|

市场调查报告书

商品编码

1836428

汽车引擎:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Automotive Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

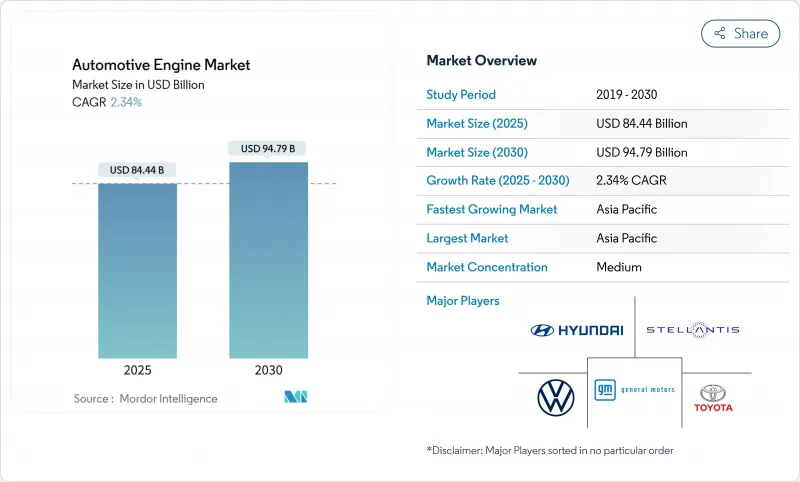

预计 2025 年汽车引擎市场价值将达到 844.4 亿美元,到 2030 年预计将达到 947.9 亿美元,复合年增长率为 2.34%。

这一稳健的发展轨迹表明,汽车引擎市场正在适应更严格的排放法规,同时透过更清洁的燃烧、混合整合和选择性采用替代燃料来维持规模。亚太地区引领需求与生产,氢燃料内燃机试验计画加速推进,合成电子燃料的出现则是为了对冲电气化的不确定性。随着纯电动车销量的扩大,汽车製造商正在透过架构分散风险、提高热效率并与能源供应商合作,以扩大汽车引擎市场的相关性。供应链的弹性,尤其是稀土和后处理基板,正成为一个关键的差异化因素,因为製造商正努力在竞争日益激烈但又分散的市场中维持净利率。

全球汽车引擎市场趋势与洞察

更严格的全球排放气体法规加速了效率的提高

与欧盟6相比,欧7法规将允许的氮氧化物排放量降低了35%,并引入了新的煞车和轮胎颗粒物限值,要求使用更大的触媒转换器、电加热后后处理装置和可变压缩燃烧策略。北美和亚太地区的主要市场正在实施类似的措施,从而推动全球动力传动系统标准化。可变气门正时、米勒循环校准和低温燃烧正在从高端配置转向基准配置。由此带来的效率提升,以及与可再生燃料混合后,可以帮助缩小电池电力传动系统的碳排放差距。总之,这些法规确保合规性,同时又不放弃液体燃料,从而增强了汽车引擎市场。

亚太新兴经济体汽车产量不断成长

2023年4月至2024年3月,乘用车、商用车、三轮车、两轮车和四轮车的总合达28,434,742辆。具有竞争力的人事费用、有利的产业政策以及日益壮大的中阶的需求,正在形成一个自我强化的生产循环。即使在成熟经济体电气化加速发展的背景下,这一势头也支撑着区域车型的内燃机投资,从而支撑了汽车引擎市场的成长。

纯电动车的快速普及将使研发预算从内燃机汽车转移

到2024年,纯电动车的销量将在几个主要市场超过新车销量,这将吸引工程人才和资本转向软体和电力电子领域。内燃机专案的更新周期将缩短,预算也将减少,即使电动车的效率不断提高,技术差距仍有可能进一步扩大。面对订单量的下降,一级供应商可能会加速工厂向电气化零件的转型,这将对剩余的内燃机生产带来成本压力,并给汽车引擎市场带来压力。

报告中分析的其他驱动因素和限制因素

- 电商物流推动轻型商用车需求

- 合成电子燃料延长内燃机寿命

- 零排放都市区区域抑制内燃机汽车销售

細項分析

凭藉成熟的模具和封装优势,直列式引擎布局将在 2024 年占据 45.12% 的汽车引擎市场份额,继续成为大众乘用车的首选结构。对置活塞引擎的复合年增长率为 4.48%,原型机的热效率实现了两位数的提升,且运动部件更少。在研引擎的功率现已超过 1,000 匹马力,同时降低了油耗和排放气体。商业和国防领域日益增长的兴趣表明,该结构很可能在 2020 年代后期实现大规模应用。 V 型配置在高端 SUV 和重型卡车中保持份额,因为功率密度可以抵消复杂性。平头引擎继续用于小批量跑车和越野车,因为其重心较低。

对创新布局的需求标誌着整个产业正转向无需完全电气化即可实现高效运作的架构。因此,汽车引擎市场正在支援多样化的工程蓝图,以降低单一技术风险,并实现动力传动系统总成组合的区域最佳化。

由于无处不在的加油网路和持续的燃烧系统升级,汽油在2024年将维持60.84%的市场份额。氢燃料内燃机将成为成长最快的细分市场,到2030年,其复合年增长率将达到13.42%。现场测试表明,氢燃料的二氧化碳排放量接近零,引擎可靠性也相当可靠。国家对绿色氢气生产的补贴,加上其适用于重型卡车的作业循环,已使其在商业性上站稳了脚跟。虽然柴油仍然是远距货运的主要燃料,但更严格的氮氧化物排放法规将提高系统成本,从而为天然气和氢气创造公平的竞争环境。

天然气燃气引擎仍然受到拥有加油站加油选项的车队用户的青睐,而支援电燃料的引擎则为原始设备製造商提供了一种无需更改设计即可满足合规要求的途径。这种燃料多样化使汽车引擎市场能够灵活应对基础设施和政策的快速变化。

汽车引擎市场报告按安装类型(直列、V型、W型、水平对置/水平对置、其他)、燃料类型(汽油、柴油、天然气/压缩天然气、其他)、车辆类型(乘用车、轻型商用车、其他)、发动机排气量(1.5公升以下、1.5-3升、其他)和地区细分。市场预测以金额(美元)和数量(单位)提供。

区域分析

亚太地区占全球销售额的41.66%,复合年增长率达3.06%,是其他地区中最高的。中国持续扩大出口,印度力争提升全球排名,东南亚则正在实现供应多元化,印尼和马来西亚的产量不断增加。成本优势、支持性政策框架以及家庭收入的不断增长,正在增强该地区内燃机(ICE)的生产。

由于更换週期、商用车更新换代以及多引擎汽车生产使工厂保持繁忙,北美将维持2.1%的复合年增长率。关税风险和资金筹措成本上升限制了成长,但内燃机汽车仍占总产量的90%以上。汽车製造商正在规划灵活的生产线,以满足未来十年混合驱动系统的需求。

欧洲将经历1.8%的复合年增长率,这反映了最严格的法规环境、不断上涨的能源成本以及疫情后的缓慢復苏。然而,该地区拥有主要的内燃机研发中心,专注于超低排放气体和可相容电燃料的发动机,这些发动机在满足合规要求的同时,还能保住国内就业机会。

总体而言,区域细分显示汽车引擎市场正在以不同的速度发展,平衡成熟市场对电气化的需求与新兴市场对成熟的燃烧动力的需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 更严格的全球排放法规推动内燃机效率提升

- 亚太新兴国家汽车产量不断成长

- 电商物流推动轻型商用车引擎需求成长

- 合成电子燃料延长内燃机的生命週期

- 48V微混合动力系统增强与内燃机的联繫

- 中重型卡车氢燃料内燃机试运行

- 市场限制

- 纯电动车的快速普及分散了研发预算

- 零排放都市区区域抑制内燃机汽车销售

- 关键合金短缺推高引擎成本

- OTA主导电力电子价值转变

- 价值/供应链分析

- 监管状况

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模与成长预测(价值,十亿美元)

- 按展示位置类型

- 排队

- V型

- W型

- 平角裤/平底鞋

- 对置活塞

- 按燃料类型

- 汽油

- 柴油引擎

- 天然气/压缩天然气

- 混合动力 ICE(轻度、全混合动力、插电式)

- 替代燃料(乙醇、液化石油气、电子燃料)

- 氢动力内燃机

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中大型商用车

- 摩托车和强力运动

- 越野/农业/建筑

- 按引擎排气量

- 1.5升或更少

- 1.5~3 L

- 3公升以上

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Toyota Motor Corporation

- Volkswagen AG

- Hyundai Motor Group

- General Motors

- Stellantis NV

- Ford Motor Company

- Mercedes-Benz Group AG

- BMW AG

- Honda Motor Co., Ltd.

- Nissan Motor Co., Ltd.

- Cummins Inc.

- Volvo Group

- Tata Motors Limited

- Scania AB

- Caterpillar Inc.

第七章 市场机会与未来展望

The automotive engine market is valued at USD 84.44 billion in 2025 and is forecast to climb to USD 94.79 billion in 2030, expanding at a 2.34% CAGR.

This measured trajectory shows that the automotive engine market is adapting to stricter emission rules while retaining scale through cleaner combustion, hybrid integration, and selective deployment of alternative fuels. Asia-Pacific leads demand and production, hydrogen internal-combustion pilots are gathering pace, and synthetic e-fuels are emerging to hedge against electrification uncertainty. Automakers are spreading risk across architectures, improving thermal efficiency, and partnering with energy suppliers to extend the relevance of the automotive engine market amid growing battery-electric sales. Supply-chain resilience, especially for rare earths and after-treatment substrates, is becoming a critical differentiator as manufacturers aim to hold margins in a competitive yet fragmented landscape.

Global Automotive Engine Market Trends and Insights

Stricter Global Emission Rules Accelerate Efficiency Upgrades

Euro 7 limits cut permissible NOx by 35% versus Euro 6 and introduce fresh particulate caps for brakes and tires, prompting bigger catalytic converters, electrically heated after-treaters, and variable-compression combustion strategies. Similar measures in North America and key Asia-Pacific markets are forcing global power-train standardization, which helps scale next-gen components. Variable valve timing, Miller-cycle calibrations, and low-temperature combustion are shifting from premium options to baseline fitments. The resulting efficiency gains narrow the carbon gap with battery-electric drivetrains when renewable fuels are blended. Altogether, these regulations reinforce the automotive engine market by ensuring compliance without abandoning liquid fuels.

Rising Vehicle Production in Emerging Asia-Pacific Economies

From April 2023 to March 2024, the combined production of Passenger Vehicles, Commercial Vehicles, Three-Wheelers, Two-Wheelers, and Quadricycles reached 28,434,742 units. Competitive labor costs, supportive industrial policies, and expanding middle-class demand create a self-reinforcing production loop. Such momentum sustains internal-combustion investment for regional models even as electrification accelerates in mature economies, thereby underpinning growth in the automotive engine market.

Rapid BEV Adoption Diverts R&D Budgets from ICE

Battery-electric volumes topped new-car sales in several major markets during 2024, pulling engineering talent and capital toward software and power electronics. Internal-combustion programs face shorter refresh cycles and leaner budgets, which risks widening a technology gap against ever-improving EV efficiency. Tier-one suppliers confronted with smaller order volumes may accelerate factory retooling toward electrified components, placing cost pressure on remaining ICE output and weighing on the automotive engine market.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Logistics Boosts Light-Commercial-Vehicle Demand

- Synthetic E-fuels Extend the Combustion Engine Lifecycle

- Zero-Emission Urban Zones Curb ICE Sales

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Due to established tooling and packaging advantages, the in-line layout secured 45.12% of 2024 revenue in the automotive engine market and remains the preferred architecture for mass-market passenger cars. Opposed-piston units are expanding at a 4.48% CAGR; prototypes demonstrate double-digit thermal-efficiency gains and fewer moving parts. Research engines now exceed 1,000 hp while cutting fuel use and emissions. Growing interest from commercial and defence segments suggests a viable pathway to volume adoption in the late 2020s. V-type configurations hold share in premium SUVs and heavy-duty trucks, where power density offsets complexity. Flat engines continue in low-volume sports and off-road vehicles that benefit from a low centre of gravity.

Demand for innovative layouts signals a wider industry pivot toward architectures that deliver efficiency without full electrification. The automotive engine market, therefore, supports diversified engineering roadmaps, mitigating single-technology risk and allowing regional optimisation of power-train portfolios.

Gasoline retained 60.84% share in 2024, bolstered by ubiquitous refuelling networks and continuous combustion-system upgrades. Hydrogen internal-combustion variants are the fastest-growing segment with a 13.42% CAGR through 2030; field tests demonstrate near-zero CO2 alongside familiar engine reliability. National subsidies for green-hydrogen production, combined with heavy-truck duty-cycle suitability, create an early commercial beachhead. Diesel still dominates long-haul freight, yet tightening NOx caps raise system cost, levelling the field for gas and hydrogen.

Natural-gas engines maintain relevance for fleet users with depot refuelling, whereas e-fuel-ready engines give OEMs a route to compliance without redesign. This fuel diversification keeps the automotive engine market resilient against rapid shifts in infrastructure and policy.

The Automotive Engine Market Report is Segmented by Placement Type (In-Line, V-Type, W-Type, Boxer / Flat, and More), Fuel Type (Gasoline, Diesel, Natural Gas / CNG, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Engine Capacity (Below 1. 5 L, 1. 5 To 3 L, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific holds 41.66% of global turnover and posts a 3.06% CAGR that outpaces every other region. China continues to scale exports, India aspires to top world rankings, and Southeast Asia diversifies supply with Indonesia and Malaysia stepping up output. Cost advantages, supportive policy frameworks, and rising household incomes reinforce regional ICE production.

North America sustains a 2.1% CAGR as replacement cycles, commercial-fleet renewal, and multipropulsion manufacturing keep plants busy. Tariff risks and elevated financing costs curb upside, but ICE still commands more than 90% of output today. Automakers plan flexible lines to serve mixed propulsion demand into the next decade.

Europe records a 1.8% CAGR, reflecting the toughest regulatory climate, higher energy costs, and slower post-pandemic recovery. The bloc nevertheless hosts leading combustion R&D centres focused on ultra-low emission and e-fuel-ready engines that enable compliance while retaining domestic employment.

Overall, geography segmentation shows that the automotive engine market evolves at different speeds, balancing mature-market electrification with developing-market demand for proven combustion power.

- Toyota Motor Corporation

- Volkswagen AG

- Hyundai Motor Group

- General Motors

- Stellantis N.V.

- Ford Motor Company

- Mercedes-Benz Group AG

- BMW AG

- Honda Motor Co., Ltd.

- Nissan Motor Co., Ltd.

- Cummins Inc.

- Volvo Group

- Tata Motors Limited

- Scania AB

- Caterpillar Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter global emission regulations driving ICE efficiency upgrades

- 4.2.2 Rising vehicle production in emerging Asia-Pacific economies

- 4.2.3 E-commerce logistics boosting LCV engine demand

- 4.2.4 Emergence of synthetic e-fuels extending ICE lifecycle

- 4.2.5 48-V micro-hybrid systems reinforcing ICE relevance

- 4.2.6 Hydrogen-fueled ICE pilots for medium & heavy trucks

- 4.3 Market Restraints

- 4.3.1 Rapid BEV adoption diverting R&D budgets

- 4.3.2 Zero-emission urban zones curbing ICE sales

- 4.3.3 Critical alloy shortages inflating engine costs

- 4.3.4 OTA-driven value shift toward power electronics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Bn)

- 5.1 By Placement Type

- 5.1.1 In-line

- 5.1.2 V-type

- 5.1.3 W-type

- 5.1.4 Boxer / Flat

- 5.1.5 Opposed-piston

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 Natural Gas / CNG

- 5.2.4 Hybrid-ICE (Mild, Full, Plug-in)

- 5.2.5 Alternative Fuels (Ethanol, LPG, e-Fuels)

- 5.2.6 Hydrogen ICE

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Two-Wheelers and Powersports

- 5.3.5 Off-road / Agricultural / Construction

- 5.4 By Engine Capacity

- 5.4.1 Below 1.5 L

- 5.4.2 1.5 to 3 L

- 5.4.3 Over 3 L

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of the Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Toyota Motor Corporation

- 6.4.2 Volkswagen AG

- 6.4.3 Hyundai Motor Group

- 6.4.4 General Motors

- 6.4.5 Stellantis N.V.

- 6.4.6 Ford Motor Company

- 6.4.7 Mercedes-Benz Group AG

- 6.4.8 BMW AG

- 6.4.9 Honda Motor Co., Ltd.

- 6.4.10 Nissan Motor Co., Ltd.

- 6.4.11 Cummins Inc.

- 6.4.12 Volvo Group

- 6.4.13 Tata Motors Limited

- 6.4.14 Scania AB

- 6.4.15 Caterpillar Inc.