|

市场调查报告书

商品编码

1836632

汽车离合器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Automotive Clutch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

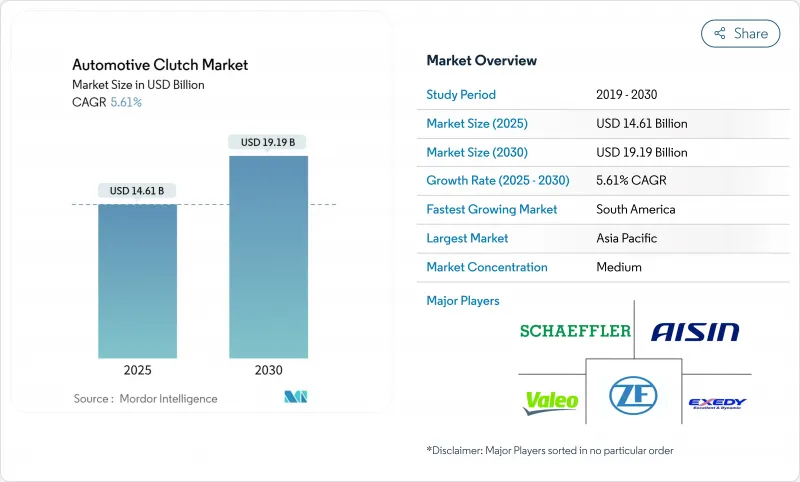

预计 2025 年汽车离合器市场价值将达到 146.1 亿美元,到 2030 年预计将达到 191.9 亿美元,复合年增长率为 5.61%。

双离合器变速箱 (DCT) 技术的普及、全球二氧化碳排放法规的收紧以及轻型汽车产量(尤其是在亚太地区)的强劲增长,为这一前景提供了支撑。由于新型车辆越来越多地将轻度混合动力系统与电子驱动相结合,从而提高换檔速度和效率,需求主要以原始设备製造商 (OEM) 层面为主。然而,由于车辆车龄超过 12 年,且纯电动车 (BEV) 减少了传统摩擦离合器的安装数量,同时保持了更换需求,售后市场销量依然保持强劲。竞争动态正在改变。领先的供应商正在将其机械技术与软体和电子设备相结合,以支援混合动力架构并捍卫其市场份额。最显着的例子是舍弗勒与 Vitesco Technologies 的合併。

全球汽车离合器市场趋势与洞察

OEM快速转向双离合器和自动变速箱

双离合器变速箱 (DCT) 的效率比液力变矩器自动变速箱 (Turn Converter Automatic Transmission) 高出 28%,使汽车製造商能够在不影响性能的情况下实现车辆二氧化碳排放目标,从而推动汽车市场从高端细分市场向大众细分市场的更广泛转变。随着零件通用的提高,单位成本下降,使得 6 速和 8 速双离合器变速箱 (DCT) 能够应用于 B-Class 和 C-Class 车型。像麦格纳 48V 双离合器变速箱 (DCT) 这样的混合动力汽车将内燃机和电力推进系统紧密整合,使引擎的离岸滑行更加平稳。商用车原始设备製造商 (OEM) 正在采用混合动力自动手排变速箱 (HAT) 来降低远距运输的油耗,这推动了对具有更高热容量的重型离合器的需求。

新兴经济体轻型汽车产量增加

随着汽车製造商推进动力传动系统本地化并利用区域供应链,中国和印度组装产量的不断增长将维持核心需求。在印度,政府的奖励措施鼓励新工厂批量配置手动离合器,而不断提升的车型配置也整合了自动化选配配置,这增加了高端摩擦材料的应用机会。在中国,经历了动盪的2024年后,产量趋于稳定,随着本土品牌采用双离合器变速箱(DCT)以保持竞争力,推动了单位价值的成长。在亚洲以外,巴西和墨西哥是可靠零件更换週期的基础驱动力。都市化的加速将推动二、三线城市网约车车队的成长,在这些城市,走走停停的强制规定加速了车辆的磨损,从而推动了售后市场的销售量。

随着纯电动车的普及,传统离合器将会被淘汰。

中国的目标是到2020年,电动车占新车销售的45%。欧洲的原始设备製造商也积极推进电气化蓝图,直接用固定传动比的电力驱动联轴器取代传统的摩擦离合器。然而,混合动力架构在高速公路巡航过程中仍然使用分离离合器来分离引擎。通用汽车在基于离合器的混合动力齿轮组方面的专利活动表明,电动传动系统对复杂嚙合系统的持续需求。

报告中分析的其他驱动因素和限制因素

- 严格的二氧化碳排放目标推动了对节能离合器的需求

- 轻度混合动力架构采用48V电子离合器系统

- CVT动力传动系统在入门级车辆中日益普及

細項分析

虽然到2024年,手排变速箱仍将占据汽车离合器市场的65.10%,但双离合器变速箱已成为成长最快的细分市场,2025年至2030年的复合年增长率将达到9.19%。这一成长将由小型车的主流应用推动,因为这类车的成本差距正在缩小,监管压力也鼓励提高效率。双离合器系统的汽车离合器市场规模预计将随着八速设计的出现而成长,因为八速设计在保持性能的同时,还能更严格地控制引擎转速。

在双踏板架构中,供应商正在重新设计摩擦组件,使其配备低惯性轮毂和高导电性衬套,以限制怠速时的阻力矩。采埃孚的8速湿式双离合器变速箱(DCT)实现了28%的损耗降低,标誌着一项支援轻度混合动力P2配置的技术转变。重型卡车的自动手排变速箱(AMT)采用单副轴或双副轴,并结合耐高温有机衬套,为车队营运商提供了节省燃油的选择,而无需承担全混合动力的成本。总而言之,这些趋势将使离合器技术保持多样性,并在未来十年内保持整个汽车离合器市场的强劲成长势头。

2024年,乘用车将满足74.57%的需求,而中型和重型卡车将成为成长最快的领域,随着混合动力传动系统在区域和城市配送中越来越受欢迎,其复合年增长率将达到7.88%。与重型平台相关的汽车离合器市场规模受益于更高的单位成本,因为需要多片组和更大的热质量来处理斜坡起步时的扭矩峰值。

伊顿专为 DT12 和 i-Shift 等自动手排变速箱设计的重型离合器凸显了这一机会,并采用高速气流设计,以便在启动停止工况下散热。氢燃料卡车 Pilot 则提供了另一个利基市场,它将单级变速箱与分离离合器结合,将泵浦和压缩机分开。乘用车混合动力传动系统透过在引擎和变速箱之间插入 P2 或 P3 模组来实现电动导航,扩展了离合器的适用性。因此,即使纯电动车 (BEV) 市场不断扩张,汽车离合器市场仍能维持不同车型的均衡分布。

区域分析

受中国生产规模和印度政策驱动的製造业成长的支撑,亚太地区将在2024年维持49.65%的汽车离合器市场。到2030年,该地区的复合年增长率将达到5.41%,这反映了内燃机市场需求的稳定以及混合动力汽车部署的加速。日本和韩国是电子执行领域的领导者,将透过指定整合式电子离合器模组来推高平均单价。随着全球汽车製造商供应链多元化并确保离合器大规模在地采购,东协组装商将吸引新的投资。

南美洲是成长最快的地区,复合年增长率高达6.77%。巴西和其他南美洲国家不断增长的汽车保有量支撑了强劲的汽车更换率。新的区域贸易奖励正在推动新增运力,都市区货运电气化试点计画正在引入混合动力AMT变速箱,从而提升每辆车的货运量。阿根廷老化的车队严重依赖独立售后市场,供应商的扩张范围已超越了原厂通路。

北美和欧洲的复合年增长率分别为3.21%和2.81%,但这两个地区都实施最严格的排放气体和颗粒物法规。美国平均燃料效率(CAFE)规定每年需提升2%,并鼓励原始设备製造商将轻度混合动力模组与高效离合器结合。欧洲的欧7法规限制了煞车和离合器的磨损碎屑,加速了无铜衬片和轻量化板的采用。俄罗斯以及中东和非洲地区则因本地组装和都市区车辆保有量增加而贡献了增量。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- OEM快速转向双离合器和自动变速箱

- 新兴国家轻型汽车产量增加

- 严格的二氧化碳排放目标推动了对节能离合器的需求

- 采用48V电子离合器系统打造轻度混合动力架构

- 轻量复合摩擦材料,符合整体车辆 MPG 标准

- 二、三线城市对符合排放标准的计程车改装需求不断增加

- 市场限制

- 纯电动车的广泛应用消除了传统离合器

- CVT动力传动系统在入门级汽车中日益普及

- 双品质飞轮可靠性问题导致保固成本上升

- 无铜摩擦材料强制规定扰乱供应链

- 价值/供应链分析

- 监管状况

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模与成长预测(价值,十亿美元)

- 按传动类型

- 手动的

- 自动变速器(变矩器)

- 自动手排变速箱(AMT)

- 双离合器变速箱(DCT)

- 其他(电子离合器、CVT离合器组等)

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中大型商用车

- 非公路用车(农业、建筑)

- 按下离合器组件

- 离合器圆盘和轮毂

- 压板和盖

- 分离轴承/工作缸

- 飞轮(单质量和双质量)

- 驱动系统(液压、电液、电子)

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Schaeffler AG

- Valeo SA

- ZF Friedrichshafen AG

- EXEDY Corporation

- Aisin Corporation

- Eaton Corporation plc

- BorgWarner Inc.

- Magneti Marelli SpA

- Continental AG

- LuK

- WABCO(ZF CV Systems)

- Setco Automotive Ltd.

- FCC Co., Ltd.

- Zhejiang Tieliu Clutch Co., Ltd.

- Nissin Kogyo Co., Ltd.

- Haldex AB

- Twin Disc Inc.

- Transtar Industries Inc.

- Helix Auto Transmission

- Sachs

第七章 市场机会与未来展望

The automotive clutch market is valued at USD 14.61 billion in 2025 and is forecast to reach USD 19.19 billion by 2030, expanding at a 5.61% CAGR.

DCT technology adoption, tightening global CO2 rules, and steady light-vehicle production growth, particularly in Asia-Pacific, underpin this outlook. OEM-level demand dominates because new models increasingly pair mild-hybrid systems with electronic actuation that improves shift speed and efficiency. Meanwhile, aftermarket volumes remain resilient as vehicle fleets age well past 12 years, sustaining replacement demand even as battery-electric vehicles (BEVs) reduce installations of conventional friction clutches. Competitive dynamics are changing: leading suppliers are bundling mechanical know-how with software and electronics to protect their share while positioning for hybrid architectures, most visibly in Schaeffler's merger with Vitesco Technologies, which folds power electronics into a historic clutch portfolio.

Global Automotive Clutch Market Trends and Insights

Rapid OEM Shift Toward Dual-Clutch & Automated Transmissions

DCT efficiency advantages of up to 28% over torque-converter automatics allow carmakers to hit fleet CO2 targets without detracting from performance, prompting broad migration from premium to mass-market segments. Unit costs fall as component commonality rises, making six- and eight-speed DCTs viable for B- and C-segment cars. Hybrid variants such as Magna's 48 V DCT merge combustion and electric propulsion within tight packaging, enabling smoother engine-off coasting. Commercial-vehicle OEMs adopt hybrid automated manuals to cut fuel burn on long-haul routes, reinforcing demand for heavy-duty clutches with higher thermal capacity.

Rising Light-Vehicle Production in Emerging Economies

Expanding assembly volumes in China and India sustain core demand as automakers localize drivetrains and leverage regional supply chains. Government incentives in India encourage new plants that specify high-volume manual clutches, yet rising trim levels integrate automated options, adding premium friction-material opportunities. In China, output stabilized after 2024 turbulence, and local brands now adopt DCTs to stay competitive, driving incremental unit value. Outside Asia, Brazil and Mexico collectively field a base that fuels a dependable parts replacement cycle. Urbanization accelerates ride-hailing fleets in Tier-2 and Tier-3 cities, where stop-and-go duty accelerates wear and lifts aftermarket volumes.

Escalating BEV Penetration Eliminating Conventional Clutches

China targets a 45% EV share of new-vehicle sales by decade-end, and European OEMs deploy aggressive electric roadmaps, directly substituting the traditional friction clutch with fixed-ratio e-drive couplings. Nonetheless, hybrid architectures still use disconnect clutches to de-link engines at highway cruise. Patent activity from General Motors on clutch-based hybrid gearsets demonstrates the ongoing need for sophisticated engagement systems even in electrified drivelines.

Other drivers and restraints analyzed in the detailed report include:

- Stringent CO2 Targets Driving Demand for Fuel-Efficient Clutches

- Adoption of 48-V e-Clutch Systems for Mild-Hybrid Architectures

- Rising Popularity of CVT Powertrains in Entry-Level Cars

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual units still represented 65.10% of the automotive clutch market in 2024, yet the dual-clutch transmissions emerged as the fastest-growing segment at 9.19% CAGR from 2025-2030. That growth rides on mainstream adoption in compact cars, where cost gaps have narrowed and regulatory pressure rewards efficiency. The automotive clutch market size for dual-clutch systems is forecast to rise in tandem with eight-speed designs that maintain performance while controlling engine speed more tightly.

Across two-pedal architectures, suppliers are re-engineering friction packs with low-inertia hubs and high-conductivity liners that limit drag torque at idle. ZF's 8-speed wet DCT illustrates the technology shift, offering 28% loss reduction and supporting mild-hybrid P2 configurations. Automated manual transmissions (AMTs) in heavy trucks deploy single or twin countershafts coupled with high-heat organic linings, giving fleet operators a fuel-saving alternative without the cost of full hybrids. Together, these trends sustain broad diversity in clutch technology and preserve overall automotive clutch market momentum through the decade.

Passenger cars delivered 74.57% of demand in 2024, but medium and heavy trucks are the fastest-rising slice, expanding at 7.88% CAGR as hybrid drivetrains proliferate in regional haul and urban delivery. The automotive clutch market size attached to heavy-duty platforms benefits from higher unit value per vehicle, since multi-plate packs and greater thermal mass are needed to handle torque peaks during launch on grades.

Eaton's heavy-duty clutches, engineered for automated manuals such as DT12 and I-Shift, underscore this opportunity and include high-velocity airflow designs that dissipate heat under stop-start duty. Hydrogen-fuel truck pilots pair single-stage gearboxes with disconnect clutches that isolate pumps and compressors, offering another niche. In passenger cars, hybrid powertrains extend clutch relevance by inserting P2 or P3 modules between the engine and transmission to enable electric sailing. Consequently, the automotive clutch market maintains a balanced exposure across vehicle classes even as BEVs expand.

The Automotive Clutch Market Report is Segmented by Transmission Type (Manual, Automatic, AMT, DCT, and More), Vehicle Type (Passenger Cars, LCV, and More), Clutch Component (Clutch Disc and Hub, Pressure Plate and Cover, Release Bearing/Slave Cylinder, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific maintained a 49.65% share of the automotive clutch market in 2024, underpinned by China's production scale and India's policy-fueled manufacturing uptick. Regional CAGR of 5.41% through 2030 reflects stable internal combustion demand plus accelerating hybrid rollouts. Japan and South Korea, leaders in electronic actuation, drive higher average unit value by specifying integrated e-clutch modules. ASEAN assemblers attract new investment as global OEMs diversify supply chains, ensuring localized clutch sourcing at scale.

South America is the fastest-growing geography at 6.77% CAGR, fueled by a larger vehicle population in Brazil and other South American countries that sustains robust replacement volumes. New regional trade incentives spark fresh capacity commitments, while urban freight electrification trials integrate hybrid AMTs that lift content per vehicle. Argentina's aging fleet leans heavily on the independent aftermarket, widening supplier exposure beyond OEM channels.

North America and Europe show modest 3.21% and 2.81% CAGRs, respectively, yet both regions impose the toughest emissions and particulate rules. CAFE mandates in the United States stipulate 2% annual efficiency gains, encouraging OEMs to pair mild-hybrid modules with high-efficiency clutches. European Euro 7 standards limit brake and clutch wear particles, accelerating the adoption of copper-free linings and lightweight plates. Russia and the Middle East and Africa contribute incremental growth tied to localized assembly and rising urban ownership.

- Schaeffler AG

- Valeo SA

- ZF Friedrichshafen AG

- EXEDY Corporation

- Aisin Corporation

- Eaton Corporation plc

- BorgWarner Inc.

- Magneti Marelli SpA

- Continental AG

- LuK

- WABCO (ZF CV Systems)

- Setco Automotive Ltd.

- FCC Co., Ltd.

- Zhejiang Tieliu Clutch Co., Ltd.

- Nissin Kogyo Co., Ltd.

- Haldex AB

- Twin Disc Inc.

- Transtar Industries Inc.

- Helix Auto Transmission

- Sachs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid OEM shift toward dual-clutch and automated transmissions

- 4.2.2 Rising light-vehicle production in emerging economies

- 4.2.3 Stringent CO2 targets driving demand for fuel-efficient clutches

- 4.2.4 Adoption of 48-V e-clutch systems for mild-hybrid architectures

- 4.2.5 Lightweight composite friction materials to meet fleet-wide MPG norms

- 4.2.6 Growing retrofit demand in Tier-2/3 cities for emission-compliant taxis

- 4.3 Market Restraints

- 4.3.1 Escalating BEV penetration eliminating conventional clutches

- 4.3.2 Rising popularity of CVT powertrains in entry-level cars

- 4.3.3 Dual-mass-flywheel reliability issues causing warranty cost spikes

- 4.3.4 Upcoming copper-free friction-material mandates disrupting supply chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Billion)

- 5.1 By Transmission Type

- 5.1.1 Manual

- 5.1.2 Automatic (Torque-Converter)

- 5.1.3 Automated Manual Transmission (AMT)

- 5.1.4 Dual-Clutch Transmission (DCT)

- 5.1.5 Others (e-Clutch, CVT Clutch Packs, etc.)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Off-Highway (Agricultural and Construction)

- 5.3 By Clutch Component

- 5.3.1 Clutch Disc and Hub

- 5.3.2 Pressure Plate and Cover

- 5.3.3 Release Bearing/Slave Cylinder

- 5.3.4 Flywheel (Single and Dual-Mass)

- 5.3.5 Actuation Systems (Hydraulic, Electro-Hydraulic, Electronic)

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Schaeffler AG

- 6.4.2 Valeo SA

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 EXEDY Corporation

- 6.4.5 Aisin Corporation

- 6.4.6 Eaton Corporation plc

- 6.4.7 BorgWarner Inc.

- 6.4.8 Magneti Marelli SpA

- 6.4.9 Continental AG

- 6.4.10 LuK

- 6.4.11 WABCO (ZF CV Systems)

- 6.4.12 Setco Automotive Ltd.

- 6.4.13 FCC Co., Ltd.

- 6.4.14 Zhejiang Tieliu Clutch Co., Ltd.

- 6.4.15 Nissin Kogyo Co., Ltd.

- 6.4.16 Haldex AB

- 6.4.17 Twin Disc Inc.

- 6.4.18 Transtar Industries Inc.

- 6.4.19 Helix Auto Transmission

- 6.4.20 Sachs

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2025-2029年全球汽车离合器分离轴承市场

2025-2029年全球汽车离合器分离轴承市场 乘用车离合器压盘市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、产品类型、地区和竞争格局划分,2021-2031)商用车离合器压盘市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、产品类型、地区和竞争格局划分,2021-2031年)汽车中重型商用车离合器片市场 - 全球产业规模、份额、趋势、机会及预测(按类型、需求类别、地区和竞争格局划分,2021-2031年)汽车乘用车离合器片市场 - 全球产业规模、份额、趋势、机会及预测(按类型、需求类别、地区和竞争格局划分,2021-2031年)汽车离合器压盘市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、产品类型、地区和竞争格局划分,2021-2031年)汽车离合器市场 - 全球产业规模、份额、趋势、机会、预测:按传动方式、车辆类型、地区和竞争格局划分,2021-2031年汽车离合器片市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、类型、地区和竞争格局划分,2021-2031年)

乘用车离合器压盘市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、产品类型、地区和竞争格局划分,2021-2031)商用车离合器压盘市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、产品类型、地区和竞争格局划分,2021-2031年)汽车中重型商用车离合器片市场 - 全球产业规模、份额、趋势、机会及预测(按类型、需求类别、地区和竞争格局划分,2021-2031年)汽车乘用车离合器片市场 - 全球产业规模、份额、趋势、机会及预测(按类型、需求类别、地区和竞争格局划分,2021-2031年)汽车离合器压盘市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、产品类型、地区和竞争格局划分,2021-2031年)汽车离合器市场 - 全球产业规模、份额、趋势、机会、预测:按传动方式、车辆类型、地区和竞争格局划分,2021-2031年汽车离合器片市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、需求类别、类型、地区和竞争格局划分,2021-2031年) 草坪割草机离合器市场按类型、车辆类型、材质、应用和分销管道划分 - 全球预测 2026-2032 年汽车轻型商用车离合器片市场 - 全球产业规模、份额、趋势、机会和预测,按类型、需求类别、地区和竞争格局划分,2021-2031年预测

草坪割草机离合器市场按类型、车辆类型、材质、应用和分销管道划分 - 全球预测 2026-2032 年汽车轻型商用车离合器片市场 - 全球产业规模、份额、趋势、机会和预测,按类型、需求类别、地区和竞争格局划分,2021-2031年预测