants, and nutrients. Its porous structure provides a large surface area for adsorption, making it an effective and sustainable method for water purification. This application is valuable in addressing water pollution issues and enhancing the overall quality of water resources.

- Biochar is also being used more extensively in the water treatment industry. The German water treatment industry is the largest in Europe and continues to grow considerably. The country includes the largest market for industrial wastewater treatment (WTP) plants across Europe.

- There are around 3,000 treatment plants spread across the region, with around 12,000 discharging companies. Every year, more than 920 million cubic meters of industrial wastewater is treated before being safely discharged into the environment.

- According to the Statistisches Bundesamt, the industry revenue of water collection, treatment, and supply in Germany was valued at USD 11.41 billion in 2023 and is projected to reach USD 11.73 billion by 2025.

- Thus, the abovementioned factors indicate the growth of end-user applications of biochar in Europe, thereby strengthening demand for biochar during the forecast period.

Europe Biochar Industry Overview

The European biochar market is fragmented, with the top players accounting for a marginal market share. Some of the key companies in the market include (not in any particular order) Carbofex Ltd, Circular Carbon GmbH, Sonnenerde GmbH, Novocarbo GmbH, and BussmeEnergy AB.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Organic Farming in the Agricultural Industry

- 4.1.2 Increasing Focus on the Waste Management Sector

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 Non-EBC Certified Biochar Production

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Technology

- 5.1.1 Pyrolysis

- 5.1.2 Gasification Systems

- 5.1.3 Other Technologies

- 5.2 Application

- 5.2.1 Agriculture

- 5.2.2 Animal Farming

- 5.2.3 Industrial Uses

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Nordic

- 5.3.7 Turkey

- 5.3.8 Russia

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Bussme Energy AB

- 6.4.2 Circular Carbon Gmbh

- 6.4.3 Carbofex Ltd

- 6.4.4 Carbon Centric

- 6.4.5 Carbon Finland Oy

- 6.4.6 Carbon Gold Ltd

- 6.4.7 Carbuna

- 6.4.8 Charline Gmbh

- 6.4.9 Egos Gmbh

- 6.4.10 Eoc Energy Ocean

- 6.4.11 Lucrat Gmbh

- 6.4.12 Nettenergy BV

- 6.4.13 Novocarbo Gmbh

- 6.4.14 Sonnenerde Gmbh

- 6.4.15 Verora AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Potential Use in Wastewater Treatment and Construction Material

生物炭市场规模、份额和趋势分析报告:按技术、应用、地区和细分市场预测(2026-2033 年)

生物炭市场规模、份额和趋势分析报告:按技术、应用、地区和细分市场预测(2026-2033 年) 全球生物炭市场预测(2025-2030 年),按生产技术、原料类型、产品形态、应用和分销管道划分

全球生物炭市场预测(2025-2030 年),按生产技术、原料类型、产品形态、应用和分销管道划分 生物炭市场-全球产业规模、份额、趋势、机会及预测,依技术(热解、气化、其他)、应用(农业、工业、其他)、地区及竞争细分,2020-2030 年预测

生物炭市场-全球产业规模、份额、趋势、机会及预测,依技术(热解、气化、其他)、应用(农业、工业、其他)、地区及竞争细分,2020-2030 年预测 全球浓缩生物炭市场

全球浓缩生物炭市场 生物炭燃烧器市场按类型、技术和地区划分

生物炭燃烧器市场按类型、技术和地区划分 生物炭的全球市场2026-2036

生物炭的全球市场2026-2036 2032 年永续大麻生物炭市场预测:按产品类型、生产技术、应用、最终用户和地区进行的全球分析2032 年生物炭市场预测:按原料、通路、技术、应用和地区分類的全球分析北美生物炭市场规模、份额和趋势分析报告:按技术、应用、国家和细分市场划分,预测(2025-2033 年)

2032 年永续大麻生物炭市场预测:按产品类型、生产技术、应用、最终用户和地区进行的全球分析2032 年生物炭市场预测:按原料、通路、技术、应用和地区分類的全球分析北美生物炭市场规模、份额和趋势分析报告:按技术、应用、国家和细分市场划分,预测(2025-2033 年) 日本生物炭市场规模、份额、趋势及预测(按原料类型、技术类型、产品形态、应用和地区),2025 年至 2033 年

日本生物炭市场规模、份额、趋势及预测(按原料类型、技术类型、产品形态、应用和地区),2025 年至 2033 年