|

市场调查报告书

商品编码

1842516

vEPC(虚拟化演进分组核心):市场占有率分析、产业趋势、统计、成长预测(2025-2030 年)Virtualized Evolved Packet Core - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

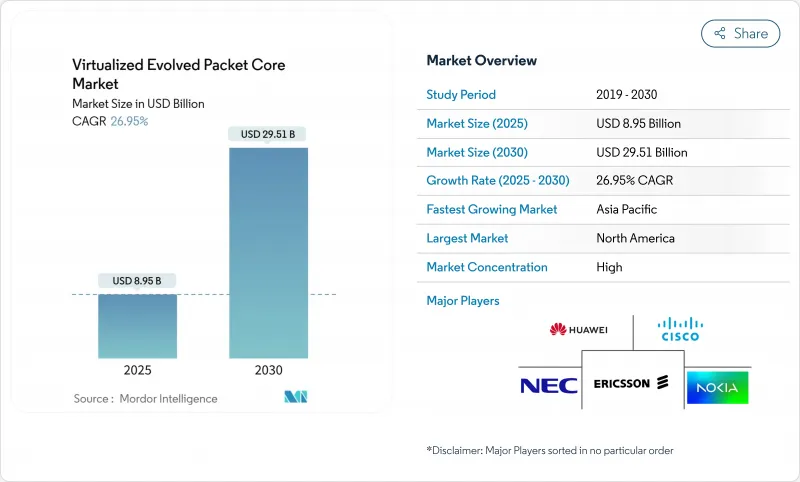

虚拟化演进分组核心 (vEPC) 市场规模预计在 2025 年为 89.5 亿美元,预计到 2030 年将达到 295.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 26.95%。

5G独立组网的部署、企业对私有行动网路日益增长的需求,以及通讯业者对节能虚拟化核心网路的永续性发展要求,共同推动此成长。通讯业者正在加速软体定义网路功能,以降低资本支出和营运支出,而超大规模公有公共云端伙伴关係则有助于加快服务发布和全球覆盖范围。亚太地区在政府支持的数位化计画的支持下,正在推动其应用,而北美地区则透过网路切片和边缘云端的协同效应,推动差异化发展。同时,在欧洲,对合规性和能源效率的关注正在影响技术需求和供应商选择。

全球 vEPC(虚拟化演进分组核心)市场趋势与洞察

加速 5G 部署需要云端原生核心

云端原生、以服务为基础的架构对于真正的 5G 独立组网至关重要,这使得 vEPC 对于追求网路切片和高阶服务的营运商而言成为一项不可或缺的投资。爱立信已于 2024 年底获得超过 120 个 5G 商用核心网合同,并在全球范围内为 37 个 5G SA 现网提供支持,这为其商用准备就绪提供了有力证据。 T-Mobile 等参与企业已利用全国范围的 5G SA 推出网路切片视讯通话,并建立了差异化的定价模式。竞争压力将迫使通讯业者加速现代化转型,否则将面临流失风险。云端原生核心网路还能让规模较小的行动虚拟网路营运商快速进入企业物联网领域。因此,vEPC(虚拟化演进分组核心)市场将在短期内经历一个良莠不齐的采用週期。

透过网路功能虚拟化节省资本支出/营运支出

随着 vEPC 设定将工作负载转移到商用硬体和共用云端资源,营运商的成本节省显着提升。研究表明,与单晶片硬体核心相比,vEPC 的资本支出减少了 68%,营运成本降低了 67%。在迁移到基于意图的虚拟化核心自动化营运后,Digital Nasional Berhad 的网路执行时间达到了 99.8%,客户投诉解决时间缩短了 90%。节能措施进一步提高了 22% 的效率,实现了预算和永续性目标。加速服务发布将收益时间从一年多缩短到不到六个月。这些经济效益正在将 vEPC 从一项可选功能转变为董事会级投资计划中的必备功能。供应商目前正在整合 AI 驱动的编配,以进一步减少营运工作负载。

操作员对传统物理 EPC 的惯性

沉没投资和对关键任务风险的规避正在减缓虚拟化计画。英国的Three公司仅在被迫进行现代化升级时才更换其二手诺基亚CloudBand网络,凸显了其不愿中断稳定的流量。 Verizon拖延的5G SA推出表明,即使是创新领导者也难以应对迁移的复杂性。在成熟市场,监管审查的加强和严格的服务水准预期使变更管理更具挑战性。因此,实体核心的效用超过了其经济效益,抑制了vEPC(虚拟化演进分组核心)市场的短期成长动能。

报告中分析的其他驱动因素和限制因素

- 用于工业 4.0 和园区连接的私有 LTE/5G 网路

- 通讯业者在节能核心网路方面的永续性义务

- 多租户云端中的安全性和合规性问题

細項分析

到2024年,云端部署将占据虚拟化演进分组核心网路 (vEPC) 市场份额的63%,这反映了通讯业者对弹性扩展和快速服务迭代的偏好。随着超大规模营运商不断增强其通讯功能集,云端部署预计将以32%的复合年增长率成长,超越本地部署和混合部署。三星、TELUS和AWS建构了北美首个虚拟漫游网关,证明了跨境服务创新可以透过在公有公共云端上原生运行的控制平面元素蓬勃发展。这些案例凸显了从基础设施所有权到敏捷性的更广泛转变。

将资料在地化的营运商正在采用过渡性混合模式,以在不牺牲云端经济效益的情况下满足主权规则。爱立信的紧凑型分组核心网 (Compact Packet Core) 将部署复杂性降低了 80%,能耗降低了 30%,这使得云端就绪捆绑包对二级营运商具有吸引力。随着越来越多的合约指定基于结果的定价,vEPC(虚拟化演进分组核心网路)市场正在整合託管服务附加元件,例如人工智慧辅助营运。规模较小的区域通讯业者和行动虚拟网路营运商 (MVNO) 正在利用 SaaS 交付,在几週内(而非几季内)推出新产品,并扩大基本客群。

虚拟化演进分组核心 (vEPC) 市场报告按部署模式(云端、本地、混合)、应用程式(物联网和 M2M、行动专用网路 (MPN) 和 MVNO、宽频无线存取 (BWA)、LTE/VoLTE/VoWiFi、5G 非独立 (NSA) 核心、其他)、终端用户(标准和电信服务)、国际企业和电信服务供应商、区域和电信)、公共

区域分析

到2024年,亚太地区将占据虚拟化演进分组核心网 (vEPC) 市场规模的38%,这得益于中国目前已部署的5,325个5G专网,其中包括超过2万个工业用例。政府的奖励和频谱政策正在加速製造业的采用,北京方面已投资30亿美元用于5G-Advanced网络,力争2025年涵盖300个城市。印度5G SA覆盖率为52%,远高于欧洲的2%,显示新兴经济体正透过云端优先部署超越传统架构。这些专案为厂商提供了在地化研发和生产的规模,巩固了亚太地区在虚拟化演进分组核心网 (vEPC) 市场的领导地位。

在北美,营运商非常重视透过网路切片和 O-RAN 整合打造的高端服务层级。 Verizon 已部署超过 13 万个支援 O-RAN 的无线存取点,推出了基于切片的视讯通话,并获得了大量高价值用户。企业间的合作催生了重要的案例研究:宝马斯帕坦堡工厂透过采用私有 5G 提升了正常运作,三星、TELUS 和 AWS 则透过完全虚拟化的核心网展示了漫游创新。频宽租赁监管的明确性进一步支援了园区部署,并增强了区域对 vEPC(虚拟化演进分组核心网路)市场的贡献。

在欧洲,我们看到了好坏参半的发展动能。英国的Three 授予爱立信一份 9 Tbps 的云端原生核心合同,而 O2 Telefónica 在六个月内就突破了 100 万 AWS 託管核心用户。然而,受制于英国《电讯安全法》等严格的安全法规,以及优先考虑稳定性而非激进现代化的风险规避文化,5G SA 的整体可用性仍然只有 2%。通讯业者正专注于能源效率和开放式 RAN 实验,正如德国电信的 O-RAN Town 计划所示。虽然这些优先事项将限制短期支出,但它们将在 vEPC 市场中创造互通性、低功耗倡议演进分组核心 (vEPC) 解决方案的长期需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- LTE/4G用户快速成长

- 加速 5G 部署需要云端原生核心

- 透过网路功能虚拟化节省资本支出/营运支出

- 用于工业 4.0 和校园连接的私人 LTE/5G 网络

- 边缘云协同实现分散式用户平面卸载

- 通讯业者对节能核心网路的永续性要求

- 市场限制

- 操作员对传统物理 EPC 的惯性

- 多租户云端中的安全性和合规性问题

- 开放核心与隔离核心之间的互通性差距

- 5G SA 工作负载的超大规模云端 TCO 难以预测

- 价值/供应链分析

- 监管状况

- 技术展望

- 投资分析(按基准)

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模及成长预测

- 依部署类型

- 云端基础

- 本地部署

- 杂交种

- 按用途

- 物联网和 M2M

- 行动专用网路 (MPN) 和 MVNO

- 宽频无线存取(BWA)

- LTE/VoLTE/VoWiFi

- 5G非独立(NSA)核心

- 5G独立(SA)核心

- 按最终用户

- 通讯业者

- 按公司和行业

- 政府/公共

- 云端服务供应商

- MVNE/MVNO

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 义大利

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 其他亚太地区

- 中东和非洲

- 中东

- 海湾合作委员会国家

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- ZTE

- Samsung Electronics

- NEC Corporation

- Mavenir

- Microsoft(Affirmed Networks)

- Athonet(HPE)

- Telrad Networks

- Core Network Dynamics

- VMware

- Juniper Networks

- Red Hat(IBM)

- Intel

- Hewlett Packard Enterprise

- Casa Systems

- Parallel Wireless

- Druid Software

第七章 市场机会与未来展望

The Virtualized Evolved Packet Core Market size is estimated at USD 8.95 billion in 2025, and is expected to reach USD 29.51 billion by 2030, at a CAGR of 26.95% during the forecast period (2025-2030).

Growth stems from 5G standalone rollouts, rising enterprise demand for private mobile networks, and operator sustainability mandates that favor energy-efficient virtualized cores. Telcos accelerate software-defined network functions to slash capital and operating outlays, while hyperscale public-cloud partnerships allow rapid service launches and global coverage. Asia Pacific drives adoption on the back of government-backed digital programs, whereas North America pushes differentiation through network slicing and edge-cloud synergies. Meanwhile, Europe emphasizes compliance and energy efficiency, a stance that shapes technical requirements and vendor selection.

Global Virtualized Evolved Packet Core Market Trends and Insights

Accelerated 5G Rollouts Demanding Cloud-Native Cores

Cloud-native service-based architectures are mandatory for true 5G standalone networks, making vEPC a non-negotiable investment for operators pursuing network slicing and premium-tier services. Ericsson secured more than 120 commercial 5G core contracts by late 2024, powering 37 live 5G SA networks worldwide, providing tangible proof of commercial readiness. Early movers such as T-Mobile leveraged nationwide 5G SA to introduce network-slice-enabled video calling, which positions them for differentiated pricing models. Competitive pressure compels lagging carriers to accelerate modernization or risk churn. Cloud-native cores also give smaller mobile virtual network operators fast-track entry into enterprise IoT niches. Consequently, the Virtualized Evolved Packet Core market experiences a compounding adoption cycle in the short term.

CapEx/OpEx Savings from Network-Function Virtualization

Operators record sizeable cost reductions as vEPC setups shift workloads to commodity hardware and shared cloud resources. Studies show 68% lower capital outlays and 67% savings on operating expense versus monolithic hardware cores. Digital Nasional Berhad achieved 99.8% network uptime and cut customer-complaint resolution time by 90% after moving to intent-based automated operations on a virtualized core. Energy savings add a further 22% efficiency, meeting both budget and sustainability goals. Faster service launches shorten time-to-revenue from over a year to less than six months. These economics shift vEPC from optional to essential in board-level investment plans. Vendors now embed AI-powered orchestration to shrink operational workloads even further.

Operator Inertia Toward Legacy Physical EPCs

Sunk investments and mission-critical risk aversion slow virtualization plans. Three UK replaced Nokia's end-of-life CloudBand only when forced to modernize, underscoring reluctance to disrupt stable traffic flows. Verizon's protracted 5G SA launch shows that even innovation leaders grapple with migration complexity. Mature markets face elevated regulatory oversight and stringent service-level expectations, making change management even more difficult. As a result, physical cores persist for longer than their economic utility justifies, dampening short-term momentum in the Virtualized Evolved Packet Core market.

Other drivers and restraints analyzed in the detailed report include:

- Private LTE/5G Networks for Industry 4.0 and Campus Connectivity

- Telco Sustainability Mandates for Energy-Efficient Core Networks

- Security and Compliance Concerns on Multi-Tenant Cloud

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud implementations represented 63% of the Virtualized Evolved Packet Core market share in 2024, reflecting carriers' preference for elastic scaling and rapid service iteration. The cloud cohort is forecast to grow at 32% CAGR, outpacing on-premises and hybrid alternatives as hyperscalers strengthen telecom feature sets. Samsung, TELUS, and AWS created North America's first virtual roaming gateway, which proves that cross-border service innovations flourish when control-plane elements run natively on the public cloud. These examples underpin a broad shift where infrastructure ownership yields to agility.

Operators that retain data on-site embrace transitional hybrid models to satisfy sovereignty rules without forfeiting cloud economics. Ericsson's Compact Packet Core reduces deployment complexity by 80% and cuts energy use by 30%, making cloud-ready bundles attractive to tier-2 carriers. As more contracts stipulate outcome-based pricing, the Virtualized Evolved Packet Core market embeds managed-service add-ons such as AI-assisted operations. Small regional telcos and MVNOs leverage SaaS delivery to launch new offers in weeks rather than quarters, broadening the customer base.

The Virtualized Evolved Packet Core Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Application (IoT and M2M, Mobile Private Networks (MPN) and MVNO, Broadband Wireless Access (BWA), LTE/VoLTE/VoWiFi, 5G Non-Standalone (NSA) Core, and More), End-User (Telecom Operators, Enterprises and Industrial Verticals, Government and Public Safety, Cloud Service Providers, and MVNE/MVNOs), and Geography.

Geography Analysis

Asia Pacific generated 38% of the 2024 Virtualized Evolved Packet Core market size, supported by China's 5,325 live private 5G networks that include more than 20,000 industrial use cases. Government incentives and spectrum policies accelerate manufacturing adoption, with Beijing investing USD 3 billion in 5G-Advanced coverage across 300 cities in 2025. India's 52% 5G SA coverage, well ahead of Europe's 2%, illustrates how emerging economies leapfrog legacy architectures via cloud-first rollouts. These programs supply scale that compels vendors to localize R&D and production, reinforcing Asia Pacific's leadership in the Virtualized Evolved Packet Core market.

North America emphasizes premium service tiers through network slicing and O-RAN integration. Verizon deployed more than 130,000 O-RAN-capable radios and launched slice-based video calling to capture high-value subscribers. Enterprise alliances produce headline case studies: BMW's Spartanburg plant realized uptime gains after adopting private 5G, and Samsung, TELUS, and AWS demonstrated roaming innovation via fully virtualized cores. Regulatory clarity around spectrum leasing further supports campus deployments, bolstering regional contribution to the Virtualized Evolved Packet Core market.

Europe shows mixed momentum. Three UK awarded Ericsson a 9 Tbps cloud-native core contract, and O2 Telefonica surpassed 1 million users on its AWS-hosted core within six months. Yet overall 5G SA availability stands at 2%, restrained by strict security rules such as the UK Telecoms Security Act and by a risk-averse culture that favors stability over aggressive modernization. Operators focus on energy efficiency and open-RAN experimentation, evidenced by Deutsche Telekom's O-RAN Town initiative. These priorities temper immediate spending but create long-term demand for highly interoperable, low-power vEPC solutions within the Virtualized Evolved Packet Core market.

- Ericsson

- Huawei Technologies

- Nokia

- Cisco Systems

- ZTE

- Samsung Electronics

- NEC Corporation

- Mavenir

- Microsoft (Affirmed Networks)

- Athonet (HPE)

- Telrad Networks

- Core Network Dynamics

- VMware

- Juniper Networks

- Red Hat (IBM)

- Intel

- Hewlett Packard Enterprise

- Casa Systems

- Parallel Wireless

- Druid Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth in LTE/4G subscriber base

- 4.2.2 Accelerated 5G roll-outs demanding cloud-native cores

- 4.2.3 CapEx / OpEx savings from network-function virtualization

- 4.2.4 Private LTE/5G networks for Industry 4.0 and campus connectivity

- 4.2.5 Edge-cloud synergies enabling distributed user-plane off-load

- 4.2.6 Telco sustainability mandates for energy-efficient core networks

- 4.3 Market Restraints

- 4.3.1 Operator inertia toward legacy physical EPCs

- 4.3.2 Security and compliance concerns on multi-tenant cloud

- 4.3.3 Inter-operability gaps across open, disaggregated cores

- 4.3.4 Unpredictable hyperscale cloud TCO for 5G SA workloads

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Investment Analysis (Baseline-specific)

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-based

- 5.1.2 On-premise

- 5.1.3 Hybrid

- 5.2 By Application

- 5.2.1 IoT and M2M

- 5.2.2 Mobile Private Networks (MPN) and MVNO

- 5.2.3 Broadband Wireless Access (BWA)

- 5.2.4 LTE/VoLTE/VoWiFi

- 5.2.5 5G Non-Standalone (NSA) Core

- 5.2.6 5G Standalone (SA) Core

- 5.3 By End User

- 5.3.1 Telecom Operators

- 5.3.2 Enterprises and Industrial Verticals

- 5.3.3 Government and Public Safety

- 5.3.4 Cloud Service Providers

- 5.3.5 MVNE/MVNOs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Italy

- 5.4.3.6 Spain

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 GCC Countries

- 5.4.5.1.2 Turkey

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Egypt

- 5.4.5.2.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ericsson

- 6.4.2 Huawei Technologies

- 6.4.3 Nokia

- 6.4.4 Cisco Systems

- 6.4.5 ZTE

- 6.4.6 Samsung Electronics

- 6.4.7 NEC Corporation

- 6.4.8 Mavenir

- 6.4.9 Microsoft (Affirmed Networks)

- 6.4.10 Athonet (HPE)

- 6.4.11 Telrad Networks

- 6.4.12 Core Network Dynamics

- 6.4.13 VMware

- 6.4.14 Juniper Networks

- 6.4.15 Red Hat (IBM)

- 6.4.16 Intel

- 6.4.17 Hewlett Packard Enterprise

- 6.4.18 Casa Systems

- 6.4.19 Parallel Wireless

- 6.4.20 Druid Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

全球虚拟化演进封包核心网路市场规模、份额、趋势和成长分析报告(2026-2034)

全球虚拟化演进封包核心网路市场规模、份额、趋势和成长分析报告(2026-2034) 虚拟化演进封包核心网路市场 - 全球产业规模、份额、趋势、机会及预测(按组件类型、部署模式、最终用户、地区和竞争格局划分,2021-2031年)

虚拟化演进封包核心网路市场 - 全球产业规模、份额、趋势、机会及预测(按组件类型、部署模式、最终用户、地区和竞争格局划分,2021-2031年) 虚拟化演进封包核心网路市场规模、份额和成长分析(按产品、解决方案、服务、应用、网路、最终用户、部署类型和地区划分)—产业预测,2026-2033年

虚拟化演进封包核心网路市场规模、份额和成长分析(按产品、解决方案、服务、应用、网路、最终用户、部署类型和地区划分)—产业预测,2026-2033年 虚拟化演进封包核心网路市场:按组件、部署模式、最终用户产业、技术类型和组织规模划分 - 全球预测,2025-2032 年

虚拟化演进封包核心网路市场:按组件、部署模式、最终用户产业、技术类型和组织规模划分 - 全球预测,2025-2032 年 2025年虚拟演进封包核心网路全球市场报告

2025年虚拟演进封包核心网路全球市场报告 虚拟演进封包核心网路(VEPC) 全球市场,2024-2028 年

虚拟演进封包核心网路(VEPC) 全球市场,2024-2028 年