|

市场调查报告书

商品编码

1836515

人工草皮:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Artificial Turf - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

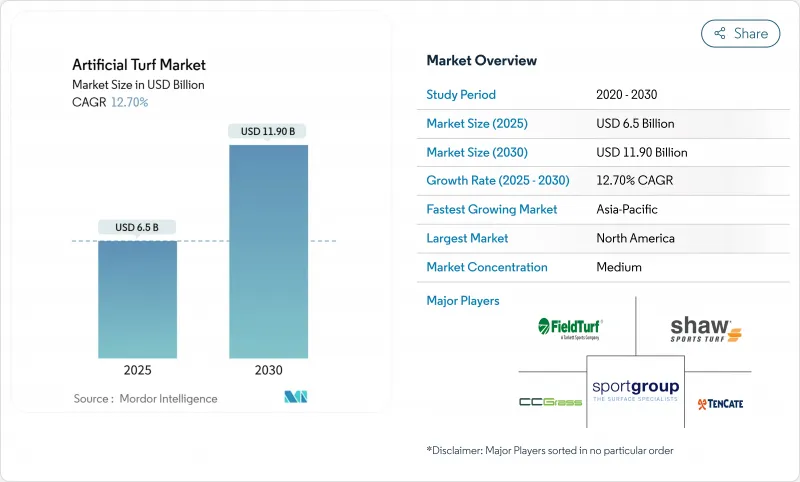

预计人工草皮草坪市场规模到 2025 年将达到 65 亿美元,到 2030 年将达到 119 亿美元,复合年增长率为 12.7%。

干旱风险上升和强制性节水法正将需求从体育场馆转向住宅、商业和民用基础设施。 Tarkett(FieldTurf)和TenCate Grass等全球领导者凭藉大规模挤出能力和早期回收计划捍卫市场份额,而Shaw Sports Turf、CCGrass和越来越多的区域专家则利用接近性和定价灵活性来赢得与市政当局和学校的合约。目前的创新集中在低热纤维化学品、不含PFAS的配方和闭合迴路回收伙伴关係关係上,以应对日益严格的欧盟微塑胶法规和北美生产者延伸责任提案。买家越来越多地评估供应商的报废解决方案和经过验证的冷却性能,即使整体市场继续分散,他们仍向技术所有者提供溢价。

全球人工草皮市场趋势与洞察

严格节水义务

加州的AB 1572法案和科罗拉多的SB 24-005法案禁止使用非功能性草坪进行饮用水灌溉,并禁止新安装非功能性草坪。这些加速的计划不仅给安装商带来了巨大的压力,还加速了人工草皮草坪的更换週期,实际上将人工草皮市场锁定在公共日程表而非球队赛季预算中。亚利桑那州、内华达州和澳洲部分地区的地方政府已开始起草类似的法令,以保护日益减少的含水层。

扩及综合体育场馆

精英场馆对场地的要求越来越高,需要在紧凑的赛程内举办足球、橄榄球和音乐会。梅赛德斯-奔驰体育场2025年的FieldTurf CORE安装项目和SoFi体育场2026年世界杯的混合草坪试点项目,透过大型合约展示了下一代系统的潜力。这些升级的规格将在两到三个竞标週期内过渡到大学和二级设施,使每个旗舰计划的收益翻倍。

审视微塑胶和奈米塑胶污染

欧洲化学品管理局估计,运动场每年排放1.6万吨微塑料,加速了欧洲大陆逐步淘汰橡胶颗粒的进程。製造商将不得不重新设计填充物,并寻找聚合物黏合或植物来源替代品,这将导致系统成本增加8%至12%。科学研究证实,奈米塑胶纤维会因机械磨损而脱落,这强化了实施更严格规格限制和扩大生产者责任计画的论点。

报告中分析的其他驱动因素和限制因素

- 住宅和商业景观美化需求飙升

- 城市热岛气候调适计划

- 初始安装成本高

細項分析

2024年,体育用品将占据人工草皮市场的42.7%,其中专业和大学场地的更换週期为8-10年。接触性运动、曲棍球、网球和棒球场正在寻求能够优化球滚动和衝击衰减的纤维配方,以增强高端产品线,即使在树脂成本上涨的情况下也能保持利润率。

升级产品包括热反射颜料和缝合标籤,用于记录维护数据以进行保固检验。同时,随着地方政府重视抗旱工作,该市场将超过任何其他体育细分市场,到2030年复合年增长率将达到15.3%。商业设施正在采用宽卷产品以消除接缝,而运动场则指定使用符合ASTM F1292跌落高度标准的垫片。

区域分析

北美38.2%的份额凸显了更换週期的规律性和锁定基准需求的监管压力。加州禁止饮用水用于非功能性草坪;科罗拉多也禁止种植草坪,导致合规计划即时,但时间安排灵活性有限。墨西哥的市立公园更倾向于使用人造草坪,以控制水费上涨,并在气温升高的情况下延长运动时间。

亚太地区将迎来最快的成长,到2030年复合年增长率将达到14.4%,这得益于中国和印度的体育场建设,以及澳洲缩短供应链的製造业规模。该地区的货运优势支撑着东南亚地区的出口,而日本人口密集的城市地区则是调温布料的试验田。在韩国,政府补助抵消了学校体育场的前期成本,加速了其在小学教育机构的应用。

欧洲的环境法规日益复杂。欧洲禁止使用颗粒填充材料,迫使俱乐部转向聚合物黏合弹性体或矿物填充材料,虽然提高了系统价格,但也延长了使用寿命。温布利球场的零废弃物回收测试展示了法甲俱乐部正在评估的2026年球场维修的循环模板。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 严格节水义务

- 将安装范围扩大到综合体育场馆

- 住宅和商业景观美化需求激增

- 城市热岛气候调适计划

- 采用自主铺设草皮机器人

- 草皮回收/EPR计划

- 市场限制

- 对微塑胶和奈米塑胶污染的担忧

- 初期实施成本高

- 欧盟禁止使用橡胶颗粒填充物

- 球员面临热应激诉讼的风险

- 监管状况

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模与成长预测(价值,美元)

- 按用途

- 运动的

- 接触性运动

- 曲棍球

- 网球

- 其他运动

- 休閒

- 景观

- 运动的

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 其他亚太地区

- 中东

- 沙乌地阿拉伯

- 其他中东地区

- 非洲

- 南非

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Tarkett(FieldTurf)

- TenCate Grass(Leonard Green & Partners, LP)

- Shaw Sports Turf

- CCGrass

- Sports Group(Polytan)

- Act Global(Beaulieu International Group)

- SprinTurf(Integrated Turf Solutions LLC)

- ForeverLawn

- SIS Pitches

- Victoria PLC

- Global Syn-Turf

- Lano Sports(Lano Carpets NV)

- Watershed Geo

第七章 市场机会与未来展望

The artificial turf market is valued at USD 6.5 billion in 2025 and is forecast to reach USD 11.9 billion by 2030, registering a 12.7% CAGR.

Heightened drought risk and mandatory water-conservation laws are shifting demand beyond sports venues into residential, commercial, and civic infrastructure. Competitive intensity remains moderate; global leaders such as Tarkett (FieldTurf) and TenCate Grass defend their share through large-scale extrusion capacity and early-stage recycling programs, while Shaw Sports Turf, CCGrass, and a growing cadre of regional specialists leverage proximity and price agility to win municipal and school contracts. Innovation now centers on low-heat fiber chemistries, PFAS-free formulations, and closed-loop recycling partnerships that address tightening EU microplastics rules and North American extended-producer-responsibility proposals. Buyers increasingly evaluate suppliers on end-of-life solutions and verified cooling performance, giving technology owners a pricing premium even as overall market fragmentation persists.

Global Artificial Turf Market Trends and Insights

Stringent Water-Conservation Mandates

California's AB 1572 and Colorado's SB 24-005 remove potable-water irrigation from nonfunctional lawns and ban new nonfunctional turf, converting discretionary upgrades into compliance obligations. Accelerated timelines strain installer capacity and pull forward replacement cycles, effectively anchoring the artificial turf market to public-policy calendars rather than team-season budgets. Municipalities in Arizona, Nevada, and parts of Australia have begun drafting parallel ordinances to safeguard dwindling aquifers.

Expanding Installation in Multi-Sport Stadia

Elite venues increasingly demand fields that can host football, soccer, and concerts within compressed scheduling windows. Mercedes-Benz Stadium's 2025 FieldTurf CORE installation and SoFi Stadium's hybrid turf pilot for the 2026 World Cup illustrate the visibility that large contracts create for next-generation systems. These specification uplifts migrate to collegiate and secondary facilities within two to three bid cycles, multiplying the revenue influence of each flagship project.

Micro- and Nano-Plastic Pollution Scrutiny

The European Chemicals Agency estimates sports pitches contribute 16,000 tons of microplastics annually, accelerating momentum for a continent-wide crumb-rubber phase-out Manufacturers must redesign infill containment and explore polymer-bound or plant-based alternatives, raising system costs by 8%-12%. Scientific studies have now confirmed nano-plastic fiber shedding under mechanical wear, strengthening arguments for tighter specification limits and extended producer responsibility schemes.

Other drivers and restraints analyzed in the detailed report include:

- Surging Residential and Commercial Landscaping Demand

- Urban Heat-Island Climate-Resilience Projects

- High Upfront Installation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sports accounted for a 42.7% slice of the artificial turf market in 2024, anchoring recurring eight- to ten-year replacement cycles across professional and collegiate venues. Contact Sports, hockey, tennis and baseball fields pursue fiber blends that optimize ball roll and shock attenuation, reinforcing a premium tier that shields margins even when resin costs climb.

Upgrades now include heat-reflective pigments and stitched labels that log maintenance data for warranty validation. Meanwhile, the landscape cohort is advancing at a 15.3% CAGR to 2030, outpacing every sports sub-segment as municipalities pivot toward drought resilience. Commercial complexes adopt wide-roll products to cut seam labor, while playgrounds specify underlay pads that meet ASTM F1292 fall-height criteria.

The Artificial Turf Market is Segmented by Usage (Sports, Leisure, and Landscape) and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 38.2% stake underscores replacement-cycle regularity and regulatory pressure that lock in baseline demand. California's potable-water ban for nonfunctional lawns and Colorado's turf-planting moratorium create immediate compliance projects with limited scheduling flexibility. Mexico's municipal parks favor synthetics to curb rising water bills and extend play hours despite temperature spikes.

Asia-Pacific delivers the fastest growth at 14.4% CAGR through 2030, propelled by stadium construction in China and India, plus an Australian manufacturing scale that shortens supply chains. The region's freight advantage supports exports across Southeast Asia, while Japan's dense urban zones provide test beds for heat-mitigating fibers. Government grants in South Korea offset upfront costs for school pitches, accelerating penetration in primary education facilities.

Europe wrestles with environmental regulation complexity. The European ban on particulate infill forces clubs to transition to polymer-bound elastomers or mineral options, lifting system prices, but also extending service life. Wembley Stadium's zero-landfill pitch-recycling trial showcases a circular template that French Ligue 1 clubs are now evaluating for 2026 renovations.

- Tarkett (FieldTurf)

- TenCate Grass (Leonard Green & Partners, L.P.)

- Shaw Sports Turf

- CCGrass

- Sports Group (Polytan)

- Act Global (Beaulieu International Group)

- SprinTurf (Integrated Turf Solutions LLC)

- ForeverLawn

- SIS Pitches

- Victoria PLC

- Global Syn-Turf

- Lano Sports (Lano Carpets NV)

- Watershed Geo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent water-conservation mandates

- 4.2.2 Expanding installation in multi-sport stadia

- 4.2.3 Surging residential and commercial landscaping demand

- 4.2.4 Urban-heat-island climate resilience projects

- 4.2.5 Adoption of autonomous turf-laying robots

- 4.2.6 Circular turf recycling/EPR programs

- 4.3 Market Restraints

- 4.3.1 Micro and nano-plastic pollution scrutiny

- 4.3.2 High upfront installation cost

- 4.3.3 European Union ban on crumb-rubber infill

- 4.3.4 Player heat-stress litigation risk

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat from Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Usage

- 5.1.1 Sports

- 5.1.1.1 Contact Sports

- 5.1.1.2 Field Hockey

- 5.1.1.3 Tennis

- 5.1.1.4 Other Sports

- 5.1.2 Leisure

- 5.1.3 Landscape

- 5.1.1 Sports

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of Noth America

- 5.2.2 South America

- 5.2.2.1 Brazil

- 5.2.2.2 Argentina

- 5.2.2.3 Rest of South America

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 Russia

- 5.2.3.7 Rest of Europe

- 5.2.4 Asia-Pacific

- 5.2.4.1 China

- 5.2.4.2 Japan

- 5.2.4.3 India

- 5.2.4.4 Australia

- 5.2.4.5 Rest of Asia-Pacific

- 5.2.5 Middle East

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Rest of Middle East

- 5.2.6 Africa

- 5.2.6.1 South Africa

- 5.2.6.2 Rest of Africa

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tarkett (FieldTurf)

- 6.4.2 TenCate Grass (Leonard Green & Partners, L.P.)

- 6.4.3 Shaw Sports Turf

- 6.4.4 CCGrass

- 6.4.5 Sports Group (Polytan)

- 6.4.6 Act Global (Beaulieu International Group)

- 6.4.7 SprinTurf (Integrated Turf Solutions LLC)

- 6.4.8 ForeverLawn

- 6.4.9 SIS Pitches

- 6.4.10 Victoria PLC

- 6.4.11 Global Syn-Turf

- 6.4.12 Lano Sports (Lano Carpets NV)

- 6.4.13 Watershed Geo

7 Market Opportunities and Future Outlook

足球场人工草皮市场:按最终用户、纱线材料、填充物类型、安装类型、草丝高度和背衬材料划分,全球预测,2026-2032年

足球场人工草皮市场:按最终用户、纱线材料、填充物类型、安装类型、草丝高度和背衬材料划分,全球预测,2026-2032年 人工草皮市场报告:按材料、应用、通路和地区划分,2026-2034年日本人工草皮市场报告:按材料、应用、通路和地区划分(2026-2034年)

人工草皮市场报告:按材料、应用、通路和地区划分,2026-2034年日本人工草皮市场报告:按材料、应用、通路和地区划分(2026-2034年) 2026年全球人工草皮草坪市场报告

2026年全球人工草皮草坪市场报告 人工草皮市场-全球产业规模、份额、趋势、机会及预测(按材料、应用、填充材、分销管道、地区和竞争格局划分,2021-2031年)高尔夫球场人工草皮市场:2026-2032年全球预测(按产品类型、球场类型、安装类型、应用和销售管道)人工草皮市场(按纤维材料、填充材、安装类型、应用、最终用户和分销管道)—2025-2032 年全球预测

人工草皮市场-全球产业规模、份额、趋势、机会及预测(按材料、应用、填充材、分销管道、地区和竞争格局划分,2021-2031年)高尔夫球场人工草皮市场:2026-2032年全球预测(按产品类型、球场类型、安装类型、应用和销售管道)人工草皮市场(按纤维材料、填充材、安装类型、应用、最终用户和分销管道)—2025-2032 年全球预测 全球人工草皮运动草坪市场

全球人工草皮运动草坪市场 人工草皮市场:产业趋势·全球预测 (~2035年):用途·材料·适用地区·安装类型·企业规模·主要各地区全球人工草皮市场:2034 年的市场机会与策略

人工草皮市场:产业趋势·全球预测 (~2035年):用途·材料·适用地区·安装类型·企业规模·主要各地区全球人工草皮市场:2034 年的市场机会与策略