|

市场调查报告书

商品编码

1693816

电力设备-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Power Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

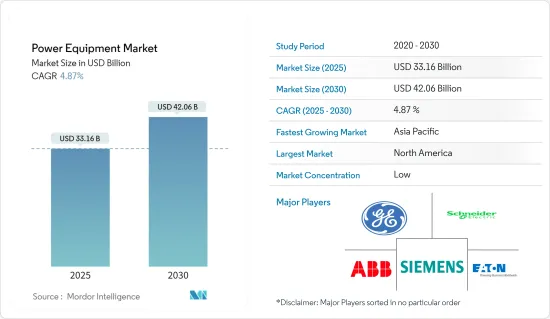

预计 2025 年电力设备市场规模为 331.6 亿美元,到 2030 年将达到 420.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.87%。

2020年新冠疫情对市场产生了负面影响,目前市场已恢復到疫情前的水准。

关键亮点

- 从中期来看,由于人口成长和基础设施发展,预计能源需求将增加,这将导致预测期内对电力设备的需求增加。

- 另一方面,高昂的营运和维护成本预计会阻碍市场成长。

- 加大对可再生能源和智慧电网基础设施开发的技术投资预计将为电力设备市场创造重大机会。

电力设备市场趋势

预计发电将主导市场

- 由于人口成长、都市化和工业化,全球对电力的需求正在增加。因此,发电设施在满足日益增长的需求和确保稳定的电力供应方面发挥着至关重要的作用。

- 此外,人们对太阳能、风能、水力发电和地热发电等可再生能源发电的日益关注也增强了发电设备的优势。向更清洁、更永续的能源过渡需要专门的发电设备,如太阳能板、风力发电机和水力发电机。

- 例如,2022 年 6 月,Vestas AS 获得一份合同,为 EnBW 的 900 MW He Dreiht离岸风力发电计划供应 64 台 V235-15.0 MW风力发电机。维斯塔斯还与卡德勒签署了涡轮机运输和安装合同,计划于 2025 年第二季度开始。

- 世界各国政府也正在实施政策、奖励和可再生能源发电目标,进一步刺激了对发电设备的需求,尤其是在可再生能源领域。

- 因此,全球可再生能源的装置容量正在增加。根据国际可再生能源机构的预测,2022年全球可再生能源装置容量将达到3,371.8吉瓦,而2021年为3,077.23吉瓦,2021年至2022年的成长率将超过9.5%。

- 因此,由于能源需求的增加、对可再生能源的关注、政府措施和发电,发电已成为电力设备市场的主导部分。

亚太地区成长强劲

- 亚太地区拥有世界相当一部分人口和许多世界最大城市。未来几年,随着数百万新用户用电范围扩大,该地区的电力需求预计将激增。需求激增是由于人口快速成长和工业化程度不断提高所致。

- 预计亚太地区将在不久的将来成为电力设备的主要市场。关键驱动因素是再生能源来源的使用增加、电力消耗增加、电力供应增加以及电网基础设施的持续改善。预计中国、印度、日本和澳洲等主要国家将在塑造该地区的电力设备市场方面发挥关键作用。

- 根据英国石油公司《世界能源统计评论》的数据,2021 年该地区的发电量为 13,994.4 TWh,比 2020 年增长 8.4%,比 2011 年至 2021 年间增长 4.7%。

- 此外,该地区的政府透过实施有利于发电和配电基础设施的政策、措施和投资发挥关键作用。这些为确保能源安全、推广可再生能源和改善电力供应所做的努力进一步推动了亚太地区对电力设备的需求。

- 例如,中国政府宣布了雄心勃勃的计划,将于2022年在戈壁沙漠建造450吉瓦的太阳能和风能发电厂。该计划旨在推动中国在2030年实现其可再生能源目标。

- 这些进步实现了高效和永续的电力管理,巩固了该地区在电力设备市场中的地位。

- 由于经济快速成长、都市化、政府措施、可再生能源的采用、基础设施发展、工业需求和技术进步,亚太地区可望主导电力设备市场。

电力设备产业概况

全球电力设备市场正走向半固体化。该市场的主要企业(不分先后顺序)包括通用电气公司、施耐德电气公司、ABB、伊顿公司和西门子。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章执行摘要

第三章调查方法

第四章 市场概述

- 介绍

- 至2028年的市场规模及需求预测(单位:美元)

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 人口成长和基础设施发展

- 限制因素

- 运作维护成本高

- 驱动程式

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁产品/服务

- 竞争对手之间的竞争

第五章市场区隔

- 设备类型

- 发电机

- 变形金刚

- 开关设备

- 电路断流器

- 电源线

- 其他设备

- 发电源

- 石化燃料为基础

- 太阳热

- 风

- 核能

- 水力发电

- 最终用户

- 住宅

- 工商

- 公共产业

- 应用

- 发电

- 动力传输

- 配电

- 2028 年前的地区、市场规模和需求预测(按地区)

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 澳洲

- 日本

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 北美洲

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- General Electric Company

- Siemens AG

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Toshiba Corporation

- Honeywell International Inc.

- Bharat Heavy Electricals Limited

- Crompton Greaves Ltd.

- Larsen & Toubro Limited

- Fuji Electric Co., Ltd.

- Rockwell Automation, Inc.

- ABB Ltd.

第七章 市场机会与未来趋势

- 增加对可再生能源和智慧电网基础设施建设的技术投资

简介目录

Product Code: 5000125

The Power Equipment Market size is estimated at USD 33.16 billion in 2025, and is expected to reach USD 42.06 billion by 2030, at a CAGR of 4.87% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. Presently, the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, increasing population growth and infrastructure development are expected to increase energy demand, consequently increasing the demand for power equipment during the forecasted period.

- On the other hand, high operations and maintenance costs are expected to hinder market growth.

- Nevertheless, the increasing technological investments in developing renewable energy and smart grid infrastructure are expected to create huge opportunities for the power equipment market.

Power Equipment Market Trends

Power Generation Expected to Dominate the Market

- The global electricity demand is rising, driven by population growth, urbanization, and industrialization. As a result, power generation equipment plays a critical role in meeting this escalating demand and ensuring a consistent electricity supply.

- Moreover, the expanding focus on renewable energy sources, such as solar, wind, hydro, and geothermal power, further contributes to the dominance of power generation equipment. The transition towards cleaner and more sustainable energy necessitates specialized power generation equipment like solar panels, wind turbines, and hydroelectric generators.

- For instance, in June 2022, Vestas AS won a contract to supply 64 V235-15.0 MW wind turbines for EnBW's 900 MW He Dreiht offshore wind project. Vestas has also entered into an agreement with Cadeler for the transportation and installation of the turbines, which is planned to start in Q2 2025.

- Governments worldwide are also implementing policies, incentives, and renewable energy targets, further boosting the demand for power generation equipment, particularly in the renewable energy sector.

- This has led to an increase in renewable energy installed capacity globally. According to the International Renewable Energy Agency, in 2022 the global renewable energy installed capacity was 3371.8 GW, compared to 3077.23 GW in 2021, registering a growth rate of more than 9.5% between 2021 and 2022.

- Therefore, with increasing energy demand, the focus on renewable energy, government initiatives, and power generation, power generation emerges as the dominant segment within the power equipment market.

Asia-Pacific to Witness Significant Growth

- Asia-Pacific houses a significant proportion of the global population and has numerous major cities. In the coming years, the region is expected to witness a surge in power demand due to the expanding access to electricity among millions of new customers. This escalating demand can be attributed to rapid population growth and the ongoing process of industrialization.

- The Asia-Pacific region is poised to emerge as a prominent market for power equipment in the foreseeable future. The main drivers are the increasing use of renewable energy sources, rising power consumption, increased access to electricity, and ongoing improvements to power grid infrastructure. Key countries such as China, India, Japan, and Australia are anticipated to play pivotal roles in shaping the power equipment market within the region.

- According to the BP statistical review of world energy, the electricity generation in the region was 13,994.4 TWh in 2021, an increase of 8.4% compared to 2020 and 4.7% between 2011 and 2021.

- Additionally, governments in the region are playing a crucial role by implementing favorable policies, initiatives, and investments in power generation and distribution infrastructure. This commitment to energy security, renewable energy promotion, and improved electricity access further propel the demand for power equipment in Asia-Pacific.

- For instance, the Chinese government unveiled its ambitious plan in 2022 to construct solar and wind energy power plants with a total capacity of 450 gigawatts in the Gobi desert regions. This initiative aims to propel the nation towards achieving its renewable energy target by 2030.

- These advancements enable efficient and sustainable power management, enhancing the region's prominence in the power equipment market.

- Asia Pacific is therefore poised to dominate the power equipment market due to rapid economic growth, urbanization, government initiatives, the deployment of renewable energy sources, infrastructure development, industrial demand, and technological advancements.

Power Equipment Industry Overview

The global power equipment market is semi-consolidted. Some of the key players in this market (in no particular order) are General Electric Company, Schneider SE, ABB Ltd., Eaton Corporation, and Siemens AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Population Growth and Infrastructure Development

- 4.5.2 Restraints

- 4.5.2.1 High Operational and Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Equipment Type

- 5.1.1 Generator

- 5.1.2 Transformer

- 5.1.3 Switchgears

- 5.1.4 Circuit Breakers

- 5.1.5 Power Cable

- 5.1.6 Other Equipment Types

- 5.2 Power Generation Source

- 5.2.1 Fossil Fuel Based

- 5.2.2 Solar

- 5.2.3 Wind

- 5.2.4 Nuclear

- 5.2.5 Hydro

- 5.3 End-User

- 5.3.1 Residential

- 5.3.2 Industrial and Commercial

- 5.3.3 Utility

- 5.4 Application

- 5.4.1 Power Generation

- 5.4.2 Transmission

- 5.4.3 Distribution

- 5.5 Geography [Market Size and Demand Forecast till 2028 (for regions only)]

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Australia

- 5.5.3.4 Japan

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Nigeria

- 5.5.4.4 South Africa

- 5.5.4.5 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Chile

- 5.5.5.4 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 General Electric Company

- 6.3.2 Siemens AG

- 6.3.3 Schneider Electric SE

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 Eaton Corporation plc

- 6.3.6 Toshiba Corporation

- 6.3.7 Honeywell International Inc.

- 6.3.8 Bharat Heavy Electricals Limited

- 6.3.9 Crompton Greaves Ltd.

- 6.3.10 Larsen & Toubro Limited

- 6.3.11 Fuji Electric Co., Ltd.

- 6.3.12 Rockwell Automation, Inc.

- 6.3.13 ABB Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technological Investments in Developing Renewable Energy and Smart Grid Infrastructure

02-2729-4219

+886-2-2729-4219

无线工具市场:依工具类型、动力来源、销售管道、最终用途及通路划分-2026-2032年全球市场预测

无线工具市场:依工具类型、动力来源、销售管道、最终用途及通路划分-2026-2032年全球市场预测 电力设备市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、功能、安装类型及解决方案划分

电力设备市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、功能、安装类型及解决方案划分 全球电气装置数位双胞胎市场:预测(至2034年)-按孪生类型、组件、安装类型、部署方法、技术、应用、最终用户和地区进行分析

全球电气装置数位双胞胎市场:预测(至2034年)-按孪生类型、组件、安装类型、部署方法、技术、应用、最终用户和地区进行分析 全球电厂电池市场:市场规模分析(按类型、应用和地区划分)及未来预测(2025-2035 年)

全球电厂电池市场:市场规模分析(按类型、应用和地区划分)及未来预测(2025-2035 年) 全球动力设备用电池市场

全球动力设备用电池市场 电力设备的全球市场,市场规模和占有率的分析 - 成长趋势与预测(2025年~2033年)

电力设备的全球市场,市场规模和占有率的分析 - 成长趋势与预测(2025年~2033年)