|

市场调查报告书

商品编码

1844639

催化剂再生:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Catalyst Regeneration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

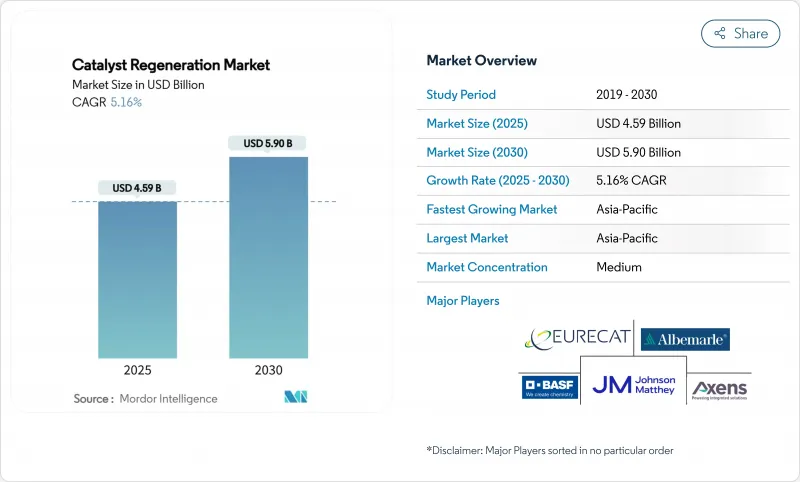

预计 2025 年催化剂再生市场规模为 45.9 亿美元,到 2030 年将达到 59 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.16%。

这一稳定的成长轨迹得益于日益严格的排放法规、不断上涨的新催化剂成本以及鼓励低碳生产路线的循环经济指令的不断扩展。事实上,炼油厂和石化企业越来越重视废催化剂的处理,塑胶热解和挥发性有机化合物 (VOC) 减量等新应用吸引了越来越多的客户。低温臭氧氧化和预测分析等技术进步进一步促进了停机时间的减少和成本效率的提高,推动了成熟经济体和新兴经济体催化剂再生市场的发展。

全球催化剂再生市场趋势与见解

有关炼油厂和石化排放的严格环境法规

国家和地区监管机构正在收紧允许排放法规,从而改变催化剂再利用的经济性。美国环保署更新的《有害空气污染物标准》将每年减少2,200吨有害排放,每年带来超过1亿美元的货币化健康效益。加州的低碳燃料标准要求在2030年将燃料循环的碳强度降低30%,到2045年降低90%,这推动了对再生催化剂的需求,以符合生命週期核算规则。欧盟的《工业排放指令》已将催化剂再生纳入其废弃物处理的最佳可用技术,进一步加强了以合规为导向的再生主导于掩埋的规定。亚洲各地正在製定类似的法规,迅速扩大催化剂再生的影响。

再生触媒成本压力上升

钯、铂和铑的价格波动使得再生催化剂的采购成为一项高风险的预算项目。学术评估表明,再生轻度污染的水处理催化剂可以恢復80%以上的基准活性,而成本不到新催化剂的一半。海湾化学冶金公司营运的金属回收设施通常将99%的废催化剂转化为可销售的钼和镍流,从而提高了炼油厂的循环价值。在亚太地区产量较大的枢纽,成本节省倍增,促使设施经理签订多年期再生协议。

金属中毒催化剂回收率降低

重质原油中的钒、镍和铁会不可逆地与活性位点结合,进而降低再生产率。实验室研究表明,钒含量超过5%(重量百分比)会导致孔隙堵塞和相变,使加氢脱硫活性降低一半以上。改良的脱金属处理方法可以去除高达89.2%的镍,但通常会以牺牲骨架稳定性为代价,从而限制其再利用週期。因此,使用残余原料的业者必须权衡部分回收的成本与购买新催化剂的成本,有时甚至会选择将其丢弃。

細項分析

现场设施拥有强大的热处理和化学处理系统,能够恢復 80-90% 的新鲜活性,到 2024 年将占据催化剂再生市场份额的 73.18%。领先的服务提供者在金属提取之前在分级窑中去除碳氢化合物、碳和硫,并将再生量通过可无缝插入炼油厂的道路认可桶返回现场。

随着臭氧氧化技术的成熟,直接在製程设备内应用的原位再生技术正以5.88%的复合年增长率蓬勃发展。连续催化重整器操作员意识到,低温氧化可以限制反应器的冶金应力,延长容器寿命并减少停机时间。早期采用者报告称,与将原料送至异地相比,该技术可节省10天的周转时间,并将每吨催化剂再生的市场成本降低近15%。

催化剂再生报告按方法(原位和非原位)、应用(炼油厂和石化联合企业、环境、能源和电力、其他应用)和地区(亚太地区、北美、欧洲、南美、中东和非洲)细分。市场预测以美元计算。

区域分析

预计到2024年,亚太地区将占全球需求的42.54%,这得益于高炼油产能、深度石化一体化以及先进的回收法规。到2030年,催化剂再生市场的复合年增长率将达到5.67%,其中亚太地区将占据主导地位。日本回收商经营综合设施,将受污染的催化剂、废弃电池和电子废弃物转化为高纯度钯和钒,确保国内原料的流通。在印度,待开发区的综合炼油厂计划投资现场再生列车,以避免跨国废弃物运输。

北美正受益于监管确定性和数位化领导力。美国墨西哥湾沿岸的炼油厂正在将运作资料馈送输入云端基础演算法,以推荐最佳燃烧时间;加拿大加氢裂解厂正在接收根据闭合迴路合约交付的回收钴钼系统,以确保金属价格。碳排放税抵免正在增加第二条收益来源,鼓励中部大陆的独立炼油厂在合规调整日期之前安排返工。

在欧洲,严格的环境监管与製程技术出口正在取得平衡。法国和德国的授权人正在捆绑供应和再生方案,使中东客户能够透过欧洲枢纽获得「从摇篮到摇篮」的服务。随着专用反应器转向客製化催化剂等级,需要精确的再生循环来保持选择性,欧盟对绿氢能和电子燃料的资助将进一步刺激区域需求。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 有关炼油厂和石化排放的严格环境法规

- 新鲜催化剂的成本压力不断增加

- 碳强度要求有利于回收催化剂

- 现场臭氧氧化技术的突破减少了停机时间

- 预测分析实现基于条件的再生

- 市场限制

- 降低金属污染催化剂的回收率

- 缺乏全球实验室检测标准

- 一次性奈米催化剂在特定製程的兴起

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 依方法

- 矿井外

- 现场施工

- 按用途

- 炼油厂和石化综合体

- 环境

- 能源和电力

- 其他用途(塑胶热解、特殊用途)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- Advanced Catalyst Systems

- Albemarle Corporation

- AMETEK Inc.

- Axens

- BASF

- CORMETECH

- EBINGER Katalysatorservice GmbH & Co. KG

- Eurecat

- EvoNik Industries AG

- Honeywell International Inc.

- Johnson Matthey

- NIPPON KETJEN Co. Ltd.

- Topsoe A/S

- WR Grace and Co.

- Yokogawa Cororation. of America

第七章 市场机会与未来展望

The Catalyst Regeneration Market size is estimated at USD 4.59 billion in 2025, and is expected to reach USD 5.90 billion by 2030, at a CAGR of 5.16% during the forecast period (2025-2030).

This steady trajectory is underpinned by increasingly stringent emission norms, the escalating cost of fresh catalysts, and expanding circular-economy mandates that reward lower-carbon production routes. In practice, refineries and petrochemical complexes are sharpening focus on end-of-life catalyst handling, while emerging applications in plastics pyrolysis and volatile organic compound (VOC) abatement broaden the customer base. Technology advances such as low-temperature ozone oxidation and predictive analytics further reduce downtime and enhance cost efficiency, reinforcing the momentum of the catalyst regeneration market across both mature and developing economies.

Global Catalyst Regeneration Market Trends and Insights

Strict Environmental Regulations on Refinery and Petrochemical Emissions

National and regional regulators are tightening allowable emission limits, changing the economics of catalyst reuse. The U.S. Environmental Protection Agency's updated hazardous-air-pollutant standards will cut toxic releases by 2,200 short tons a year and deliver monetized health benefits exceeding USD 100 million annually. California's Low Carbon Fuel Standard requires a 30% reduction in fuel-cycle carbon intensity by 2030 and 90% by 2045, elevating demand for regenerated catalysts to comply with lifecycle accounting rules. The EU's Industrial Emissions Directive embeds catalyst regeneration in Best Available Techniques for waste treatment, reinforcing a compliance-driven preference for regeneration over landfill. Across Asia, similar limits are being drafted, ensuring the driver's influence spreads rapidly.

Rising Cost Pressure of Fresh Catalysts

Volatile prices for palladium, platinum, and rhodium have turned fresh catalyst procurement into a high-risk budget item. Academic assessments show that regenerating lightly fouled hydroprocessing catalysts recovers more than 80% of baseline activity at less than half the cost of a new supply. Metal-recovery facilities operated by Gulf Chemical and Metallurgical Corporation routinely convert 99% of spent catalyst into sellable molybdenum and nickel streams, illustrating the circular-value upside for refiners. In volume-heavy APAC hubs, the savings multiply, prompting facility managers to lock in multi-year regeneration contracts.

Lower Recovery on Metal-Poisoned Catalysts

Vanadium, nickel, and iron from heavy crudes bind irreversibly to active sites, curtailing regeneration yields. Laboratory work shows vanadium loads above 5 wt.% slash hydrodesulfurization activity by more than half because of pore blockage and phase changes. Although modified demetallization treatments strip up to 89.2% of nickel, they often damage framework stability, limiting reuse cycles. Operators running resid feeds therefore weigh the cost of partial recovery against fresh catalyst outlay, sometimes opting for disposal.

Other drivers and restraints analyzed in the detailed report include:

- Carbon-Intensity Mandates Favouring Regenerated Catalysts

- On-Site Ozone-Oxidation Breakthroughs Cut Downtime

- Lack of Global Lab Test-Method Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ex-situ facilities captured 73.18% of the catalyst regeneration market share in 2024 on the strength of robust thermal and chemical treatment trains capable of restoring 80-90% of fresh activity. Leading service providers remove hydrocarbons, carbon, and sulfur in staged kilns before metal extraction, delivering regenerated volumes back to the site in road-approved drums that slot seamlessly into refining units.

In-situ regeneration, applied directly inside process equipment, is gaining 5.88% CAGR momentum as ozone-oxidation technology matures. Continuous catalytic reformer operators appreciate that low-temperature oxidation curbs metallurgical stress on reactors, extending vessel life while slashing downtime. Early adopters report 10-day turnaround savings compared with sending material off-site and cutting the catalyst regeneration market cost per tonne by nearly 15%.

The Catalyst Regeneration Report is Segmented by Method (Ex-Situ and In-Situ), Application (Refineries and Petrochemical Complexes, Environmental, Energy and Power, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific carried 42.54% of global demand in 2024 thanks to high refining capacity, deep petrochemical integration, and progressive recycling regulations. Regional growth of 5.67% CAGR through 2030 keeps the catalyst regeneration market firmly centered on APAC. Japanese recyclers run integrated facilities that convert fouled catalyst, spent batteries, and electronic scrap into high-purity palladium and vanadium, ensuring secure domestic raw-material flows. In India, greenfield integrated refineries earmark capex for on-site regeneration trains to avoid cross-border waste shipments.

North America benefits from regulatory certainty and digital leadership. Refineries on the U.S. Gulf Coast stream operating-data feeds to cloud-based algorithms that recommend optimal burn times, while Canadian hydrocrackers receive recycled Co-Mo systems delivered under closed-loop contracts that guarantee metals buy-back pricing. Carbon-tax credits add a second revenue line, nudging mid-continental independent refiners to schedule regeneration just before compliance reconciliation dates.

Europe balances stringent environmental oversight with process-technology exports. French and German licensors bundle supply-and-regeneration packages, allowing clients in the Middle East to receive cradle-to-cradle service routed through European hubs. EU funding for green hydrogen and e-fuels further boosts regional demand as specialty reactors switch to tailored catalyst grades that require precise regeneration cycles to maintain selectivity.

- Advanced Catalyst Systems

- Albemarle Corporation

- AMETEK Inc.

- Axens

- BASF

- CORMETECH

- EBINGER Katalysatorservice GmbH & Co. KG

- Eurecat

- EvoNik Industries AG

- Honeywell International Inc.

- Johnson Matthey

- NIPPON KETJEN Co. Ltd.

- Topsoe A/S

- W.R. Grace and Co.

- Yokogawa Cororation. of America

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict Environmental Regulations on Refinery And Petrochemical Emissions

- 4.2.2 Rising Cost-Pressure of Fresh Catalysts

- 4.2.3 Carbon-Intensity Mandates Favouring Regenerated Catalysts

- 4.2.4 On-Site Ozone-Oxidation Breakthroughs Cut Downtime

- 4.2.5 Predictive Analytics Enabling Condition-Based Regeneration

- 4.3 Market Restraints

- 4.3.1 Lower Recovery on Metal-Poisoned Catalysts

- 4.3.2 Lack of Global Lab Test-Method Standards

- 4.3.3 Rise of Single-Use Nano-Catalysts in Select Processes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Method

- 5.1.1 Ex-Situ

- 5.1.2 In-Situ

- 5.2 By Application

- 5.2.1 Refineries and Petrochemical Complexes

- 5.2.2 Environmental

- 5.2.3 Energy and Power

- 5.2.4 Other Application (Plastics Pyrolysis, Speciality)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Advanced Catalyst Systems

- 6.4.2 Albemarle Corporation

- 6.4.3 AMETEK Inc.

- 6.4.4 Axens

- 6.4.5 BASF

- 6.4.6 CORMETECH

- 6.4.7 EBINGER Katalysatorservice GmbH & Co. KG

- 6.4.8 Eurecat

- 6.4.9 EvoNik Industries AG

- 6.4.10 Honeywell International Inc.

- 6.4.11 Johnson Matthey

- 6.4.12 NIPPON KETJEN Co. Ltd.

- 6.4.13 Topsoe A/S

- 6.4.14 W.R. Grace and Co.

- 6.4.15 Yokogawa Cororation. of America

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

催化剂再生市场(按催化剂类型、再生技术和应用划分)—2025-2032年全球预测

催化剂再生市场(按催化剂类型、再生技术和应用划分)—2025-2032年全球预测 催化剂再生市场规模、份额及成长分析(按催化剂类型、再生方法、应用、最终用户和地区)- 产业预测,2025-2032

催化剂再生市场规模、份额及成长分析(按催化剂类型、再生方法、应用、最终用户和地区)- 产业预测,2025-2032 催化剂再生市场:预测(2025-2030)

催化剂再生市场:预测(2025-2030)