|

市场调查报告书

商品编码

1693831

南美氟聚合物:市场占有率分析、产业趋势和成长预测(2024-2029)South America Fluoropolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

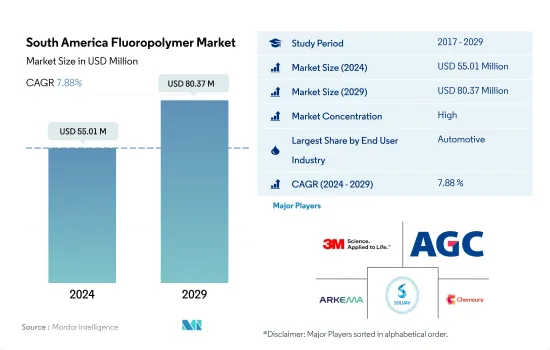

南美氟树脂市场规模预计在 2024 年达到 5,501 万美元,预计到 2029 年将达到 8,037 万美元,预测期内(2024-2029 年)的复合年增长率为 7.88%。

阿根廷汽车工业主导氟聚合物市场

- 由于其多功能性和韧性,氟聚合物已在各种最终用户行业中得到应用。 2022年,由于工业应用的不断增加,氟聚合物已成为越来越商业性的材料。氟树脂的常见用途包括烹调器具、电线、半导体、医疗设备、屋顶材料和防水膜。

- 2017-19年期间,氟聚合物的需求呈现稳定成长,主要受该地区电气和电子产品成长的推动。 2020年,受疫情影响,各种业务、旅行和贸易限制导致氟聚合物的需求与前一年同期比较17.88%。在所有终端用户产业中,汽车和工业机械产业的需求受到的打击最严重,其2019年的销售额分别下降了32.66%和28.41%。随着限制措施的放宽,对氟聚合物的需求增加到疫情前的水平。这一增长主要受到阿根廷的推动。

- 氟聚合物的应用日益广泛,是因为它们能够承受高低温和严重的腐蚀环境,预计大多数化学物质将推动对氟聚合物的需求成长。在南美洲所有终端用户中,阿根廷的汽车产业预计将经历最高成长,预测期内的复合年增长率为 10.65%。预计在预测期内,该地区对氟聚合物的需求量将以 6.21% 的复合年增长率增长,以金额为准将以 7.95% 的复合年增长率增长。

阿根廷经济呈现高成长态势,受汽车产业快速成长支撑

- 南美洲是全球第四大氟聚合物消费量,2022 年的消费量比重仅 1.43%。在南美洲,氟塑胶用于电气/电子、汽车和医疗设备製造业的各种应用。

- 预计预测期内对氟聚合物的需求将稳定成长,复合年增长率为 6.19%。在该地区所有国家的所有子树脂类型中,阿根廷对氟化乙丙烯 (FEP) 的需求成长最快。就数量而言,预计预测期内复合年增长率为 8.40%。

- 2020年,疫情期间的营运和贸易限制导致劳动力短缺、原材料短缺等各种限制因素严重影响了各个终端用户产业,对该地区对氟聚合物的需求产生了负面影响。其中,巴西对氟聚合物的需求受到的打击最为严重。 2020年巴西需求量较去年与前一年同期比较13.20%,地区较去年与前一年同期比较下降10.18%。

- 2021 年,限制措施有所放宽,对氟聚合物的需求超过了疫情前的水准。这一成长主要得益于阿根廷等国家汽车产量的快速扩张。预计这一成长趋势将在整个预测期内持续下去,其中阿根廷对氟聚合物的需求将成长最快。总体而言,南美洲对氟聚合物的需求预计将成长,预测期内以收益为准的复合年增长率为 7.93%。

南美洲氟聚合物市场趋势

技术创新步伐加快推动产业成长

- 在南美洲,巴西在2017年占据该地区电气和电子产品製造业收益的最大份额,接近40%。 2017年,巴西电子产品在电商领域的渗透率接近20%。该地区的技术进步增加了对智慧电视、智慧冰箱、智慧空调等家用电子电器产品以及其他电气和电子产品的需求。 2017-2019年期间,南美电气和电子製造业收入的复合年增长率超过6.16%。

- 2020年,受疫情影响,远距办公和家庭娱乐等家用电子电器产品需求增加,该地区电气和电子产品产量较去年与前一年同期比较成长1.1%。可支配收入的增加、奢侈品需求的不断增长、技术进步和生活水准的提高是推动电气和电子设备市场成长的一些关键因素。因此,该地区 2021 年电气和电子设备产量销售额也成长了 14.9%。

- 电子创新的快速步伐推动着对更新、更快的电气和电子产品的持续需求。因此,该地区对电气和电子设备生产的需求也在增加。 LG、三星、微软、松下、戴尔、英特尔、东芝、索尼、飞利浦、夏普、苹果和联想等跨国公司的存在也对电气和电子设备市场产生了积极影响。预计所有这些因素将在预测期内推动该地区电气和电子设备产量增加约 7%。

南美洲氟聚合物产业概况

南美洲氟聚合物市场相当集中,前五大公司占了79.37%的市占率。市场的主要企业包括 3M、AGC Inc.、Arkema、Solvay、The Chemours Company 等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 最终用户趋势

- 航太

- 车

- 建筑与施工

- 电气和电子

- 包装

- 进出口趋势

- 氟树脂交易

- 法律规范

- 阿根廷

- 巴西

- 价值炼和通路分析

第五章市场区隔

- 最终用户产业

- 航太

- 车

- 建筑与施工

- 电气和电子

- 工业/机械

- 其他的

- 子树脂类型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯(PVF)

- 聚二氟亚乙烯(PVDF)

- 其他子树脂类型

- 国家

- 阿根廷

- 巴西

- 南美洲其他地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介

- 3M

- AGC Inc.

- Arkema

- Dongyue Group

- Gujarat Fluorochemicals Limited(GFL)

- Solvay

- The Chemours Company

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架(产业吸引力分析)

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 数据包

- 词彙表

简介目录

Product Code: 5000169

The South America Fluoropolymer Market size is estimated at 55.01 million USD in 2024, and is expected to reach 80.37 million USD by 2029, growing at a CAGR of 7.88% during the forecast period (2024-2029).

The automotive industry in Argentina to dominate the market for fluoropolymers

- Fluoropolymers find applications in a range of end-user industries due to their versatile and tough nature. In 2022, the increase in industrial applications made fluoropolymers an increasingly commercial material. Common fluoropolymer applications are cookware, wires, semiconductors, medical devices, roofing materials, and waterproof films.

- During the 2017-19 period, the demand for fluoropolymers witnessed steady growth, which was majorly driven by the increase in electrical and electronics products in the region. In 2020, due to various operational, travel, and trade restrictions, because of the pandemic, the demand for fluoropolymers witnessed a Y-o-Y decline of 17.88%. Among all end-user industries, the demand from the automotive and industrial machinery industries took the worst hit, declining by 32.66% and 28.41% of their 2019 revenue. As the restrictions eased, the demand for fluoropolymers increased to pre-pandemic levels. This growth was majorly driven by Argentina.

- The increasing applications of fluoropolymers are due to their ability to resist high and low temperatures and severe corrosive environments, and most chemicals are expected to drive the growth in the demand for fluoropolymers. Among all end users in South America, the automotive industry in Argentina is expected to witness the highest growth, with a CAGR of 10.65% in volume terms during the forecast period. The regional demand for fluoropolymers is expected to register CAGRs of 6.21% and 7.95% in volume and value terms, respectively, during the forecast period.

Argentina to exhibit high growth, aided by fast-paced automobile industry

- South America ranks fourth in the consumption of fluoropolymers globally, and it occupied a share of just 1.43%, by volume, in 2022. In South America, fluoropolymers find a range of applications in the electrical and electronics, automotive, and healthcare device manufacturing industries.

- During the forecast period, the demand for fluoropolymers is expected to witness steady growth, registering a CAGR of 6.19%, mainly driven by the rapid growth in the electrical and electronics industry in countries like Argentina. Among all sub-resin types in all countries in the region, the demand for fluorinated ethylene-propylene (FEP) in Argentina witnesses the highest growth. In volume terms, its demand is expected to record a CAGR of 8.40% during the forecast period.

- In 2020, various restraining factors like worker unavailability and raw material shortages, which resulted from operational and trade restrictions during the pandemic, severely affected various end-user industries, negatively affecting the region's fluoropolymer demand. Among all countries, Brazil's fluoropolymer demand received the biggest impact. In 2020, the country's Y-o-Y demand volume declined by 13.20%, whereas the regional Y-o-Y decline was 10.18%.

- In 2021, as the restrictions eased, fluoropolymer demand outgrew its pre-pandemic levels. This growth was majorly driven by the rapid growth in automotive production in countries like Argentina. This growth trend is expected to continue throughout the forecast period, with Argentina witnessing the highest growth in fluoropolymer demand among all countries. Overall, fluoropolymer demand from South America is expected to grow, recording a CAGR of 7.93% in revenue terms during the forecast period.

South America Fluoropolymer Market Trends

Rapid pace of technological innovations to boost the industry growth

- In South America, Brazil held the major share of nearly 40% of the region's electrical and electronics production revenue in 2017. In 2017, Brazilian electronics products had a penetration of nearly 20% in the e-commerce sector. The advancement of technology in the region increased the demand for consumer electronics products, such as smart TVs, smart refrigerators, smart air conditioners, and other electrical and electronic products. South American electrical and electronics production revenue witnessed a CAGR of over 6.16% between 2017 and 2019.

- In 2020, with the rise in demand for consumer electronics for remote working and home entertainment due to the pandemic, the production of electrical and electronic products in the region increased at a growth rate of 1.1% by revenue compared to the previous year. Rising disposable income, increased demand for luxury products, technological advancements, and improvement in living standards are some of the major factors driving the electrical and electronics market's growth. As a result, in the region, electrical and electronics production also increased at a rate of 14.9% by revenue in 2021.

- The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for the production of electrical and electronics in the region. The penetration of multinational companies, like LG, Samsung, Microsoft, Panasonic, Dell, Intel, Toshiba, Sony, Philips, Sharp, Apple, and Lenovo, also positively affects the electrical and electronics market. All such factors are expected to fuel the production revenue of electrical and electronics in the region during the forecast period at a rate of around 7%.

South America Fluoropolymer Industry Overview

The South America Fluoropolymer Market is fairly consolidated, with the top five companies occupying 79.37%. The major players in this market are 3M, AGC Inc., Arkema, Solvay and The Chemours Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Other End-user Industries

- 5.2 Sub Resin Type

- 5.2.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.3 Polytetrafluoroethylene (PTFE)

- 5.2.4 Polyvinylfluoride (PVF)

- 5.2.5 Polyvinylidene Fluoride (PVDF)

- 5.2.6 Other Sub Resin Types

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arkema

- 6.4.4 Dongyue Group

- 6.4.5 Gujarat Fluorochemicals Limited (GFL)

- 6.4.6 Solvay

- 6.4.7 The Chemours Company

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

高纯度氟聚合物(PFA)管材和管道-2026-2032 年全球市场份额和排名、总销售额和需求预测。

高纯度氟聚合物(PFA)管材和管道-2026-2032 年全球市场份额和排名、总销售额和需求预测。 医用氟聚合物市场:2026-2032年全球市场预测(按产品类型、形态、技术、应用和最终用途产业划分)氟聚合物市场:按类型、形态、製程和最终用户划分-2026-2032年全球市场预测半导体氟聚合物管材市场:管材类型、材质、製造流程、直径范围、应用及最终用途-2026-2032年全球市场预测5G含氟聚合物市场:依产品类型、形态、製造流程和最终用途产业划分-2026-2032年全球预测

医用氟聚合物市场:2026-2032年全球市场预测(按产品类型、形态、技术、应用和最终用途产业划分)氟聚合物市场:按类型、形态、製程和最终用户划分-2026-2032年全球市场预测半导体氟聚合物管材市场:管材类型、材质、製造流程、直径范围、应用及最终用途-2026-2032年全球市场预测5G含氟聚合物市场:依产品类型、形态、製造流程和最终用途产业划分-2026-2032年全球预测 全球高通量纤维增强塑胶(HPF)市场(至2030年):按类型(PTFE、FEP、PFA/MFA、ETFE)、形状、应用(涂层和衬里、组件、薄膜、添加剂)、终端用户产业(电气和电子、工业流程、交通运输、医疗)和地区划分

全球高通量纤维增强塑胶(HPF)市场(至2030年):按类型(PTFE、FEP、PFA/MFA、ETFE)、形状、应用(涂层和衬里、组件、薄膜、添加剂)、终端用户产业(电气和电子、工业流程、交通运输、医疗)和地区划分 氟聚合物加工助剂市场分析与预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、製程、功能

氟聚合物加工助剂市场分析与预测(至2035年):类型、产品类型、应用、技术、材料类型、最终用户、製程、功能 全球氟聚合物市场规模、份额、趋势和成长分析报告(2026-2034)

全球氟聚合物市场规模、份额、趋势和成长分析报告(2026-2034) 熔融加工型含氟聚合物的市场规模、成长与预测(至2034年)功能性保护套管市场按产品类型、材质、应用、最终用途产业、分销通路、安装类型和直径划分-2026年至2032年全球预测

熔融加工型含氟聚合物的市场规模、成长与预测(至2034年)功能性保护套管市场按产品类型、材质、应用、最终用途产业、分销通路、安装类型和直径划分-2026年至2032年全球预测

▼