|

市场调查报告书

商品编码

1836498

交通号誌识别:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Traffic Signal Recognition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

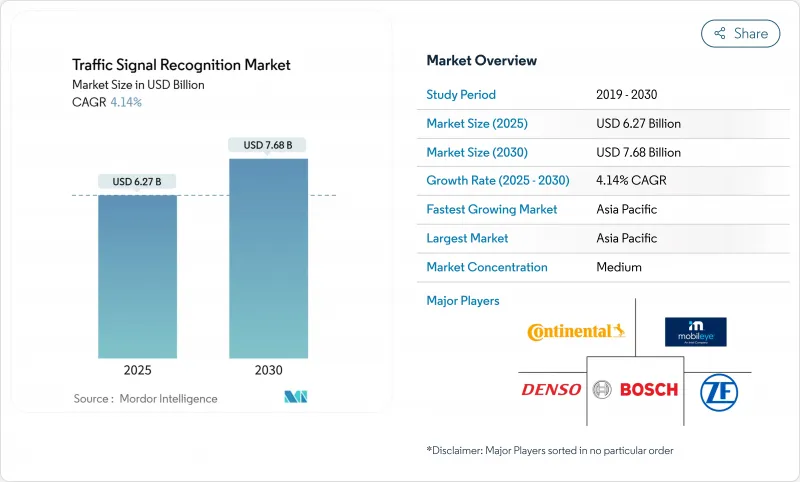

交通号誌辨识市场预计在 2025 年价值 62.7 亿美元,预计到 2030 年将达到 76.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.14%。

监管规定、摄影机价格下降以及 Level 2 Plus 自动驾驶技术正在将目标市场拓展至高阶车型之外。原厂配套量如今为感测器供应商提供了必要的规模经济效益,使其能够将摄影机成本控制在至关重要的 10 美元阈值以下。同时,软体的增强功能正在提升识别准确性,这将有助于保险远端资讯处理评分和未来的自动驾驶汽车认证。

全球交通号誌识别市场趋势与洞察

ADAS的监理整合

具有约束力的法规已将交通号誌侦测从选购附加功能转变为必备安全功能。欧盟《通用安全法规 II》(2024 年 7 月生效)要求所有新车型必须配备由交通号誌输入支援的智慧限速援助,而美国国家公路交通安全管理局 (NHTSA) 关于自动紧急煞车的规定则推动了对感知套件的需求。 OEM 厂商目前正在围绕可扩展感知能力构建电气系统,以应对未来的规则制定,从而有效地锁定了交通号誌识别市场多年的需求。

相机成本曲线降至每台 10 美元以下

影像感测器终于克服了曾经阻碍大众市场车辆采用先进视觉技术的成本障碍。SONY的车用CMOS蓝图和安森美半导体的3µm像素製程已将HDR提升至120 dB,并将暗电流降低了28倍,同时将单价降至10美元以下。更低的价格使OEM厂商能够在每辆车上部署八个或更多摄像头,从而提供更多观点,从而提高在眩光、背光和LED闪烁场景下的识别精度。

极端天气下能见度差、知觉力差

雪、雾和暴雨持续影响摄影机性能,导致影像品质下降,损害了公众的信任。像 Snow-CLOC(冬季检测准确率高达 86.61%)这样的实验室成功案例尚未转化为统一的道路行驶性能,这促使开发人员转向雷射雷达与摄影机融合和热感迭加技术。可靠性方面的差距给监管机构带来了沉重的负担,他们要求在推进免提驾驶立法之前,必须明确定义性能范围。

报告中分析的其他驱动因素和限制因素

- 2级以上自动驾驶的普及

- 支援 V2I 的动态标誌更新

- 各国资料集检验成本

細項分析

到2024年,基于颜色的检测将占交通号誌识别市场收益的46.18%,证明了RGB阈值的长期应用。然而,到2030年,深度学习侦测的复合年增长率将达到4.71%,因为卷积网路和变压器网路在遮蔽和光照变化条件下表现出色。预计到2030年,深度学习侦测的交通号誌辨识市场规模将呈指数级增长,这反映了OEM厂商对可透过软体升级的精度提升的偏好。

YOLOv5 和基于注意力机制的网路目前实现了超过 95% 的准确率和超过 98% 的召回率,同时推理时间保持在 45 毫秒以内,满足即时安全预算。随着无线传输管道的成熟,汽车製造商将能够使用边缘影像重新训练模型,并在无需更换硬体的情况下推送更新。交通号誌辨识市场正持续向以 AI 为中心的技术堆迭转型,其差异化在于资料管理而非电路设计。

2024年,摄影机系统将占交通号誌辨识市场收益的63.21%,这得益于系统效率和功能的提升,这得益于BOM成本的降低以及先进软体工具的整合。这一主导地位凸显了摄影机系统在交通号誌辨识应用中的日益普及。儘管成长率有所放缓,但预计到2030年,在技术持续进步的推动下,交通号誌辨识摄影机系统的市场规模将以强劲的复合年增长率飙升。

光达与摄影机融合是成长最快的细分市场,复合年增长率高达 4.34%,禾赛等供应商计划降价50%,以将固态单元纳入主流车型。 SparseLIF 和类似框架将点云几何与影像纹理对齐,从而创造冗余,即使在眩光或降水遮挡摄影机的情况下也能保持识别。雷达辅助选项增加了速度向量来预测相位变化,这反映了多感测器融合如何再形成交通号誌辨识市场。

区域分析

预计到2024年,亚太地区将占据交通号誌辨识市场最大的收入份额,达到38.75%,到2030年,复合年增长率将达到4.21%。国内法规、智慧城市试点和垂直整合正在推动中国、日本和韩国交通号誌识别市场的集中度。深圳的V2I走廊为测试车辆提供即时相位图,而东京的感测器产业则为全球原始设备製造商提供HDR成像仪。该地区的高密度交通创造了多样化的数据集,增强了深度学习的稳健性,并加快了全球检验週期。

欧洲受通用安全法规II的驱动。大陆集团新成立的Aumovio部门和博世的感测器融合套件正在支援供应,而严格的网路安全规则正在塑造资料处理架构。德国和英国的保险远端资讯处理系统因合规而获得奖励,这推动了消费者对交通号誌识别的需求。

北美正受益于联邦安全法规和新创企业自动驾驶测试。在加州,严格的法规要求供应商记录故障安全性能,而加拿大的冬季气候则为恶劣天气测试提供了天然的试验场。这些因素共同造就了一个多元化但又相互连结的地区,一个地区的进步可以透过遍布全球的原始设备製造商计画迅速传播到其他地区。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- ADAS 的监管吸收

- 相机成本曲线低于 10 美元/台

- 2级以上自动驾驶的普及

- 使用 V2I 进行动态标誌更新

- 高清地图数位双胞胎构建

- 保险远距资讯处理奖励TSR准确性

- 市场限制

- 极端天气条件下能见度差和能见度低

- 特定国家/地区的资料检验成本

- 虚假标籤的网路责任

- OEM 预算转向竞争性感测器

- 价值/供应链分析

- 监管状况

- 技术展望

- 五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模与成长预测:价值(美元)

- 依检测方法

- 基于颜色的检测

- 基于形状的检测

- 特征/深度学习检测

- 透过感测器技术

- 网路摄影系统

- 雷达辅助TSR

- LiDAR 与摄影机融合

- 多模态

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中大型商用车

- 公车和长途客车

- 按组件

- 硬体

- 软体

- 按最终用户

- OEM安装

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Mobileye(Intel)

- ZF Friedrichshafen AG

- HELLA(FORVIA)

- Aptiv PLC

- Valeo SA

- Magna International Inc.

- Panasonic Holdings

- Hyundai Mobis

- Hitachi Astemo

- Veoneer/S-SW

- Ford Motor Company

- General Motors Company

- Tesla Inc.

- NVIDIA Corporation

第七章 市场机会与未来展望

The Traffic Signal Recognition Market size is estimated at USD 6.27 billion in 2025, and is expected to reach USD 7.68 billion by 2030, at a CAGR of 4.14% during the forecast period (2025-2030).

Regulatory mandates, lower camera prices, and Level-2 Plus autonomy expand the addressable base beyond premium models. Original-equipment volumes now give sensor suppliers the economies of scale needed to hold camera costs below the pivotal USD 10 threshold. At the same time, software enhancements sharpen recognition accuracy that feeds insurance telematics scoring and future autonomous-vehicle certification.

Global Traffic Signal Recognition Market Trends and Insights

Regulation-Mandated ADAS Inclusion

Binding rules have turned traffic light detection from an optional extra into a required safety feature. The European Union's General Safety Regulation II, effective July 2024, obliges every new model to include intelligent speed assistance underpinned by traffic-signal inputs, while a parallel NHTSA rule on automatic emergency braking heightens demand for perception suites. OEMs now architect their electrical systems around scalable perception capacity that anticipates future rule-making, effectively locking in multi-year demand for the traffic signal recognition market.

Camera Cost Curve Drops Below USD 10/Unit

Imaging sensors finally cleared the cost hurdle that once kept advanced vision off mass-market vehicles. Sony's automotive CMOS roadmap and onsemi's 3 µm pixel process have driven unit prices beneath USD 10 while boosting HDR to 120 dB and cutting dark current by 28 times. Low prices let OEMs deploy eight or more cameras per vehicle, multiplying viewpoints that collectively raise recognition precision across glare, back-light, and LED-flicker scenarios.

Poor Recognition in Low-Visibility and Weather Eextremes

Snow, fog, and heavy rain still challenge cameras, creating service drops that undermine public trust. Laboratory gains such as Snow-CLOCs (86.61% detection accuracy in winter) have yet to translate into uniform street performance, pushing developers toward LiDAR-camera fusion and thermal overlays. Reliability gaps weigh on regulators who demand clearly defined performance envelopes before advancing hands-free legislation.

Other drivers and restraints analyzed in the detailed report include:

- Level-2 Plus Autonomy Proliferation

- V2I-Enabled Dynamic Sign Updates

- Country-Specific Dataset Validation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Color-based Detection held 46.18% of the traffic signal recognition market revenue in 2024, a testament to its long-standing use of RGB thresholds. Yet Deep-Learning Detection is rising at 4.71% CAGR to 2030 as convolutional and transformer networks prove superior under occlusion and variable lighting. The traffic signal recognition market size for Deep-Learning Detection is projected to grow exponentially by 2030, reflecting OEM preferences for software-upgradable accuracy gains.

YOLOv5 and attention-based networks now achieve more than 95% precision and over 98% recall while keeping inference below 45 ms, meeting real-time safety budgets. As over-the-air pipelines mature, automakers can retrain models on edge-case footage and push updates without hardware swaps. The traffic signal recognition market continues transitioning toward AI-centric stacks where differentiators sit in data curation, not circuit design.

In 2024, Camera Systems captured 63.21% of the traffic signal recognition market revenue, driven by declining BOM costs and the integration of advanced software tooling, which enhanced system efficiency and functionality. This dominance highlights the growing adoption of Camera Systems in traffic signal recognition applications. Despite a moderation in growth rates, the market size for Camera Systems in traffic signal recognition is projected to surge at a strong CAGR through 2030, supported by continuous technological advancements.

LiDAR-Camera Fusion is the fastest-advancing sub-segment at 4.34% CAGR as suppliers like Hesai plan 50% price cuts that place solid-state units within mainstream trims. SparseLIF and similar frameworks align point-cloud geometry with image texture, producing redundancy that sustains recognition when glare or precipitation blinds cameras. Radar-assisted options add speed vectors that predict phase changes, illustrating how multi-sensor blending reshapes the traffic signal recognition market.

The Traffic Signal Recognition Market Report is Segmented by Detection Method (Color-Based Detection, Shape-Based Detection, and Feature-Based Detection), Sensor Technology (Camera Systems, Radar-Assisted TSR, and More), Vehicle Type (Passenger Cars and More), Component (Hardware and Software), End-User (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 38.75% of the traffic signal recognition market revenue share in 2024 and is expected to grow at a 4.21% CAGR through 2030. Domestic regulations, smart-city pilots, and vertical integration concentrate the traffic signal recognition market in China, Japan, and South Korea. Shenzhen's V2I corridors feed real-time phase maps to test fleets, while Tokyo's sensor industry supplies HDR imagers to global OEMs. Regional high-density traffic creates diverse datasets that sharpen deep-learning robustness and accelerate global validation cycles.

Europe follows, propelled by General Safety Regulation II. Continental's new Aumovio division and Bosch's sensor-fusion suites anchor supply, while stringent cybersecurity rules shape data-handling architectures. Insurance telematics in Germany and the United Kingdom reward verified compliance, channeling consumer demand into the traffic signal recognition market.

North America benefits from federal safety mandates and venture-backed autonomy pilots. California's edge-case legal scrutiny pushes suppliers to document fail-safe performance, while Canada's winter climate provides natural laboratories for adverse-weather testing. Together, these factors sustain a diversified yet interconnected geography where advances in one region ripple quickly to others through globally distributed OEM programs.

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Mobileye (Intel)

- ZF Friedrichshafen AG

- HELLA (FORVIA)

- Aptiv PLC

- Valeo SA

- Magna International Inc.

- Panasonic Holdings

- Hyundai Mobis

- Hitachi Astemo

- Veoneer / S-SW

- Ford Motor Company

- General Motors Company

- Tesla Inc.

- NVIDIA Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulation-mandated ADAS inclusion

- 4.2.2 Camera Cost Curve Drops Below USD10/unit

- 4.2.3 Level-2 Plus Autonomy Proliferation

- 4.2.4 V2I-Enabled Dynamic Sign Updates

- 4.2.5 HD-Map Digital-Twin Build-Outs

- 4.2.6 Insurance Telematics Rewarding TSR Accuracy

- 4.3 Market Restraints

- 4.3.1 Poor Recognition in Low-Visibility and Weather Extremes

- 4.3.2 Country-Specific Dataset Validation Costs

- 4.3.3 Cyber-Liability For Erroneous Sign Display

- 4.3.4 OEM Budget Shift to Competing Sensor Priorities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Detection Method

- 5.1.1 Color-based Detection

- 5.1.2 Shape-based Detection

- 5.1.3 Feature / Deep-Learning Detection

- 5.2 By Sensor Technology

- 5.2.1 Camera Systems

- 5.2.2 Radar-Assisted TSR

- 5.2.3 LiDAR-Camera Fusion

- 5.2.4 Multi-modal

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Buses and Coaches

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.2 Software

- 5.5 By End-User

- 5.5.1 OEM-installed

- 5.5.2 Aftermarket Retrofit

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 DENSO Corporation

- 6.4.4 Mobileye (Intel)

- 6.4.5 ZF Friedrichshafen AG

- 6.4.6 HELLA (FORVIA)

- 6.4.7 Aptiv PLC

- 6.4.8 Valeo SA

- 6.4.9 Magna International Inc.

- 6.4.10 Panasonic Holdings

- 6.4.11 Hyundai Mobis

- 6.4.12 Hitachi Astemo

- 6.4.13 Veoneer / S-SW

- 6.4.14 Ford Motor Company

- 6.4.15 General Motors Company

- 6.4.16 Tesla Inc.

- 6.4.17 NVIDIA Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

深度学习晶片组市场(按设备类型、部署模式、最终用户和应用)—全球预测,2025-2032

深度学习晶片组市场(按设备类型、部署模式、最终用户和应用)—全球预测,2025-2032 2025年深度学习全球市场报告

2025年深度学习全球市场报告 全球资料中心处理器市场

全球资料中心处理器市场 深度学习市场:按组件、应用、最终用户和地区划分

深度学习市场:按组件、应用、最终用户和地区划分 2025 年至 2033 年深度学习市场规模、份额、趋势及预测(依产品类型、应用、最终用途产业、架构及地区)

2025 年至 2033 年深度学习市场规模、份额、趋势及预测(依产品类型、应用、最终用途产业、架构及地区) 交通号誌辨识市场规模、份额、成长分析(按组件、按车辆类型、按技术、按应用、按地区)- 产业预测,2025 年至 2032 年

交通号誌辨识市场规模、份额、成长分析(按组件、按车辆类型、按技术、按应用、按地区)- 产业预测,2025 年至 2032 年 深度学习晶片组市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032)

深度学习晶片组市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032) 深度学习:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)日本深度学习市场报告(按产品类型、应用、最终用途产业、架构和地区)2025-2033深度造假技术市场(按组件、按技术、按地区)

深度学习:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)日本深度学习市场报告(按产品类型、应用、最终用途产业、架构和地区)2025-2033深度造假技术市场(按组件、按技术、按地区)