|

市场调查报告书

商品编码

1842515

钻孔机:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Drilling Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

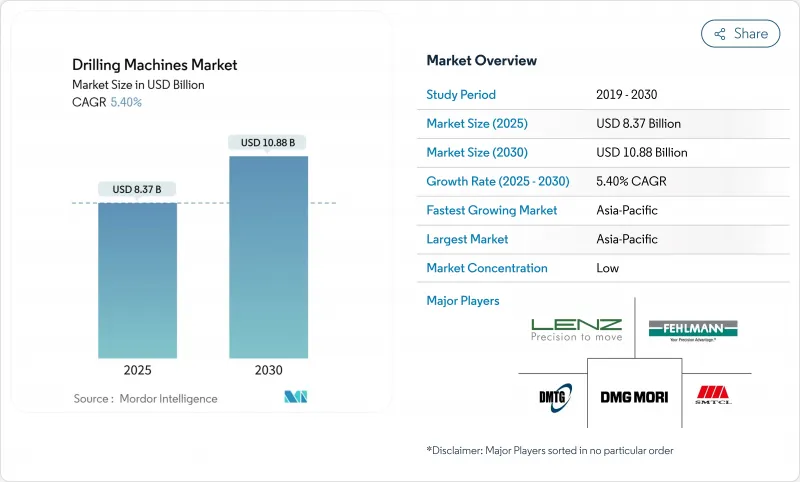

预计 2025 年钻孔机市场价值将达到 83.7 亿美元,到 2030 年将达到 108.8 亿美元,复合年增长率为 5.40%。

成长与电动车电池生产线对高精度、多主轴的需求、商用航太生产的復苏以及风力发电机零件产能的扩大息息相关。在大宗商品持续波动的背景下,持续的自动化、轻质材料使用的增加以及对深孔、大直径加工的需求正在推动资本投资。儘管石油和天然气应用领域存在短期采购犹豫,但电池製造商、变速箱供应商和造船厂的增加投资仍维持着设备积压。领先的供应商正在扩展改装服务和数位化套件,以填补熟练操作员的短缺,并在技术要求高的竞标中脱颖而出。

全球钻孔机市场趋势与洞察

电动车和可再生能源製造业的快速成长需要高精度多轴钻孔

由于电池组组装对孔公差的要求达到亚微米级别,电池供应商正在指定能够在高产量下保持刚性的多主轴系统。各大电池集团正在整合闭合迴路扭力工具和3D定位系统,以控制扣夹力变化并保护电极对准,同时提高年度生产线产能。类似的精度门槛也正在转向太阳能追踪器支架和机舱轮毂,在这些应用中,必须在不影响疲劳性能的情况下对轻质铝型材进行钻孔。设备供应商正在透过在主轴头上安装硬体安装振动感测器,并搭配可在毫秒内调整进给速度的边缘运算模组来应对此需求。亚太地区的需求最为强劲,但欧洲超级工厂和北美公用事业规模的太阳能发电场也需要类似的能力。

商业航太生产的加速推动了对大型径向机器的需求

Airframe Prime 正在将其单通道飞机计划恢復到每月 60 架,并更新了竞标,该钻机可在一次设置过程中切割钛框架构件。五轴自动化和托盘共享允许以更少的工位移动机身部分,同时保持 25 微米的位置重复精度。数位孪生现在将即时扭力和推力数据输入製造执行系统,在铆钉错位之前标记工具磨损异常。这种方法对于永续性认证至关重要,因为减少材料废料可以直接减少范围 3排放。虽然北美 Tear-On 仍然处于领先地位,但欧盟航空结构供应商也正在效仿扩大产能,以实现订单的恢復目标。

大宗商品投资週期削弱资本设备订单

平均而言,油田服务公司会在原油价格超过损益平衡点时增加工具机采购,但当价格下跌时,他们会迅速延后采购。因此,钻井承包商在产能过剩和维护延期之间摇摆不定,导致设备製造商的报价週期难以预测。中游加工厂也反映了这种节奏,将采购承诺推迟到最终投资决策做出时。外汇波动为以美元采购设备的拉丁美洲矿业公司带来了额外的不确定性。这导致销售管道变长,供应商需要增加营运资金(例如备件和演示设备),以确保快速週转的订单。

細項分析

径向铣床因其在汽车底盘、通用机械和中型铸件等应用领域的多功能性,在2024年创造了最大的收益。立式铣床和车削中心占据32.45%的市场份额,支援生产单元以均衡的触觉流程完成矩形零件。由于汽车原始设备製造商继续供应量产车型,而钢製和铁製转向节属于径向生产能力范围,因此需求仍然强劲。然而,深孔/BTA子集的成长速度最快,复合年增长率达到6.8%,这得益于大直径能源零件、压力容器管板和航太机翼樑的广泛应用。买家表示,他们转换该子集的原因是每个孔的循环时间更短、冷却液输送更佳以及自动排屑排放。

复杂的推拉式工具和严格的同心度要求,使得这个细分市场拥有更高的利润空间。跨国国防造船厂和海上齿轮箱联合体正在选择龙门式配置,以便在进程内恢復热变形。可携式磁力钻和微型钻机丛集为电子设备和现场服务管道提供了紧凑且可快速重新部署的单元。虽然这些设备在钻机市场中只占很小的份额,但它们在感测器融合和电池模组方面具有开创性,并随后进入了更重型的领域,从而形成了技术的良性循环。

由于入门成本低且易于维护,手动钻机仍占已安装基数的45.65%。加工车间处理混合批次的维修工作,夹具周转率率高于週期效率,因此手动主轴和机械限位器仍然具有吸引力。儘管如此,随着大型按图生产工厂进行现代化改造以满足可追溯性要求并弥补劳动力缺口,数控/自动化系统的复合年增长率最高,达到7.3%。机器製造商正在将程式码模拟、刀具寿命仪錶板和车间MES连结捆绑为标准配置,而不是付费附加元件。

半自动格式构成中阶,将液压进给与操作员监控结合。半自动格式构成中阶层,将液压进给与操作员监控相结合,在定制重型设备生产线中表现出色,这些生产线的几何形状会随批次变化,且切削深度保持较高。物联网主轴探头安装在復古立柱上,并将振动和推力数据发送到云分析,从而从沉没资产中获取额外运转率。此类改造透过在已经折旧免税额的硬体上增加订阅软体收益来扩大钻机市场。

区域分析

预计到2024年,亚太地区将占销售额的46.76%,到2030年将维持7.1%的复合年增长率。受政府鼓励国产数控系统(CNC)的政策推动,中国工具机园区持续扩张。日本製造商正在东协地区实现零件加工本地化,以规避外汇风险。印度製造群也在与生产挂钩的激励措施下进行现代化升级。单元工厂、离岸风力发电和地铁车辆铸造厂的兴起将保持较高的主轴运转率,并增加维修和改装机会。

北美的设备基础技术先进,但在大宗商品价格下跌的周期中却未被充分利用。回流奖励和清洁能源税额扣抵正在提振高端製造商的订单,为航空航天桁条和电池模组托架的新型复合材料电池提供了保障。加拿大石化工厂和美国航太墨西哥湾沿岸的造船厂正在升级为液压深孔钻机,以支持液化天然气(LNG)的扩张,从而稳定了大型钻机的市场规模,使其不受週期性钻机数量的影响。

欧洲正走向成熟,但正转向零排放强制标准,加速淘汰传统的三轴钻孔机,转而采用配备线上功率分析仪的伺服电动龙门架。一家德国整合商正在测试一种预测性润滑演算法,可将风电塔法兰生产线的非计划性停机时间减少12%。一家南欧造船厂正在竞标一台6公尺行程的大直径立柱机,该机器能够一次生产镀锌舱壁贯穿件,用于船舶翻新。

在中东和非洲,预计钻机需求将成长31%,这得益于阿联酋自升式钻井平台的维修以及沙乌地阿拉伯製造业村为配合「2030愿景」钢铁计画而进行的场地升级。撒哈拉以南非洲地区铁路基础设施的现代化建设,推动了对能够在现场条件下加工轨道接头的移动式磁力钻的需求。在南美洲,巴西的盐层下开发和阿根廷的页岩油田开发处于领先地位,需要配备高扭矩液压钻床的管道修整车间。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 电动车和可再生能源製造业的快速成长需要高精度多轴钻孔

- 商业航太生产的加速推动了对大型径向机器的需求

- 全球风力发电机齿轮箱产能扩张刺激深孔钻探投资

- 现场模组化施工的兴起促进了可携式磁力钻的采用

- 全球国防造船计划强制要求本地化

- 上游油田修井维修增加对大型工具的需求

- 市场限制

- 大宗商品投资週期抑制资本设备订单

- 全球数控操作员和机械师技能短缺

- 复杂形状的积层製造替代方案

- 五轴钻孔中心对于中小型企业来说初始成本较高

- 价值/供应链分析

- 监理展望

- 科技趋势

- 製造业展望

- 产业吸引力—五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按类型

- 旋臂钻床

- 立式/立柱式/支柱式钻床

- 敏感/桌上型钻床

- 排钻孔机

- 深孔/BTA 和枪钻机

- 可携式钻孔机

- 转塔钻床

- 其他(磁力钻、微型钻、专用钻孔机)

- 按操作

- 手动型

- 半自动

- 数控/自动

- 按技术/动力来源

- 机械/电动式

- 油压

- 气压

- 按最终用户产业

- 车

- 航太/国防

- 加工和工业机械

- 建造

- 石油、天然气和能源

- 电子和电气

- 造船/海洋

- 其他最终用户(重型机械、医疗设备等)

- 按工作材质

- 金属

- 复合材料、聚合物和塑料

- 木头

- 其他(陶瓷、玻璃、混凝土等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘鲁

- 其他南美

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- Nordix(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东协(印尼、泰国、菲律宾、马来西亚、越南)

- 其他亚太地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- DMG MORI Co. Ltd.

- Mazak Corporation

- Okuma Corporation

- Haas Automation Inc.

- Doosan Machine Tools Co. Ltd.

- Makino Milling Machine Co. Ltd.

- Dalian Machine Tool Group Co. Ltd.

- SMTCL(Shenyang Machine Tool)

- Tongtai Machine & Tool Co. Ltd.

- Hurco Companies Inc.

- ERNST LENZ Maschinenbau GmbH

- Fehlmann AG

- Gate Machinery International Ltd.

- Kaufman Manufacturing Company

- DATRON AG

- Scantool Group

- Taiwan Winnerstech Machinery Co. Ltd.

- Roku-Roku Co. Ltd.

- Hsin Geeli Hardware Enterprise Co. Ltd.

- Minitool Inc.

- LTF SpA*

第七章 市场机会与未来展望

The Drilling Machines Market was valued at USD 8.37 billion in 2025 and is forecast to reach USD 10.88 billion by 2030, advancing at a 5.40% CAGR.

Growth is tied to high-precision, multi-spindle requirements in electric-vehicle battery lines, recovering commercial aerospace output, and expanding wind-turbine component capacity. Continued automation, wider use of lightweight materials, and demand for deep-hole, large-radial formats keep capital expenditures on track even as commodity volatility persists. Rising investments by battery producers, gearbox suppliers, and shipyards sustain equipment backlogs despite short-term procurement hesitancy in oil and gas applications. Major suppliers are broadening retrofit services and digital suites to offset skilled-operator scarcity and differentiate in technically demanding bids.

Global Drilling Machines Market Trends and Insights

Surge in EV & Renewable-Energy Manufacturing Requiring High-Precision Multi-Spindle Drilling

Battery pack assembly now demands sub-micron hole tolerances, pushing cell suppliers to specify multi-spindle systems that can maintain rigidity at elevated throughput. Leading battery groups have integrated closed-loop torque tools and 3-D positioning to control clamp-force variation, lifting annual line capacity while safeguarding electrode alignment. Similar precision thresholds are migrating into solar-tracker mounts and nacelle hubs, where lightweight aluminum sections must be drilled without compromising fatigue performance. Equipment vendors have reacted by hard-mounting vibration sensors in spindle heads and pairing them with edge-computing modules that adjust feed rates in milliseconds. Demand is strongest in the Asia-Pacific corridor, but European gigafactories and North American utility-scale solar yards also seek identical capabilities.

Accelerating Commercial Aerospace Production Boosting Demand for Large Radial Machines

Airframe primes are ramping single-aisle programs back to 60 aircraft per month, renewing tenders for long-reach radial drills that cut titanium frame members in one-setup passes. Five-axis automation and pallet pools allow fuselage sections to move through fewer stations while sustaining 25 µm positional repeatability. Digital twins now feed real-time torque and thrust data to manufacturing execution systems, flagging tool-wear anomalies before rivet misalignment can occur. The approach is critical for sustainability credentials, as material scrap reductions directly lower Scope 3 emissions. North American tier-ones remain the pacesetters, yet EU aerostructure suppliers are mirroring capacity additions to meet backlog recovery targets.

Commodity-Investment Cyclicality Dampening Capital Equipment Orders

Oil-field service firms expand machine-tool fleets when crude averages above breakeven, yet they swiftly defer procurement under price dips. Drilling contractors, therefore, swing between over-capacity and deferred maintenance, creating unpredictable quoting cycles for machine builders. Mid-stream fabrication yards mirror this rhythm, delaying purchase commitments until final investment decisions close. Currency swings add further uncertainty for Latin American miners sourcing dollar-denominated equipment. The result is elongated sales funnels requiring vendors to carry higher working capital in spares and demo fleets to capture short-window orders.

Other drivers and restraints analyzed in the detailed report include:

- Global Expansion of Wind-Turbine Gearbox Capacity Spurring Deep-Hole Drill Investments

- Rise of On-Site Modular Construction Fueling Portable Magnetic Drill Adoption

- Global CNC-Operator and Machinist Skill Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radial machines generated the largest revenue in 2024 on the strength of their versatility across automotive chassis, general machinery, and medium-sized casting work. At a 32.45% share, they anchor production cells that pair vertical mills and turning centers to complete prismatic components in balanced takt flows. Demand remains buoyant as vehicle OEMs still deliver volume models whose steel and iron knuckles fall within radial capacity envelopes. Yet the deep-hole/BTA subset is rising fastest, logging a 6.8% CAGR amid broader adoption in large-bore energy parts, pressure-vessel tube sheets, and aerospace wing spars. Buyers cite lower per-hole cycle times, improved coolant delivery, and automated chip evacuation as reasons for switching.

The niche commands incremental premium margins, given its complex push-pull tooling and tight concentricity specifications. Multinational defense yards and offshore gearbox consortiums opt for gantry configurations able to reclaim heat distortion in-process. Portable magnetic and micro-drill clusters round out the category, feeding electronics and field-service channels with compact units amenable to fast redeployment. These variants, though a smaller slice of the drilling machines market, pioneer sensor fusion and battery modules that later migrate to heavier classes, creating a virtuous technology loop.

Manual rigs still occupy 45.65% of the installed base thanks to low entry costs and simple maintenance. Job-shops handle mixed-lot repair work where fixture turnover outweighs cycle efficiency, preserving the appeal of hand-feed quills and mechanical depth stops. Nevertheless, CNC/automatic systems chart the steepest 7.3% CAGR as large build-to-print houses modernize to meet traceability mandates and mitigate labor gaps. Machine builders bundle code simulation, tool-life dashboards, and shop-floor MES links as standard rather than chargeable add-ons.

Semi-automatic formats form an intermediate tier, marrying hydraulic feeds to operator supervision. They thrive in custom heavy-equipment lines where geometry changes every batch, yet cut depths stay high. Digital retrofits further blur lines; IoT spindle probes mounted on vintage columns broadcast vibration and thrust data to cloud analytics, squeezing extra utilization from sunk assets. Such retrofits enlarge the drilling machines market by inserting subscription software revenue atop hardware already depreciated.

The Drilling Machines Market is Segmented by Type (Radial Drilling Machines, and Others), by Operation (Manual, and Others), by Technology / Power Source (Mechanical, and Others), by End-User Industry (Automotive, and Others), by Work-Piece Material (Metals, and Others), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 46.76% of 2024 revenue and is projected to maintain a robust 7.1% CAGR through 2030. China's machine-tool park continues to swell, propelled by state incentives for domestic CNC controllers that challenge entrenched foreign incumbents. Japanese builders localize component machining across ASEAN to blunt currency risks, while Indian fabrication clusters modernize under Production-Linked Incentive schemes. Rising cell factories, offshore wind yards, and metro-car foundries keep spindle utilization high, lifting service and retrofit opportunities.

North America's installed base remains technologically advanced yet underutilized in commodity down-cycles. Reshoring incentives and clean-energy tax credits now underwrite new composite-capable cells for aerospace stringers and battery-module carriers, brightening order books for high-end builders. Canada's petrochemical plants and U.S. Gulf Coast yards upgrade to hydraulic deep-hole rigs to support LNG expansion, stabilizing the drilling machines market size for heavy-duty formats against cyclic rig counts.

Europe, though mature, pivots toward zero-emission mandates, accelerating the retirement of legacy 3-axis drills in favor of servo-electric gantries with in-line power analyzers. German integrators test predictive greasing algorithms that cut unplanned downtime by 12% on wind-tower flange lines. Southern European shipyards, galvanized by naval-fleet renewal, tender for large-diameter column machines with 6-m stroke capacity to produce bulkhead penetrations in a single pass.

The Middle East and Africa anticipate a 31% uplift in drilling rig demand, translating into yard upgrades in UAE jack-up refurbishments and Saudi fabrication villages aligned with Vision 2030 steel programs. Sub-Saharan rail infrastructure modernizations call for mobile magnetic drills able to process track joints under field conditions. South American prospects center on Brazilian pre-salt developments and Argentine shale growth, which both require tubular dressing shops equipped with high-torque hydraulic drill presses.

- DMG MORI Co. Ltd.

- Mazak Corporation

- Okuma Corporation

- Haas Automation Inc.

- Doosan Machine Tools Co. Ltd.

- Makino Milling Machine Co. Ltd.

- Dalian Machine Tool Group Co. Ltd.

- SMTCL (Shenyang Machine Tool)

- Tongtai Machine & Tool Co. Ltd.

- Hurco Companies Inc.

- ERNST LENZ Maschinenbau GmbH

- Fehlmann AG

- Gate Machinery International Ltd.

- Kaufman Manufacturing Company

- DATRON AG

- Scantool Group

- Taiwan Winnerstech Machinery Co. Ltd.

- Roku-Roku Co. Ltd.

- Hsin Geeli Hardware Enterprise Co. Ltd.

- Minitool Inc.

- LTF SpA*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV & Renewable-Energy Manufacturing Requiring High-Precision Multi-Spindle Drilling

- 4.2.2 Accelerating Commercial Aerospace Production Boosting Demand for Large Radial Machines

- 4.2.3 Global Expansion of Wind-Turbine Gearbox Capacity Spurring Deep-Hole Drill Investments

- 4.2.4 Rise of On-Site Modular Construction Fueling Portable Magnetic Drill Adoption

- 4.2.5 Localization Mandates in Defense Shipbuilding Programs Worldwide

- 4.2.6 Upstream Oilfield Revamps Increasing Demand for Heavy-Duty Tooling

- 4.3 Market Restraints

- 4.3.1 Commodity-Investment Cyclicality Dampening Capital Equipment Orders

- 4.3.2 Global CNC-Operator and Machinist Skill Shortage

- 4.3.3 Substitution by Additive Manufacturing for Complex Geometries

- 4.3.4 High Up-Front Cost of 5-Axis Drilling Centers for Small & Medium Enterprises

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Trends

- 4.7 Manufacturing-Sector Outlook

- 4.8 Industry Attractiveness - Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Type

- 5.1.1 Radial Drilling Machines

- 5.1.2 Upright/Column/ Pillar Drilling Machines

- 5.1.3 Sensitive/Bench Drilling Machines

- 5.1.4 Gang Drilling Machines

- 5.1.5 Deep-Hole/BTA & Gun Drilling Machines

- 5.1.6 Portable Drilling Machines

- 5.1.7 Turret Drilling Machines

- 5.1.8 Others (Magnetic, Micro/Mini Drilling, Special-Purpose Drilling Machines)

- 5.2 By Operation

- 5.2.1 Manual

- 5.2.2 Semi-Automatic

- 5.2.3 CNC/Automatic

- 5.3 By Technology / Power Source

- 5.3.1 Mechanical/Electric

- 5.3.2 Hydraulic

- 5.3.3 Pneumatic

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace & Defense

- 5.4.3 Fabrication & Industrial Machinery

- 5.4.4 Construction

- 5.4.5 Oil & Gas and Energy

- 5.4.6 Electronics & Electricals

- 5.4.7 Shipbuilding & Marine

- 5.4.8 Other End-users (Heavy Equipment, Medical Devices, etc.)

- 5.5 By Work-piece Material

- 5.5.1 Metals

- 5.5.2 Composites, Polymers & Plastics

- 5.5.3 Wood

- 5.5.4 Others (Ceramics, Glass, Concrete, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Peru

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Qatar

- 5.6.5.4 Kuwait

- 5.6.5.5 Turkey

- 5.6.5.6 Egypt

- 5.6.5.7 South Africa

- 5.6.5.8 Nigeria

- 5.6.5.9 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DMG MORI Co. Ltd.

- 6.4.2 Mazak Corporation

- 6.4.3 Okuma Corporation

- 6.4.4 Haas Automation Inc.

- 6.4.5 Doosan Machine Tools Co. Ltd.

- 6.4.6 Makino Milling Machine Co. Ltd.

- 6.4.7 Dalian Machine Tool Group Co. Ltd.

- 6.4.8 SMTCL (Shenyang Machine Tool)

- 6.4.9 Tongtai Machine & Tool Co. Ltd.

- 6.4.10 Hurco Companies Inc.

- 6.4.11 ERNST LENZ Maschinenbau GmbH

- 6.4.12 Fehlmann AG

- 6.4.13 Gate Machinery International Ltd.

- 6.4.14 Kaufman Manufacturing Company

- 6.4.15 DATRON AG

- 6.4.16 Scantool Group

- 6.4.17 Taiwan Winnerstech Machinery Co. Ltd.

- 6.4.18 Roku-Roku Co. Ltd.

- 6.4.19 Hsin Geeli Hardware Enterprise Co. Ltd.

- 6.4.20 Minitool Inc.

- 6.4.21 LTF SpA*

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

爆破钻机市场:依钻孔方法、功率、零件和终端用户产业划分-2026-2032年全球预测立式多组钻孔机市场:依机器类型、最终用户、应用、钻孔深度、功率、钻孔技术、机器移动性、销售管道,全球预测,2026-2032年多联钻床市场:按类型、主轴数量、驱动系统、应用、最终用户、分销管道划分,全球预测(2026-2032年)自动多组钻孔机市场:依最终用户、类型、应用、组件和操作模式划分,全球预测,2026-2032年

爆破钻机市场:依钻孔方法、功率、零件和终端用户产业划分-2026-2032年全球预测立式多组钻孔机市场:依机器类型、最终用户、应用、钻孔深度、功率、钻孔技术、机器移动性、销售管道,全球预测,2026-2032年多联钻床市场:按类型、主轴数量、驱动系统、应用、最终用户、分销管道划分,全球预测(2026-2032年)自动多组钻孔机市场:依最终用户、类型、应用、组件和操作模式划分,全球预测,2026-2032年 隧道和岩石钻孔设备市场规模、份额和成长分析:按动力来源、控制系统、设备类型、应用、地区和产业预测,2026-2033年便携式二氧化碳玻璃冷却器市场:按产品类型、容量、价格范围、应用、最终用户和分销管道划分,全球预测(2026-2032年)玻璃钻孔机市场按类型、钻孔技术、机器尺寸、应用和终端用户产业划分-全球预测,2026-2032年钻桿机械市场按类型、钻井深度、功率、应用和最终用户划分,全球预测,2026-2032年

隧道和岩石钻孔设备市场规模、份额和成长分析:按动力来源、控制系统、设备类型、应用、地区和产业预测,2026-2033年便携式二氧化碳玻璃冷却器市场:按产品类型、容量、价格范围、应用、最终用户和分销管道划分,全球预测(2026-2032年)玻璃钻孔机市场按类型、钻孔技术、机器尺寸、应用和终端用户产业划分-全球预测,2026-2032年钻桿机械市场按类型、钻井深度、功率、应用和最终用户划分,全球预测,2026-2032年 日本钻井设备市场:规模、份额、趋势和预测:按类型、类别、动力来源、安装方式、分销管道、最终用途和地区划分(2026-2034 年)

日本钻井设备市场:规模、份额、趋势和预测:按类型、类别、动力来源、安装方式、分销管道、最终用途和地区划分(2026-2034 年) 2026年全球岩石开挖设备市场报告

2026年全球岩石开挖设备市场报告