|

市场调查报告书

商品编码

1693970

永续发展顾问服务 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Sustainability Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

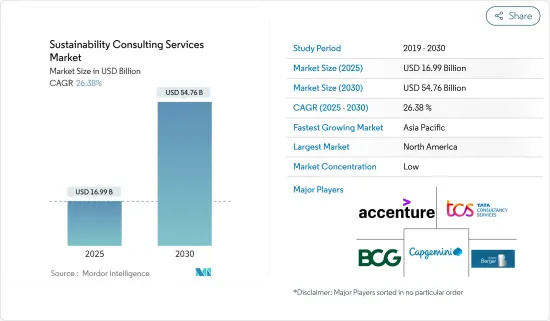

永续发展咨询服务市场规模预计在 2025 年为 169.9 亿美元,预计到 2030 年将达到 547.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 26.38%。

永续发展咨询服务市场的扩张受到多种因素的推动。这些包括对环境、社会和管治(ESG) 问题的认识不断提高、对减少碳足迹的关注度不断提高、相关人员的压力不断增加、监管合规要求越来越严格以及公司需要采取可持续的做法来满足客户期望并提高其声誉。

关键亮点

- 此外,这种成长代表着商业环境的重大变化,永续性已成为企业策略和决策的核心。随着企业努力适应不断变化的气候条件、致力于减少温室气体排放并实现全球永续发展基准,全球永续发展咨询服务市场将持续扩大。因此,咨询公司在帮助政府、企业和非营利组织制定策略、采取永续做法和应对日益复杂的气候变迁方面发挥关键作用。

- 人们对减少碳排放的兴趣日益浓厚,以及企业实现净零目标的需求日益增长,推动了对永续发展咨询服务的需求。世界各地的公司越来越致力于实现温室气体「净零」排放,以配合应对气候变迁的努力。这积极推动了企业对永续发展咨询服务的需求,以有效实现净零目标。

- 世界各国纷纷制定应对气候变迁的国家目标,大大增加了对永续发展咨询服务的需求。世界各国政府都在采取措施实现净零排放,这刺激了对永续发展咨询服务的需求,这些服务在製定策略和指导政府实现净零目标方面发挥着至关重要的作用。

- 现实差距大和采用率低是阻碍全球永续发展咨询服务市场成长的主要因素。由于各国对永续发展措施的采用仍处于停滞状态,环境顾问公司在推动永续发展方面面临挑战。由于财政、技术和人力资源有限,组织往往难以解决气候变迁调适等复杂且有争议的问题。结果,私营和公共部门组织对永续性咨询服务的使用有所下降。

- 持续不断的俄乌战争对全球永续发展咨询服务市场产生了重大影响。俄乌战争对全球经济成长和劳动市场造成重大影响,加剧了通膨压力,并导致供应链严重中断。战争正在破坏供应链,特别是永续发展计划所必需的材料和商品的供应链。尤其是电动车电池必不可少的镍和钯,在供应链中面临重大挑战。

永续发展咨询服务市场的趋势

气候变迁咨询服务占主要市场占有率

- 气候变迁咨询服务包括碳足迹和缓解分析、替代能源开发和能源效率、气候适应和策略、紧急管理、碳补偿/净零服务、环境合规服务、废弃物管理和循环经济以及其他服务。

- 气候变迁咨询服务的需求不断增长,因为企业和组织寻求专家建议,以减少对环境的影响、减少碳足迹、适应气候变迁、管理风险、确保遵守法规和永续实践。

- 世界各地的企业都在努力应对气候变迁的影响。因此,对于希望在新的净零模式下保持竞争力和蓬勃发展的企业来说,管理与气候变迁相关的风险(包括物理风险、过渡风险和责任风险)变得至关重要。这种不断变化的情况导致对一系列以气候变迁为重点的咨询服务的需求增加,以帮助应对复杂的情况。

- 根据全球大气研究/联合研究中心排放资料库(EDGAR/JRC)发布的2024年世界各国温室气体(GHG)排放报告显示,2023年全球温室气体(GHG)排放再创新高,达到529.6亿吨二氧化碳当量(Gt CO2e),比与前一年同期比较增长2%。

- 此外,在气候变迁议题上发挥领导作用的公司将提高其声誉,并将自己定位为永续发展的领导者。这种积极主动的方法可以吸引客户、人才和宝贵的伙伴关係,为您带来显着的竞争优势。

- 永续发展咨询市场的供应商正在收购气候变迁顾问公司。该策略旨在扩大其提供的服务范围,提高其市场占有率并满足日益增长的气候变迁咨询服务需求。

- 例如,2024 年 6 月,永续发展顾问公司 ERM 宣布已同意收购澳洲气候风险与能源转型顾问公司 Energetics。此举旨在加强亚太地区企业风险管理的发展。 Energetics 专门提供客製化服务,例如製定气候适应性策略、提供气候风险和可再生能源转型洞察、指导企业实现净零目标以及监控可再生能源交易的购电协议 (PPA)。 ERM表示,此次收购将增强其为澳洲和亚太地区的客户提供策略建议和实际实施的能力。

- 总体而言,气候变迁咨询服务预计将占据全球永续发展咨询市场的最大份额。随着企业和组织越来越意识到气候变迁的影响,面临减少碳排放的监管压力,以及全球气候行动的激增,对气候变迁咨询服务的需求也在增加。企业寻求透过积极主动的气候变迁风险管理来提高竞争力,这进一步推动了这项需求。

亚太地区经济强劲成长

- 多样化的法律规范和快速的工业化正在塑造亚太地区的永续发展咨询市场。政府对环境标准法规的加强,特别是在製造业、石油天然气和建设业等能源密集型行业,对该地区的扩张做出了重大贡献。为此,亚太地区的永续发展顾问公司正在帮助企业实现合规目标、采用绿色策略并将永续实践纳入业务中。

- 中国和印度等国家正在经历快速的都市化和工业化,并面临环境恶化的问题。这促使政府制定了更严格的环境标准。在此背景下,永续发展顾问公司发挥着至关重要的作用,指导企业创建协调成长与环境管理的经营模式,同时确保遵守国家和国际永续发展基准。

- 例如,在都市化加快和国家「双碳」目标(即2030年碳排放达到高峰、2060年实现完全碳中和)的推动下,中国正在加大建筑业绿色化。根据政府数据,2020年中国77%的城镇新建计划被归类为绿建筑。

- 2023年10月,上海宣布了一项三年计划,旨在加强在该市运营的外资企业的ESG能力。该计画鼓励企业增加研发投入,采用数位化、绿色和低碳技术,以增强创新和竞争力,并增加对永续发展咨询解决方案的需求。

- 亚太地区越来越多的公司正在采用 ESG 原则来吸引全球投资者并提高其品牌声誉。永续发展顾问公司正在透过确定需要加强的领域、实施 ESG 策略和准备国际永续发展报告标准来帮助这些公司。

永续发展咨询服务市场概览

永续发展咨询服务市场的特点是既有参与企业企业,也有新兴参与企业,形式多元。主要参与企业包括埃森哲(Accenture PLC)、波士顿顾问集团、塔塔咨询服务有限公司、Capgemini SA顾问公司和罗兰贝格公司。

该市场中适度的退出障碍奖励了新参与企业,同时允许现有企业在收益较低时期退出。业界领先的公司越来越多地采用整合解决方案来吸引客户。相较之下,规模较小的新进入者预计将采取具有成本效益的策略与规模较大的参与者竞争,加剧竞争。

此外,近期合资企业和收购的显着增加证明了全球商业界对永续性的重视。因此,全球永续发展市场中竞争公司之间的敌意依然突出。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 评估市场的宏观经济因素

第五章市场动态

- 市场驱动因素

- 更重视减少碳足迹和实现净零目标

- 世界各国应对气候变迁的国家目标

- 市场问题

- 采用率低,与现实状况差距较大

第六章市场区隔

- 按服务类型

- 气候变迁咨询服务

- 绿建筑咨询服务

- ESG咨询服务

- 其他可持续发展咨询服务

- 按最终用户

- 建筑和房地产

- 能源动力

- 公共部门

- 其他的

- 按地区

- 北美洲

- 欧洲

- 英国

- 德国

- 比荷卢经济联盟

- 西班牙

- 法国

- 北欧的

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Accenture PLC

- The Boston Consulting Group, Inc.

- Tata Consultancy Services Limited

- Capgemini SE

- Roland Berger GmbH

- Bain & Company, Inc.

- KPMG International Limited

- Ernst & Young Global Limited

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers LLP

- McKinsey & Company

- Kearney

- Godrej & Boyce Mfg. Co. Ltd(Godrej Industries Limited)

- RPS Group(Tetra Tech Inc.)

- SEA Energy

第八章投资分析

第九章:未来市场展望

The Sustainability Consulting Services Market size is estimated at USD 16.99 billion in 2025, and is expected to reach USD 54.76 billion by 2030, at a CAGR of 26.38% during the forecast period (2025-2030).

The expansion of the sustainability consulting services market is driven by several factors. These include increased awareness of environmental, social, and governance (ESG) issues, a stronger focus on reducing carbon footprints, heightened stakeholder pressures, more stringent regulatory compliance requirements, and the necessity for businesses to adopt sustainable practices to meet customer expectations and enhance their reputation.

Key Highlights

- Moreover, this growth signifies a pivotal transformation in the business landscape, with sustainability taking center stage in corporate strategies and decision-making. As companies increasingly adapt to evolving climate conditions, aim to reduce greenhouse gas emissions, and strive to meet global sustainability benchmarks, the global sustainability consulting services market is poised for continued expansion. Consequently, consulting firms play a vital role in assisting governments, businesses, and nonprofit entities in creating strategies, adopting sustainable practices, and navigating the increasing complexities of the changing climate.

- The rising focus on carbon footprint reduction and the growing need to fulfill businesses' net zero targets drive the demand for sustainability consulting services. Companies worldwide increasingly commit to achieving "net zero" greenhouse gas emissions, aligning with initiatives to combat climate change. This positively drives businesses' demand for sustainability consulting services to achieve their net-zero targets efficiently.

- Countries worldwide are setting national goals to combat climate change, significantly boosting the demand for sustainability consulting services. Governments are implementing measures to achieve net-zero emissions, fueling the demand for sustainability consulting services, which are pivotal in guiding governments and formulating strategies toward their net-zero targets.

- Lower levels of adoption, with large gaps in reality, are a major factor hindering the growth of the global sustainability consulting services market. Environmental consulting firms face challenges in promoting sustainability due to the sluggish adoption of sustainability initiatives across various nations. Organizations frequently struggle with limited financial, technical, and human resources, making addressing intricate and contentious issues such as climate change adaptation difficult. Consequently, this dynamic results in diminished uptake of sustainability consulting services, both in the private sector and among public sector enterprises.

- The ongoing Russia-Ukraine War significantly impacts the global sustainability consulting services market. It has profoundly affected global economic growth and labor markets, intensifying inflationary pressures and causing significant supply chain disruptions. The war has disrupted supply chains, especially for materials and goods vital to sustainability projects. Notably, nickel and palladium, essential for electric vehicle batteries, have faced significant supply chain challenges.

Sustainability Consulting Services Market Trends

Climate Change Consultancy Services Type Holds Major Market Share

- Climate change consultancy services considered under the scope include Carbon Footprint and Mitigation Analysis, Alternative Energy Development and Energy Efficiency, Climate Adaptation and Strategy, Emergency Management, Carbon Offset/Net Zero Services, Environmental Regulatory Compliance Services, Waste Management and Circularity, and Other Services.

- The increasing demand for climate change consultancy services is driven by businesses and organizations seeking expert advice on reducing environmental impact, lowering carbon footprints, adapting to climate change, managing risks, ensuring regulatory compliance, and implementing sustainable practices.

- Across the globe, businesses are grappling with the repercussions of climate change. As a result, managing climate-related risks, such as physical, transitional, or liability-based, has become paramount for firms eager to maintain their competitive edge and thrive in the emerging Net Zero paradigm. This evolving landscape has spurred a heightened demand for various consultancy services centered on climate change, aiding businesses in navigating these complexities.

- According to the 2024 report on GHG emissions from all world countries, published by 'The Emissions Database for Global Atmospheric Research/Joint Research Centre (EDGAR/JRC)'' global greenhouse gas (GHG) emissions hit a record high in 2023, reaching 52.96 billion metric tons of carbon dioxide equivalent (Gt CO2e), marking a two percent year-over-year increase.

- Moreover, companies that take the initiative in confronting climate change issues bolster their reputation and position themselves as leaders in sustainability. Such a proactive stance can translate into a significant competitive advantage, drawing in customers, top talent, and valuable partnerships.

- Vendors in the sustainability consulting market are acquiring climate change consulting firms. This strategy aims to broaden their service offerings, bolster their market presence, and cater to the rising demand for climate change consultancy services.

- For instance, in June 2024, ERM, a sustainability advisory firm, announced its agreement to acquire Energetics, a climate risk and energy transition consultancy based in Australia. This move aims to bolster ERM's growth in the Asia Pacific region. Energetics specializes in tailored services, such as crafting climate resiliency strategies, offering insights on climate risks and renewable energy transitions, guiding companies towards net-zero goals, and monitoring power purchase agreements (PPAs) for renewable energy transactions. ERM asserts that this acquisition will bolster its capacity to provide clients with both strategic advice and hands-on implementation across Australia and the broader Asia Pacific region.

- Overall, climate change consultancy services are expected to hold the largest share of the global sustainability consulting market. As businesses and organizations become more aware of climate impacts, face regulatory pressures to reduce their carbon footprints, and witness a global surge in climate action initiatives, there's a rising demand for climate change consultancy services. This demand is further fueled by businesses seeking a competitive edge through proactive climate change risk management.

Asia Pacific to Register Major Growth

- Diverse regulatory frameworks and swift industrialization shape the sustainability consulting market in the Asia-Pacific region. The region's expansion is largely fueled by heightened government regulations on environmental standards, especially in energy-intensive sectors such as manufacturing, oil and gas, and construction. In response, sustainability consulting firms in the Asia-Pacific help businesses meet compliance targets, adopt green strategies, and weave sustainable practices into their operations.

- Countries like China and India, witnessing rapid urbanization and industrialization, face environmental degradation. This has led their governments to enforce stricter environmental standards. In this context, sustainability consulting firms play a pivotal role, guiding companies to craft business models that harmonize growth with environmental stewardship, all while ensuring adherence to both national and international sustainability benchmarks.

- For instance, driven by rising urbanization and its national "Dual Carbon" targets-aiming for peak carbon emissions by 2030 and full carbon neutrality by 2060-China is intensifying its efforts to green its building and construction sector. Government data reveals that in 2020, a significant 77% of China's new urban construction projects were classified as green buildings.

- In October 2023, Shanghai unveiled a three-year initiative aimed at bolstering the ESG capabilities of foreign businesses in the city. Thereby, the plan encourages companies to ramp up Research and Development investments and embrace digital, green, and low-carbon technologies, enhancing their innovation and competitiveness, and heightening the demand for sustainability consulting solutions.

- In the Asia-Pacific region, companies are increasingly adopting ESG principles to draw in global investors and bolster their brand reputation. Sustainability consulting firms assist these businesses by pinpointing areas for enhancement, executing ESG strategies, and gearing up for international sustainability reporting standards.

Sustainability Consulting Services Market Overview

The sustainability consulting services market is characterized by a diverse mix of both established and emerging players. Some of the major players in the market are Accenture PLC, The Boston Consulting Group, Inc., Tata Consultancy Services Limited, Capgemini SE, and Roland Berger GmbH, among others.

Moderate exit barriers in the market incentivize new entrants while allowing established firms to exit during low-profit periods. Leading industry players are increasingly focusing on integrated solutions to attract customers. In contrast, smaller and newer market entrants are expected to adopt cost-benefit strategies to vie with their larger counterparts, intensifying competition.

Furthermore, a notable surge in joint ventures and acquisitions recently underscores the global business community's heightened emphasis on sustainability. As a result, competitive rivalry in the global sustainability market remains pronounced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Focus on the Reduction of Carbon Footprint and Fulfilment of Net Zero Targets

- 5.1.2 National Goals Across the Globe to Combat Climate Change

- 5.2 Market Challenges

- 5.2.1 Lower Levels of Adoption with Large Gaps in the Realistic Scenario

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Climate Change Consultancy Services

- 6.1.2 Green Building Consultancy Services

- 6.1.3 ESG Consultancy Services

- 6.1.4 Other Sustainability Consultancy Services

- 6.2 By End User

- 6.2.1 Construction and Real Estate

- 6.2.2 Energy and Power

- 6.2.3 Public Sector

- 6.2.4 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Benelux

- 6.3.2.4 Spain

- 6.3.2.5 France

- 6.3.2.6 Nordics

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 The Boston Consulting Group, Inc.

- 7.1.3 Tata Consultancy Services Limited

- 7.1.4 Capgemini SE

- 7.1.5 Roland Berger GmbH

- 7.1.6 Bain & Company, Inc.

- 7.1.7 KPMG International Limited

- 7.1.8 Ernst & Young Global Limited

- 7.1.9 Deloitte Touche Tohmatsu Limited

- 7.1.10 PricewaterhouseCoopers LLP

- 7.1.11 McKinsey & Company

- 7.1.12 Kearney

- 7.1.13 Godrej & Boyce Mfg. Co. Ltd (Godrej Industries Limited)

- 7.1.14 RPS Group (Tetra Tech Inc.)

- 7.1.15 SEA Energy

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

2025年全球保险咨询服务市场报告2025年全球房地产咨询服务市场报告2025年全球精算咨询服务市场报告

2025年全球保险咨询服务市场报告2025年全球房地产咨询服务市场报告2025年全球精算咨询服务市场报告 企业敏捷转型服务市场:依服务类型、部署模式、产业垂直领域、组织规模、调查方法、转型阶段和参与模式划分-全球预测,2025-2032年咨询 4.0 市场按产品类型、应用、最终用户、分销管道和技术划分 - 全球预测 2025-20322025年全球公司秘书服务市场报告2025年金融服务咨询全球市场报告2025年全球IT咨询市场报告2025年全球企业敏捷转型服务市场报告2025年全球设计、研究、推广与咨询服务市场报告

企业敏捷转型服务市场:依服务类型、部署模式、产业垂直领域、组织规模、调查方法、转型阶段和参与模式划分-全球预测,2025-2032年咨询 4.0 市场按产品类型、应用、最终用户、分销管道和技术划分 - 全球预测 2025-20322025年全球公司秘书服务市场报告2025年金融服务咨询全球市场报告2025年全球IT咨询市场报告2025年全球企业敏捷转型服务市场报告2025年全球设计、研究、推广与咨询服务市场报告