|

市场调查报告书

商品编码

1693854

中东卫星通讯:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Middle East Satellite Communications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

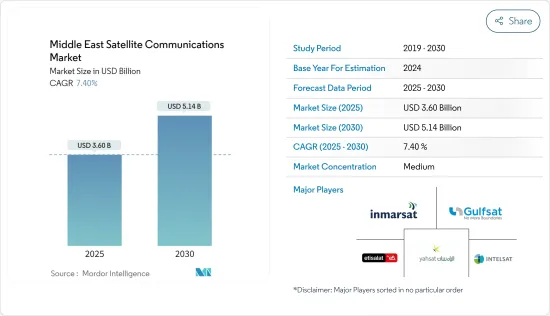

中东卫星通讯市场规模预计在 2025 年为 36 亿美元,预计到 2030 年将达到 51.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.4%。

关键亮点

- 预计行动宽频需求不断增长、智慧型手机和智慧型穿戴装置使用量不断增长以及行动视讯采用需求激增等因素将在预测期内推动 5G 的成长,从而推动研究市场的成长。此外,小型化、连接技术、强大的网路环境、低功耗计算、无线射频识别和 M2M通讯的进步预计将推动卫星通讯市场的发展。

- 对于宽频通讯的需求持续有增无减,且不一定与地点相关。这种需求包括在固定地点和移动中作业的飞机、船舶和车辆(包括紧急应变人员)上的使用者的连接需求。这三个平台都需要沿途保持持续的连接,而这些线路通常会经过大都会圈服务不足和人口稀少的地区。预计这些趋势将推动市场的成长。

- 卫星通讯的变化以及各种通讯和电脑流程的进步导致了该领域创新领域新机会的出现。随着工业生产设施和采矿作业进入更难以到达的地形,透过地面和通讯通讯实现高效无线互连的需求正在迅速增加。

- 利用地面通讯基础设施实现此类操作的解决方案(通常是 LTE,长期演进)相对较慢、昂贵且不易扩展。卫星通讯是一种有效的替代方案,因为它具有卓越的可靠性、成本效益、良好的可访问性和可扩展性,为研究市场的成长提供了无数机会。

- 然而,卫星技术的快速发展和该地区卫星通讯服务的持续普及,增加了网路攻击的风险和频率,这可能会影响中东卫星通讯领域的发展和稳定。

- 由于卫星通讯在提供语音和数据方面有广泛的应用,新冠疫情增加了对卫星通讯的需求。此外,为了维持企业运作和人们之间的联繫,对卫星通讯(包括网路和宽频服务)的需求也在增加。娱乐业进一步依赖卫星通讯来传递新闻和娱乐,让人们可以在舒适的家中随时了解 COVID-19 指南和其他必要资讯。这种日益增长的依赖性极大地支持了被调查市场的成长。

中东卫星通讯市场趋势

网路营运中心 (NOC) 推动成长

- 网路营运中心 (NOC) 是透过电脑、通讯或卫星网路进行网路监控和控製或网路管理的一个或多个站点。卫星网路环境处理大量音讯和影像资料以及情报、监控和侦察资料。凭藉更强大的基础设施,许多组织受益于更好的管理和按需报告。监控功能可帮助 NOC 减少不必要的警报和警报疲劳。

- 随着中东地区采用 5G、物联网 (IoT) 和边缘运算等新技术,日益增加的复杂性正在决定 NOC 的未来。随着企业转向云端基础的服务并采用最新、最具创新性的技术,网路管理必须变得同样灵活、跟上步伐并保持最佳实践。预计 NOC 将变得更加灵活和多功能,充分发挥其潜力,取得成果,并无缝现代化,以反映新的先进能力。

- 此外,预计透过该地区的合作伙伴关係实现的扩张将有助于预测期内的市场成长率。例如,2023年9月,卫星服务供应商OneWeb与NEOM认知技术生态系统背后的科技公司TONOMUS的合资企业First Tech Web Company Limited委託沙乌地阿拉伯建设公司Albabtain LeBlanc在沙乌地阿拉伯塔布克开发卫星站。

- 该卫星站将成为合资企业地面基础设施的一部分,透过为该地区服务不足的人群和企业提供稳定、高速的宽频连接,帮助解决沙乌地阿拉伯以及全部区域落差问题。该站预计将于 2023 年底完工,Al-Babaten LeBlanc 将加入 OneWeb,与中东、欧洲、非洲和亚洲的合作伙伴携手合作。

- 总体而言,中东卫星通讯市场网路营运中心(NOC)的成长受到几个关键因素的推动,这些因素主要导致了全部区域对高效、可靠的通讯解决方案的需求不断增长。

土地部分确认增长

- 陆地平台部门是指专为陆基营运和通讯需求设计的卫星通讯解决方案和服务。卫星通讯陆地平台解决方案旨在为陆地上的固定和偏远地区以及陆地基础设施提供无缝连接、可靠的数据传输和高效的通讯服务,使用户能够建立强大而可靠的通讯链路、访问关键数据并确保中东多样化陆地景观和地形的持续运营连接。

- 中东地区地面基础设施正在快速发展,包括不断扩大的都市区、工业区和交通网络,这推动了跨地面设施和地点的数据传输、连接和运营协调的需求,需要强大而可靠的通讯解决方案。

- 此外,国防和政府部门重视安全和有弹性的通讯服务以支援国防和边防安全,这进一步推动了陆地平台领域采用卫星通讯解决方案。根据斯德哥尔摩国际和平实验室(SIPRI)的数据,2022年中东地区军费总开支估计为1,840亿美元,比2021年成长3.2%。

- 这一成长主要得益于沙乌地阿拉伯王国的支出成长 16%,预计 2022 年沙乌地阿拉伯的支出将达到 750 亿美元,位居中东第一、全球第五,这也是该国自 2018 年以来首次增加支出。卡达位居中东第三、全球第 20 位,预计支出为 156 亿美元,是支出增幅最高的国家,与前一年同期比较增长了 27%。中东地区军事开支的快速成长凸显了该地区对加强国家安全和防御态势的日益重视,从而导致对满足军事和防御需求的先进卫星通讯解决方案的需求增加。

- 总体而言,陆地平台市场部分受到地面基础设施的持续发展以及国防和政府部门对安全和弹性通讯服务的日益重视的推动,从而促进了陆地平台市场部分的持续增长。

中东卫星通讯产业概况

在中东卫星通讯市场,许多供应商透过各种成长策略相互竞争,包括联盟、伙伴关係和新进者。知名参与企业包括 E&ETISALAT(阿联酋电信集团公司 PJSC)、L3Harris Technologies Inc.、Gulfsat Communications Company、Al Yah Satellite Communications Company PJSC 和 Inmarsat Global Limited(Viasat Inc.)。

2023 年 9 月,Al Yahr 卫星通讯公司与阿联酋政府伙伴关係政府解决方案部门 Yahrsat 政府解决方案,引起波动。此次合作旨在未来 17 年提供基于通讯的託管服务,使该公司的收益增加 51 亿美元,并在整个预测期内显着加强市场影响。

同时,欧洲通讯卫星公司 (Eutelsat Communications SA) 完成了与全球领先的低地球轨道 (LEO) 卫星通讯网路 OneWeb 的全股票合併。该子公司以 Eutelsat OneWeb 的名称进行商业性运营,并在伦敦设有营运基地,这标誌着该公司发展历程中的一个重要里程碑。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 物联网 (IoT) 与自主系统的发展

- 军事和国防卫星通讯解决方案需求不断增长

- 市场限制

- 卫星通讯面临的网路安全威胁

- 资料传输受到干扰

第六章市场区隔

- 按类型

- 地面设施

- 卫星网关

- 甚小孔径终端(VSAT)设备

- 网路营运中心(NOC)

- 卫星新闻采集(SNG)设备

- 服务

- 行动卫星服务(MSS)

- 地球观测服务

- 地面设施

- 按平台

- 可携式的

- 土地

- 海上

- 航空

- 按行业

- 海上

- 国防和政府机构

- 企业

- 媒体和娱乐

- 其他最终用户

第七章竞争格局

- 公司简介

- Inmarsat Global Limited(Viasat Inc.)

- Al Yah Satellite Communications Company PJSC

- Gulfsat Communications Company

- L3Harris Technologies Inc.

- E& ETISALAT and(Emirates Telecommunication Group Company PJSC)

- Eutelsat Communications SA

- Intelsat SA

- Thales Group

- Saudi Telecom Company(STC)

- Raytheon Technologies Corporation

- Arabsat

第八章投资分析

第九章 市场机会与未来趋势

The Middle East Satellite Communications Market size is estimated at USD 3.60 billion in 2025, and is expected to reach USD 5.14 billion by 2030, at a CAGR of 7.4% during the forecast period (2025-2030).

Key Highlights

- Factors such as the rising demand for mobile broadband, the growing use of smartphones and smart wearable devices, and the surging demand for mobile video adoption are expected to drive the growth of 5G over the forecast period, which is expected to aid the growth of the market studied. Furthermore, advancements in miniaturization, connected technologies, robust network environment, low-power computing, radio frequency identification, and M2M communication are anticipated to drive the satellite communication market.

- The demand for broadband communications continues unabated and is not necessarily location-specific. Such demands include connectivity requirements for users on aircraft, ships, and vehicles (including first responders) that operate at fixed locations and while in motion. These three platforms need continuous connectivity along their travel routes, often taking them through unserved parts of major metropolitan areas and less densely populated areas. Such trends are expected to aid in the growth of the studied market.

- Changes in satellite communications and the progress in all kinds of telecommunications and computer processes led to the evolution of new opportunities in innovative areas in the sector. As industrial production facilities and mining operations move further into inaccessible terrains, the requirement for efficient wireless interconnection through terrestrial and satellite communications is increasing rapidly.

- To fulfill the operations, the solutions leveraging terrestrial mobile communication infrastructures, typically like long-term evolution (LTE), are relatively slow, expensive, and not easily scalable. Satellite communication is an efficient alternative because of its superior reliability, cost-effectiveness, excellent accessibility, and scalability, thereby providing plenty of opportunities for the growth of the market being studied.

- However, as the region continues to witness rapid advancements in satellite technology and an upsurge in satellite communication services, there is an increased risk and frequency of cyberattacks, which might impact the growth and stability of the satellite communications sector in the Middle East.

- The COVID-19 pandemic increased the demand for satellite communication due to its vast applications in providing voice data. Furthermore, the demand was driven by the increasing need for satellite communications, including internet and broadband services, to continue operations and keep people connected. The entertainment industry has further depended on satellite communication to deliver news and entertainment, which allowed people to remain updated regarding COVID-19 guidelines and other necessary information while being restricted at home. Such increased dependency has largely supported the growth of the studied market.

Middle East Satellite Communications Market Trends

Network Operation Center (NOC) is to Witness the Growth

- A network operations center (NOC) is one or more sites from which network monitoring and control, or network management, over a computer, telecommunications, or satellite network is exercised. Large volumes of voice and video data and intelligence, surveillance, and reconnaissance data are processed in satellite network environments. With enhanced infrastructure, many organizations benefit from better administration and on-demand reporting. With their monitoring capabilities, NOCs help reduce undesirable alerts and alert fatigue.

- As new technologies, like 5G, the Internet of Things (IoT), and edge computing are adopted in the Middle East, deepening complexity defines the future of NOCs. As businesses advance toward cloud-based services and adopt the latest, most innovative technologies, network management must be just as agile, keep pace, and maintain best practices. The NOC is expected to become even more flexible and versatile, to work at its full potential and deliver results, and seamlessly modernize to reflect new, progressive capabilities.

- Further, the growing expansions through collaborations in the region are analyzed to contribute to the market growth rate during the forecast period. For instance, in September 2023, First Tech Web Company Limited, a joint venture between OneWeb, a satellite service provider, and TONOMUS, the tech company powering the ecosystem of cognitive technologies at NEOM - has appointed Albabtain LeBlanc, a Saudi Arabian construction company, to develop a satellite station in Tabuk, Saudi Arabia.

- By providing a consistent, fast broadband connection to people and businesses that are unserved or under-resourced throughout the Middle East regions, this station forms part of joint ventures' ground infrastructure, which seeks to support the objective of addressing the Digital Divide between Saudi Arabia and the wider MENA region. With Albabtain LeBlanc joining the OneWeb roster for partners across the Middle East, Europe, Africa, and Asia, this station is scheduled to be completed by the end of 2023.

- Overall, the growth of the Network Operation Center (NOC) in the Middle East satellite communications market is primarily driven by several key factors that contribute to the increasing demand for efficient and reliable communication solutions across the region.

Land Segment to Witness the Growth

- The land platform segment refers to satellite communication solutions and services specifically designed for terrestrial operations and communication requirements on land. Land platform solutions in satellite communications are developed to facilitate seamless connectivity, reliable data transmission, and efficient communication services for fixed terrestrial locations, remote sites, and terrestrial infrastructure, thereby enabling users to establish robust and dependable communication links, access critical data, and ensure continuous operational connectivity across diverse terrestrial landscapes and geographical terrains in the Middle East.

- The ongoing development of terrestrial infrastructure in the Middle East, including expanding urban areas, industrial zones, and transportation networks, necessitates robust and reliable communication solutions to support the growing need for data transmission, connectivity, and operational coordination across various terrestrial facilities and locations.

- Additionally, the defense and government sector's emphasis on secure and resilient communication services to support national defense and border security further drives the adoption of satellite communication solutions within the land platform segment. The total military spending in the Middle East was estimated to be USD 184 billion in 2022, up 3.2% from 2021, according to data from the Stockholm International Peace Research Institute (SIPRI).

- The increase was attributed to the Kingdom of Saudi Arabia's 16% spending growth, which resulted in an estimated USD 75 billion in 2022, ranking first in the Middle East and five globally, its first increase since 2018, and Qatar, which ranked third in the Middle East and 20 globally with an estimated spend of USD 15.6 billion, registered the highest year-over-year spending growth of any country, with a 27% increase. The surge in military spending across the Middle East highlights the region's growing emphasis on strengthening national security and defense preparedness, leading to an increased demand for sophisticated satellite communication solutions tailored to the requirements of military and defense applications.

- Overall, the land platform segment in the market is being driven by the continuous development of terrestrial infrastructure, increasing emphasis on secure and resilient communication services within the defense and government sectors, contributing to the sustained growth of the land platform segment in the market.

Middle East Satellite Communications Industry Overview

In the Middle East satellite communications market, numerous vendors vie for prominence through diverse growth strategies such as collaborations, partnerships, and new launches. Notable players include E& ETISALAT (Emirates Telecommunication Group Company PJSC), L3Harris Technologies Inc., Gulfsat Communications Company, Al Yah Satellite Communications Company PJSC, and Inmarsat Global Limited (Viasat Inc.).

In September 2023, Al Yah Satellite Communications made waves with its Government Solutions arm, Yahsat Government Solutions, forging a partnership with the UAE government. This alliance aims to deliver satellite communication-based managed services for the next 17 years, propelling the company's revenue by USD 5.1 Billion and significantly bolstering its market presence across Middle Eastern countries throughout the forecast period.

Simultaneously, Eutelsat Communications SA finalized an all-share merger with OneWeb, a prominent global low Earth orbit (LEO) satellite communications network. Operating commercially as Eutelsat OneWeb, this subsidiary maintains its operational hub in London, marking a significant milestone in the company's trajectory.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 The Growth of Internet of Things (IoT) and Autonomous Systems

- 5.1.2 Increasing Demand for Military and Defense Satellite Communication Solutions

- 5.2 Market Restraints

- 5.2.1 Cybersecurity Threats to Satellite Communication

- 5.2.2 Interference in Transmission of Data

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Ground Equipment

- 6.1.1.1 Satellite Gateway

- 6.1.1.2 Very Small Aperture Terminal (VSAT) Equipment

- 6.1.1.3 Network Operation Center (NOC)

- 6.1.1.4 Satellite News Gathering (SNG) Equipment

- 6.1.2 Services

- 6.1.2.1 Mobile Satellite Services (MSS)

- 6.1.2.2 Earth Observation Services

- 6.1.1 Ground Equipment

- 6.2 By Platform

- 6.2.1 Portable

- 6.2.2 Land

- 6.2.3 Maritime

- 6.2.4 Airborne

- 6.3 By End-User Vertical

- 6.3.1 Maritime

- 6.3.2 Defense and Government

- 6.3.3 Enterprises

- 6.3.4 Media and Entertainment

- 6.3.5 Other End-User Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Inmarsat Global Limited (Viasat Inc.)

- 7.1.2 Al Yah Satellite Communications Company PJSC

- 7.1.3 Gulfsat Communications Company

- 7.1.4 L3Harris Technologies Inc.

- 7.1.5 E& ETISALAT and (Emirates Telecommunication Group Company PJSC)

- 7.1.6 Eutelsat Communications S.A.

- 7.1.7 Intelsat S.A.

- 7.1.8 Thales Group

- 7.1.9 Saudi Telecom Company (STC)

- 7.1.10 Raytheon Technologies Corporation

- 7.1.11 Arabsat

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年极地卫星通讯全球市场报告2025年5G卫星通讯全球市场报告2025年全球天基网路市场报告2025年立方卫星下行链路服务全球市场报告

2025年极地卫星通讯全球市场报告2025年5G卫星通讯全球市场报告2025年全球天基网路市场报告2025年立方卫星下行链路服务全球市场报告 5G卫星通讯市场按组件、频谱、轨道类型、应用和最终用户划分-2025-2032年全球预测M2M卫星通讯市场:2025-2032年全球预测(依产业、应用、平台类型、频宽及服务类型划分)

5G卫星通讯市场按组件、频谱、轨道类型、应用和最终用户划分-2025-2032年全球预测M2M卫星通讯市场:2025-2032年全球预测(依产业、应用、平台类型、频宽及服务类型划分) 卫星IoT通讯的全球市场 - 第5版卫星通讯市场按组件、通讯类型、分析技术、卫星类型、频段、应用和最终用户划分-2025-2032年全球预测卫星通讯市场按组件类型、轨道类型、技术、频宽、应用、最终用户和市场管道划分 - 全球预测 2025-2032无人机(UAV)卫星通讯市场按组件、卫星类型、频段、飞机类型、无人机重量等级、任务持续时间和应用划分-全球预测,2025-2032年

卫星IoT通讯的全球市场 - 第5版卫星通讯市场按组件、通讯类型、分析技术、卫星类型、频段、应用和最终用户划分-2025-2032年全球预测卫星通讯市场按组件类型、轨道类型、技术、频宽、应用、最终用户和市场管道划分 - 全球预测 2025-2032无人机(UAV)卫星通讯市场按组件、卫星类型、频段、飞机类型、无人机重量等级、任务持续时间和应用划分-全球预测,2025-2032年