|

市场调查报告书

商品编码

1693761

中国农业生技药品:市场占有率分析、产业趋势与统计、成长预测(2025-2030年)China Agricultural Biologicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

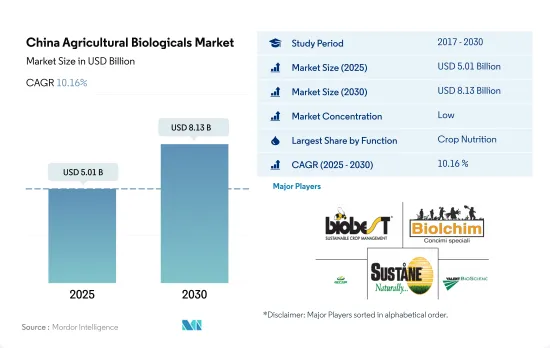

预计2025年中国农业生技药品市场规模将达50.1亿美元,2030年预计将达到81.3亿美元,预测期内(2025-2030年)的复合年增长率为10.16%。

- 2022年,作物营养投入品约占中国农业生技药品市场的87.1%。在作物营养领域,有机肥料是全国消耗最多的生物投入品。有机肥料的优越性主要归功于其在有机农业和传统农业中的广泛应用。

- 堆肥在该国的有机肥料市场中占据主导地位,预计 2022 年市场价值将达到 14.2 亿美元。堆肥传统上用作有机和非有机农业的基础肥料,并且可以增加土壤中的有机质和碳含量。堆肥类别之后是其他有机肥料类别,包括鱼粪、蝙蝠粪、鱼乳剂、蚯蚓堆肥、糖蜜和其他堆肥等肥料。 2022 年其他有机肥料部门的价值约为 8.322 亿美元。

- 2022 年,作物剂占据作物保护领域的主导地位,占有 52.8% 的份额。大型生物防治剂将主导中国的生物防治剂市场,预计 2022 年市场规模约 2.792 亿美元。大型生物防治剂的主导地位主要归因于其能够控制多种害虫。

- 捕食性害虫在中国生物防治剂市场中占据大型生物製剂领域的主导地位,主要是因为它们能够攻击不同生命阶段的害虫,甚至攻击不同种类的害虫。它们也比其他生物防治剂更贪婪。 2022 年,捕食者子区隔约占中国生物防治剂市场大型生物细分市场的 47.4%。

中国农业生物防治剂市场趋势

农药使用零成长和有机产品出口增加促进有机农业

- 根据FiBL和IFOAM的最新报告,中国有机食品市场正以每年25.0%的速度成长。鑑于中国每年出口29.1亿美元的农产品,从传统农业向有机农业的转变意味着中国转向更永续的食品体系的转变。

- 随着收入的增加和食品安全日益重要,越来越多的人开始购买有机产品,中国的有机农场面积迅速成长。过去三年,中国有机种植面积增加了10%,2020年达到240万公顷。此外,国家推出了推动有机生产的政策,并提出了「绿水青山就是金山银山」和「绿色发展」的口号。

- 中国的有机农业主要以出口为导向。出口和进口商品包括谷物、大豆、水果和蔬菜。中国东北三省(辽宁、吉林、黑龙江)是全国有机农产品生产总量、数量、面积最大的省区。中国北方(如山东省和辽宁省)的大多数有机农场都向周边城市供应有机蔬菜和水果。另外部分产品也出口到日本、韩国、欧美等美国。

- 由于过度使用合成肥料和杀虫剂导致土壤污染,人们越来越担心土壤毒性,中国对永续农业实践和有机食品生产的需求正在增长。农业实践的这种变化是一个缓慢但不断增长的趋势,并且它正在增加对作物营养和保护产品的需求。

由于对有机产品的需求不断增长,约73%的中国消费者希望购买有机食品。

- 中国有机食品市场发展迅速,中国消费者对有机食品的潜在需求庞大。更富裕的中阶的崛起和对健康影响的认识不断提高是这一现象背后的驱动力。 2021年,中国有机食品销售额约达775.4亿美元。

- 由于政府的各项法律都倾向于有机食品而非食品安全,且消费者偏好有机食品而非传统食品,因此对有机食品的需求大幅增加。中国的有机蔬菜价格是传统蔬菜的3至15倍,而有机蔬菜的价格一般是传统蔬菜的5至10倍。然而,儘管价格因素是一个障碍,富裕家庭和有健康问题的个人仍愿意扩大预算,约 73% 的中国消费者愿意为有机食品支付额外费用。

- 中国政府正逐步实现有机食品领域的自给自足。例如,透过鼓励农民减少使用化学肥料并改用生物替代品,经济正逐步转向绿色农业实践。中国连锁专利权协会2020年的调查显示,中国已开发城市民众了解永续食品生产概念的有机意识已达83%。儘管中国的有机食品产业仍规模较小,远未满足国内外消费者的需求,但考虑到2021年国内销售额预计将成长4.01%,可以说中国有机食品在国内外市场都具有巨大的潜力。

中国农业生技药品产业概况

中国农业生技药品市场细分化,前五大企业市占率合计为1.05%。市场的主要企业包括 Biobest Group NV、Biolchim SPA、Genliduo Bio-tech Corporation Ltd、Sustane Natural Fertilizer Inc.、Valent Biosciences LLC 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 有机种植区

- 有机产品人均支出

- 法律规范

- 中国

- 价值炼和通路分析

第五章市场区隔

- 功能

- 作物营养

- 生物肥料

- 固氮螺菌

- 固氮菌

- 菌根真菌

- 解磷细菌

- 根瘤菌

- 其他生物肥料

- 生物肥料

- 胺基酸

- 富里酸

- 腐植酸

- 蛋白质水解物

- 海藻萃取物

- 其他生物刺激素

- 有机肥

- 肥料

- 餐食基肥料

- 油饼

- 其他有机肥料

- 作物保护

- 生物防治剂

- 大型微生物

- 微生物

- 生物防治剂

- 生物真菌剂

- 生物除草剂

- 生物杀虫剂

- 其他生物防治剂

- 作物营养

- 作物类型

- 经济作物

- 园艺作物

- 耕地作物

第六章 竞争格局

- 重大策略倡议

- 市场占有率分析

- 商业状况

- 公司简介

- Biobest Group NV

- Biolchim SPA

- Genliduo Bio-tech Corporation Ltd

- Haifa Group

- Henan Jiyuan Baiyun Industry Co. Ltd

- Novozymes

- Shandong Sukahan Bio-Technology Co. Ltd

- Sustane Natural Fertilizer Inc.

- Trade Corporation International

- Valent Biosciences LLC

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

The China Agricultural Biologicals Market size is estimated at 5.01 billion USD in 2025, and is expected to reach 8.13 billion USD by 2030, growing at a CAGR of 10.16% during the forecast period (2025-2030).

- Crop nutrition inputs accounted for about 87.1% of the Chinese agricultural biologicals market in 2022. In the crop nutrition segment, organic fertilizers are the most consumed biological inputs in the country. The dominance of organic fertilizers is mainly due to their application in bulk quantities both in organic and conventional farming.

- Manure dominates the country's organic fertilizers market, valued at USD 1.42 billion in 2022. Manure is conventionally used as a primary fertilizer both in organic and non-organic cultivation and is known to increase organic matter and carbon content in the soil, which would increase the nutrient uptake of the crop and, thus, the grain yield. The manure segment is followed by the other organic fertilizers segment, which includes fertilizers like fish guano, bat guano, fish emulsion, vermicompost, molasses, and other composted fertilizers. The other organic fertilizers segment was valued at about USD 832.2 million in 2022.

- Biocontrol agents dominated the crop protection segment, with a share of 52.8% in 2022. Macrobial biocontrol agents dominated the Chinese biocontrol agents market, valued at about USD 279.2 million in 2022. The domination of macrobial biocontrol agents is mainly due to their ability to control various pests.

- Predators dominate the macrobials segment of the Chinese biocontrol agents market mainly due to their ability to attack different life stages of pests and even different pest species. They are also voracious feeders compared to other biocontrol agents. The predators sub-segment accounted for about 47.4% of the macrobials segment of the Chinese biocontrol agents market in 2022.

China Agricultural Biologicals Market Trends

Country's zero growth in pesticides use and increasing exports under organic products driving the organic cultivation.

- According to the latest reports by FiBL and the IFOAM, the market for organic food in China is growing at an annual rate of 25.0%. The shift from conventional to organic is a transformation toward a more sustainable food system within China, given the USD 2.91 billion of agri-food commodities exported from China each year.

- The size of organic farmland increased rapidly in China because more people started buying organic products due to increased incomes and the increasing importance of food safety. In the last three years, China's organic planting area increased by 10%, reaching 2.4 million ha in 2020. In addition, national policies have been adopted to promote organic production, advocating the slogans that state, "lucid waters and lush mountains are invaluable assets" and "green development".

- Organic farming in China is majorly export-oriented. The products that are both exported and imported include cereals, soybeans, fruits, and vegetables. China's three northeastern provinces (Liaoning, Jilin, and Heilongjiang) support the largest organic production nationally in terms of output, volume, and area. Most organic farms located in the northern part of China (e.g., Shandong and Liaoning) supply organic vegetables and fruits to nearby cities. In addition, they export some products to Japan, South Korea, Europe, and the United States.

- With the increasing concerns of soil toxicity due to the overuse of synthetic fertilizers and pesticides that lead to soil contamination, the demand for sustainable agriculture practices and organic food production is on the rise in China. This moderately slow yet increasing shift in cultivation practices has also subsequently increased the demand for crop nutrition and protection products.

The growing demand for organic products, approximately 73% of Chinese consumers are willing to have organic food

- China's organic food market is developing rapidly, and the potential demand for organic food among Chinese consumers is enormous. This is due to the growth of the wealthier middle classes and a greater awareness of the health implications. In 2021, organic food sales in China amounted to about USD 77.54 billion.

- Due to various government laws that favor organic food over food safety and customer preferences for organic food over conventional food, the demand for organic food items has considerably expanded. While prices of organic vegetables in China range from 3 to 15 times the cost of conventional produce, prices for organic vegetables are generally between 5 and 10 times that of their conventional counterparts. However, despite the price factor being a barrier, wealthy families and individuals with health problems are eager to increase their budget, with approximately 73% of Chinese consumers willing to pay extra for organic foods.

- The Chinese government is slowly aiming to become self-reliant in the organic food sector. For instance, the economy is slowly moving toward a green agriculture practice by encouraging farmers to scale back the use of chemical fertilizers and switch to bio-based alternatives. The China Chain Store and Franchise Association (CCFA) research in 2020 declared that organic awareness among the Chinese population in developed cities was at 83% when it came to an understanding of the concept of sustainable food production. Although China's organic food sector is still quite small and falls far short of satisfying domestic and international consumer demand, it can be stated that organic food in China has enormous potential in both the domestic and foreign markets, considering the rise in domestic sales by 4.01% in 2021.

China Agricultural Biologicals Industry Overview

The China Agricultural Biologicals Market is fragmented, with the top five companies occupying 1.05%. The major players in this market are Biobest Group NV, Biolchim SPA, Genliduo Bio-tech Corporation Ltd, Sustane Natural Fertilizer Inc. and Valent Biosciences LLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Crop Nutrition

- 5.1.1.1 Biofertilizer

- 5.1.1.1.1 Azospirillum

- 5.1.1.1.2 Azotobacter

- 5.1.1.1.3 Mycorrhiza

- 5.1.1.1.4 Phosphate Solubilizing Bacteria

- 5.1.1.1.5 Rhizobium

- 5.1.1.1.6 Other Biofertilizers

- 5.1.1.2 Biostimulants

- 5.1.1.2.1 Amino Acids

- 5.1.1.2.2 Fulvic Acid

- 5.1.1.2.3 Humic Acid

- 5.1.1.2.4 Protein Hydrolysates

- 5.1.1.2.5 Seaweed Extracts

- 5.1.1.2.6 Other Biostimulants

- 5.1.1.3 Organic Fertilizer

- 5.1.1.3.1 Manure

- 5.1.1.3.2 Meal Based Fertilizers

- 5.1.1.3.3 Oilcakes

- 5.1.1.3.4 Other Organic Fertilizers

- 5.1.2 Crop Protection

- 5.1.2.1 Biocontrol Agents

- 5.1.2.1.1 Macrobials

- 5.1.2.1.2 Microbials

- 5.1.2.2 Biopesticides

- 5.1.2.2.1 Biofungicides

- 5.1.2.2.2 Bioherbicides

- 5.1.2.2.3 Bioinsecticides

- 5.1.2.2.4 Other Biopesticides

- 5.1.1 Crop Nutrition

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Biobest Group NV

- 6.4.2 Biolchim SPA

- 6.4.3 Genliduo Bio-tech Corporation Ltd

- 6.4.4 Haifa Group

- 6.4.5 Henan Jiyuan Baiyun Industry Co. Ltd

- 6.4.6 Novozymes

- 6.4.7 Shandong Sukahan Bio-Technology Co. Ltd

- 6.4.8 Sustane Natural Fertilizer Inc.

- 6.4.9 Trade Corporation International

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

动物微生物组市场规模、份额和增长分析:按动物种类、产品类型、原材料、形态、应用、最终用户、通路和地区划分——2026-2033年行业预测

动物微生物组市场规模、份额和增长分析:按动物种类、产品类型、原材料、形态、应用、最终用户、通路和地区划分——2026-2033年行业预测 农业生物製品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

农业生物製品:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球农业生技药品市场规模、份额、趋势和成长分析报告(2026-2034年)

全球农业生技药品市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球农业生技药品市场报告

2026年全球农业生技药品市场报告 生物合理作物保护市场依产品类型、作物类型、配方、作用机制、成分及应用方法划分-2026-2032年全球预测

生物合理作物保护市场依产品类型、作物类型、配方、作用机制、成分及应用方法划分-2026-2032年全球预测 农业生技药品市场规模、份额和趋势分析报告:按作物类型、产品类型、应用方法、地区和细分市场预测(2026-2033 年)

农业生技药品市场规模、份额和趋势分析报告:按作物类型、产品类型、应用方法、地区和细分市场预测(2026-2033 年) 日本农业生物製品市场报告(按类型、来源、应用方式、应用领域和地区划分,2026-2034年)

日本农业生物製品市场报告(按类型、来源、应用方式、应用领域和地区划分,2026-2034年) 农业生技药品市场规模、份额和成长分析(按类型、来源、应用、作物类型和地区划分)-2026-2033年产业预测

农业生技药品市场规模、份额和成长分析(按类型、来源、应用、作物类型和地区划分)-2026-2033年产业预测 农业生技药品市场规模、份额和成长分析(按类型、来源、应用、作物类型和地区划分)-2026-2033年产业预测农业生技药品市场-2025-2030年预测

农业生技药品市场规模、份额和成长分析(按类型、来源、应用、作物类型和地区划分)-2026-2033年产业预测农业生技药品市场-2025-2030年预测