|

市场调查报告书

商品编码

1836623

细菌生物防治剂:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Bacterial Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

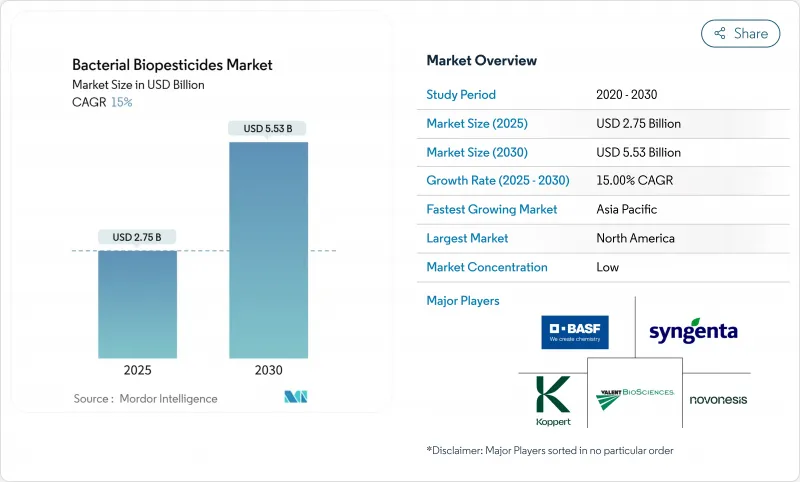

细菌生物农药市场规模预计在 2025 年达到 27.5 亿美元,预计到 2030 年将达到 55.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 15%。

市场成长的动力来自监管部门的快速核准、消费者对无农药残留农产品日益增长的需求、有机农业的扩张以及提高製剂稳定性和田间药效的技术进步。根据 FiBL 预测,2023 年全球有机农业面积将达到 9,890 万公顷,成长 2.6%。苏力菌(Bt) 占据市场主导地位,销售额占比达 74%,而枯草芽孢桿菌则因其兼具病虫害防治和植物生长促进特性而呈现快速增长。精准种子处理应用、用于受控环境农业的液体製剂以及主要农化公司的产品组合整合正在支持市场扩张。细菌生物农药的采用率受到低温运输储存要求和与化学替代品相比药效较慢的影响,各公司正在努力在竞争日益激烈的市场中应对这些挑战。

全球细菌生物农药市场趋势与洞察

监管和政策支持

欧洲生物农药的核准流程已从九年缩短至约三年,涵盖了100多种待审批物质。欧盟委员会计划于2025年实施新的欧盟法规,以在第四季前优化生物农药的核准流程。 2026年《生物技术法案》将着重于填补当前的监管空白。巴西也取得了类似的进展,核准了一种惰性伯克氏菌细胞的生物农药产品。美国环保署(EPA)正在减少《联邦杀虫剂、杀菌剂和灭鼠剂法案》(FIFRA)下的申请积压。这些监管变化将扩大登记机会,降低合规成本,并使小型企业能够进入细菌生物农药市场。

人们越来越意识到传统农药的危害

研究表明,合成农药会导致生物多样性丧失和土壤劣化,这正在影响高端零售通路的购买决策。麻省理工学院的一项2025年研究显示,全球31%的农业土壤面临农药污染的高风险。北美和欧洲的零售商正在实施严格的残留限量,并青睐零残留生物製品。随着种植者适应这些要求,细菌已从一种仅限有机的解决方案发展成为综合虫害管理方案的重要组成部分。这种转变正在推动细菌生物农药市场的成长,尤其是对于收穫前间隔较短的作物。

低温运输物流限制生物製药的保存期限

活孢子製剂通常在25°C以上就会失去活力,需要冷藏运输和储存,增加了最终成本。这项挑战在赤道地区市场尤其明显,因为这些地区的经销网路规模较小,缺乏温控储存设施。虽然新的封装技术可以提高细胞在室温下的活力,减少分销限制,但生产规模扩大和监管审批过程需要多个培养期。这些物流限制限制了市场渗透,并使细菌生物农药的竞争力低于保质期更长、储存要求更低的化学农药。

报告中分析的其他驱动因素和限制因素

- 无农药农产品需求推动Bt解决方案

- 受控环境农业的扩展推动液体製剂的发展

- 对击倒速度慢的认知降低了农场的采用率

細項分析

Bt 将在细菌生物农药市场保持主导地位,到 2024 年将占总收益的 74%。这一市场领先地位归功于其针对鳞翅目幼虫的靶向毒性、广泛的有机认证以及全球监管核准。由于新型封装技术能够提高 Bt 产品在强紫外线条件下的田间持效性,预计 Bt 产品的市场规模将进一步扩大。 2024 年的一项研究证实了 Bt 毒素对鳞翅目、鞘翅目、半翅目、双翅目和线虫类害虫的有效性。

枯草桿菌展现出强劲的成长潜力,尤其是在高价值园艺领域,由于其具有抑制疾病和促进植物生长的双重功效,预计复合年增长率为17%。萤光假单胞菌已在控制土壤传播病原体方面确立了其作用,而沙雷氏菌和链霉菌则因其几丁质酶活性和产生抗生素代谢的能力,在特殊应用领域越来越受欢迎。

区域分析

北美将保持主导地位,到2024年将占全球销售额的38%。美国正透过在大规模玉米和大豆种植中广泛整合细菌解决方案来推动市场规模成长。加拿大的温室丛集正在透过使用与水耕施肥系统相容的液体接种剂来刺激区域需求。 2023年,加拿大920个商业温室蔬菜生产基地将生产802,163吨蔬菜,比2022年增加7%。

预计亚太地区将呈现最强劲的成长轨迹,到2030年复合年增长率将达到18%。中国的五年期绿色病虫害防治计画和印度的生物投入补贴计画将鼓励国内生产和应用。日本和新加坡的垂直农业正在为受控环境农业开发的液体製剂市场开闢新天地。

儘管欧洲对生物防治剂的监管一直很严格,但最近的变化加速了这些措施的实施。欧盟委员会的2025年快速通道法规缩短了檔案审查时间,使其与北美标准保持一致,促进了更多产品註册,并鼓励製造商扩大欧盟产品标籤的使用范围。斯堪的纳维亚半岛学校膳食的公共采购政策以及德国「从农场到餐桌」的农药减量目标,推动了对生物防治剂的需求增长,Bt和枯草叶面喷布产品尤其受益。东欧的谷物种植者已开始测试基于芽孢桿菌的种子处理剂,以应对出口市场严格的残留要求,并将应用范围扩展到传统的高价值园艺应用之外。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 法规和政策支持

- 人们越来越意识到传统农药造成的危害

- 无农药农产品需求推动Bt解决方案

- 受控环境农业的扩张将推动对液体细菌製剂的需求

- 越来越多采用综合虫害管理(IPM)策略

- 配方和输送系统的技术进步

- 市场限制

- 低温运输物流限制生物农药的保存期限

- 生产和配方挑战

- 对击倒速度慢的认知降低了农场的采用率

- 成本高于传统农药

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 依产品类型

- 苏力菌

- 枯草桿菌

- 萤光假单胞菌

- 其他类型

- 采用喷涂法

- 叶面喷布

- 种子处理

- 土壤处理

- 后处理

- 按作物类型

- 水果和蔬菜

- 谷物和谷类

- 油籽和豆类

- 草坪和观赏作物

- 种植作物

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 其他欧洲国家

- 非洲

- 南非

- 埃及

- 其他非洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 其他亚太地区

- 北美洲

第六章 竞争态势

- 策略趋势

- 市占率分析

- 公司简介

- Certis Biologicals

- Valent BioSciences

- Bayer CropScience AG

- Syngenta AG

- Corteva Agriscience

- BASF SE

- UPL Limited

- FMC Corporation

- Nufarm Limited

- Koppert Biological Systems

- Novonesis

第七章 市场机会与未来趋势

The Bacterial Biopesticides Market size is estimated at USD 2.75 billion in 2025, and is anticipated to reach USD 5.53 billion by 2030, at a CAGR of 15% during the forecast period (2025-2030).

The market growth is driven by expedited regulatory approvals, increasing consumer demand for residue-free produce, expansion of organic farming, and technological advancements that enhance formulation stability and field efficacy. According to FiBL, the global organic farming area reached 98.9 million hectares in 2023, representing a 2.6% increase. Bacillus thuringiensis (Bt) dominates the market with a 74% revenue share, while Bacillus subtilis shows rapid growth due to its combined pest control and plant growth promotion capabilities. Precision seed treatment applications, liquid formulations for controlled-environment agriculture, and the consolidation of portfolios among major agrochemical companies support the market expansion. Adoption rate of the bacterial biopesticides is affected by cold-chain storage requirements and slower efficacy compared to chemical alternatives, as companies work to address these challenges in an increasingly competitive market.

Global Bacterial Biopesticides Market Trends and Insights

Regulatory and Policy Support

The European approval process for biopesticides has reduced from nine years to approximately three years, addressing a backlog of over 100 pending substances. The European Commission intends to implement new EU regulations in 2025 to optimize biopesticide approval processes by Q4. The 2026 Biotech Act will focus on filling current regulatory gaps. Brazil has demonstrated similar progress by approving bio-insecticidal products derived from inactivated Burkholderia cells. The United States Environmental Protection Agency (EPA) is reducing application backlogs under FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act). These regulatory changes expand registration opportunities, reduce compliance costs, and enable smaller companies to enter the bacterial biopesticides market.

Rising Awareness of the Harms of Conventional Pesticides

Research demonstrating biodiversity loss and soil degradation from synthetic pesticides influences purchasing decisions in premium retail channels. A 2025 Massachusetts Institute of Technology study revealed that 31% of global agricultural soils faced high risks from pesticide contamination. North American and European retailers implement strict residue limits, favoring zero-residue biological products. As growers adapt to these requirements, bacterial agents have evolved from organic-only solutions to essential components of integrated pest management programs. This transition drives growth in the bacterial biopesticides market, especially for crops with short pre-harvest intervals.

Cold-Chain Logistics Limiting Shelf-Life of Biologicals

Live spore formulations typically lose viability at temperatures above 25°C, necessitating refrigerated transport and storage, which increases the final cost. This challenge is particularly significant in equatorial markets where small-scale distribution networks lack temperature-controlled storage facilities. While new encapsulation technologies are improving cell viability at room temperature and reducing distribution constraints, the processes for scale-up and regulatory approval require multiple growing seasons. These logistical limitations restrict market penetration, reducing the competitiveness of bacterial biopesticides against chemical pesticides that offer extended shelf life and minimal storage requirements.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Residue-Free Produce Driving Bt Solutions

- Expansion of Controlled-Environment Agriculture Boosting Liquid Formulations

- Perceived Slower Knock-Down Reducing Adoption in Farms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bt accounted for 74% of 2024 revenue, maintaining its dominant position in the bacterial biopesticides market. This market leadership stems from its targeted toxicity against lepidopteran larvae, extensive organic certifications, and regulatory acceptance worldwide. The market size for Bt products is projected to expand due to new encapsulation technologies that improve field persistence in high-UV conditions. A 2024 study confirmed Bt toxins' effectiveness against lepidopteran, coleopteran, hemipteran, dipteran, and nematode pests.

Bacillus subtilis shows strong growth potential with a projected 17% CAGR, driven by its dual benefits of disease suppression and plant growth promotion, particularly in high-value horticulture. Pseudomonas fluorescens has established its role in controlling soil-borne pathogens, while Serratia and Streptomyces species are gaining traction in specialized applications through their chitinase activity and antibiotic metabolite production capabilities.

The Bacterial Biopesticides Market Report is Segmented by Product Type (Bacillus Thuringiensis, Bacillus Subtilis, Pseudomonas Fluorescens, and Other Types), Mode of Application (Seed Treatment, Foliar Spray, and More ), Crop Type (Grains and Cereals, Oilseeds and Pulses, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained its dominant position with a 38% share of the 2024 global revenue. The United States drives market volumes through widespread integration of bacterial solutions in large-scale corn and soybean operations. Canadian greenhouse clusters strengthen regional demand by utilizing liquid inoculants compatible with hydroponic fertigation systems. In 2023, Canada's 920 commercial greenhouse vegetable operations produced 802,163 metric tons of vegetables, a 7% increase from 2022.

Asia-Pacific demonstrates the strongest growth trajectory with an anticipated 18% CAGR through 2030. China's five-year green pest-control plan and India's bio-input subsidy programs encourage domestic production and adoption. Japan and Singapore's vertical farming operations provide established markets for liquid formulations specifically developed for controlled environment agriculture.

Europe maintains strict regulations for biopesticides, though recent changes have accelerated their adoption. The European Commission's 2025 fast-track regulation reduced dossier review times to align with North American standards, enabling more product registrations and encouraging manufacturers to expand their EU product labels. The demand for biopesticides has increased through Scandinavian public procurement policies for school meals and Germany's Farm-to-Fork pesticide reduction targets, particularly benefiting Bt and B. subtilis foliar products. Eastern European grain producers have initiated Bacillus-based seed treatment trials in response to export markets' stricter residue requirements, expanding beyond traditional high-value horticultural applications.

- Certis Biologicals

- Valent BioSciences

- Bayer CropScience AG

- Syngenta AG

- Corteva Agriscience

- BASF SE

- UPL Limited

- FMC Corporation

- Nufarm Limited

- Koppert Biological Systems

- Novonesis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory and Policy Support

- 4.2.2 Rising Awareness of the Harms of Conventional Pesticides

- 4.2.3 Demand for residue-free produce driving Bt solutions

- 4.2.4 Expansion of controlled-environment agriculture boosting demand for liquid bacterial formulations

- 4.2.5 Increasing adoption of integrated pest management (IPM) strategies

- 4.2.6 Technological advancements in formulation and delivery systems

- 4.3 Market Restraints

- 4.3.1 Cold-chain logistics limiting shelf-life of Biological biopesticides

- 4.3.2 Production and Formulation Challenges

- 4.3.3 Perceived slower knock-down reducing adoption in farms

- 4.3.4 Higher costs compared to conventional pesticides

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Bargaining Power of Buyers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Bacillus thuringiensis

- 5.1.2 Bacillus subtilis

- 5.1.3 Pseudomonas fluorescens

- 5.1.4 Other Types

- 5.2 By Mode of Application

- 5.2.1 Foliar Spray

- 5.2.2 Seed Treatment

- 5.2.3 Soil Treatment

- 5.2.4 Post-Harvest Treatment

- 5.3 By Crop Type

- 5.3.1 Fruits and Vegetables

- 5.3.2 Cereals and Grains

- 5.3.3 Oilseeds and Pulses

- 5.3.4 Turf and Ornamentals

- 5.3.5 Plantation Crops

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Rest of Europe

- 5.4.4 Africa

- 5.4.4.1 South Africa

- 5.4.4.2 Egypt

- 5.4.4.3 Rest of Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Rest of Asia-Pacific

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Certis Biologicals

- 6.3.2 Valent BioSciences

- 6.3.3 Bayer CropScience AG

- 6.3.4 Syngenta AG

- 6.3.5 Corteva Agriscience

- 6.3.6 BASF SE

- 6.3.7 UPL Limited

- 6.3.8 FMC Corporation

- 6.3.9 Nufarm Limited

- 6.3.10 Koppert Biological Systems

- 6.3.11 Novonesis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球生物农药市场规模、份额、趋势和成长分析报告(2026-2034年)

全球生物农药市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球生物农药市场报告

2026年全球生物农药市场报告 生物製药市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、应用、製剂、地区和竞争格局划分,2021-2031年

生物製药市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、应用、製剂、地区和竞争格局划分,2021-2031年 农业生物农药市场按类型、作用方式、应用、作物类型和剂型划分-2026-2032年全球预测芽孢桿菌作物保护市场按作物类型、配方类型、应用方法、最终用户和销售管道划分-2026-2032年全球预测

农业生物农药市场按类型、作用方式、应用、作物类型和剂型划分-2026-2032年全球预测芽孢桿菌作物保护市场按作物类型、配方类型、应用方法、最终用户和销售管道划分-2026-2032年全球预测 生物农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

生物农药:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本生物农药市场报告(按产品类型(生物除草剂、生物杀虫剂、生物杀菌剂及其他)、应用(作物用、非作物用)和地区划分,2026-2034)

日本生物农药市场报告(按产品类型(生物除草剂、生物杀虫剂、生物杀菌剂及其他)、应用(作物用、非作物用)和地区划分,2026-2034) 全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析生物农药:主要国家天然农药市场分析生物农药市场(按类型、作物、剂型、应用和销售管道)——2025-2030 年全球预测

全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析生物农药:主要国家天然农药市场分析生物农药市场(按类型、作物、剂型、应用和销售管道)——2025-2030 年全球预测