|

市场调查报告书

商品编码

1836697

陶瓷基复合材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030)Ceramic Matrix Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

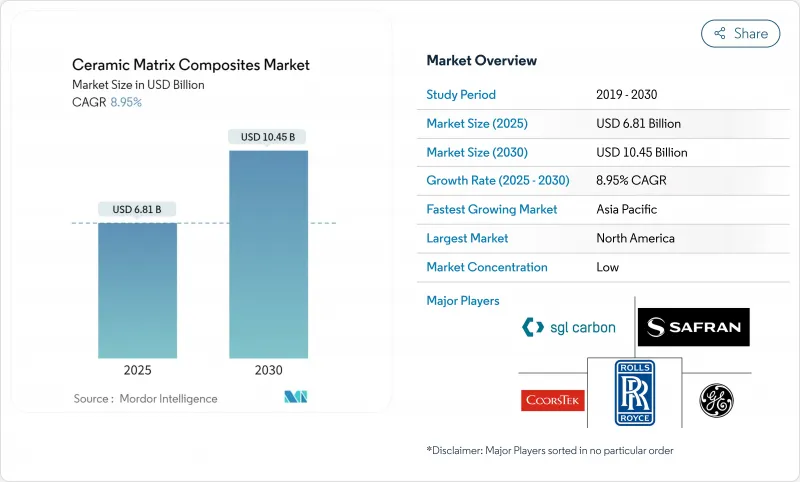

预计到 2025 年全球陶瓷基复合材料市场规模将达到 68.1 亿美元,到 2030 年将达到 104.5 亿美元,复合年增长率为 8.95%。

这一市场扩张取决于该材料能否将金属的韧性与陶瓷的耐热性相结合,有助于提升航太发动机、高超音速系统和工业燃气涡轮机的性能。轻量化推进系统的投资、燃油燃烧标准的收紧、可变燃料涡轮机的采用以及对更持久耐高温部件的追求,正在塑造当前的需求前景。自动化纤维铺放和反应熔体渗透技术的成本驱动型进步正在缩短生产週期,并缩小与镍基高温合金的成本差距。从化学加工商到核融合能源开发商,越来越多的终端用户正在指定使用陶瓷基复合材料 (CMC),这反映出多元化的机会组合,有助于支撑其长期成长韧性。

全球陶瓷基复合材料市场趋势与洞察

增加国防级隔热的使用

国防机构现在将热性能作为主要的设计过滤器。美国高超音速弹药计画要求材料在2000 度C以上仍能保持结构稳定,而这个阈值将大多数高温合金排除在外。洛克希德马丁公司的一系列测试凸显了陶瓷基复合材料(CMC)在电子设备加强和气动外壳防护方面的重要性。优质国防承包商愿意接受的生存能力加速了CMC的早期认证,从而创造了一条惠及其他行业的学习曲线。碳纤维增强碳化硅复合材料在多次高温循环后已展现出可重复使用的性能,这一优势改变了生命週期成本方程式。

对轻量化汽车平臺的需求

电动车和自动驾驶汽车专案正在积极追求减重目标,因为每减轻一公斤重量,就能提升续航里程和燃气涡轮机铺放,该工艺可将数小时的积层法转化为几分钟的循环。

製造成本高于超合金

由于高温纤维拉伸和较长的浸润步骤,CMC零件的价格仍然比同类金属零件高出三到五倍。 SCANCUT计划透过创新的铣削路径将加工时间缩短了70%,类似的自动化突破正在缩小差距。随着CMC使用寿命的延长,整体拥有成本有所改善,但对于价格敏感的电力和汽车用户来说,初始购买价格仍然是一个障碍。通用电气公司斥资2亿美元在阿拉巴马州建造的工厂旨在平衡航太领域的成本。

报告中分析的其他驱动因素和限制因素

- 不断增长的可再生燃气涡轮机维修超音速

- 加速汽车研发

- 复杂的多阶段製造路线

細項分析

2024年,SiC/SiC复合材料占据了陶瓷基复合材料市场份额的55.19%,预计到2030年将以11.05%的复合年增长率成长。细间距纤维的整合使强度达到2GPa以上,正在扩大其结构应用范围。随着新型喷射引擎核心零件对罩壳、燃烧室衬套和喷嘴延伸件的合格越来越高,SiC/SiC应用的陶瓷基复合材料市场规模预计将大幅成长。碳/碳系统在可控制氧化的火箭喷嘴领域仍占有一席之地,而氧化物/氧化物系统在工业热交换器领域正日益受到青睐,因为在工业热交换器中,固有的氧化稳定性比峰值温度更为重要。

製程改进包括奈米工程界面,可减轻热循环过程中的纤维损伤。三菱化学集团的碳纤维基C/SiC可耐受1500°C的高温,展现了混合化学如何拓展太空船应用的温度上限。将SiC浆料沉淀到织物预製件上,可实现传统积层法无法实现的复杂冷却通道。这些创新技术维持了SiC/SiC系列的领先地位,并吸引了涡轮机主厂商的投资。

区域分析

凭藉其密集的航太和国防生态系统,预计北美将在2024年占据陶瓷基复合材料市场收益的37.96%。该地区拥有垂直整合的供应链,涵盖碳化硅纤维拉挤、零件积层法、机械加工和引擎组装。先进复合材料製造创新研究所等政府倡议正在津贴试验生产线并支持区域产能。劳斯莱斯和通用电气已签订多年期订单,以平滑需求週期并为进一步的工厂扩张提供理由。

随着中国和日本加大战略材料项目的力度,到2030年,亚太地区将迎来最快的复合年增长率,达到10.84%。各国政府计画实现高性能纤维的供应独立,并将2035年定为里程碑目标。汽车电气化也将刺激该地区对轻量化、耐热部件的需求。劳动力成本下降和积极的补贴使出口价格具有竞争力,使该地区成为全球陶瓷基复合材料市场的重要消费国和供应国。

欧洲透过支援可再生电网的涡轮机维修以及劳斯莱斯UltraFan等新型飞机引擎的演示,保持了稳定的市场份额。欧盟研究网络汇集公共和私人资金,用于成熟适用于工业炉的氧化物材料,从而拓宽了其应用范围。严格的排放法规为陶瓷基复合材料(CMC)等增效材料创造了有利的政策环境,从而增强了欧洲的需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 增加国防级隔热的使用

- 对轻量化汽车平臺的需求

- 陶瓷基复合材料在国防领域的应用不断扩大

- 可再生燃气涡轮机改装正在兴起

- 加速高超音速飞行器研发

- 市场限制

- 与高温合金相比製造成本更高

- 复杂的多阶段製造路线

- 加强纤维粉尘排放监管

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模及成长预测(金额)

- 依产品类型

- C/C

- C/SiC

- Oxide/Oxide

- SiC/SiC

- 按最终用户产业

- 车

- 航太

- 防御

- 能源和电力

- 电气和电子

- 其他终端用户产业(医疗等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 土耳其

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- applied thin films inc.

- CeramTec GmbH

- COIC

- CoorsTek Inc.

- General Electric Company

- KYOCERA Corporation

- LANCER SYSTEMS

- Mitsubishi Chemical Group Corporation

- Pratt & Whitney

- Rolls-Royce

- Safran

- SGL Carbon

- Starfire Systems Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

第七章 市场机会与未来展望

The global ceramic matrix composites market is valued at USD 6.81 billion in 2025 and is forecast to reach USD 10.45 billion by 2030, registering an 8.95% CAGR through the period.

Expansion rests on the material's ability to combine the toughness of metals with the heat resistance of ceramics, a balance that unlocks performance gains for aerospace engines, hypersonic systems, and industrial gas turbines. Investment in lightweight propulsion, stricter fuel-burning standards, adoption of variable-fuel turbines, and the search for longer-life high-temperature parts shape the current demand outlook. Cost-down progress in automated fiber placement and reactive melt infiltration is compressing cycle times and closing the cost gap with nickel super-alloys, while government grants for advanced-materials plants are de-risking capacity additions. A wider set of end users-from chemical processors to fusion-energy developers-now specify CMCs, reflecting a more diversified opportunity mix that supports long-term growth resilience.

Global Ceramic Matrix Composites Market Trends and Insights

Increasing Defense-Grade Thermal Barrier Applications

Defense agencies now treat thermal capability as a primary design filter. Hypersonic munitions programs in the United States require materials that remain structurally stable above 2,000 °C, a threshold that eliminates most super-alloys. Lockheed Martin's test series highlights the need for CMCs in electronics ruggedization and aero-shell protection. The premium prices defense contractors accept for survivability accelerate early CMC qualification, generating learning curves that benefit other sectors. Carbon-fiber reinforced silicon carbide composites have demonstrated reusable performance after multiple high-heat cycles, an advantage that shifts life-cycle cost equations.

Lightweight Vehicle Platforms Demand

Electric and autonomous vehicle programs pursue aggressive mass-reduction targets because every kilogram saved improves driving range and cooling efficiency. Ceramic matrix composites weigh up to 65% less than nickel-based alloys yet retain functional strength at exhaust temperatures. Demonstration ceramic gas turbines in Japan reached thermal efficiencies above 40% while cutting component weight by double-digit percentages. Automotive production volumes push suppliers toward near-net-shape processes such as automated fiber placement that convert hours-long layups into minute-level cycles.

High Production Cost vs. Super-Alloys

CMC parts still cost 3-5 times more than comparable metallic parts due to high-temperature fiber draw and lengthy infiltration steps. The SCANCUT project cut machining time by 70% through novel milling paths, and similar automation breakthroughs are narrowing the gap. Total cost of ownership improves as CMC lifetimes lengthen, but initial acquisition price remains a hurdle for price-sensitive power and automotive users. GE's USD 200 million Alabama facility targets cost parity at scale geaerospace.

Other drivers and restraints analyzed in the detailed report include:

- Growing Renewable Gas-Turbine Retrofits

- Hypersonic Vehicle R&D Acceleration

- Complex Multi-Step Manufacturing Routes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SiC/SiC composites held 55.19% ceramic matrix composites market share in 2024 and are projected to grow at an 11.05% CAGR to 2030. Integration of finer pitch fibers delivering strengths above 2 GPa has expanded their structural envelope. The ceramic matrix composites market size for SiC/SiC applications is forecast to rise sharply as new jet engine cores qualify shrouds, combustor liners, and nozzle extensions. Carbon/carbon systems maintain niches in rocket nozzles where oxidation can be controlled, and oxide/oxide grades gain traction in industrial heat exchangers that value inherent oxidation stability over peak temperature.

Process advances include nano-engineered interphases that mitigate fiber damage during thermal cycling. Mitsubishi Chemical Group's carbon-fiber-based C/SiC, qualified for 1,500 °C exposure, shows how hybrid chemistries extend temperature ceilings for space vehicles. The additive deposition of SiC slurry onto woven preforms makes complex cooling passages not feasible with legacy layups. Such innovations maintain the lead of the SiC/SiC family and attract investment from turbine primes.

The Ceramic Matrix Composites Market Report Segments the Industry by Product Type (C/C, C/SiC, Oxide/Oxide, and More), End-User Industry (Automotive, Aerospace, Defense, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Due to dense aerospace and defense ecosystems, North America commanded 37.96% of the ceramic matrix composites market revenue in 2024. The region houses vertically integrated supply chains that span SiC fiber draw, component layup, machining, and engine assembly. Government initiatives like the Institute for Advanced Composites Manufacturing Innovation funnel grants toward pilot lines, underpinning local capacity. Rolls-Royce and GE place multi-year orders that smooth demand cycles and justify further plant expansions.

Asia-Pacific delivers the fastest 10.84% CAGR through 2030 as China and Japan escalate strategic materials programs. National plans seek supply independence for high-performance fibers, with milestone targets set for 2035. Automotive electrification also stimulates regional demand for lightweight, thermally resilient parts. Lower labor costs and proactive subsidies enable competitive export pricing, positioning the region as a significant consumer and global ceramic matrix composites market supplier.

Europe maintains a steady share through turbine retrofits that support renewable-heavy grids and through new aircraft engine demonstrators such as Rolls-Royce UltraFan. EU research networks pool public and private funds to mature oxide-oxide grades suitable for industrial furnaces, widening application scope. Strict emission regulations create a positive policy environment for efficiency-raising materials like CMCs, reinforcing European demand.

- 3M

- applied thin films inc.

- CeramTec GmbH

- COIC

- CoorsTek Inc.

- General Electric Company

- KYOCERA Corporation

- LANCER SYSTEMS

- Mitsubishi Chemical Group Corporation

- Pratt & Whitney

- Rolls-Royce

- Safran

- SGL Carbon

- Starfire Systems Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing defense-grade thermal barrier applications

- 4.2.2 Lightweight vehicle platforms demand

- 4.2.3 Increasing Application of Ceramic Matrix Composites in Defense Sector

- 4.2.4 Growing renewable gas-turbine retrofits

- 4.2.5 Hypersonic vehicle R&D acceleration

- 4.3 Market Restraints

- 4.3.1 High production cost vs. super-alloys

- 4.3.2 Complex multi-step manufacturing routes

- 4.3.3 Stricter fibre-dust emission norms

- 4.4 ValueChain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 C/C

- 5.1.2 C/SiC

- 5.1.3 Oxide/Oxide

- 5.1.4 SiC/SiC

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace

- 5.2.3 Defense

- 5.2.4 Energy & Power

- 5.2.5 Electrical & Electronics

- 5.2.6 Other End-User Industries (Medical, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 Nordic Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 applied thin films inc.

- 6.4.3 CeramTec GmbH

- 6.4.4 COIC

- 6.4.5 CoorsTek Inc.

- 6.4.6 General Electric Company

- 6.4.7 KYOCERA Corporation

- 6.4.8 LANCER SYSTEMS

- 6.4.9 Mitsubishi Chemical Group Corporation

- 6.4.10 Pratt & Whitney

- 6.4.11 Rolls-Royce

- 6.4.12 Safran

- 6.4.13 SGL Carbon

- 6.4.14 Starfire Systems Inc.

- 6.4.15 TORAY INDUSTRIES, INC.

- 6.4.16 UBE Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球陶瓷基质材料市场规模、份额、趋势和成长分析报告(2026-2034)

全球陶瓷基质材料市场规模、份额、趋势和成长分析报告(2026-2034) 陶瓷基质材料市场规模、份额、趋势及预测(按复合材料材料类型、纤维类型、纤维材料、应用和地区划分),2026-2034年

陶瓷基质材料市场规模、份额、趋势及预测(按复合材料材料类型、纤维类型、纤维材料、应用和地区划分),2026-2034年 陶瓷基复合材料市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)

陶瓷基复合材料市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年) 2026年全球陶瓷基质复合材料市场报告日本陶瓷基复合材料市场报告(按复合材料类型、纤维类型、纤维材料、应用和地区划分,2026-2034年)

2026年全球陶瓷基质复合材料市场报告日本陶瓷基复合材料市场报告(按复合材料类型、纤维类型、纤维材料、应用和地区划分,2026-2034年) 陶瓷基质复合材料市场预测至2032年:按基体类型、纤维材料、製造流程、最终用户和地区分類的全球分析

陶瓷基质复合材料市场预测至2032年:按基体类型、纤维材料、製造流程、最终用户和地区分類的全球分析 陶瓷基质材料市场规模、份额、成长分析(按纤维类型、基体类型、纤维材料、终端应用产业和地区划分)-2026-2033年产业预测

陶瓷基质材料市场规模、份额、成长分析(按纤维类型、基体类型、纤维材料、终端应用产业和地区划分)-2026-2033年产业预测 陶瓷基复合材料市场-全球产业规模、份额、趋势、机会和预测,依产品类型、应用、地区和竞争格局划分,2020-2030年预测全球柔性陶瓷复合材料市场:预测至2032年-按纤维类型、基材、製造流程、最终用户和地区分類的分析

陶瓷基复合材料市场-全球产业规模、份额、趋势、机会和预测,依产品类型、应用、地区和竞争格局划分,2020-2030年预测全球柔性陶瓷复合材料市场:预测至2032年-按纤维类型、基材、製造流程、最终用户和地区分類的分析 陶瓷基复合材料 (CMC) 市场(按基质类型、增强类型、製造技术、应用、最终用途行业和分销渠道)- 全球预测,2025-2032 年

陶瓷基复合材料 (CMC) 市场(按基质类型、增强类型、製造技术、应用、最终用途行业和分销渠道)- 全球预测,2025-2032 年