|

市场调查报告书

商品编码

1842570

压电元件:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Piezoelectric Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

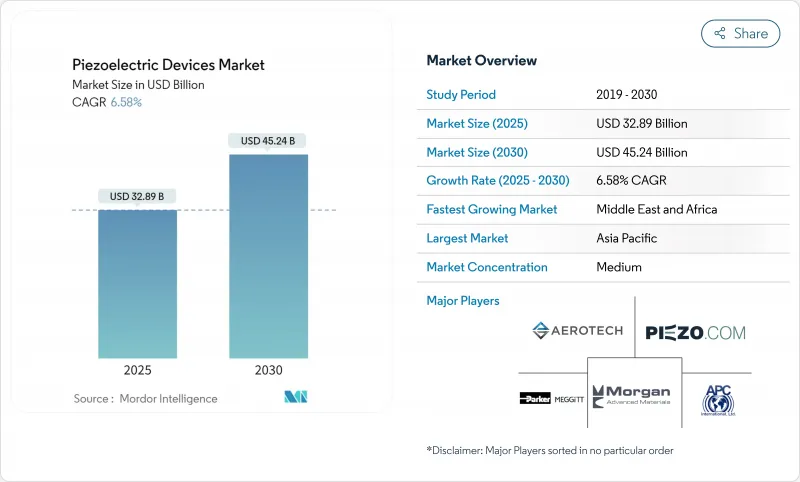

压电元件市场规模预计在 2025 年达到 329 亿美元,到 2030 年将增加至 452.4 亿美元,复合年增长率为 6.58%。

推动这一扩张的因素包括 5G RF 滤波器的小型化、汽车电气化的日益发展以及依赖坚固、节能的压电元件的工业 4.0维修。体声波滤波器中氮化铝钪的采用使智慧型手机频率能够达到 6 GHz 以上,而欧盟的无铅政策正在加速向铌酸钾钠和钛酸铋钠的转变,儘管它们的製造成本较高。亚太地区凭藉大规模消费性电子产品生产引领需求,而中东和非洲则因石油和天然气能源采集计划而经历快速成长。虽然 TDK、村田製作所和京瓷等垂直整合供应商确保上游材料和下游生产能力,缓和了竞争,但铌和锂的供应风险给国防和航太用户带来了不确定性。

全球压电市场趋势与洞察

5G智慧型手机压电MEMS射频滤波器的小型化(亚洲)

基于氮化铝钪的体声波滤波器现在可以实现 6 GHz 以上的频率,耦合因子比标准氮化铝高 40%,同时保持高达 400 度C 的热稳定性。这些进步将晶粒尺寸缩小至 0.83 x 0.75 mm2,并将插入损耗降低至 1.5 dB 以下,从而延长智慧型手机电池寿命。3D机械共振器进一步将多频段功能整合到单一晶片上,为超宽频连接创建可扩展的解决方案。亚洲的晶圆级密封硅共振器平台实现了超过 439 的品质因数,从而减少了製造流程和成本。加速的 6G 和毫米波计画将推动对超紧凑铌酸锂基滤波器晶片的需求,从而加强我们在亚太地区的技术领先地位。

用于欧洲高檔汽车燃油喷射和 ADAS 的电动压电致动器

采用铜电极的爱普科斯( EPCOS) 多层致动器在 170 度C下可承受超过 10 亿次操作,性能比银钯执行器提高 20%。 Denso 的 i-ART 系统将微处理器与压电喷射器整合在一起,可即时调节燃油输送,从而在更严格的排放法规下提高引擎效率。半主动悬吊模组中的压电感测器支援磁流变减震器,可提高电动平台的乘坐舒适性和稳定性。框架式致动器传递的力道是惯性模型的 300 倍,可为高级驾驶辅助系统 (ADAS) 提供快速的机械响应。使用 PowerHap 堆迭的触觉回馈模组现在可以透过精确的触觉提示移动 2 公斤的车载显示屏,增强人机互动。

欧盟无铅指令推高PZT替代品成本

《限制有害物质指令》正在推动从PZT(压电陶瓷)到无铅陶瓷的转变,但这也导致製造成本增加了15%至20%,并使全球供应策略复杂化。基于KNN的织构陶瓷的压电係数最近已达到550 pC/N,在25°C至150°C之间的变化小于1.2%,使其在性能关键型应用中具有竞争力。透过逆向复合製程再生氧化物的回收方法可将能源需求降低至原始生产的1%,同时维持感测品质。製造商必须维持两条供应链来供应依赖PZT的地区,同时为欧盟买家扩展原始生产线,这增加了间接成本。儘管监管截止日期已在不到两年内临近,但成本差异已推迟了价格敏感型消费性电子应用中的替代。

細項分析

到2024年,感测器将占据压电器件市场份额的32.1%,这反映了其在智慧型手机、汽车和工业监控等领域的跨产业普及。能量收集器是成长最快的细分市场,复合年增长率为9.1%,这与青睐免维护节点的自供电物联网设备的部署趋势一致。致动器和马达将占据第二大收入份额,受益于电动车的普及和精密製造。随着5G部署对网路同步要求的提高,共振器正获得新的发展动力。此细分市场的加速发展反映了压电奈米发电机与硅橡胶复合材料结合的突破,其在常规弯曲下的功率密度可达1.56 pW/cm²。如今,混合设备将感测、驱动和能量收集功能整合在一个堆迭中,为自主机器人提供了紧凑的解决方案。嵌入地砖中的发电机在人流作用下可产生 249.6 mW 的电力,每块地砖的成本约为 10.2 美元,展示了智慧建筑的低入口能量收集。

日益增长的需求给高温无铅材料和低成本聚合物共混物带来了上行压力。压电变压器在50 kHz时拥有88%的转换效率,能够为远端感测器节点实现射频能源采集。随着製造商整合边缘AI,杂讯滤波测量和双向回馈迴路变得至关重要,从而保持了感测设备在压电市场中的中心地位。

得益于PZT成熟的供应链和高度的电子机械耦合,陶瓷材料将在2024年占据67.4%的收益。由于采用柔性穿戴装置和生物医学植入的兴起,聚合物(尤其是PVDF)正以8.7%的复合年增长率快速成长。单晶材料为航太和国防领域提供了卓越的性能,而复合材料结构则融合了不同的优势。湿纺PVDF纤维目前在50N压缩下输出电压为0.88V,线性度为R²=0.996,使其在软性机器人领域的效用前景广阔。

带隙为 5.9 eV 的 MgSiN2 薄膜表现出 2.3 pC/V 的逆係数,拓展了压电材料在纳机电系统中的整合度。无铅 Ba0.85Ca0.15Ti0.9Zr0.1O3 陶瓷的逆係数超过 650 pC/N,同时维持 96.5°C 的居里温度,在不产生重大影响的情况下符合欧盟标准。 Y 掺杂的 ZnO 透过控制载流子浓度实现了 8.5 倍的输出跃迁,推动氧化物半导体应用于滤波器和感测器领域。这些并行的进展表明,压电市场将继续以陶瓷为中心,但市场将日益多元化。

区域分析

受行动电话组装、汽车电气化和高速5G部署的规模经济推动,亚太地区将在2024年占据全球销售额的38.8%。中国和韩国正在推动智慧超音波仪表和微型射频滤波器的发展,而日本的村田製作所、TDK和京瓷则将其深厚的陶瓷专业知识应用于高利润的多层元件。印度和东南亚吸引了对成本敏感的大宗商品的感测器组装,澳洲的矿业公司则部署了能源采集用于资产监控。人事费用的上升刺激了自动化投资,从而增强了对高端压电元件的需求。

北美在价值方面排名第二,这得益于国防和航太专案对高超音速陶瓷的需求。美国国防部将SBIR 24.1计画拨款用于积层製造纹理压电元件,刺激了国内研发。加拿大资源矿场指定使用重型采集器用于偏远油井,美国晶片工厂也扩大了精密平台的采用。 Physik Instrumente在麻萨诸塞州开设了一家占地12万平方英尺的工厂,以满足美国每年30%至50%的需求成长。由于供应链距离较近,墨西哥汽车厂将压电喷油嘴与ADAS触觉模组整合在一起。

在欧洲,严格的环保法规和豪华汽车的生产正在推动无铅陶瓷和下一代致动器的采用。德国原始设备製造商正在采用压电悬吊和喷射器,北欧电力公司正在采用电网感测器,法国航太业则对高温单晶的需求日益增长。随着海湾地区的管道、智慧城市和太阳能园区部署管道振动收集器和基础设施流量计,中东和非洲地区的复合年增长率将在2030年达到最高水平,达到8.5%。非洲的供应多元化措施可能导致上游材料在预测期内占据主导地位。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 5G智慧型手机压电MEMS射频滤波器的小型化(亚洲)

- 欧洲高阶汽车 ADAS 的燃油喷射和压电致致动器电气化

- 美国离散製造业对压电感测器的工业4.0改装需求

- 韩国和中国公共部署智慧超音波水錶

- 远程石油和天然气管道的微振动能源采集(中东)

- 美国国防部高超音速压电陶瓷获得联邦政府资助

- 市场限制

- 欧盟无铅指令增加PZT替代品的成本

- 铌和锂供应单一导致价格波动

- 资本密集型多阶段生产限制中小企业进入(日本/德国)

- 航空引擎压电压电薄膜的温度极限

- 产业供应链分析

- 监管和技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 依产品类型

- 致动器和电机

- 感应器

- 感应器

- 发电机

- 能量收集器

- 共振器

- 按材质

- 陶瓷製品

- 单晶

- 聚合物(PVDF等)

- 复合材料/其他

- 按运转方式

- 纵向位移/d33模式

- 并行/d15模式

- 横向位移/d31模式

- 厚度模式超音波

- 按最终用户产业

- 资讯科技/通讯

- 家电

- 製造和工业自动化

- 汽车和运输设备

- 医疗保健和医疗设备

- 航太/国防

- 能源与公共产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 北欧的

- 其他欧洲国家

- 南美洲

- 巴西

- 其他南美

- 亚太地区

- 中国

- 日本

- 印度

- 东南亚

- 其他亚太地区

- 中东和非洲

- 中东

- 波湾合作理事会成员国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略性倡议(併购、合资、资金筹措、许可)

- 市占率分析

- 公司简介

- APC International, Ltd.

- Physik Instrumente(PI)GmbH and Co. KG

- Morgan Advanced Materials plc

- CTS Corporation(incl. Noliac)

- CeramTec GmbH

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Kyocera Corporation

- Piezotech SAS(Arkema Group)

- Piezomechanik Dr. Lutz Pickelmann GmbH

- Piezosystem Jena GmbH

- Mad City Labs, Inc.

- Aerotech, Inc.

- Johnson Matthey Piezo Products GmbH

- Kistler Group

- Piezo.com(Meggitt PLC)

- Parker Hannifin-Meggitt Sensing

- Mide Technology(QinetiQ North America)

- TRS Technologies, Inc.

- Triumph Group-Transducer Systems

第七章 市场机会与未来展望

The piezoelectric devices market size reached USD 32.9 billion in 2025 and is forecast to climb to USD 45.24 billion by 2030, reflecting a 6.58% CAGR.

Expansion stems from the miniaturization of 5G RF filters, rising automotive electrification, and Industry 4.0 retrofits that rely on robust, energy-efficient piezo components. The adoption of aluminum scandium nitride for bulk acoustic wave filters enables smartphone frequencies above 6 GHz, while the European Union's lead-free agenda accelerates the shift to potassium sodium niobate and bismuth sodium titanate despite their higher manufacturing costs. Asia-Pacific leads demand through large-scale consumer electronics output, and Middle East and Africa shows the fastest growth on oil-and-gas energy harvesting projects. Competitive intensity is moderate because vertically integrated suppliers such as TDK, Murata, and Kyocera secure upstream materials and downstream capacity, yet supply risks around niobium and lithium introduce volatility for defense and aerospace users.

Global Piezoelectric Devices Market Trends and Insights

Miniaturization of Piezo-MEMS RF Filters for 5G Smartphones (Asia)

Bulk acoustic wave filters built on aluminum scandium nitride now achieve frequencies above 6 GHz with coupling coefficients 40% higher than standard aluminum nitride, while maintaining thermal stability to 400 °C. These advances shrink die footprints to 0.83 X 0.75 mm2 and keep insertion losses below 1.5 dB, preserving smartphone battery life. Three-dimensional nanomechanical resonators further consolidate multiband functions onto single chips, creating scalable solutions for ultrawide-band connectivity. Asian wafer-level sealed silicon cavity platforms have achieved quality factors above 439, reducing production steps and cost. As 6G and millimeter-wave initiatives gather pace, demand rises for lithium niobate-based ultra-small filter chips, reinforcing Asia-Pacific's technology leadership.

Electrified Fuel-Injection and ADAS Piezo Actuators in European Premium Cars

Copper-electroded EPCOS multilayer actuators withstand more than 1 billion cycles at 170 °C, offering 20% performance gains over silver-palladium units while trimming material expenses. DENSO's i-ART system integrates microprocessors with piezo injectors to tailor fuel delivery in real time, enhancing engine efficiency under stricter emission norms.] Piezo sensors in semi-active suspension modules support magnetorheological dampers that raise ride comfort and stability for electrified platforms. Frame-type actuators transmit forces over 300 times higher than inertial models, giving advanced driver-assistance systems quicker mechanical response. Haptic feedback modules using PowerHap stacks now move 2 kg automotive displays with precise tactile cues that bolster human-machine interaction.

EU Lead-Free Directive Increasing Cost of PZT Substitutes

The Restriction of Hazardous Substances mandate propels the migration from PZT to lead-free ceramics that carry 15-20% higher production costs and complicate global supply strategies. KNN-based textured ceramics recently reached 550 pC/N piezo coefficients with less than 1.2% variability between 25 °C and 150 °C, making them competitive for performance-critical uses. Recycling methods that reclaim oxides via upside-down composite processing slash energy demand to 1% of virgin production and keep sensing quality intact. Manufacturers must maintain twin supply chains to serve PZT-dependent regions while scaling pristine lines for EU buyers, raising overheads. Cost differentials slow substitution in price-sensitive consumer electronics even as regulatory deadlines loom within two years.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Retrofit Demand for Piezo Sensors in United States Discrete Manufacturing

- Smart Ultrasonic Meter Roll-outs in South-Korea and China Utilities

- Price Volatility from Single-Source Niobium and Lithium Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sensors captured 32.1% of piezoelectric devices market share in 2024, reflecting their cross-industry ubiquity in smartphones, vehicles, and industrial monitoring. Energy harvesters form the fastest-growing cohort at a 9.1% CAGR, aligned with self-powered IoT rollouts that favor maintenance-free nodes. Actuators and motors hold the second-largest slice by revenue, benefiting from EV adoption and precision manufacturing. Resonators see renewed traction as 5G deployment raises network synchronization requirements. The segment's acceleration mirrors break-throughs in piezoelectric nanogenerators that pair silicone rubber composites with power densities of 1.56 pW/cm2 under daily flexing. Hybrid devices now combine sensing, actuation, and harvesting within a single stack, offering compact solutions for autonomous robots. Generators embedded in floor tiles yield 249.6 mW under foot traffic at roughly USD 10.2 per tile, illustrating low-entry energy harvesting for smart buildings.

Demand convergence places upward pressure on high-temperature lead-free materials and low-cost polymer blends. Piezoelectric transformers boasting 88% conversion efficiency at 50 kHz enable RF-energy harvesting for distant sensor nodes As manufacturers integrate edge AI, noise-filtered measurements and two-way feedback loops become essential, preserving the centrality of sensing devices within the piezoelectric devices market.

Ceramics accounted for 67.4% of 2024 revenue, maintained by PZT's mature supply chain and high electromechanical coupling. Polymers, especially PVDF, are growing fastest at an 8.7% CAGR thanks to flexible wearables and biomedical implants. Single-crystal options deliver premium performance for aerospace and defense, while composite architectures merge disparate advantages. Wet-spun PVDF fibers now register 0.88 V outputs under 50 N compression with R2 = 0.996 linearity, extending utility into soft robotics.

MgSiN2 thin films with a 5.9 eV bandgap show converse coefficients of 2.3 pm/V, broadening piezo integration in nanoelectromechanical systems. Lead-free Ba0.85Ca0.15Ti0.9Zr0.1O3 ceramics top 650 pC/N while keeping Curie temperatures of 96.5 °C, addressing EU compliance without severe trade-offs. Y-doped ZnO exhibits an 8.5-fold output jump through carrier-concentration control, pushing oxide semiconductors toward filter and sensor roles. These parallel advances suggest the piezoelectric devices market will remain ceramic-centric yet increasingly diversified.

The Piezoelectric Devices Market Report is Segmented by Product Type (Actuators and Motors, Sensors, Transducers, and More), Material (Ceramics, Single-Crystal, Polymers, and More), Operating Mode (Compression/D33 Mode, Shear/D15 Mode, and More), End-User Industry (IT and Telecommunication, Consumer Electronics, Healthcare and Medical Devices, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.8% of global revenue in 2024, driven by scale advantages in handset assembly, automotive electrification, and fast 5G rollouts. China and South Korea advance smart ultrasonic meters and miniaturized RF filters, while Japan's Murata, TDK, and Kyocera channel deep ceramics expertise into higher-margin multilayer components. India and Southeast Asia attract sensor assembly for cost-sensitive goods, whereas Australia's mining firms deploy energy harvesting for asset monitoring. Rising labor costs spur automation investments, reinforcing premium piezo demand.

North America ranks second in value, underpinned by defense and aerospace programs that require hypersonic-grade ceramics. The Department of Defense earmarked SBIR 24.1 funds for additively manufactured textured piezo components, sparking domestic R&D. Canadian resource sites specify rugged harvesters for remote wells, and US chip fabs expand precision-stage adoption. Physik Instrumente opened a 120,000 sq ft Massachusetts plant to meet 30-50% annual US demand growth. Mexico's vehicle plants integrate piezo injectors and ADAS haptic modules, given supply chain proximity.

Europe leverages stringent environmental rules and luxury-car production to drive lead-free ceramics and next-gen actuators. German OEMs embed piezo suspensions and injectors; Nordic utilities incorporate grid sensors; France's aerospace sector demands high-temperature single crystals. The Middle East and Africa region posts the highest CAGR at 8.5% to 2030 as Gulf pipelines, smart cities, and solar parks deploy pipeline vibration harvesters and infrastructure flow meters. Supply diversification efforts in Africa could evolve into upstream material advantages over the forecast horizon.

- APC International, Ltd.

- Physik Instrumente (PI) GmbH and Co. KG

- Morgan Advanced Materials plc

- CTS Corporation (incl. Noliac)

- CeramTec GmbH

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Kyocera Corporation

- Piezotech S.A.S. (Arkema Group)

- Piezomechanik Dr. Lutz Pickelmann GmbH

- Piezosystem Jena GmbH

- Mad City Labs, Inc.

- Aerotech, Inc.

- Johnson Matthey Piezo Products GmbH

- Kistler Group

- Piezo.com (Meggitt PLC)

- Parker Hannifin - Meggitt Sensing

- Mide Technology (QinetiQ North America)

- TRS Technologies, Inc.

- Triumph Group - Transducer Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Miniaturization of Piezo-MEMS RF Filters for 5G Smartphones (Asia)

- 4.2.2 Electrified Fuel-Injection and ADAS Piezo Actuators in European Premium Cars

- 4.2.3 Industry 4.0 Retrofit Demand for Piezo Sensors in United States Discrete Manufacturing

- 4.2.4 Smart Ultrasonic Meter Roll-outs in South-Korea and China Utilities

- 4.2.5 Micro-Vibration Energy Harvesting for Remote Oil and Gas Pipelines (Middle East)

- 4.2.6 Federal Funding for Hypersonic-Grade Piezo Ceramics in United States Defense

- 4.3 Market Restraints

- 4.3.1 EU Lead-Free Directive Increasing Cost of PZT Substitutes

- 4.3.2 Price Volatility from Single-Source Niobium and Lithium Supply

- 4.3.3 Capital-Intensive Multi-Axis Stage Production Limiting SME Entry (JP/DE)

- 4.3.4 Temperature Limits of Polymer Piezo Films in Aero-engines

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Actuators and Motors

- 5.1.2 Sensors

- 5.1.3 Transducers

- 5.1.4 Generators

- 5.1.5 Energy Harvesters

- 5.1.6 Resonators

- 5.2 By Material

- 5.2.1 Ceramics

- 5.2.2 Single-Crystal

- 5.2.3 Polymers (e.g., PVDF)

- 5.2.4 Composites/Others

- 5.3 By Operating Mode

- 5.3.1 Compression/d33 Mode

- 5.3.2 Shear/d15 Mode

- 5.3.3 Bending/d31 Mode

- 5.3.4 Thickness-Mode Ultrasonic

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunication

- 5.4.2 Consumer Electronics

- 5.4.3 Manufacturing and Industrial Automation

- 5.4.4 Automotive and Transportation

- 5.4.5 Healthcare and Medical Devices

- 5.4.6 Aerospace and Defense

- 5.4.7 Energy and Utilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, Tech-Licensing)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 APC International, Ltd.

- 6.4.2 Physik Instrumente (PI) GmbH and Co. KG

- 6.4.3 Morgan Advanced Materials plc

- 6.4.4 CTS Corporation (incl. Noliac)

- 6.4.5 CeramTec GmbH

- 6.4.6 TDK Corporation

- 6.4.7 Murata Manufacturing Co., Ltd.

- 6.4.8 Kyocera Corporation

- 6.4.9 Piezotech S.A.S. (Arkema Group)

- 6.4.10 Piezomechanik Dr. Lutz Pickelmann GmbH

- 6.4.11 Piezosystem Jena GmbH

- 6.4.12 Mad City Labs, Inc.

- 6.4.13 Aerotech, Inc.

- 6.4.14 Johnson Matthey Piezo Products GmbH

- 6.4.15 Kistler Group

- 6.4.16 Piezo.com (Meggitt PLC)

- 6.4.17 Parker Hannifin - Meggitt Sensing

- 6.4.18 Mide Technology (QinetiQ North America)

- 6.4.19 TRS Technologies, Inc.

- 6.4.20 Triumph Group - Transducer Systems

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

IC拾放处理设备市场按产品类型、元件类型、应用和最终用户划分,全球预测(2026-2032年)

IC拾放处理设备市场按产品类型、元件类型、应用和最终用户划分,全球预测(2026-2032年) 压电器件市场分析及预测(至2035年):依类型、产品类型、技术、材料类型、应用、组件、最终用户、功能及安装类型划分

压电器件市场分析及预测(至2035年):依类型、产品类型、技术、材料类型、应用、组件、最终用户、功能及安装类型划分 2026年全球压电器件市场报告

2026年全球压电器件市场报告 全球压电装置市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球压电装置市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 压电器件市场-全球产业规模、份额、趋势、机会及预测(依产品、材料、组件、最终用户、地区及竞争格局划分),2021-2031年压电被动式蜂鸣器市场按端子类型、音调类型、工作电压、应用和最终用户产业划分,全球预测(2026-2032年)汽车压电致动器市场:按致动器类型、安装类型、应用、车辆类型和最终用户划分 - 全球预测 2026-2032线性压电位移平台市场:按致动器类型、驱动类型、应用、最终用户和分销管道划分,全球预测,2026-2032年

压电器件市场-全球产业规模、份额、趋势、机会及预测(依产品、材料、组件、最终用户、地区及竞争格局划分),2021-2031年压电被动式蜂鸣器市场按端子类型、音调类型、工作电压、应用和最终用户产业划分,全球预测(2026-2032年)汽车压电致动器市场:按致动器类型、安装类型、应用、车辆类型和最终用户划分 - 全球预测 2026-2032线性压电位移平台市场:按致动器类型、驱动类型、应用、最终用户和分销管道划分,全球预测,2026-2032年 压电智慧材料市场,全球市场,2025-2029

压电智慧材料市场,全球市场,2025-2029 全球压电半球市场

全球压电半球市场