|

市场调查报告书

商品编码

1844451

过氧化钙:市场占有率分析、产业趋势、统计、成长预测(2025-2030)Calcium Peroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

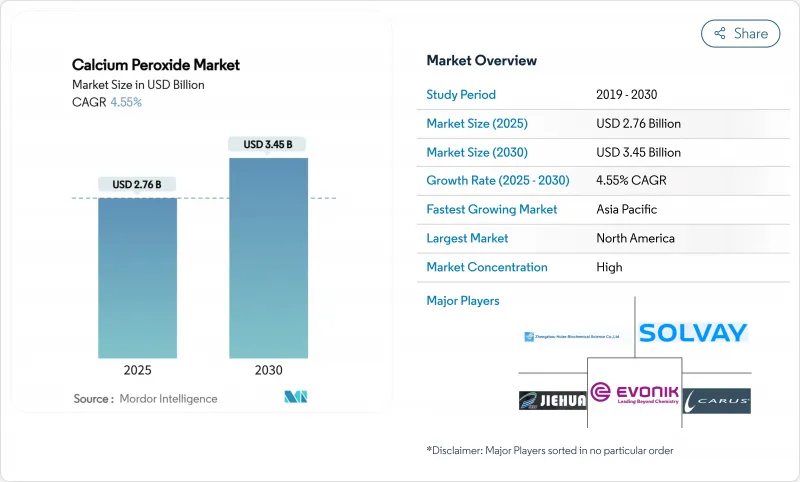

过氧化钙市场规模预计在 2025 年为 27.6 亿美元,预计到 2030 年将达到 34.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.55%。

目前发展动能的驱动力来自于对氧化剂的持续需求,这类氧化剂能够分解成氢氧化钙和氧气,且不会留下有害的产品残留物。成长要素包括织物调理领域的大规模应用、不断扩大的环境修復计划,以及精密农业中种子丸粒化的广泛应用。竞争的焦点在于能够缩短加工週期、改善水质、提高发芽率并同时满足严格监管标准的专用配方。生产商也透过垂直整合和区域产能扩张来规避原材料价格波动的影响。风险涉及操作风险、挥发性石灰和碳酸钙的成本,以及低价过氧化物替代的压力。

全球过氧化钙市场趋势与见解

在烘焙业中越来越多地用作麵团改良剂

随着传统醒发製程逐渐被快速麵团製程所取代,工业烘焙企业对过氧化钙的需求日益增长。 20-35 ppm 的最佳添加量可提高麵筋强度、保湿性和冷冻麵团稳定性,帮助大型烘焙企业实现全厂品质标准化。虽然偶氮二甲酰胺在欧洲被禁用,但这种化合物因其降解产物可最大程度降低健康风险而日益受到欢迎。在北美和欧洲扩大生产规模可确保为跨国食品集团提供稳定的供应。零售通路冷冻和预烘焙食品消费量的不断增长,支撑了过氧化钙市场的长期成长。整合线上氧化剂注入功能的设备升级也简化了过氧化钙的采用。

口腔护理和牙齿美白产品的采用率不断提高

奈米颗粒在牙齿美白凝胶和漱口水中越来越受欢迎,因为它们能够持续释放氧气,抑制生物膜形成,同时亮白珐琅质。临床研究表明,过氧化钙比过氧化氢更能渗透牙本质小管,从而降低牙龈敏感度。领先的口腔清洁用品品牌将过氧化钙定位为「温和氧气」成分,顺应清洁标籤的趋势。亚太地区的快速都市化正在扩大高端美白产品的消费群体,从而增加短期需求。美国、欧盟和日本的监管核准将促进非处方药和专业美白产品的商业化。

储存和处理过程中的健康和安全危害

过氧化钙被归类为强氧化剂;与有机物接触会加剧火灾,其粉尘会刺激眼睛、皮肤和呼吸道。仓库需要与可燃物隔离,并进行温度控制和局部排气通风。这些措施会增加合规成本,尤其对于新兴市场的小型加工企业而言。缺乏既定的职业接触限值会增加监管的不确定性,并可能延迟工厂核准。培训和个人防护设备的要求也会增加整体拥有成本,从而阻碍过氧化钙市场中对成本敏感的细分市场的快速普及。

細項分析

2024年,食品级过氧化钙将占据56.66%的市场份额,这反映了全球烘焙企业在严格的食品安全规范下对氧化剂性能的持续需求。优质供应商提供的产品符合FCC和ASTM基准,并保持较窄的粒径范围,使其能够在高速搅拌机中均匀分散。受土壤修復、水产养殖和精密农业扩张的推动,预计到2030年,工业级过氧化钙的复合年增长率将达到5.12%。用于口腔护理和製药应用的特殊奈米颗粒净利率高,吸引了化学巨头的研发投资。

北美和欧洲的监管审核正在加强供应商选择标准,青睐那些拥有有效危害分析计画的长期生产商。同时,工业级配方师优先考虑产量氧量、水不溶性和流动性,以满足修復承包商对加药设备的要求。亚太地区直播水稻和池塘水处理的应用,支持了工业级过氧化钙产量的持续成长。严格的认证与性能定制之间的相互作用,维持了整体平衡,从而支撑了过氧化钙市场的长期韧性。

区域分析

2024年,美国以38.34%的收入份额领先市场,这得益于严格的修復方法、技术先进的烘焙行业以及早期部署的精准播种工具,这些工具尤其青睐基于过氧化钙的供氧剂。美国环保署的棕地津贴持续刺激对固态氧化剂的需求,以降低场地运作的风险。加拿大紧随其后,在不列颠哥伦比亚省开展资源行业的土壤修復和水产养殖试验,而墨西哥则受益于依赖美国供应链的食品加工出口。过氧化氢工厂的产能扩张,例如Engro为供应下游过氧化钙生产的投资,增强了原料的安全性。

受大规模水产养殖和直播水稻推广的推动,到2030年,亚太地区的复合年增长率将达到6.33%,位居榜首。日本的鳗鱼养殖场和越南的虾池展示了池塘增氧应用的广泛性,推动了每月持续性需求。中国的污染土地修復法规、印度的机械化水稻插秧机以及韩国的口腔清洁用品创新生态系统都在拓展应用的多样性。中国和马来西亚的地区製造商正在石灰岩矿床附近建造新工厂,以降低物流成本并缩短交货週期,从而增强该地区过氧化钙市场的竞争力。

在欧洲,偶氮二甲酰胺正在逐步退出烘焙生产线,德国、法国和英国的烘焙厂正在转向使用过氧化钙替代品。波兰和义大利的旧工业区正在进行进一步的土壤修復。北欧的高价值水产养殖业正在试行沉积物氧化制度,并持续增加其应用案例。在南美洲、中东和非洲,巴西塞拉多的开垦和埃及的吴郭鱼池塘正在利用来自亚太地区的技术转让,提供新的可能性。基础设施缺口和监管变化正在减缓成长,但仍为全球过氧化钙市场提供越来越多的供应。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 在烘焙业中越来越多地用作麵团改良剂

- 扩大在口腔护理和牙齿美白产品的应用

- 对原位土壤和地下水修復的需求不断增加

- 扩大种子丸粒化技术在精密农业的应用

- 推广水产养殖池增氧技术

- 欧洲逐步淘汰偶氮二甲酰胺,促进过氧化物替代

- 市场限制

- 储存和处理过程中的健康和安全危害

- 更廉价的过氧化氢/苯甲酰替代品的威胁

- 挥发性石灰和碳酸钙原料定价

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按年级

- 食品级

- 工业级

- 按用途

- 麵团调理剂

- 种子消毒剂

- 漂白

- 氧化剂

- 中间化学品

- 其他用途

- 按最终用户产业

- 饮食

- 农业

- 矿业

- 纸浆和造纸

- 製药

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太地区其他国家

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- AkzoNobel NV

- American Elements

- BASF SE

- Carus Group Inc.

- Evonik Industries AG

- Mahalaxmi Enterprise

- Nikunj Chemicals

- Noshly Pty Ltd

- Pioneer Enterprise

- Shangyu Jie Hua Chemical

- Solvay SA

- STP Chem Solutions

- Sunway Lab

- Zhengzhou Huize Biochemical Technology Co. Ltd

第七章 市场机会与未来展望

The Calcium Peroxide Market size is estimated at USD 2.76 billion in 2025, and is expected to reach USD 3.45 billion by 2030, at a CAGR of 4.55% during the forecast period (2025-2030).

Current momentum comes from sustained demand for an oxidizing agent that decomposes into calcium hydroxide and oxygen, leaving no hazardous by-products. Growth levers include large-scale adoption in dough conditioning, expanding environmental remediation projects, and wider use in seed pelleting for precision agriculture. Competitive activity centers on application-specific formulations that shorten processing cycles, improve water quality, or raise germination rates while meeting strict regulatory standards. Producers also hedge against feedstock price swings by vertical integration and regional capacity additions. Risks relate to handling hazards, volatile lime and calcium carbonate costs, and substitution pressure from lower-priced peroxides.

Global Calcium Peroxide Market Trends and Insights

Increased Use as Dough-Conditioner in Bakery Industry

Demand for calcium peroxide in industrial bakeries rises as no-time dough processes replace traditional proofing. Optimum addition rates of 20-35 ppm improve gluten strength, moisture retention, and frozen dough stability, helping large bakers standardize quality across plants. Regulatory bans on azodicarbonamide in Europe further favour the compound because its breakdown products pose minimal health risks. Production scale-up in North America and Europe secures a consistent supply for multinational food groups. Greater consumption of frozen and par-baked items in retail channels sustains long-term volume growth for the calcium peroxide market. Equipment upgrades that integrate inline oxidant dosing also streamline adoption.

Growing Adoption in Oral-Care & Dental Whitening Products

Nanoparticle grades are gaining traction in tooth whitening gels and mouthwashes because slow oxygen release inhibits biofilms while brightening enamel. Clinical studies show better penetration into dentinal tubules than hydrogen peroxide, reducing sensitivity. Major oral-care brands position calcium peroxide as a "gentle oxygen" ingredient, aligning with clean-label trends. Rapid urbanisation in the Asia Pacific widens the consumer base for premium whitening products, adding near-term demand. Regulatory approvals across the United States, European Union, and Japan smooth commercialisation for both OTC and professional lines.

Health & Safety Hazards During Storage/Handling

Calcium peroxide is classified as a strong oxidizer; contact with organics can intensify fires, and the dust irritates eyes, skin, and respiratory tracts. Warehouses require isolation from combustible materials, temperature control, and local exhaust ventilation systems. These measures raise compliance costs, especially for small processors in emerging markets. Absence of an established occupational exposure limit adds regulatory uncertainty and may delay plant approvals. Training and personal protective equipment requirements also elevate the total cost of ownership, restraining rapid diffusion in cost-conscious segments of the calcium peroxide market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for In-Situ Soil & Groundwater Remediation

- Expansion of Seed Pelleting for Precision Agriculture

- Volatile Lime & Calcium Carbonate Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food Grade accounted for 56.66% of the calcium peroxide market share in 2024, reflecting entrenched demand from global bakery groups that require consistent oxidant performance under strict food safety codes. Premium suppliers deliver products that conform to FCC and ASTM benchmarks and maintain a narrow particle-size span, enabling homogeneous dispersion in high-speed mixers. Industrial Grade is forecast to post a 5.12% CAGR to 2030 as soil remediation, aquaculture, and precision agriculture gain scale. Specialty nanoparticle variants aimed at oral-care and pharmaceutical uses command higher margins, attracting R&D investments from chemical majors.

Regulatory audits in North America and Europe reinforce supplier selection criteria, favouring long-standing producers with validated hazard-analysis plans. Meanwhile, Industrial Grade formulators emphasise oxygen yield, water insolubles, and flowability to meet remediation contractors' dosing equipment requirements. Adoption of direct-seeded rice and pond treatment in Asia Pacific underpins sustained tonnage growth for Industrial Grade. The interplay of stringent certification on one side and performance customisation on the other maintains overall balance and undergirds long-term resilience of the calcium peroxide market.

The Calcium Peroxide Market Report is Segmented by Grade (Food Grade, Industrial Grade), Application (Dough Conditioner, Seed Disinfectant, Bleaching Agent, Oxidizing Agent, and More), End-User Industry (Food and Beverage, Agriculture, Mining, Pulp and Paper, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with a 38.34% revenue share in 2024 thanks to stringent remediation legislation, a technologically advanced bakery sector, and early deployment of precision seeding tools that favour calcium peroxide-based oxygen donors. The United States Environmental Protection Agency's brownfield grants continue to stimulate demand for solid-form oxidants that lower site operation hazards. Canada follows with resource-sector soil clean-up and aquaculture trials in British Columbia, while Mexico benefits from food-processing exports that hinge on US supply chains. Capacity additions in hydrogen peroxide plants, such as Engro's investment that feeds downstream calcium peroxide production, enhance raw material security.

Asia Pacific posts the fastest regional CAGR at 6.33% to 2030, propelled by large-scale aquaculture operations and direct-seeded rice adoption. Japanese eel farms and Vietnamese shrimp ponds illustrate the breadth of pond-oxygenation uses, driving recurring monthly demand. China's contaminated-land restoration mandates, India's mechanised rice planters, and South Korea's oral-care innovation ecosystem all expand application diversity. Regional manufacturers in China and Malaysia commission new plants close to limestone deposits to trim logistics costs and shorten delivery cycles, reinforcing competitiveness of the calcium peroxide market in the region.

Europe's trajectory is shaped by the phased withdrawal of azodicarbonamide from bakery lines, pushing bakeries in Germany, France, and the United Kingdom toward calcium peroxide alternatives. Soil remediation in old industrial belts of Poland and Italy presents additional volume. Northern Europe's high-value aquaculture sector pilots sediment oxidation regimes, adding another use case. South America and the Middle East & Africa provide emerging potential, with Brazil's Cerrado reclamation and Egypt's tilapia ponds drawing on technology transfer from Asia Pacific. Infrastructure gaps and regulatory variability temper the growth slope yet still feed incremental tonnage into the global calcium peroxide market.

- AkzoNobel N.V.

- American Elements

- BASF SE

- Carus Group Inc.

- Evonik Industries AG

- Mahalaxmi Enterprise

- Nikunj Chemicals

- Noshly Pty Ltd

- Pioneer Enterprise

- Shangyu Jie Hua Chemical

- Solvay SA

- STP Chem Solutions

- Sunway Lab

- Zhengzhou Huize Biochemical Technology Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased use as dough-conditioner in bakery industry

- 4.2.2 Growing adoption in oral-care and dental whitening products

- 4.2.3 Rising demand for in-situ soil and groundwater remediation

- 4.2.4 Expansion of seed-pelleting for precision agriculture

- 4.2.5 Aquaculture pond-oxygenation technologies gaining traction

- 4.2.6 Europe phase-down of azodicarbonamide drives peroxide alternatives

- 4.3 Market Restraints

- 4.3.1 Health and safety hazards during storage/handling

- 4.3.2 Substitution threat from cheaper hydrogen/benzoyl peroxides

- 4.3.3 Volatile lime and calcium carbonate feedstock pricing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Food Grade

- 5.1.2 Industrial Grade

- 5.2 By Application

- 5.2.1 Dough Conditioner

- 5.2.2 Seed Disinfectant

- 5.2.3 Bleaching Agent

- 5.2.4 Oxidizing Agent

- 5.2.5 Intermediary Chemicals

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage

- 5.3.2 Agriculture

- 5.3.3 Mining

- 5.3.4 Pulp and Paper

- 5.3.5 Pharmaceutical

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of APAC

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 American Elements

- 6.4.3 BASF SE

- 6.4.4 Carus Group Inc.

- 6.4.5 Evonik Industries AG

- 6.4.6 Mahalaxmi Enterprise

- 6.4.7 Nikunj Chemicals

- 6.4.8 Noshly Pty Ltd

- 6.4.9 Pioneer Enterprise

- 6.4.10 Shangyu Jie Hua Chemical

- 6.4.11 Solvay SA

- 6.4.12 STP Chem Solutions

- 6.4.13 Sunway Lab

- 6.4.14 Zhengzhou Huize Biochemical Technology Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increasing Environmental Concern Regarding Soil Remediation and Oil-spill Recovery

2026年全球过氧化钙市场报告

2026年全球过氧化钙市场报告 过氧化钙市场规模、份额及成长分析(按等级、应用、最终用途及地区划分)-2026-2033年产业预测

过氧化钙市场规模、份额及成长分析(按等级、应用、最终用途及地区划分)-2026-2033年产业预测 全球过氧化钙市场

全球过氧化钙市场 全球过氧化钙市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球过氧化钙市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测