|

市场调查报告书

商品编码

1836656

顺丁烯二酸酐:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Maleic Anhydride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

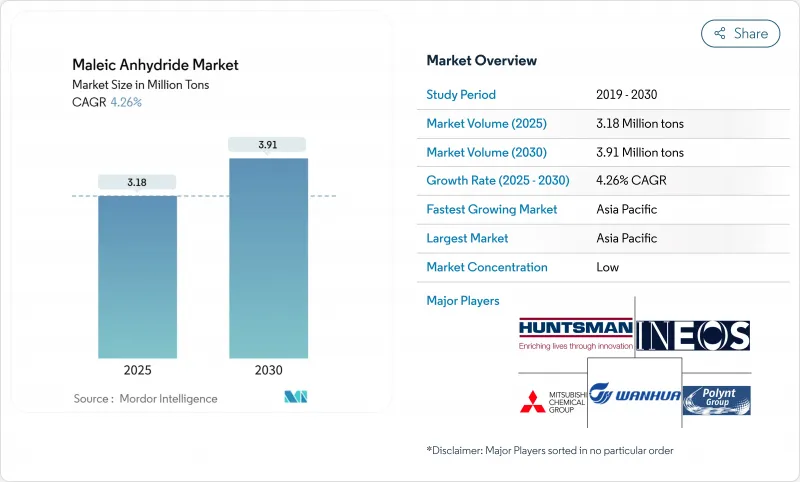

预计2025年顺丁烯二酸酐市场规模将达318万吨,2030年成长至391万吨,复合年增长率为4.26%。

不断扩张的基础设施项目、对不饱和聚酯树脂的持续需求以及正丁烷作为原材料快速替代苯,是支撑顺丁烯二酸酐市场成长的关键因素。受再生PET UPR的采用和欧洲严格的绿色建筑法规的推动,建筑业占据了消费的大部分。北美汽车製造商正在扩大轻质SMC板材的应用,刺激了对树脂的需求。在供应方面,亚太地区的产能仍然占据主导地位,但中国的供应过剩正在挤压全球利润率,并迫使其他生产商转向更高价值的利基市场。

全球顺丁烯二酸酐市场趋势与见解

欧洲建设产业对再生PET UPR的采用激增

随着欧盟包装法规于2024年强制规定废弃物材料含量基准值,建商正转向使用再生PET不饱和聚酯树脂。这些配方的拉伸强度可达65-72 MPa,与原生UPR相当,同时可减少高达25%的嵌入碳含量。顺丁烯二酸酐可增强聚合物基质中的界面黏合力,提升复合材料的耐久性,并支持低碳建筑材料领域的顺丁烯二酸酐市场。

提高正丁烷工厂产能以降低原料成本

近期的正丁烷产能波动计划扩大了与苯的原料成本差距。BASF的三叶催化剂使顺丁烯二酸酐产率提高了高达2%,并透过抑制热点温度降低了能耗强度。正丁烷路线的成本优势使其在顺丁烯二酸酐市场的份额达到70%。

经合组织收紧苯排放法规,提高合规成本

美国《有毒物质控制法》和欧盟化学品管理法规的变化将迫使苯基装置维修或关闭,从而推高营业成本,并推动向正丁烷氧化法的转变。这种转变将增加资本投资需求,并抑制以老旧设备为主的地区的成长。

报告中分析的其他驱动因素和限制因素

- 电动车轻质SMC面板加速北美UPR消费

- 生物基琥珀酸路线创造高利润共聚物

- 正丁烷价格波动与原油价格挂钩

細項分析

到2024年,不饱和聚酯树脂将占据顺丁烯二酸酐市场份额的50%,到2030年,该细分市场的复合年增长率将达到4.9%。再生PET UPR牌号具有相同的机械性质,且碳足迹降低高达25%,有助于其在节能建筑上的应用。同时,轻型船舶结构和电动车零件的成长也支撑了需求。因此,用于UPR应用的顺丁烯二酸酐市场规模预计将保持高于行业整体平均水平。

1,4-丁二醇、共聚物和特殊界面活性剂等多元化产品正在拓宽产品组合。使用Cu-ZnO催化剂,顺丁烯二酸酐连续加氢製备BDO,在190°C下产率达85%,製程效率显着提升。以生物基琥珀酸为原料的特种共聚物为生物分解性塑胶带来了高价,从而支撑了顺丁烯二酸酐产业的利润成长。

与苯相比,正丁烷氧化製程具有单位成本更低、有害副产品更少等特点,预计到2024年将占顺丁烯二酸酐市场的70%。亨斯迈的固定台技术与BASF的三叶催化剂结合,将在降低压降的同时提高产量,从而增强成本领先地位。

苯法装置主要在基础设施较落后的地区运作。儘管规模较小,但到2030年,其复合年增长率将达到4.69%,这反映了特定市场的选择性升级和原料价格竞争。这种双原料格局正在影响资本配置决策,并支持顺丁烯二酸酐市场的供应弹性。

区域分析

预计到2024年,亚太地区将占据顺丁烯二酸酐市场的69%,到2030年,复合年增长率将达到4.61%。中国的产能超过全球整体的三分之二,支撑着马来酸酐的供应。印度和东南亚地区正透过基础设施投资和不断增长的汽车产量来满足需求,而日本和韩国则透过日本触媒等公司贡献製程创新。

北美是一个技术先进且成本竞争力十足的生产基地。亨斯迈在佛罗里达州和路易斯安那州经营大型装置,将原料流与下游应用整合在一起。轻量化电动车面板和即将进行的正丁烷扩建项目正在提振该地区的成长,并增强顺丁烯二酸酐市场的收益韧性。欧洲面临能源成本上升和排放法规的严格限制,但在采用永续性方面处于领先地位,尤其是在再生PET/UPR领域。

南美特种肥料螯合物的市占率较小,但正在成长。 YPF KIMICA正在开发生物基途径,以配合该地区的精密农业重点。中东和非洲正在投资石化多元化,利用其丰富的原料来开发正丁烷计划,这可能会推动未来全球顺丁烯二酸酐市场的扩张。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 欧洲建设产业对再生PET基UPR的采用激增

- 透过提高正丁烷工厂的产能来降低原料成本

- 电动车轻质SMC面板正在加速北美UPR的消费

- 生物基琥珀酸路线生产高利润共聚物

- 南美洲水溶性肥料螯合物的成长。

- 市场限制

- 经合组织苯排放法规收紧导致合规成本上升

- 中国新增产能造成全球供应过剩

- 正丁烷价格波动与原油价格相关

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 价格趋势

第五章市场规模及成长预测(数量)

- 依产品类型

- 不饱和聚酯树脂

- 1,4-丁二醇

- 润滑油添加剂

- 顺丁烯二酸酐共聚物

- 苹果酸

- 富马酸

- 烷基琥珀酸酐

- 表面活性剂和塑化剂

- 其他产品类型

- 按原料

- 正丁烷

- 苯

- 按形状

- 固体(薄片/浆体)

- 融化

- 按最终用户产业

- 建造

- 车

- 电子产品

- 饮食

- 石油产品

- 个人护理

- 製药

- 农业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- AOC

- Arkema

- Ashland

- Bartek Ingredients Inc.

- BASF

- Borealis AG

- Clariant

- Evonik Industries AG

- Huntsman International LLC

- IG Petrochemicals Ltd.(IGPL)

- INEOS AG

- LANXESS

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- NIPPON SHOKUBAI CO., LTD.

- PETRONAS Chemicals Group Berhad

- Polynt SpA

- Sinopec Qilu Petrochemical

- SK Functional Polymer

- Thirumalai Chemicals

- Wanhua

第七章 市场机会与未来展望

The maleic anhydride market size reached 3.18 million tons in 2025 and is forecast to climb to 3.91 million tons by 2030, translating to a 4.26% CAGR.

Expanding infrastructure programs, sustained demand for unsaturated polyester resins, and the rapid substitution of benzene with n-butane feedstock are the principal growth vectors behind the maleic anhydride market. Construction accounts for the bulk of consumption, reinforced by recycled-PET UPR adoption and stringent green-building rules in Europe. North American automakers are broadening the application scope of lightweight SMC panels, adding momentum to resin demand. On the supply side, Asia Pacific's capacity leadership remains decisive, yet Chinese oversupply is compressing global margins and pushing producers elsewhere toward high-value niches.

Global Maleic Anhydride Market Trends and Insights

Surging Adoption of Recycled-PET UPR in Europe Construction

Mandatory recycled-content thresholds under the 2024 EU Packaging and Packaging Waste Regulation are steering builders toward recycled-PET unsaturated polyester resins. These formulations deliver tensile strength of 65-72 MPa, on par with virgin UPR, and trim embedded carbon by up to 25%. Maleic anhydride enhances interfacial adhesion in the polymer matrix, reinforcing composite durability and supporting the maleic anhydride market's push into low-carbon building materials.

Capacity Additions of N-Butane Plants Lowering Feedstock Cost

Recent n-butane swing-capacity projects are widening the feedstock cost gap versus benzene. BASF's trilobe-shaped catalyst lifts maleic anhydride yield by up to 2% and curbs hot-spot temperatures, translating into lower energy intensity. The resulting cost advantage is reinforcing the n-butane route's 70% share of the maleic anhydride market.

Stricter Benzene Emission Caps in OECD Raising Compliance Cost

Revisions to the U.S. Toxic Substances Control Act and EU chemical-management rules compel retrofits or closures of benzene-based units, inflating operating costs and incentivizing the migration to n-butane oxidation. The shift increases capital-spending needs and tempers growth in regions where older assets dominate.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight SMC Panels for EVs Accelerating UPR Consumption in North America

- Bio-based Succinic Acid Routes Creating High-Margin Copolymers

- N-Butane Price Volatility Linked to Crude

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unsaturated polyester resin held 50% of the maleic anhydride market share in 2024, and the segment is set to rise at a 4.9% CAGR through 2030. Recycled-PET UPR grades, offering identical mechanical performance and up to 25% lower carbon footprints, are catalyzing adoption in energy-efficient buildings. Concurrently, growth in lightweight marine structures and electric-vehicle components sustains demand. The maleic anhydride market size for UPR applications is therefore tracking above the overall industry average.

Diversification into 1,4-butanediol, copolymers, and specialty surfactants is widening the product mix. Continuous hydrogenation of maleic anhydride to BDO, achieving 85% yield over Cu-ZnO catalysts at 190 °C, illustrates process efficiency gains. Specialty copolymers derived from bio-based succinic acid are capturing premium pricing in biodegradable plastics, supporting margin expansion within the maleic anhydride industry.

N-butane oxidation processes contributed 70% to the maleic anhydride market in 2024, driven by lower unit costs and fewer hazardous by-products compared with benzene. Huntsman's fixed-bed technology, coupled with BASF's trilobe catalyst, lifts yield while lowering pressure drop, reinforcing cost leadership.

Benzene-based units operate mainly in regions where legacy infrastructure exists. Although smaller in scale, their 4.69% CAGR to 2030 reflects selective upgrades and competitive feedstock pricing in certain markets. This dual-track raw-material scenario shapes capital-allocation decisions and underpins supply flexibility in the maleic anhydride market.

The Maleic Anhydride Market Report Segments the Industry by Product Type (Unsaturated Polyester Resin, 1, 4-Butanediol, Lubricant Additives, and More), Raw Material (N-Butane and Benzene), Physical Form (Solid (Flake/Prill) and Molten), End-User Industry (Construction, Automobile, Food and Beverage, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia Pacific held 69% of the maleic anhydride market in 2024, and the region is poised for a 4.61% CAGR through 2030. China's capacity exceeds two-thirds of the global total, underpinning supply. India and Southeast Asia sustain demand through infrastructure spending and rising automotive output, while Japan and South Korea contribute process innovations via firms such as Nippon Shokubai.

North America presents a technologically advanced yet cost-competitive production base. Huntsman operates large-scale units in Florida and Louisiana, integrating feedstock streams and downstream applications. Lightweight EV panels and forthcoming n-butane expansions reinforce regional growth, reinforcing the maleic anhydride market's revenue resilience. Europe faces higher energy costs and strict emission curbs, yet leads sustainability adoption, especially recycled-PET UPR.

South America's share is modest but rising in specialty fertilizer chelates. YPF Quimica is developing bio-based pathways to align with regional precision-agriculture priorities. The Middle East and Africa are investing in petrochemical diversification, leveraging feedstock abundance for future n-butane projects that could broaden the maleic anhydride market's global footprint.

- AOC

- Arkema

- Ashland

- Bartek Ingredients Inc.

- BASF

- Borealis AG

- Clariant

- Evonik Industries AG

- Huntsman International LLC

- I G Petrochemicals Ltd. (IGPL)

- INEOS AG

- LANXESS

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- NIPPON SHOKUBAI CO., LTD.

- PETRONAS Chemicals Group Berhad

- Polynt S.p.A.

- Sinopec Qilu Petrochemical

- SK Functional Polymer

- Thirumalai Chemicals

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Recycled-PET-Based UPR in Europe Construction

- 4.2.2 Capacity Additions of N-Butane Plants Lowering Feedstock Cost

- 4.2.3 Lightweight SMC Panels for EVs Accelerating UPR Consumption in North America

- 4.2.4 Bio-based Succinic Acid Routes Creating High-Margin Copolymers

- 4.2.5 Water-Soluble Fertilizer Chelates Growth in South America

- 4.3 Market Restraints

- 4.3.1 Stricter Benzene Emission Caps in OECD Raising Compliance Cost

- 4.3.2 Global Oversupply from New Chinese Capacity

- 4.3.3 N-Butane Price Volatility Linked to Crude

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Price Trend

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Unsaturated Polyester Resin

- 5.1.2 1,4-Butanediol

- 5.1.3 Lubricant Additives

- 5.1.4 Maleic Anhydride Copolymers

- 5.1.5 Malic Acid

- 5.1.6 Fumaric Acid

- 5.1.7 Alkyl Succinic Anhydrides

- 5.1.8 Surfactants and Plasticizers

- 5.1.9 Other Product Types

- 5.2 By Raw Material

- 5.2.1 N-Butane

- 5.2.2 Benzene

- 5.3 By Physical Form

- 5.3.1 Solid (Flake/Prill)

- 5.3.2 Molten

- 5.4 By End-user Industry

- 5.4.1 Construction

- 5.4.2 Automobile

- 5.4.3 Electronics

- 5.4.4 Food and Beverage

- 5.4.5 Oil Products

- 5.4.6 Personal Care

- 5.4.7 Pharmaceuticals

- 5.4.8 Agriculture

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AOC

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Bartek Ingredients Inc.

- 6.4.5 BASF

- 6.4.6 Borealis AG

- 6.4.7 Clariant

- 6.4.8 Evonik Industries AG

- 6.4.9 Huntsman International LLC

- 6.4.10 I G Petrochemicals Ltd. (IGPL)

- 6.4.11 INEOS AG

- 6.4.12 LANXESS

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 NAN YA PLASTICS CORPORATION

- 6.4.15 NIPPON SHOKUBAI CO., LTD.

- 6.4.16 PETRONAS Chemicals Group Berhad

- 6.4.17 Polynt S.p.A.

- 6.4.18 Sinopec Qilu Petrochemical

- 6.4.19 SK Functional Polymer

- 6.4.20 Thirumalai Chemicals

- 6.4.21 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Commercialization of Bio-based Maleic Anhydride

马来酸酐市场:依原料、应用、终端用户产业及地区划分(2026-2034 年)

马来酸酐市场:依原料、应用、终端用户产业及地区划分(2026-2034 年) 全球马来酸酐市场规模、份额、趋势和成长分析报告(2026-2034年)

全球马来酸酐市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年顺丁烯二酸酐全球市场报告

2026年顺丁烯二酸酐全球市场报告 顺丁烯二酸酐产能、需求、平均价格及产业展望:至2034年

顺丁烯二酸酐产能、需求、平均价格及产业展望:至2034年 熔融顺丁烯二酸酐市场:按等级、形态、製造流程、通路、应用和最终用途行业划分 - 全球预测(2026-2032年)

熔融顺丁烯二酸酐市场:按等级、形态、製造流程、通路、应用和最终用途行业划分 - 全球预测(2026-2032年) 顺丁烯二酸酐市场规模、份额及成长分析(依原料、应用、终端用户产业及地区划分)-2026-2033年产业预测2026-2032年顺丁烯二酸酐市场(按原始材料、应用、最终用户产业和地区划分)

顺丁烯二酸酐市场规模、份额及成长分析(依原料、应用、终端用户产业及地区划分)-2026-2033年产业预测2026-2032年顺丁烯二酸酐市场(按原始材料、应用、最终用户产业和地区划分) 顺丁烯二酸酐市场报告:趋势、预测与竞争分析(至2031年)顺丁烯二酸酐功能化聚丁二烯市场报告:趋势、预测与竞争分析(至 2030 年)顺丁烯二酸酐市场,占有率,规模,趋势,产业分析报告:各用途,各原料,各终端用户,各地区- 市场预测,2024年~2032年

顺丁烯二酸酐市场报告:趋势、预测与竞争分析(至2031年)顺丁烯二酸酐功能化聚丁二烯市场报告:趋势、预测与竞争分析(至 2030 年)顺丁烯二酸酐市场,占有率,规模,趋势,产业分析报告:各用途,各原料,各终端用户,各地区- 市场预测,2024年~2032年