|

市场调查报告书

商品编码

1836548

地工合成材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Geosynthetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

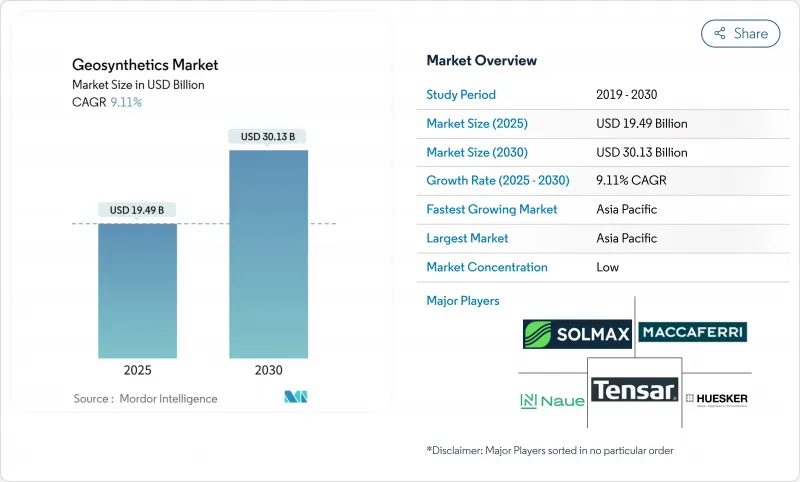

预计 2025 年地工合成材料市场规模为 194.9 亿美元,到 2030 年将达到 301.3 亿美元,预测期间(2025-2030 年)的复合年增长率为 9.11%。

成长取决于五种力量的汇聚。亚太、北美和中东的基础设施项目正在采用土工合成作为路基、挡土墙和海岸防御工事的解决方案。美国、欧盟和日本的监管机构正在强制执行更严格的遏制和过滤标准,这些标准更倾向于地工止水膜和地工织物,而不是传统材料。智慧材料的持续研发正在整合感测器和再生聚合物,以延长使用寿命并实现即时状态监测。农业和采矿业是新兴的终端用户,它们被新型地工格网和脱水管的侵蚀控制和尾矿管理优势所吸引。同时,原材料波动和不断变化的欧洲微塑胶法规正在降低短期盈利,但也刺激了可生物降解和可回收投入的创新。

全球地工合成材料市场趋势与洞察

地工织物在建设产业的应用不断扩大

道路、桥樑和地基计划的需求正在推动地工合成材料市场的发展,因为承包商可以用地工织物布加固材料取代厚骨材层,从而在保持结构承载力的同时将材料成本降低高达30%。美国联邦公路管理局目前根据「建设美国,购买美国」条款将大多数地工合成材料材料归类为建筑材料,该条款将自2025年3月起强制要求在联邦援助计画中采购国内产品。城市开发商也越来越多地选择地工合成材料用于绿色屋顶,而薄膜和排水复合材料可将雨水径流和冷却负荷降低高达50%。这些变化加在一起,将在2024年推动该领域的应用份额达到38%,从而保持该行业的长期发展势头。

地工织物在采矿活动中的使用日益增多

尾矿仓储设施营运商正在安装复合式衬垫、地工格网和脱水管,以符合尾矿管理的全球行业标准,降低液化风险并提高安全记录。 Husker公司已为矿山运输道路和废弃物堆部署了专用加固和过滤系统,其澳洲业务的使用寿命显着延长。随着金属需求的激增,地工合成材料的产业应用正在促进采矿业收益的成长,推动整体复合年增长率达到0.3%。

聚丙烯价格波动

聚丙烯和高密度聚乙烯价格波动推高了生产成本,并挤压了整个地工合成材料市场的利润空间。生产商正在尝试对消费后塑胶进行化学回收,以规避原材料风险并减少碳足迹。巴西石化公司(Braskem)在巴西的13.9万吨产能扩张计画预计在2026年前缓解拉丁美洲的供应紧张。

报告中分析的其他驱动因素和限制因素

- 严格的环境保护法规结构

- 增加农业用途

- 欧洲新推出的微塑胶法规

細項分析

聚丙烯、聚乙烯和聚酯合计将占2024年总收入的94%,预计到2030年,其整体复合年增长率将达到9.1%,凸显了它们的性价比优势。这类合成纤维拥有久经考验的抗拉强度、耐化学性和供应充足性——这些指标支撑了它们在地工合成材料市场的领先地位。在严格的美国通讯协定下,高密度聚苯乙烯地工止水膜仍是危险废弃物处理池和堆浸垫片的首选衬垫。

企业永续性的不断加强,正在推动天然纤维和可生物降解聚合物的研究。儘管该领域目前的市场份额仅为个位数,但欧盟对微塑胶的监管压力正在加速植物来源地工格网和聚乳酸(PLA)混合不织布的现场试验。使用香蒲(Typha domingensis)製成的纤维格栅进行的示范试验表明,它们符合侵蚀控制设计要求,同时在作物週期内完全可生物降解。如果这些创新得到大规模检验,地工合成材料市场中的生态材料部分可望从2028年起实现两位数的成长率。

预计地工止水膜将在 2024 年占据 35% 的市场份额,成为收入的主导,超过地工合成材料市场中的其他产品类型,到 2030 年的复合年增长率为 10.27%。垃圾掩埋盖板的最初应用已扩展到需要接近零渗透性的 PFAS 围堵池、厌氧舄湖和浮体式覆盖水库计划。

地工织物仍然是过滤和加固领域的主要材料。然而,随着监管部门对纤维损耗的严格审查,以及材料替代的不断增加,其成长正在放缓。地工复合物和衬垫(将排水芯与地工织物或膜结合在一起)因其轻薄的外形和多功能性而日益受到青睐,对那些寻求减少开挖量和温室气体排放的承包商来说极具吸引力。这些动态表明,在预测期内,地工合成材料的市场份额将逐渐转移到多功能工程系统。

区域分析

随着公共部门计划与私人工业的合併,到2024年,亚太地区将占全球总收入的45%,复合年增长率达9.99%。中国的「一带一路」走廊将推动高铁路堤防和沙漠公路用地工止水膜的大量订单。印度的「智慧城市计画」将鼓励地方政府掩埋改造和将地工织物嵌入混凝土护岸的运河建设合约。日本和韩国正在推动抗震挡土墙的研发,将地工合成材料材料加强与轻型路堤相结合,增强了对土工膜抗震性能的需求。

受美国基础设施现代化计画的推动,北美终端用户使用量持续成长。日本国土交通省要求在国内采购建筑材料,这推动了联邦公路、陆军工程兵团防洪计划以及机场跑道扩建计画的采用。加拿大油砂产业的尾矿坝维修和墨西哥的跨洋走廊建设也将成为进一步的成长点。

欧洲严格的循环经济政策维持了现有的采用率,但在生产者适应微塑胶限制措施的同时,短期产量成长受到限制。德国、法国和英国青睐符合报废回收标准的优质地工止水膜和地工复合物。在斯堪地那维亚的基础设施领域,创新公司正在试用可生物降解的衬垫,这预示着未来地工合成材料市场份额将向环保认证产品转变。

南美、中东和非洲的贡献虽小,但战略需求正在成长。巴西Mineracao的扩张正在推动矾土残渣计划中地工合成材料的使用,而沙乌地阿拉伯的NEOM和红海旅游计划则指定使用地工格网来稳定海岸。用于集水坝和沙漠公路网络的地工格网融资正在支撑这些新兴地区的稳定需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 地工织物在建设产业的应用不断扩大

- 采矿业中地工织物的使用日益增多

- 严格的环境保护法规结构

- 增加农业用途

- 材料工程的技术进步

- 市场限制

- 聚丙烯价格波动

- 欧洲微塑胶法规日益严格,或将限制传统地工织物的使用

- 产品标准化问题

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模及成长预测(金额)

- 按材质

- 聚丙烯、聚乙烯、聚酯

- 其他的

- 按类型

- 地工织物

- 地工止水膜

- 地工复合物

- 土工合成衬垫等

- 按功能

- 分离

- 引流

- 加强

- 过滤

- 防潮层

- 按用途

- 建筑学

- 运输

- 环境

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ACE Geosynthetics

- Agru America Inc.

- Belton Industries

- Berry Global Inc.

- Bonar Plastics

- Carthage Mills

- Contech Engineered Solutions LLC

- Dow

- Freudenberg Group

- Geo-Synthetics Systems LLC(GSI)

- Hanes Geo Components

- Huesker International

- KayTech

- Minerals Technologies Inc.

- Naue GmbH & Co. KG

- Officine Maccaferri SpA

- Presto Products Company

- SKAPS Industries

- Solmax

- Strata Systems Inc.

- Taian Modern Plastic Co., Ltd

- TENAX SPA

- Tensar, A Division of CMC

- Tessilbrenta SpA

第七章 市场机会与未来展望

The Geosynthetics Market size is estimated at USD 19.49 billion in 2025, and is expected to reach USD 30.13 billion by 2030, at a CAGR of 9.11% during the forecast period (2025-2030).

Growth rests on five converging forces. Infrastructure programmes in Asia Pacific, North America, and the Middle East are embedding geosynthetic solutions in roadbeds, retaining walls, and coastal defences because the materials cut aggregate demand and accelerate build schedules. Regulatory bodies in the United States, the European Union, and Japan are mandating stricter containment and filtration standards that favour geomembranes and geotextiles over conventional options. 1 Ongoing R&D in smart materials integrates sensors and recycled polymers to extend service life and enable real-time condition monitoring. Agriculture and mining are emerging end-users, drawn by the erosion-control and tailings-management benefits achieved with newer geogrids and dewatering tubes. Meanwhile, raw-material volatility and evolving European microplastic rules are tempering near-term profitability but also stimulating innovation toward biodegradable or recycled inputs.

Global Geosynthetics Market Trends and Insights

Growing Usage of Geotextiles in Construction Industry

Demand from road, bridge, and foundation projects is elevating the geosynthetics market as contractors replace thicker aggregate layers with geotextile reinforcement that preserves structural capacity while trimming up to 30% of material costs. The U.S. Federal Highway Administration now classifies most geosynthetics as construction materials under the Build America Buy America provisions, triggering mandatory domestic sourcing on federal-aid schemes from March 2025. Urban developers are also selecting geosynthetics for green roofs, where membranes and drainage composites cut stormwater runoff and drop cooling loads by up to 50%. Collectively, these changes underpin a 38% application share in 2024 and sustain long-term momentum for the segment.

Increase Usage of Geotextiles in Mining Activities

Operators of tailings storage facilities are installing composite liners, geogrids, and dewatering tubes to comply with the Global Industry Standards for Tailings Management, thereby reducing liquefaction risks and improving safety records. HUESKER has rolled out purpose-built reinforcement and filtration systems for mine haul roads and waste piles, demonstrating service life gains in Australian operations. As metals demand surges, industry uptake of geosynthetics helps mining account for a growing revenue slice and delivers a 0.3% uplift to the overall CAGR.

Volatile Polypropylene Pricing

Price swings in polypropylene and HDPE inflate production costs and compress margins across the geosynthetics market. Producers are trialling chemical recycling of used plastics to hedge raw-material risk and lower carbon footprints. Braskem's 139,000-ton capacity expansion in Brazil may ease supply tightness in Latin America by 2026.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Regulatory Framework for Environmental Protection

- Increased Agricultural Applications

- Emerging Europe Micro-plastic Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene, polyethylene and polyester together represented 94% of 2024 revenue and should mirror the overall 9.1% CAGR toward 2030, underscoring their cost-to-performance advantage. This synthetic cohort enjoys well-documented tensile strength, chemical resistance and supply availability, indicators that underpin its leadership in the geosynthetics market. High-density polyethylene geomembranes remain the preferred liner for hazardous-waste cells and heap leach pads under strict EPA protocols epa.gov.

Rising corporate sustainability commitments are propelling natural-fiber and biodegradable polymer research. Though the segment currently secures a single-digit share, EU regulatory pressure on microplastics is accelerating field trials of plant-based geogrids and PLA-blended nonwovens. Demonstrations with Typha domingensis fibre grids revealed break strengths that satisfy erosion-control design values while allowing full biodegradation within a cropping cycle. If validated at scale, these innovations could grow the eco-material slice of the geosynthetics market size at double-digit rates after 2028.

Geomembranes led 2024 turnover with a 35% share and are positioned to register a 10.27% CAGR to 2030, outperforming other product categories in the geosynthetics market. Early adoption in landfill caps has expanded to PFAS containment basins, anaerobic lagoons, and floating-cover reservoir projects that demand near-zero permeability.

Geotextiles remain a large-volume workhorse for filtration and reinforcement. Yet growth is slower as regulatory scrutiny on fibre loss intensifies, spurring material substitutions. Geocomposites and liners that pair drainage cores with geotextiles or membranes are picking up velocity because they combine multiple functions in a thinner profile, appealing to contractors chasing lower excavation volumes and reduced greenhouse-gas footprints. These dynamics imply a gradual redistribution of geosynthetics market share toward multifunctional engineered systems through the forecast window.

The Geosynthetics Market Report Segments the Industry by Material (Polypropylene, Polyethylene, and Polyester, and Others), Type (Geotextile, Geomembrane, Geocomposite, and More), Function (Separation, Drainage, Reinforcement, and More), Application (Construction, Transportation, Environmental, and Other Applications) and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia Pacific held 45% of 2024 revenue and will expand at a 9.99% CAGR as public-sector megaprojects converge with private industrial parks. China's Belt and Road corridors drive bulk orders for geomembranes in high-speed rail embankments and desert expressways. India's Smart Cities Mission catalyses municipal landfill upgrades and canal-lining contracts that embed geotextiles in concrete revetments. Japan and South Korea channel R&D into earthquake-resistant retaining walls that combine geosynthetic reinforcement with lightweight fills, reinforcing demand resilience.

North America continues to consolidate end-user uptake, led by the United States' infrastructure modernisation package. DOT mandates for domestic sourcing of construction materials elevate adoption throughout federal highways, Army Corps flood-control projects and airport runway extensions. Canada's tailings-dam upgrades in the oil-sand sector and Mexico's inter-oceanic corridor represent additional growth nodes.

Europe's stringent circular-economy policies sustain existing penetration yet temper short-term volume gains while producers adapt to microplastic caps. Germany, France and the United Kingdom favour premium geomembranes and geocomposites that meet end-of-life recyclability criteria. Innovators trial biodegradable liners in Scandinavian infrastructure, signalling future shifts in geosynthetics market share toward eco-certified products.

South America and the Middle East & Africa contribute smaller but increasingly strategic volumes. Brazil's Mineracao expansion spurs geosynthetic containment in bauxite residue disposal, whereas Saudi Arabia's NEOM and Red Sea tourism projects specify geogrids for coastal stabilisation. Multilateral financing for water-harvesting dams and desert road networks underpins a steady demand trajectory across these emerging territories.

- ACE Geosynthetics

- Agru America Inc.

- Belton Industries

- Berry Global Inc.

- Bonar Plastics

- Carthage Mills

- Contech Engineered Solutions LLC

- Dow

- Freudenberg Group

- Geo-Synthetics Systems LLC (GSI)

- Hanes Geo Components

- Huesker International

- KayTech

- Minerals Technologies Inc.

- Naue GmbH & Co. KG

- Officine Maccaferri SpA

- Presto Products Company

- SKAPS Industries

- Solmax

- Strata Systems Inc.

- Taian Modern Plastic Co., Ltd

- TENAX SPA

- Tensar, A Division of CMC

- Tessilbrenta S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Usage of Geotextiles in Construction Industry

- 4.2.2 Increase Usage of Geotextiles in Mining Activities

- 4.2.3 Stringent Regulatory Framework for Environmental Protection

- 4.2.4 Increased Agricultural Applications

- 4.2.5 Technological Advancements in Material Engineering

- 4.3 Market Restraints

- 4.3.1 Volatile Polypropylene Pricing

- 4.3.2 Emerging Europe Micro-plastic Rules Potentially Restricting Conventional Geotextiles

- 4.3.3 Product Standardization Issues

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polypropylene, Polyethylene, and Polyester

- 5.1.2 Others

- 5.2 By Type

- 5.2.1 Geotextile

- 5.2.2 Geomembrane

- 5.2.3 Geocomposite

- 5.2.4 Geosynthetic Liner and Others

- 5.3 By Function

- 5.3.1 Separation

- 5.3.2 Drainage

- 5.3.3 Reinforcement

- 5.3.4 Filtration

- 5.3.5 Moisture Barrier

- 5.4 By Application

- 5.4.1 Construction

- 5.4.2 Transportation

- 5.4.3 Environmental

- 5.4.4 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ACE Geosynthetics

- 6.4.2 Agru America Inc.

- 6.4.3 Belton Industries

- 6.4.4 Berry Global Inc.

- 6.4.5 Bonar Plastics

- 6.4.6 Carthage Mills

- 6.4.7 Contech Engineered Solutions LLC

- 6.4.8 Dow

- 6.4.9 Freudenberg Group

- 6.4.10 Geo-Synthetics Systems LLC (GSI)

- 6.4.11 Hanes Geo Components

- 6.4.12 Huesker International

- 6.4.13 KayTech

- 6.4.14 Minerals Technologies Inc.

- 6.4.15 Naue GmbH & Co. KG

- 6.4.16 Officine Maccaferri SpA

- 6.4.17 Presto Products Company

- 6.4.18 SKAPS Industries

- 6.4.19 Solmax

- 6.4.20 Strata Systems Inc.

- 6.4.21 Taian Modern Plastic Co., Ltd

- 6.4.22 TENAX SPA

- 6.4.23 Tensar, A Division of CMC

- 6.4.24 Tessilbrenta S.p.A.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Expected Increase in Usage Green Roof and Green Wall Construction

土工合成黏土衬垫市场:按应用、产品类型、最终用途和分销管道划分-2025-2032年全球预测地工合成材料市场依产品、应用、材料、最终用途产业、通路、施工类型及安装方式划分-全球预测,2025-2032年

土工合成黏土衬垫市场:按应用、产品类型、最终用途和分销管道划分-2025-2032年全球预测地工合成材料市场依产品、应用、材料、最终用途产业、通路、施工类型及安装方式划分-全球预测,2025-2032年 地工合成物全球市场报告(2025年)

地工合成物全球市场报告(2025年) 地工合成材料,全球市场 2025-2029

地工合成材料,全球市场 2025-2029 日本土工合成材料市场报告(按产品(土工布、土工膜、土工格栅、土工网、土工合成粘土衬垫、预製垂直排水管等)、类型、材料、应用和地区划分,2025 年至 2033 年)

日本土工合成材料市场报告(按产品(土工布、土工膜、土工格栅、土工网、土工合成粘土衬垫、预製垂直排水管等)、类型、材料、应用和地区划分,2025 年至 2033 年) 2026 年至 2032 年地工合成材料市场规模(依产品类型、应用、最终用户产业和地区划分)

2026 年至 2032 年地工合成材料市场规模(依产品类型、应用、最终用户产业和地区划分) 地工合成材料市场报告:2031 年趋势、预测与竞争分析

地工合成材料市场报告:2031 年趋势、预测与竞争分析 土工合成材料市场 - 全球产业规模、份额、趋势、机会和预测,按材料、类型、功能、应用、地区、竞争进行细分,2020-2030F土工合成材料市场报告按产品(土工织物、土工膜、土工格栅、土工网、土工合成粘土衬垫、预製垂直排水沟等)、类型、材料、应用和地区 2025-2033

土工合成材料市场 - 全球产业规模、份额、趋势、机会和预测,按材料、类型、功能、应用、地区、竞争进行细分,2020-2030F土工合成材料市场报告按产品(土工织物、土工膜、土工格栅、土工网、土工合成粘土衬垫、预製垂直排水沟等)、类型、材料、应用和地区 2025-2033 土工合成黏土衬垫市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年

土工合成黏土衬垫市场规模、份额、趋势分析报告:按应用、地区、细分市场、预测,2025-2030 年