|

市场调查报告书

商品编码

1844599

接触胶黏剂:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Contact Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

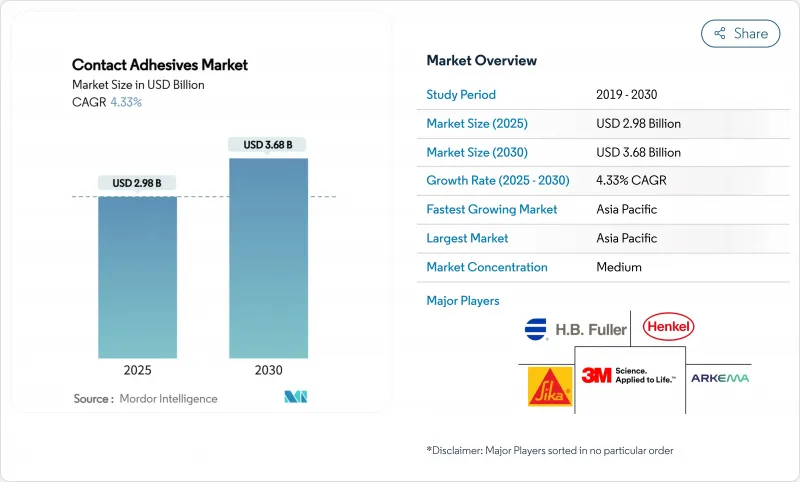

预计 2025 年接触胶市场规模为 29.8 亿美元,到 2030 年将达到 36.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.33%。

这一成长路径标誌着核心业务的成熟,这得益于对电动车电池组和可再生能源维护的新兴需求。即时黏合应用,例如鞋类组装、模组化家具和现场施工,牢牢地扎根于接触胶合剂市场的传统领域,在这些领域,瞬间黏合和抗重新定位仍然至关重要。同时,减少挥发性有机化合物 (VOC)排放的监管压力正在加速向水性配方的转变,从而在不影响胶合剂性能的前提下开闢了更大的创新空间。供应链的弹性,尤其是在亚太地区,在氯丁二烯单体短缺和原材料波动定期影响製造商的情况下,支撑了价格稳定。最后,亚洲鞋厂自动化程度的提高和风力发电机叶片的维修活动正在创造閒置频段机会,使特种等级的产品能够获得溢价。

全球接触胶合剂市场趋势与洞察

转向低VOC水性体系

包括加州日益严格的挥发性有机化合物 (VOC) 法规和加拿大2024年全国性法规在内的监管趋势正在重塑配方策略。如今,大规模生产无溶剂等级的产品具有经济优势,只需单一配方即可服务多个司法管辖区。美国提案限制消费性胶黏剂中N-Methyl Pyrrolidone的浓度不得超过45%,这进一步缩小了溶剂选择范围,并推动了全水性胶合剂的研发。 3M Fastbond 1049等产品的推出表明,接触胶粘剂市场无需溶剂载体即可达到性能基准。因此,供应商预计,随着配方在开放时间和湿强度方面更具可比性,合规等级的价格溢价将会上升,从而在成本敏感的亚洲工厂中得到更广泛的采用。

模组化家具和室内装修正在蓬勃发展

城市密集化和混合办公空间正在推动模组化建筑技术的发展,这些技术更倾向于使用基于黏合剂的组装而不是机械紧固件。黏合剂解决方案可以减轻重量、提升美观度并加快安装速度,这与亚太地区快速的住宅和商业建筑週期相契合。使用预製面板和轻质复合复合材料的计划通常会指定使用具有高初黏性且无需夹具即可垂直安装的接触式黏合剂。模组化趋势也提高了可循环性,因为黏合的组件可以干净地拆卸以便重复使用或回收。这些因素的综合作用将使接触式黏合剂市场的需求在短期内成长约0.8个百分点。

原物料价格波动

由于供应减少、恶劣天气条件和物流瓶颈,聚合级丙烯、氯丁二烯和天然橡胶的价格波动剧烈。小型生产商受到的打击最为严重,因为它们缺乏长期供应协议的筹码。亚洲乙烯和丙烯的盈利仍然疲软,阻碍了再投资,并增加了成本进一步上涨的风险。库存缓衝和双重采购策略在一定程度上缓解了这一局面,但由于不确定性,接触胶合剂市场的新资本投资决策已被推迟。

細項分析

2024年,溶剂型接触胶合剂占了76.34%的市场份额,这得益于其无与伦比的开放时间弹性和高初黏性。例如,鞋类生产线依靠快速抓取来维持高组装产量。然而,受VOC法规和树脂乳化技术的进步推动,水性胶合剂的复合年增长率高达4.98%,从而缩小了性能差距。加州最新的消费品法规和加拿大2024年VOC限量法规正在加速全球标准化进程,推动无溶剂解决方案的发展。

热熔树脂和反应性树脂占据利基市场,在耐热性和即时固化性方面,成本因素更为重要。 3M 等供应商目前正在推广一种完全无溶剂的产品线,其剥离强度可与旧款氯丁二烯配方相媲美,证明了技术融合是可能的。预计在预测期内,水性接触胶合剂市场规模将达到 9.6 亿美元,反映出在受监管领域内,水性接触胶合剂的替代效应正在稳步推进。

本报告按技术(水性、溶剂型、其他)、聚合物(聚氯丁二烯、苯乙烯-丁二烯橡胶、丙烯酸共聚物、其他)、终端用户产业(耐用消费品及电子产品、包装、汽车及运输、家具及木工、其他)及地区(亚太地区、北美、欧洲、其他)进行细分。市场预测以美元计算。

区域分析

预计到2024年,亚太地区将占据全球接触胶合剂市场的59.55%,复合年增长率为5.05%,主导中国多元化的製造业基础和印度政府推动的进口替代政策。越南、泰国和印尼正在大力投资运动鞋智慧工厂,这将推动该地区对精密低VOC配方的需求。虽然原料价格会週期性波动,但由于靠近树脂生产国,其到岸成本与进口到欧洲和美国相比更具优势。

受电动车生产和严格环保标准的推动,北美市场需求持续强劲。汽车製造商越来越多地指定使用水性胶合剂,以获得美国先进清洁交通计划的积分,从而提升了合规等级在北美的渗透率。即使在销售量成长缓慢的情况下,区域供应商也正利用其强大的智慧财产权优势,争取溢价并提高净利率。

成熟的欧洲市场以其监管领导力而闻名。 REACH法规对PFAS和甲醛的广泛限制正在加速其配方改革週期。欧洲也拥有大量待修復的风力发电机叶片,这为特种接触胶合剂带来了稳定的需求。

南美洲、中东和非洲地区提供了与住宅建筑和轻工业製造相关的前沿商机。儘管外汇波动仍然是不利因素,但这些地区的政府正在开发工业园区,并提供税收优惠政策,以吸引黏合剂加工商。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 转向低VOC水性体系

- 模组化家具和室内装修正在蓬勃发展

- 在亚洲一家鞋厂整合机器人黏合剂应用生产线

- 风力发电机叶片修復需求

- 电动车电池组内的隔热黏合剂

- 市场限制

- 原物料价格波动

- 严格的VOC和可燃性法规

- 全球氯丁二烯单体供应中断

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 原料分析

第五章市场规模及成长预测

- 依技术

- 水性

- 溶剂型

- 其他的

- 按聚合物

- 聚氯丁二烯(氯丁橡胶)

- 苯乙烯-丁二烯橡胶(SBR)

- 丙烯酸共聚物

- 聚氨酯

- 腈类及其他

- 按最终用户产业

- 耐用消费品和电子产品

- 包装

- 汽车和运输

- 家具和木工

- 鞋类和皮革製品

- 建筑(地板、板材、屋顶)

- 其他终端用户产业(风力发电、DIY等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- 3M

- AdCo UK Limited

- Aica Kogyo Co..Ltd.

- Arkema(Bostik)

- Collano

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- HB Fuller Company

- Helmitin Adhesives

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.(ITW Performance Polymers)

- Intact Adhesives(KMS Adhesives Ltd)

- Jowat

- Mapei SpA

- Permabond

- Pidilite Industries Ltd

- Pyrotek

- Sika AG

第七章 市场机会与未来展望

The Contact Adhesives Market size is estimated at USD 2.98 billion in 2025, and is expected to reach USD 3.68 billion by 2030, at a CAGR of 4.33% during the forecast period (2025-2030).

This growth path shows a maturing core business now supported by new demand in electric-vehicle battery packs and renewable-energy maintenance. Immediate-bond applications such as footwear assembly, modular furniture, and on-site construction keep the contact adhesives market firmly rooted in traditional sectors where instant tack and repositioning resistance remain critical. Meanwhile, regulatory pressure to lower volatile-organic-compound (VOC) emissions is accelerating the shift toward waterborne formulations, opening room for innovation without compromising bonding performance. Supply-chain resilience, especially in Asia-Pacific, underpins price stability even as chloroprene monomer shortages and raw-material volatility periodically challenge manufacturers. Finally, automation in Asian footwear plants and rising repair work on wind-turbine blades are creating white-space opportunities that allow premium pricing for specialized grades.

Global Contact Adhesives Market Trends and Insights

Shift to Low-VOC Water-Borne Systems

Regulatory momentum is reshaping formulation strategies as tougher VOC caps in California and Canada's 2024 national limits push manufacturers toward waterborne products. The economics now favor the scale production of solvent-free grades that meet multiple jurisdictions with a single recipe. Proposed United States restrictions on N-Methylpyrrolidone at 45% concentration for consumer adhesives narrow the solvent palette further, driving research and development toward completely water-based chemistries. Product launches such as 3M Fastbond 1049 show that the contact adhesives market can meet performance benchmarks without solvent carriers. As a result, suppliers anticipate incremental price premiums for compliant grades and broader uptake in cost-sensitive Asian factories as formulations reach parity on open time and green strength.

Booming Modular Furniture and Interior Fitouts

Urban densification and hybrid workspaces are fueling modular construction techniques that favour adhesive-based assembly over mechanical fasteners. Adhesive solutions trim weight, enhance aesthetics, and cut installation time, aligning with Asia-Pacific's fast-track residential and commercial build cycles. Projects that rely on pre-finished panels and lightweight composites often specify contact adhesives for their high initial tack, enabling vertical mounting without clamping. The modular trend also improves circularity because glued components can be removed cleanly for reuse or recycling. Together, these factors lift short-term demand in the contact adhesives market by an estimated 0.8 percentage points.

Raw-Material Price Volatility

Polymer-grade propylene, chloroprene, and natural rubber prices have swung sharply on supply cuts, weather events, and logistics bottlenecks. Small producers are hit hardest because they lack leverage to secure long-term supply contracts. Ethylene and propylene profitability remains weak in Asia, discouraging reinvestment and heightening the risk of further cost spikes. Inventory buffers and dual sourcing offer partial relief but capex decisions for new contact adhesives market capacity are delayed amid uncertainty.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Robotic Adhesive-Dispensing Lines in Asian Footwear Plants

- Repair Demand for Wind-Turbine Blades

- Stringent VOC and Flammability Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solvent-borne systems retained 76.34% of the contact adhesives market in 2024, thanks to unmatched open-time flexibility and high initial tack. Footwear production lines, for instance, rely on rapid grab that keeps assembly throughput high. Yet waterborne grades are growing at a 4.98% CAGR due to VOC rules and advancements in resin emulsification that narrow the performance gap. California's latest consumer-products rule and Canada's 2024 VOC cap accelerate global standardization efforts toward solvent-free solutions.

Hot-melt and reactive chemistries play niche roles where temperature resistance or instant set outweigh cost. Suppliers such as 3M now advertise entirely solvent-free lines that equal older chloroprene formulations in peel strength, proving technology convergence is feasible. Over the forecast period, the contact adhesives market size for water-borne formulations is expected to reach USD 960 million, reflecting steady substitution in regulated regions.

The Contact Adhesives Report is Segmented by Technology (Water-Borne, Solvent-Borne, Others), Polymer (Polychloroprene, Styrene-Butadiene Rubber, Acrylic Copolymers, and More), End-User Industry (Consumer Durables and Electronics, Packaging, Automotive and Transportation, Furniture and Woodworking, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 59.55% of the contact adhesives market in 2024 and is projected to post a 5.05% CAGR, driven by China's diversified manufacturing base and India's government-led push for import substitution. Vietnam, Thailand, and Indonesia invest heavily in smart factories for athletic shoes, pushing regional demand for precise, low-VOC formulations. Despite periodic raw-material volatility, proximity to resin producers keeps landed costs favorable compared with imports into Europe or North America.

North America maintains a robust demand anchored in electric-vehicle production and stringent environmental standards. Automakers increasingly specify waterborne adhesives to secure credits under the United States Advanced Clean Transportation program, raising North American uptake for compliant grades. Regional suppliers leverage strong intellectual-property positions to command price premiums, boosting margins even as sales volumes grow at a moderate pace.

Europe's mature market is notable for regulatory leadership. Broad PFAS and formaldehyde restrictions under REACH prompt accelerated reformulation cycles. Europe also hosts a large installed base of wind-turbine blades now entering their repair life phase, placing specialized contact adhesives in steady demand.

South America and the Middle East, and Africa offer frontier opportunities tied to residential construction and light manufacturing. Currency volatility remains a headwind, yet regional governments are rolling out industrial parks with tax incentives that could attract adhesive converters.

- 3M

- AdCo UK Limited

- Aica Kogyo Co..Ltd.

- Arkema (Bostik)

- Collano

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- H.B. Fuller Company

- Helmitin Adhesives

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc. (ITW Performance Polymers)

- Intact Adhesives (KMS Adhesives Ltd)

- Jowat

- Mapei SpA

- Permabond

- Pidilite Industries Ltd

- Pyrotek

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Low-VOC Water-Borne Systems

- 4.2.2 Booming Modular Furniture and Interior Fitouts

- 4.2.3 Integration of Robotic Adhesive-Dispensing Lines in Asian Footwear Plants

- 4.2.4 Repair Demand for Wind-Turbine Blades

- 4.2.5 Thermal-Insulation Bonding Inside EV Battery Packs

- 4.3 Market Restraints

- 4.3.1 Raw-Material Price Volatility

- 4.3.2 Stringent VOC and Flammability Rules

- 4.3.3 Global Chloroprene Monomer Supply Disruptions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Raw Material Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Others

- 5.2 By Polymer

- 5.2.1 Polychloroprene (Neoprene)

- 5.2.2 Styrene-Butadiene Rubber (SBR)

- 5.2.3 Acrylic Copolymers

- 5.2.4 Polyurethane

- 5.2.5 Nitrile and Others

- 5.3 By End-user Industry

- 5.3.1 Consumer Durables and Electronics

- 5.3.2 Packaging

- 5.3.3 Automotive and Transportation

- 5.3.4 Furniture and Woodworking

- 5.3.5 Footwear and Leather Goods

- 5.3.6 Construction (Flooring, Panels, Roofing)

- 5.3.7 Other End User Industries (Wind energy, DIY, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 AdCo UK Limited

- 6.4.3 Aica Kogyo Co..Ltd.

- 6.4.4 Arkema (Bostik)

- 6.4.5 Collano

- 6.4.6 DELO Industrie Klebstoffe GmbH & Co. KGaA

- 6.4.7 H.B. Fuller Company

- 6.4.8 Helmitin Adhesives

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International LLC

- 6.4.11 Illinois Tool Works Inc. (ITW Performance Polymers)

- 6.4.12 Intact Adhesives (KMS Adhesives Ltd)

- 6.4.13 Jowat

- 6.4.14 Mapei SpA

- 6.4.15 Permabond

- 6.4.16 Pidilite Industries Ltd

- 6.4.17 Pyrotek

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Shifting Focus toward Water-borne Adhesives