|

市场调查报告书

商品编码

1842483

汽车自动轮胎充气系统:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Automotive Automatic Tire Inflation System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

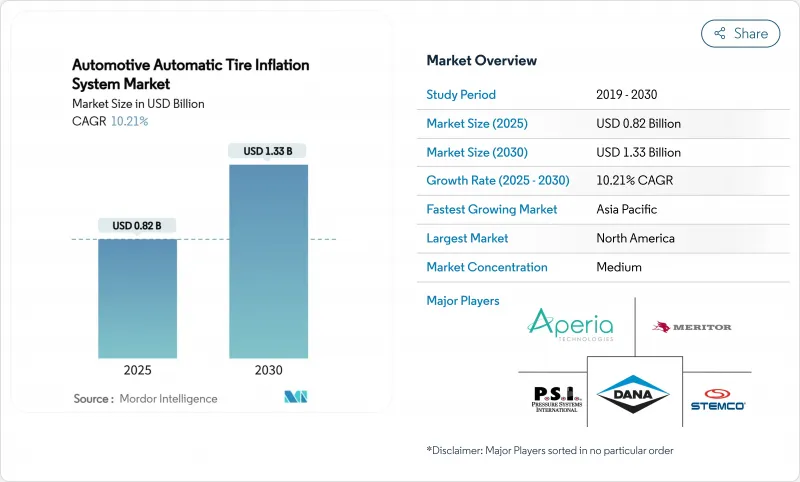

预计 2025 年汽车自动轮胎充气系统市场价值将达到 8.2 亿美元,到 2030 年将达到 13.3 亿美元,复合年增长率为 10.21%。

成长反映了协调的安全法规、降低车辆成本的需求以及与联网汽车架构更紧密的整合。北美车辆必须符合 49 CFR 393.75 的冷充气规则,欧盟的通用安全法规 II 要求所有新车必须监测轮胎压力,这间接推动了对全自动轮胎充气功能的需求。商用车辆透过保持适当的轮胎充气可节省高达 1.4% 的燃油,从而提高自动化系统的投资收益。同时,农业和施工机械製造商正在采用中央轮胎压力控制来满足土壤保护要求和精密农业需求,例如 Fendt 的 Variogrip,它可以在行驶过程中将轮胎压力从 8.7 变为 36.3 PSI。投资动能受到创投的支持,例如 Aperia Technologies 的 4,500 万美元资金筹措毂安装、自供电充气机。

全球汽车自动轮胎充气系统市场趋势与洞察

越来越多的汽车製造商致力于降低燃料和轮胎磨损成本

轮胎支出占重型卡车营运预算的15-20%,而轮胎充气不足是导致道路轮胎故障的95%的原因。 Pressure Systems International公司表示,安装自动充气系统后,燃油经济性平均可提高1.4%,轮胎寿命可延长10%。此资料丰富的平台提供即时压力、温度和负载讯息,使负责人能够优化速度曲线和维护时段。远距运输业者看到了最大的绝对收益,因为一旦牵引车年行驶里程超过12万英里,增量成本就会累积。因此,采购团队正在纳入总拥有成本模型,优先考虑在牵引车和拖车更换週期内安装自动充气系统。

全球严格的轮胎安全法规

全球立法正在加强轮胎维护纪律。欧盟通用安全法规 II 将于 2024 年 7 月生效,要求对 M1 以外的所有新认证车辆类别进行轮胎压力监测,从而创建通用基准以鼓励自动压力升级。互补的欧 7 法规设定了轮胎磨损的上限,并规定了 2032 年的合规期限。在美国,联邦汽车运输安全管理局的检查员在路边检查期间强制执行最低轮胎压力限制,促使大型车队安装自动系统以避免受到打击。随着出口导向原始设备製造商寻求与欧盟标准协调一致,类似的法规正在蔓延到南美洲和东南亚。因此,车队经理认识到市场引入自动汽车轮胎充气系统既是合规的必要条件,也是节省营运成本的途径。

前期成本高且整合复杂

每辆车的系统套件价格在 1,500 美元到 5,000 美元之间。改装计划会增加人工时间和潜在的停机时间,而许多小型卡车运输公司难以负担。商用轮胎经销商指出,预算有限的业者会将升级推迟到资本支出週期到位,儘管盈亏平衡分析通常显示投资回收期为 18 个月或更短。技术人员培训、感测器校准以及与传统电控系统的软体集成,进一步阻碍了价格敏感地区的采用。

細項分析

到2024年,中型和重型商用车将占汽车自动轮胎充气系统市场收入的66.82%,这表明该细分市场将对汽车自动轮胎充气系统市场产生重大影响。年行驶里程的增加、多轴配置以及对油耗的高灵敏度,为自动轮胎充气系统带来了极具吸引力的投资案例。远距离诊断和压力校准使负责人能够最大限度地减少路边服务呼叫,并保证交付进度。随着原始设备製造商在其车型系列中标准化充气端口和数据通讯协定,其应用范围正在扩展到区域卡车和最后一英里卡车。

非公路设备将呈现最迅猛的成长轨迹,到2030年,复合年增长率将达到11.84%。精密农业需要轻柔的土壤负荷以保障产量,而建筑和军用车辆则需要在沥青、砾石和泥浆之间快速调整。芬特的驾驶室内VarioGrip系统可在几秒钟内切换压力,从而提高牵引效率并减少压实。约翰迪尔和凯斯纽荷兰工业集团也提供类似的产品,这标誌着产业正在转向压力控制。虽然轻型商用厢型车和乘用车的销售量不高,但欧盟安全法规和消费者对高阶驾驶辅助功能的偏好,正促使原始设备製造商(OEM)采用小型自动化气动模组。

2024年,公路轮胎将占汽车自动轮胎充气系统市场收入的72.41%,主要受跨洲卡车运输的推动,在这种运输中,每行驶一英里,轮胎充气不足都会降低燃油经济性。自动充气系统会持续调整冷态充气水平,不受环境波动的影响,而传统的每週例行检查可能会导致轮胎长期充气不足。车队远端资讯处理仪錶板整合了轮胎充气压力KPI和运行时间显示,使管理人员能够根据与柴油消费量直接相关的遵从率对各仓库进行基准测试。

非公路轮胎的复合年增长率为12.29%,这反映了对采石、林业和农业智慧机械的投资。米其林的中央系统可根据土壤类型调整轮胎压力,从而将生产率提高高达4%,并节省10%的燃油。研究表明,适当的胎压可以将土壤压实深度减少高达三分之一,从而保护农田并减少耕作能耗。同样,轮式装载机操作员报告称,在实施闭合迴路压力系统后,与轮胎相关的停机时间有所减少,该系统可在侧壁夹伤发生前发出警告。儘管领先定价仍然是小型承包商的障碍,但这些优势巩固了未来的需求。

区域分析

由于清晰的法规结构和成熟的远端资讯处理技术,北美将在2024年占据汽车自动胎压系统市场的39.81%。联邦胎压法规正推动卡车运输公司采用自动化解决方案,以规避路边罚款。大型租赁车队表示,这些解决方案可节省1-3%的柴油,并延长15-20%的轮胎寿命,这些成果强化了董事会层面的永续性承诺。该地区还在大规模初步试验无人驾驶货运路线,自动驾驶开发商需要冗余的轮胎健康系统,使驾驶员免于维护。

亚太地区将迎来最快的成长速度,到2030年复合年增长率将达到12.19%。电子商务出货量的爆炸性增长、大规模的高速公路建设以及电动动力传动系统的推动,使汽车价格上涨的经济理由显而易见。印度的物流改革旨在减少与运输成本相关的12-14%的GDP损失,而胎压校正是一个显而易见的槓桿。一汽和中国重汽等中国主机厂正在将胎压阀整合到新能源卡车中,以延长电池续航里程,将汽车自动胎压系统市场定位为标准的效率衡量标准。

欧洲遵循并遵循欧盟的安全和环境指令。欧盟法规II强制所有新车安装胎压监测系统(TPMS),而欧7引入了磨损限制,该限制很大程度上取决于最佳胎压。德国和法国的业者正在将通膨数据与碳排放报告结合,以满足客户范围3的取证要求。儘管中东和非洲的整体采用率落后,但石油出口国正在投入大量基础设施资金升级专业车辆,即使服务中心密度落后,潜在需求也在成长。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 越来越多的车队注重降低燃料和轮胎磨损成本

- 全球轮胎安全法规更加严格

- 扩大车辆和货运活动

- 先进 TPMS 与互联平台的 OEM 集成

- 预测轮胎健康状况的自动驾驶卡车的需求

- 农业土壤保护转向气压管理

- 市场限制

- 前期成本高且整合复杂

- 严苛工作循环下的可靠性与维护问题

- 全球售后生态系统有限

- 联网 ATIS 中的网路安全漏洞

- 价值/供应链分析

- 监管状况

- 技术展望

- 五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模及成长预测

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中大型商用车

- 非公路用车(农业、建筑、军用)

- 按用途

- 公路车

- 越野轮胎

- 按销售管道

- OEM

- 售后市场

- 依产品类型

- 中央轮胎充气系统 (CTIS)

- 常规/轮端充气机

- 自供电轮毂充气机

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Aperia Technologies, Inc.

- Bridgestone Corporation

- Continental AG

- Goodyear Tire & Rubber Company

- Meritor, Inc.

- STEMCO Products Inc.

- CODA Development

- Denso Corporation

- Pressure Systems International, Inc.

- Dana Incorporated

- Michelin Group

- Hendrickson International

- ti.systems GmbH

- FTL Technology

- Parker Hannifin Corporation

- Haltec Corporation

- Trelleborg AB

- SKF Group

- Haldex AB

第七章 市场机会与未来展望

The automotive automatic tire inflation system market size registers a valuation of USD 0.82 billion in 2025 and is forecast to reach USD 1.33 billion by 2030, advancing at a 10.21% CAGR.

Growth reflects coordinated safety regulations, fleet cost-reduction imperatives, and tighter integration with connected-vehicle architectures. North American fleets must comply with 49 CFR 393.75 cold-inflation rules, while the European Union's General Safety Regulation II requires tire-pressure monitoring across all new vehicles, indirectly cementing demand for fully automatic inflation capabilities. Commercial fleets realize up to 1.4% fuel savings when tires remain at correct pressure, sharpening return on investment for automatic systems . In parallel, agricultural and construction equipment makers embed central pressure control to meet soil-conservation mandates and precision-farming needs, as seen in Fendt's VarioGrip that varies pressure from 8.7 to 36.3 PSI while in motion. Investment momentum is buoyed by venture funding, illustrated by Aperia Technologies' USD 45 million raise that targets hub-mounted self-powered inflators.

Global Automotive Automatic Tire Inflation System Market Trends and Insights

Rising Fleet Focus on Fuel and Tire-Wear Cost Reduction

Tire expenditures represent 15-20% of heavy-truck operating budgets, and under-inflation generates up to 95% of roadside tire failures. Pressure Systems International quantifies 1.4% mean fuel gains and 10% tire-life extension when automatic inflation is installed . Data-rich platforms deliver live pressure, temperature, and load information, letting dispatchers optimize speed profiles and maintenance windows. Long-haul carriers accrue the greatest absolute benefit because incremental savings compound across annual mileages that exceed 120,000 miles per tractor. Consequently, procurement teams embed total cost-of-ownership models that prioritize automatic inflation during tractor and trailer replacement cycles.

Stringent Global Tire-Safety Regulations

Worldwide statutes are elevating tire-maintenance discipline. The EU General Safety Regulation II, effective July 2024, mandates tire-pressure monitoring on every newly homologated vehicle category except M1, creating a universal baseline that encourages automatic inflation upgrades. Complementary Euro 7 rules set tire-abrasion caps with 2032 compliance deadlines . In the United States, Federal Motor Carrier Safety Administration inspectors enforce cold-inflation minimums during roadside checks, prompting large fleets to deploy automated systems to avoid citations. Similar provisions are cascading into South America and Southeast Asia as export-oriented OEMs harmonize with EU standards. As a result, fleet managers perceive automotive automatic tire inflation system market adoption as a compliance necessity that also unlocks operational savings.

High Upfront Cost and Integration Complexity

System packages range from USD 1,500 to USD 5,000 per vehicle. Retrofit projects add labor hours and potential downtime that many small carriers cannot absorb. Commercial tire dealers note budget-constrained operators delaying upgrades until capex cycles align, even though break-even analysis often shows payback inside 18 months. Training technicians, calibrating sensors, and harmonizing software with legacy electronic control units further slow adoption in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Commercial-Vehicle Parc and Freight Activity

- OEM Integration with Advanced TPMS and Connected Platforms

- Reliability and Maintenance Issues in Harsh Duty Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium and heavy commercial vehicles accounted for 66.82% of the automotive automatic tire inflation system market revenue in 2024, underscoring the sector's outsized influence on the automotive automatic tire inflation system market. Elevated annual mileage, multi-axle configurations, and fuel-spend sensitivity combine to produce compelling investment cases for automatic inflation. Remote diagnostics and over-the-air pressure calibration let dispatchers minimize roadside service calls and preserve delivery schedules. Adoption is now filtering into regional haul and final-mile trucks as OEMs standardize inflation ports and data protocols across model lines.

Off-highway equipment exhibits the sharpest trajectory at an 11.84% CAGR through 2030. Precision agriculture mandates gentle soil loading to protect yield, while construction and military vehicles require fast adjustments between asphalt, gravel, and mud. Fendt's in-cab VarioGrip toggles pressure inside seconds, boosting tractive efficiency and cutting compaction, and similar offerings from John Deere and CNH Industrial signal an industry shift toward embedded pressure control. Light commercial vans and passenger cars participate more modestly, yet EU safety rules and consumer preference for advanced driver-assistance features are nudging OEMs to incorporate scaled-down automatic inflation modules.

On-road tires secured 72.41% of the automotive automatic tire inflation system market revenue in 2024, anchored by cross-continental trucking, where under-inflation steals fuel economy on every highway mile. Automated systems continuously regulate cold-inflation levels regardless of ambient swings that might lead to chronic under-pressure in conventional weekly-check routines. Fleet telematics dashboards integrate pressure KPIs alongside hours-of-service readouts, and managers benchmark depots on compliance percentages that correlate directly with diesel spend.

Off-road tires are climbing at a 12.29% CAGR, reflecting investment in smart machinery for quarrying, forestry, and agriculture. Michelin's central system posts up to 4% productivity lifts and 10% fuel savings by tailoring pressure to soil type. Studies show that correct pressure can trim soil compaction depth by one-third, preserving arable land and reducing tillage energy. Similarly, wheel-loader operators report lower tire-related downtime after installing closed-loop inflation that alerts them before sidewall pinch damage occurs. These benefits cement future demand even as upfront pricing remains a barrier for smaller contractors.

The Automotive Automatic Tire Inflation System Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (On-The-Road Tires and Off-The-Road Tires), Sales Channel (OEM and Aftermarket), Product Type (Central Tire Inflation Systems (CTIS), Continuous/Wheel-End Inflators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America secured 39.81% revenue of the automotive automatic tire inflation system market in 2024, buoyed by well-defined regulatory frameworks and mature telematics penetration. Federal enforcement of tire-pressure rules prompts carriers to adopt automatic solutions as insurance against roadside fines. Large for-hire fleets cite 1-3% diesel savings and 15-20% tire-life gains, outcomes that reinforce board-level sustainability pledges. The region also hosts expansive pilots for driverless freight corridors, and autonomous developers require redundant tire-health systems that remove the driver from the maintenance loop.

Asia-Pacific posts the quickest ascent at 12.19% CAGR through 2030. Explosive e-commerce shipping volumes, extensive highway build-outs, and the push for electrified powertrains sharpen the economic rationale for automatic inflation. India's logistics overhaul seeks to trim the 12-14% GDP drain tied to freight costs, and correcting tire pressure is a visible lever. Chinese OEMs such as FAW and Sinotruk integrate inflation valves on new energy trucks to extend battery range, positioning the automotive automatic tire inflation system market as a standard efficiency measure.

Europe remains consistent, guided by Union-wide safety and environmental directives. Regulation II obliges TPMS on every new vehicle, and Euro 7 introduces abrasion limits that depend heavily on optimum pressure. Operators in Germany and France combine inflation data with carbon reporting to satisfy customer Scope 3 disclosure requests. The Middle East and Africa trail in overall penetration, yet oil-exporting economies funnel infrastructure funds into vocational fleet upgrades, which lifts baseline demand even if service-center density lags.

- Aperia Technologies, Inc.

- Bridgestone Corporation

- Continental AG

- Goodyear Tire & Rubber Company

- Meritor, Inc.

- STEMCO Products Inc.

- CODA Development

- Denso Corporation

- Pressure Systems International, Inc.

- Dana Incorporated

- Michelin Group

- Hendrickson International

- ti.systems GmbH

- FTL Technology

- Parker Hannifin Corporation

- Haltec Corporation

- Trelleborg AB

- SKF Group

- Haldex AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising fleet focus on fuel and tire-wear cost reduction

- 4.2.2 Stringent global tire-safety regulations

- 4.2.3 Expanding commercial?vehicle parc and freight activity

- 4.2.4 OEM integration with advanced TPMS and connected platforms

- 4.2.5 Autonomous-trucking demand for predictive tire health

- 4.2.6 Agricultural shift to on-the-go soil-conserving pressure control

- 4.3 Market Restraints

- 4.3.1 High upfront cost and integration complexity

- 4.3.2 Reliability and maintenance issues in harsh duty cycles

- 4.3.3 Limited global aftermarket service ecosystem

- 4.3.4 Cyber-security vulnerabilities in connected ATIS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.1.4 Off-Highway Vehicles (Agricultural, Construction, Military)

- 5.2 By Application

- 5.2.1 On-the-Road Tires

- 5.2.2 Off-the-Road Tires

- 5.3 By Sales Channel

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Product Type

- 5.4.1 Central Tire Inflation Systems (CTIS)

- 5.4.2 Continuous/Wheel-End Inflators

- 5.4.3 Self-Powered Hub Inflators

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Aperia Technologies, Inc.

- 6.4.2 Bridgestone Corporation

- 6.4.3 Continental AG

- 6.4.4 Goodyear Tire & Rubber Company

- 6.4.5 Meritor, Inc.

- 6.4.6 STEMCO Products Inc.

- 6.4.7 CODA Development

- 6.4.8 Denso Corporation

- 6.4.9 Pressure Systems International, Inc.

- 6.4.10 Dana Incorporated

- 6.4.11 Michelin Group

- 6.4.12 Hendrickson International

- 6.4.13 ti.systems GmbH

- 6.4.14 FTL Technology

- 6.4.15 Parker Hannifin Corporation

- 6.4.16 Haltec Corporation

- 6.4.17 Trelleborg AB

- 6.4.18 SKF Group

- 6.4.19 Haldex AB

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽车自动胎压调节系统市场:按类型、组件、轮胎类型、车辆类型、最终用户和分销管道划分 - 全球预测 2026-2032

汽车自动胎压调节系统市场:按类型、组件、轮胎类型、车辆类型、最终用户和分销管道划分 - 全球预测 2026-2032 汽车轮胎充气机市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)

汽车轮胎充气机市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035) 汽车自动胎压调节系统市场规模、份额及成长分析(依车辆类型、类型、销售管道及地区划分)-2026-2033年产业预测

汽车自动胎压调节系统市场规模、份额及成长分析(依车辆类型、类型、销售管道及地区划分)-2026-2033年产业预测 汽车自动轮胎充气系统市场 - 全球产业规模、份额、趋势、机会和预测,按类型、销售管道、车辆类型、地区和竞争格局划分,2020-2030 年预测

汽车自动轮胎充气系统市场 - 全球产业规模、份额、趋势、机会和预测,按类型、销售管道、车辆类型、地区和竞争格局划分,2020-2030 年预测 全球汽车轮胎充气机市场

全球汽车轮胎充气机市场 自动轮胎充气系统市场(按类型、组件、车辆类型和地区)2026 年至 2032 年

自动轮胎充气系统市场(按类型、组件、车辆类型和地区)2026 年至 2032 年 汽车自动轮胎充气系统市场规模、份额、趋势分析报告:按类型、按车辆、按组件、按销售管道、按地区、细分市场预测,2024-2030年

汽车自动轮胎充气系统市场规模、份额、趋势分析报告:按类型、按车辆、按组件、按销售管道、按地区、细分市场预测,2024-2030年