|

市场调查报告书

商品编码

1693765

印度有机肥料:市场占有率分析、产业趋势与统计、成长预测(2025-2030)India Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

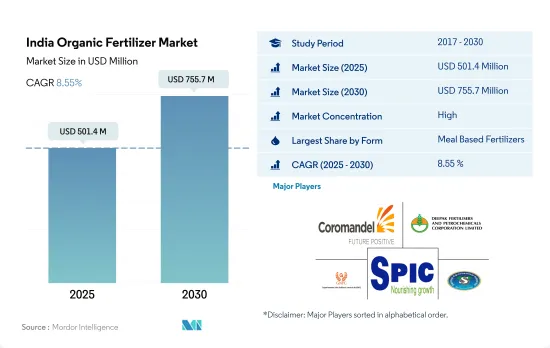

印度有机肥料市场规模预计在 2025 年为 5.014 亿美元,预计到 2030 年将达到 7.557 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.55%。

- 有机肥料含有大量的有机质,能增加土壤的生物活性,维持并增强土壤生物多样性。 2022 年,有机肥料占印度作物营养总量的 69.9%,因为它们广泛应用于有机和传统农业实践。

- 餐食基肥料是评价最高的有机肥料,占 2022 年有机肥料市场的 67.5%。然而,肉粉市场,尤其是牛肉粉,在印度尚未得到广泛认可,而且该国许多地区的骨粉产量有限。

- 肥料是印度消耗量最大的有机肥料,其供应量占了最大的市场占有率。它适用于几乎所有作物,无论作物品种。农民通常可以透过适当使用堆肥作为肥料来节省资金。预计 2023 年至 2029 年期间该细分市场的复合年增长率为 4.8%。

- 有机肥料消费以连续作物为主,占2022年市场规模的约85.0%。连续作物的主导地位主要是因为其在该国的种植面积很大,2022年约占有机作物总面积的59.8%。

- 国内外市场对有机产品的需求很高,过度使用化学肥料是该国面临的主要挑战之一。印度政府透过提供有机肥料奖励等各种计划和方案来推广永续有机农业实践,预计将在 2023 年至 2029 年期间推动市场发展。

印度有机肥料市场趋势

由于有机生产者的增加,有机种植面积增加,主要用于连续作物。

- 印度是世界上经过认证的有机生产者总数最多的国家,2019 年拥有 130 万名有机生产者。儘管有机生产者数量众多,但该国的有机种植面积约占该国农业总面积的 2.0%。 2021年全国有机种植面积为711,094.0公顷,较2017年成长约3.4%。

- 该国的有机农业集中在几个州。全国排名前 10 名的有机作物州约占有机作物总面积的 80.0%。一些州在扩大有机农业应用方面处于领先地位。中央邦、拉贾斯坦邦和马哈拉斯特拉邦是有机农业发展最好的三个邦。 2019 年,中央邦约占印度有机种植总面积的 27.0%。

- 该国以连续作物的有机种植为主。 2021年,行作物约占有机种植作物总面积的59.7%。该国以谷类作物生产为主,作物谷类稻米、小麦、小米和玉米。大多数谷类都是在喀里夫季节(六月至九月)种植的。这段时期种植的作物主要依赖雨水或需要更多的水,例如水稻、玉米、棉花和大豆。

- 有机经济作物的整体种植面积呈上升趋势,从2017年的27万公顷增加到2021年的28万公顷。该国生产的主要经济作物包括棉花、甘蔗、茶叶和香辛料。目前,该国有机园艺作物的生长有限。由于对有机产品的需求不断增加以及印度政府大力推行有机农业,预计 2023-2029 年期间有机作物种植面积将会增加。

不断增长的需求和透过电子商务管道随时可用将推动人均有机食品支出的成长

- 印度人均有机产品支出为0.23美元,与亚太地区人均有机产品支出平均值相比相对较低。然而,近年来,消费者需求日益转向有机产品。因为有机产品免疫力更强,品质更高,而且更容易透过电商管道买到。印度是有机食品和饮料的一个有前景的市场。预计到 2024 年,印度有机食品和饮料产业的价值将达到 1.38 亿美元,2019 年至 2024 年期间的复合年增长率为 13%。

- 2022年,该国消费了价值1.08亿美元的有机食品和饮料。该国有机产品消费额从 2016 年的 4,500 万美元成长至 2021 年的 9,600 万美元。有机食品销售额的成长主要得益于消费者意识的提高,高所得消费者推动了有机食品和饮料的消费。需求最高的类别包括有机鸡蛋、乳製品、水果和蔬菜等必需食品。

- 有机饮料消费占据市场主导地位,占 2022 年有机食品和饮料总合市值的约 85.2%。有机饮料部分包括经核准认证机构认证的有机包装食品和饮料产品。 2020-2022年期间,有机饮料消费量复合年增长率为14%。有机产品的价格溢价限制了低收入消费者的购买,是有机食品消费的主要限制因素。然而,积极的促销和有机产品的优势预计将在预测期内推动有机食品市场的发展。

印度有机肥料产业概况

印度有机肥料市场相当集中,前五大公司占72.35%的市占率。市场的主要企业有 Coromandel International Ltd、Deepak Fertilisers & Petrochemicals Corp. Ltd、Gujarat Narmada Valley Fertilizers & Chemicals Ltd、Southern Petrochemical Industries Corp. Ltd、Swaroop Agrochemical Industries 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 有机种植区

- 有机产品人均支出

- 法律规范

- 印度

- 价值炼和通路分析

第五章市场区隔

- 形式

- 肥料

- 餐食基肥料

- 油饼

- 其他有机肥料

- 作物类型

- 经济作物

- 园艺作物

- 田间作物

第六章竞争格局

- 重大策略倡议

- 市场占有率分析

- 商业状况

- 公司简介

- Amruth Organic Fertilizers

- Coromandel International Ltd

- Deepak Fertilisers & Petrochemicals Corp. Ltd

- GrowTech Agri Science Private Limited

- Gujarat Narmada Valley Fertilizers & Chemicals Ltd

- Gujarat State Fertilizers & Chemicals Ltd

- Prabhat Fertilizer And Chemical Works

- Southern Petrochemical Industries Corp. Ltd

- Swaroop Agrochemical Industries

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

The India Organic Fertilizer Market size is estimated at 501.4 million USD in 2025, and is expected to reach 755.7 million USD by 2030, growing at a CAGR of 8.55% during the forecast period (2025-2030).

- Organic fertilizers contain organic matter in large quantities, which boosts biological activities in soil and aids in maintaining and enhancing soil biodiversity. Organic fertilizers accounted for 69.9% of the total Indian crop nutrition segment in 2022, owing to their widespread use in organic and conventional farming.

- Meal-based fertilizers constituted the most valued organic fertilizer, accounting for 67.5% of the organic fertilizer market in 2022. However, the meat meal market, especially cattle meat-based meals, is not well accepted in India, and the production of bone meals is limited in many parts of India.

- Manures constitute the most consumed organic fertilizer in India, with the largest market share attributed to their easy availability. They are applied to almost all crops, regardless of crop variety. Farmers can often save money by properly using manure as a fertilizer. The segment's volume is projected to grow, with an estimated CAGR of 4.8% between 2023 and 2029.

- The consumption of organic fertilizers is dominant in row crops and accounted for about 85.0% of the market volume in 2022. The dominance of row crops is mainly due to their large cultivation area in the country, which accounted for approximately 59.8% of the total organic crop area in 2022.

- There is a high demand for organic products in domestic and international markets, and the overuse of chemical fertilizers is one of the major challenges in the country. The Indian government's promotion of sustainable or organic cultivation practices through various schemes or programs by providing incentives for organic fertilizers is expected to drive the market between 2023 and 2029.

India Organic Fertilizer Market Trends

Growing number of organic producers helping the increase in area under organic cultivation, primarily in row crops

- India is the largest country, in terms of the total number of certified organic producers in the world, with 1.3 million organic producers in 2019. Despite a large number of organic producers, organic cultivation areas in the country account for around 2.0% of the total agriculture area in the country. In 2021, the organic area in the country was 711,094.0 ha, which increased by about 3.4% compared to 2017.

- Organic farming in the country is concentrated in only a few states. The top ten organic farming states in the country account for about 80.0% of the total organic crop area. A few states have taken the lead in improving organic farming coverage. Madhya Pradesh, Rajasthan, and Maharashtra are the top three organic farming states in the country. Madhya Pradesh accounted for about 27.0% of India's total organic cultivation area in 2019.

- Organic cultivation of row crops is dominant in the country. Row crops accounted for about 59.7% of the total organic crop area in 2021. Cereal crop production dominates in the country, with rice, wheat, millet, and maize being the major cereals produced. Most cereal crops are grown in the Kharif season (June-September). The crops grown in this season mainly depend on rain or require more water, like rice, maize, cotton, soybean, etc.

- There has been an increasing trend in the overall organic cash crop cultivation area, from 270,000 ha in 2017 to 280,000 ha in 2021. The major cash crops produced in the country include cotton, sugarcane, tea, and spices. Currently, there is limited growth of organic horticultural crops in the country. The increasing demand for organic products and initiatives by the Indian government to go organic are anticipated to increase the organic crop area between 2023 and 2029.

Growing demand and their easy accessibility through e-commerce channels, rising the per capita spending on organic food

- India's per capita spending on organic products is relatively low at USD 0.23 compared to the average per capita spending on organic products of the Asia-Pacific region. However, in recent years, consumer demand has been increasingly shifting toward organic products as these items offer better immunity, higher quality, and more accessibility through e-commerce channels. India is a promising, developing market for organic foods and beverages. India's domestic organic food and beverage industry is expected to be worth USD 138.0 million by 2024, a CAGR of 13% between 2019 to 2024.

- In 2022, organic food and beverages worth USD 108.0 million were consumed in the country. The consumption value of organic products in the country increased from USD 45.0 million in 2016 to USD 96.0 million in 2021. Organic food sales increased mainly due to increasing consumer awareness, and high-income consumers are propelling organic food and beverage consumption. Categories that experienced the most demand included essential foods such as organic eggs, dairy, and fruits and vegetables.

- The consumption of organic beverages dominated the market and accounted for about 85.2% of the total combined organic food and beverages market value in 2022. The organic beverages segment includes organic packaged food and beverages that are certified by the approved certification body. The consumption value of organic beverages registered growth with a CAGR of 14% between 2020 to 2022. The price premium associated with organic products hampers lower-income consumer access and is the major limiting factor for organic food consumption. However, the active promotion and advantages of organic products are expected to drive the organic food market in the forecast period.

India Organic Fertilizer Industry Overview

The India Organic Fertilizer Market is fairly consolidated, with the top five companies occupying 72.35%. The major players in this market are Coromandel International Ltd, Deepak Fertilisers & Petrochemicals Corp. Ltd, Gujarat Narmada Valley Fertilizers & Chemicals Ltd, Southern Petrochemical Industries Corp. Ltd and Swaroop Agrochemical Industries (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Manure

- 5.1.2 Meal Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizers

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Amruth Organic Fertilizers

- 6.4.2 Coromandel International Ltd

- 6.4.3 Deepak Fertilisers & Petrochemicals Corp. Ltd

- 6.4.4 GrowTech Agri Science Private Limited

- 6.4.5 Gujarat Narmada Valley Fertilizers & Chemicals Ltd

- 6.4.6 Gujarat State Fertilizers & Chemicals Ltd

- 6.4.7 Prabhat Fertilizer And Chemical Works

- 6.4.8 Southern Petrochemical Industries Corp. Ltd

- 6.4.9 Swaroop Agrochemical Industries

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

全球有机肥市场:预测(至2032年)-按来源、形态、营养成分、作物类型、施用方法、最终用户和地区进行分析

全球有机肥市场:预测(至2032年)-按来源、形态、营养成分、作物类型、施用方法、最终用户和地区进行分析 有机农药市场依产品类型、作物类型、配方、施用方法及通路划分-2025-2032年全球预测有机肥料市场(按最终用户、销售管道、配方、产品形式、供应来源和应用划分)—2025-2032 年全球预测

有机农药市场依产品类型、作物类型、配方、施用方法及通路划分-2025-2032年全球预测有机肥料市场(按最终用户、销售管道、配方、产品形式、供应来源和应用划分)—2025-2032 年全球预测 2025年全球有机肥料市场报告全球绿肥市场报告(2025年)植物性有机肥市场(依产品类型、作物类型、施用方式、包装类型及通路划分)-2025-2030 年全球预测

2025年全球有机肥料市场报告全球绿肥市场报告(2025年)植物性有机肥市场(依产品类型、作物类型、施用方式、包装类型及通路划分)-2025-2030 年全球预测 有机肥市场-全球产业规模、份额、趋势、机会及预测(按来源、作物类型、形态、地区和竞争情况划分,2020-2030 年)

有机肥市场-全球产业规模、份额、趋势、机会及预测(按来源、作物类型、形态、地区和竞争情况划分,2020-2030 年) 有机肥市场规模、份额、成长分析(按来源、按作物类型、按形态、按应用类型、按地区)- 产业预测,2025-2032

有机肥市场规模、份额、成长分析(按来源、按作物类型、按形态、按应用类型、按地区)- 产业预测,2025-2032 全球有机肥料市场:产业分析、规模、份额、成长、趋势与预测(2025-2032)

全球有机肥料市场:产业分析、规模、份额、成长、趋势与预测(2025-2032) 有机肥市场规模、份额、趋势分析报告(按来源、形态、作物类型、地区、细分市场预测,2025-2030 年)

有机肥市场规模、份额、趋势分析报告(按来源、形态、作物类型、地区、细分市场预测,2025-2030 年)