|

市场调查报告书

商品编码

1842418

工业微生物学:全球市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Global Industrial Microbiology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

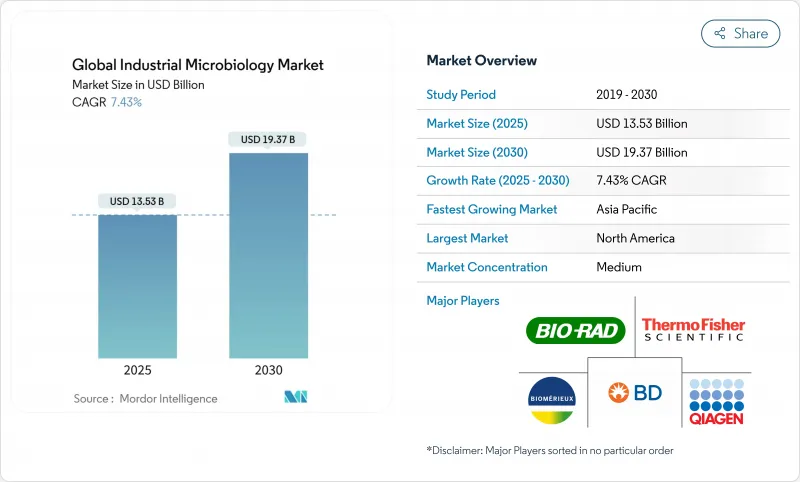

预计 2025 年工业微生物市场价值将达到 135.3 亿美元,到 2030 年预计将成长至 193.7 亿美元,复合年增长率为 7.43%。

随着生物加工、精准发酵和 ESG主导的废弃物生物修復计划为服务提供者创造新的收益来源,需求正在超越传统的品管测试。来自培养肉类设施的快速无菌和内毒素筛检要求,以及多个司法管辖区对基因改造作物的审查力度加大,正在再形成全球供应链的验证通讯协定。供应商中断,尤其是 BD 2024 年 BACTEC 血培养管瓶短缺,正在推动人们对多源采购筹资策略和自动库存追踪的兴趣,以确保实验室的运作。随着领先供应商寻求收购、一次性生物反应器创新和人工智慧驱动的污染检测软体,以在速度、数据完整性和网路安全弹性方面脱颖而出,竞争正在加剧。

全球工业微生物学市场趋势与见解

对营养补充品和发酵产品的需求不断增长

亚洲益生菌消费量激增,尤以 Zuellig Pharma 与印尼、菲律宾和台湾地区长达十年的合作伙伴关係分销 OMNi-BiOTiC 菌株为标誌,促使实验室提供以区域为重点的菌株表征服务以及代谢物分析。因此,工业微生物学市场正将其重点从病原体检测转向更深入的功能分析,以量化生物活性和区域口味偏好。製造商也在定製配方以满足当地的监管要求,这加速了新兴经济体对快速微生物品质检测基础设施的需求。从鲜味调味料到生物基甜味剂,发酵衍生成分的范围不断扩大,为污染物和脱靶代谢物增加了新的品质查核点。总的来说,这种转变正在维持正常的消费量并巩固与主要供应商的长期试剂合约。

人们对食品安全的兴趣日益浓厚,监管也更加严格

最近因李斯特菌而引发的补充奶昔召回事件促使监管机构收紧污染确认的周转目标,从而刺激了高通量 PCR 和全基因组测序工作流程的采用。 FDA 更新的《药物微生物学手册》要求统一的内毒素和抗菌功效检测与符合 21 CFR 11 的资料撷取系统无缝整合。生物梅里埃等供应商已推出其 3P ENTERPRISE 平台,将数位环境监控与审核的电子记录相结合。区块链支援的供应链透明度增加了另一层文檔,并迫使 QC 实验室产生防篡改的微生物测试报告。这种压力推动了对自动培养箱、快速阅读器和中间件的支出增加,这些设备可以缩短结果週期,同时满足不断发展的全球基准。

食品中基因改造作物的监管衝突

由于 CRISPR 编辑作物的框架多种多样,合规性变得复杂,欧盟提案对新兴基因组技术采取双重监管途径,而美国则倾向于透过 ICH 进行协调。因此,服务全球客户的实验室必须维护平行的通讯协定、认证和报告格式,这会增加营运成本并扩大技术纯熟劳工的能力。中国加强的生物安全监管也要求出口商证明基因改造微生物从谱係到最终产品的可追溯性。由于有超过 1,900 项 CRISPR作物专利且没有统一的治疗方法,工业微生物学市场的品质控制提供者在规划针对基因改造作物的分析平台的资本投资时面临不确定性。这些不一致性正在减缓跨境采用针对基因改造生物的快速微生物检测方法。

报告中分析的其他驱动因素和限制因素

- 研发费用不断增加,生物製药产品线不断扩大

- 扩大生质燃料和酵素的工业发酵

- 专业培养基投入的供应链不确定性

細項分析

至2024年,耗材将占全球总营收的52.38%,凸显其在日常营运中的关键角色。随着每个自动化週期的推进,试剂用量也不断增加,预计到2030年,与耗材相关的工业微生物学市场规模将以9.28%的复合年增长率成长,因为高通量设备需要更大、更高品质的批次。製药无尘室环境监测准则的日益严格推动了培养基和培养物製备的扩展。支援RFID的管瓶和培养皿提高了库存准确性,并支援远端批次放行检验,加深了实验室对品牌耗材的依赖。

仪器与系统部门将受益于一次性技术,该技术可将清洁验证步骤减少50%,但由于资本预算遵循多年週期,其份额成长将放缓。过滤和离心技术的创新有利于封闭式系统配置,从而阻止可疑微生物进入上游。自动菌落计数器系统减少了分析人员的时间,从而提高了供应商的通量并改善了试剂回收率。这些协同效应有助于供应商在日益激烈的竞争中保持净利率。

在全球HACCP标准的推动下,预计到2024年,食品饮料产业将占据工业微生物学市场份额的32.42%。然而,预计到2030年,製药和生物技术产业将以10.22%的复合年增长率成长,推动内毒素、霉浆菌和无菌检测套组等工业微生物学市场规模的成长。细胞和基因治疗製造领域的成长将最为强劲,因为快速放行检测可以将产品前置作业时间缩短数週。

随着 ESG主导的清洁基金赞助工业场所的石油、重金属和 PFAS 的微生物修復,环境检测正日益受到关注。农业越来越多地利用根瘤菌来促进植物生长,以分析土壤健康状况;而化妆品品牌则投资于微生物友善配方,并要求进行活菌培养稳定性评估。这种用例的多样化分散了服务供应商的风险,并鼓励各行各业广泛采用这些设备。

区域分析

北美的领先地位归功于成熟的GMP执行和持续的资本投资,例如赛默飞世尔科技在美国投资20亿美元升级项目。加拿大生技丛集正在利用优惠的研发税额扣抵,开发植物来源食品的微生物联盟,而墨西哥生产商则专注于跨境协调,以满足USMCA食品安全审核的要求。涵盖自动化资料系统的网路安全框架进一步区分了区域供应商,并结合了基于角色的存取控制和加密备份。

亚太地区两位数的成长轨迹得益于中国国营生技药品製药厂寻求全球cGMP认证、印度疫苗和生物相似药出口商,以及日本机能性食品企业对先进菌株稳定性分析的需求。韩国和澳洲政府对mRNA设施的支持也加速了对快速品质控制解决方案的需求。区域供应商实现消费品在地化生产将缩短前置作业时间,避免进口关税,并从老牌跨国公司手中抢占市场份额。

欧洲正在平衡严格的监管与绿色转型的奖励。欧盟推动ISCC Plus认证将鼓励广泛采用可再生塑胶耗材,赛多利斯公司实现化石塑胶减量50%的里程碑就证明了这一点。德国和法国正率先使用预测性微生物分析技术建立生物製程4.0试点工厂,英国则在公共领域资助噬菌体疗法的研发。然而,由于各国在基因改造作物方面的监管规定存在差异,跨国实验室必须实施重复的通讯协定,这在一定程度上限制了跨境效率。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 对营养补充品和发酵产品的需求不断增长

- 对食品安全的日益关注和更严格的监管

- 研发费用不断增加,生物製药产品线不断扩大

- 扩大生质燃料和酵素的工业发酵

- 培养肉生产中的快速品质控制需求

- ESG资助的微生物组废弃物生物修復计划

- 市场限制

- 食品中基因改造作物的监管衝突

- 产品召回增加导致审查力道加大

- 专业媒体投入的供应链不确定性

- 自动化微生物资料系统的网路安全风险

- 价值/供应链分析

- 监管状况

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场规模及成长预测(金额)

- 依产品类型

- 设备和系统

- 发酵系统

- 生物反应器和发酵罐

- 过滤和离心分离系统

- 其他的

- 耗材

- 培养基/培养液

- 培养皿和管瓶

- 其他耗材

- 试剂

- 酵素和缓衝液

- 其他的

- 设备和系统

- 按应用领域

- 食品和饮料业

- 製药和生物技术

- 农业

- 环保产业

- 化妆品和个人护理行业

- 其他应用领域

- 依微生物类型

- 细菌

- 酵母和霉菌

- 病毒和噬菌体

- 按测试类型

- 无菌测试

- 生物负载测试

- 内毒素检测

- 其他的

- 按地区(金额)

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 其他亚太地区

- 中东和非洲

- GCC

- 南非

- 其他中东和非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 北美洲

第六章 竞争态势

- 市场集中度

- 市占率分析

- 公司简介

- 3M Company

- Agilent Technologies

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Danaher Corporation

- bioMerieux SA

- Bio-Rad Laboratories Inc.

- Becton, Dickinson & Company

- Sartorius AG

- Eppendorf AG

- QIAGEN NV

- Novozymes A/S

- Lonza Group AG

- Charles River Laboratories

- Pall Corporation(Danaher)

- Shimadzu Corporation

- Waters Corporation

- Asiagel Corporation

- Bio-Techne Corporation

- Grant Instruments

- BD Diagnostic Systems

第七章 市场机会与未来展望

The industrial microbiology market is valued at USD 13.53 billion in 2025 and is forecast to climb to USD 19.37 billion by 2030, reflecting a 7.43% CAGR over the period.

Demand is widening beyond traditional quality-control testing as bioprocessing, precision fermentation, and ESG-driven waste-bioremediation projects create fresh revenue pools for service providers. Rapid sterility and endotoxin screening requirements originating from cultivated-meat facilities, together with stricter GMO oversight in multiple jurisdictions, are reshaping validation protocols across the global supply chain. Supplier disruptions-in particular BD's shortage of BACTEC blood-culture vials in 2024-have amplified interest in multisource procurement strategies and automated inventory tracking to secure laboratory uptime. Competitive intensity is accelerating as leading vendors pursue acquisitions, single-use bioreactor innovations, and AI-driven contamination-detection software to differentiate on speed, data integrity, and cybersecurity resilience.

Global Industrial Microbiology Market Trends and Insights

Growing Demand for Nutraceuticals & Fermented Products

Surging probiotic consumption across Asia, highlighted by Zuellig Pharma's decade-long alliance to distribute OMNi-BiOTiC strains in Indonesia, Philippines, and Taiwan, is pushing laboratories to offer localized strain-characterization services alongside metabolite profiling. The industrial microbiology market is therefore pivoting from pathogen detection toward deeper functional analytics that quantify bioactivity and regional taste preferences. Manufacturers are also tailoring formulations to match local regulatory requirements, which accelerates demand for rapid microbial-quality testing infrastructure in emerging economies. The widening palette of fermentation-derived ingredients-ranging from umami seasonings to bio-based sweeteners-is adding new QC checkpoints for contaminants and off-target metabolites. These shifts collectively sustain recurring consumable uptake and cement long-term reagent contracts for leading suppliers.

Rising Concern for Food Safety & Stringent Regulations

Recent Listeria-linked recalls involving supplement shakes prompted regulators to enforce tighter turnaround targets for contamination confirmation, spurring adoption of high-throughput PCR and whole-genome-sequencing workflows. The FDA's updated Pharmaceutical Microbiology Manual demands harmonized endotoxin and antimicrobial-effectiveness assays that integrate seamlessly with 21 CFR 11-compliant data-capture systems. Vendors such as bioMerieux responded with the 3P ENTERPRISE platform, pairing digital environmental monitoring with audit-ready electronic records. Blockchain-supported supply-chain transparency adds another documentation layer, compelling QC labs to generate tamper-proof microbial test reports. Collectively, these pressures increase spending on automated incubators, rapid readers, and middleware that can cut result cycles while meeting evolving global benchmarks.

Regulatory Conflicts Over GMOs in Food Sources

Divergent frameworks for CRISPR-edited crops create compliance complexity as the EU proposes dual regulatory pathways for new genomic techniques, while the U.S. leans on harmonization through the ICH. Testing laboratories servicing global clients must therefore maintain parallel protocols, certifications, and reporting formats, increasing operating costs and stretching skilled-labor capacity. China's heightened biosafety oversight further obliges exporters to demonstrate traceability of genetically modified microorganisms from strain lineage to final product. As patent volumes for CRISPR crops exceed 1,900 yet lack uniform treatment, QC providers in the industrial microbiology market face uncertainty when planning capital investments in GMO-specific analytical platforms. These discrepancies slow cross-border adoption of rapid microbial assays tailored to engineered organisms.

Other drivers and restraints analyzed in the detailed report include:

- Increasing R&D Spend & Biopharma Pipeline Expansion

- Expansion of Industrial Fermentation for Biofuels & Enzymes

- Supply-Chain Volatility in Specialty Culture Media Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables represented 52.38% of global revenue in 2024, underscoring their vital role in day-to-day operations. Reagent volumes rise with each automation cycle, and the industrial microbiology market size attached to consumables is projected to grow at 9.28% CAGR to 2030 as high-throughput instruments demand larger lot-qualified batches. Media & culture preparations expand in tandem with stricter environmental-monitoring guidelines for pharmaceutical clean rooms. RFID-enabled vials and plates improve inventory accuracy and support remote batch-release verification, deepening laboratory reliance on branded disposables.

The equipment & systems segment benefits from single-use technologies that cut cleaning validation steps by 50%, yet its share grows more gradually because capital budgets follow multi-year cycles. Filtration and centrifugation innovations favor closed-system configurations that block adventitious microbes upstream. Automated colony-counters reduce analyst hours, which translates into higher throughput and greater reagent pull-through for suppliers. Such synergies help vendors defend margins even as competition intensifies.

The food & beverage sector held 32.42% of industrial microbiology market share in 2024 on the back of global HACCP standards. However, the pharmaceutical & biotechnology segment is forecast to deliver a 10.22% CAGR through 2030, expanding the industrial microbiology market size for endotoxin, mycoplasma, and sterility testing kits. Growth is strongest in cell- and gene-therapy manufacturing, where rapid release testing can shave weeks off product lead-times.

Environmental testing is gaining traction as ESG-directed remediation funds sponsor microbiome-based clean-up of oil, heavy metals, and PFAS at industrial sites. Agricultural applications increasingly involve soil-health profiling using plant-growth-promoting rhizobacteria, while cosmetic brands invest in microbiome-friendly formulations that require live-culture stability assessments. These diversified use-cases spread risk for service providers and underpin broader instrument penetration across verticals.

The Industrial Microbiology Market is Segmented by Product Type (Equipment & Systems [Fermentation Systems, and More], Consumables [Media & Culture Preparations, and More], Reagents), by Application Area (Food & Beverage Industry, Pharmaceutical & Biotechnology Industry, and More), by Microbial Type (Bacteria, and More), by Test Type (Sterility Testing, and More), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America's leadership stems from mature GMP enforcement and ongoing capital investment such as Thermo Fisher's USD 2 billion U.S. upgrade program, which expands local single-use media output and strengthens supply resilience. Canadian biotech clusters leverage favorable R&D tax credits to develop microbial consortia for plant-based foods, whereas Mexican producers focus on cross-border harmonization to meet USMCA food-safety audits. Cybersecurity frameworks targeting automated data systems further differentiate regional vendors that embed role-based access controls and encrypted backups.

Asia-Pacific's double-digit trajectory arises from China's state-backed biologics plants seeking global cGMP accreditation, India's vaccine and biosimilar exporters, and Japan's functional-food incumbents requiring advanced strain-stability analytics. Government support for mRNA facilities in South Korea and Australia also accelerates demand for rapid QC solutions. Regional suppliers that localize consumable production reduce lead times and skirt import duties, capturing share from established multinationals.

Europe balances regulatory rigor with green-transition incentives. The EU's push for ISCC Plus certification drives uptake of renewable-plastic consumables, as demonstrated by Sartorius' 50% fossil-plastic reduction milestone. Germany and France spearhead bioprocess-4.0 pilot plants deploying predictive microbial analytics, while the UK channels public funding into phage-therapy R&D. Divergent GMO rules, however, oblige multi-national labs to run dual protocols, mildly constraining cross-border efficiencies.

- 3M

- Agilent Technologies

- Thermo Fisher Scientific

- Merck

- Danaher

- bioMerieux

- Bio-Rad Laboratories

- Beckton Dickinson

- Sartorius

- Eppendorf

- QIAGEN

- Novozymes A/S

- Lonza Group

- Charles River

- Pall Corporation (Danaher)

- Shimadzu

- Waters Corporation

- Asiagel

- Bio-Techne

- Grant Instruments

- BD Diagnostic Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for nutraceuticals & fermented products

- 4.2.2 Rising concern for food safety & stringent regulations

- 4.2.3 Increasing R&D spend & biopharma pipeline expansion

- 4.2.4 Expansion of industrial fermentation for biofuels & enzymes

- 4.2.5 Rapid QC needs in cultivated-meat manufacturing

- 4.2.6 ESG-funded microbiome waste-bioremediation projects

- 4.3 Market Restraints

- 4.3.1 Regulatory conflicts over GMOs in food sources

- 4.3.2 Escalating product recalls heightening scrutiny

- 4.3.3 Supply-chain volatility in specialty culture media inputs

- 4.3.4 Cyber-security risks to automated microbiology data systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Equipment & Systems

- 5.1.1.1 Fermentation Systems

- 5.1.1.2 Bioreactors & Fermenters

- 5.1.1.3 Filtration & Centrifugation Systems

- 5.1.1.4 Others

- 5.1.2 Consumables

- 5.1.2.1 Media & Culture Preparations

- 5.1.2.2 Petri Dishes & Vials

- 5.1.2.3 Other Consumables

- 5.1.3 Reagents

- 5.1.3.1 Enzymes & Buffers

- 5.1.3.2 Others

- 5.1.1 Equipment & Systems

- 5.2 By Application Area

- 5.2.1 Food & Beverage Industry

- 5.2.2 Pharmaceutical & Biotechnology Industry

- 5.2.3 Agricultural Industry

- 5.2.4 Environmental Industry

- 5.2.5 Cosmetic / Personal-Care Industry

- 5.2.6 Other Application Areas

- 5.3 By Microbial Type

- 5.3.1 Bacteria

- 5.3.2 Yeasts & Molds

- 5.3.3 Viruses & Phages

- 5.4 By Test Type

- 5.4.1 Sterility Testing

- 5.4.2 Bioburden Testing

- 5.4.3 Endotoxin Testing

- 5.4.4 Others

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Agilent Technologies

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Merck KGaA

- 6.3.5 Danaher Corporation

- 6.3.6 bioMerieux SA

- 6.3.7 Bio-Rad Laboratories Inc.

- 6.3.8 Becton, Dickinson & Company

- 6.3.9 Sartorius AG

- 6.3.10 Eppendorf AG

- 6.3.11 QIAGEN NV

- 6.3.12 Novozymes A/S

- 6.3.13 Lonza Group AG

- 6.3.14 Charles River Laboratories

- 6.3.15 Pall Corporation (Danaher)

- 6.3.16 Shimadzu Corporation

- 6.3.17 Waters Corporation

- 6.3.18 Asiagel Corporation

- 6.3.19 Bio-Techne Corporation

- 6.3.20 Grant Instruments

- 6.3.21 BD Diagnostic Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment