|

市场调查报告书

商品编码

1844641

耐热涂料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Heat-Resistant Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

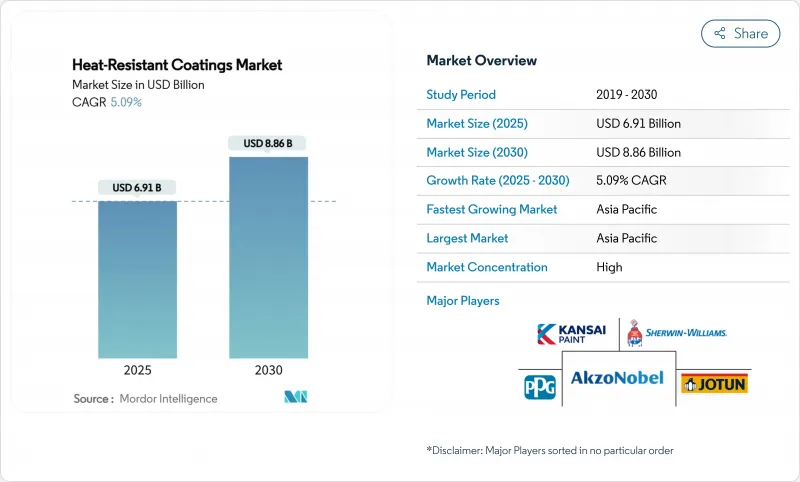

耐热涂料市场规模预计在 2025 年达到 69.1 亿美元,预计到 2030 年将达到 88.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.09%。

全球基础设施投资增加、消防安全法规更加严格以及可重复使用太空船推动的航太产业持续推动需求。亚太地区透过政府主导的建设计划和扩大製造业保持规模优势,而北美和欧洲则强调符合更严格环境法规的高性能解决方案。技术采用呈现两种明显的趋势:水性系统因其低 VOC排放而保持其产量优势,而 UV/EB 固化化学品因其快速固化和最小环境影响的结合而增长最快。有机硅树脂在 600°C 以上具有无与伦比的稳定性,在规模和成长方面占据主导地位,新兴发电工程正在将产量转移到温度控管至关重要的能源基础设施。虽然原料价格波动和认证施用器短缺仍然是不利因素,但永续配方和自动喷涂系统的持续创新使长期前景更加光明。

全球耐热涂料市场趋势与洞察

全球基础设施支出激增

各国政府正以创纪录的水平投资基础设施建设,以应对气候变迁并支持城市发展。美国《基础建设投资与就业法案》累计2.25亿美元,用于更新影响涂层规格的能源标准。亚太地区新兴经济体发展势头强劲,印尼、印度和中国加快了机场、桥樑和智慧城市计划的建设,并指定使用高温阻隔膜。交通隧道和区域供热管道领域的官民合作关係将进一步推动长週期隔热涂层的需求。

加强全球消防安全法规

消防法规改革提高了耐火性、烟雾毒性和最终使用表面温度的最低性能标准。 2024年国际消防法规引入了更新的火灾蔓延标准,这将立即影响涂料配方。加州消防法规第24章要求,处理耐热产品的喷漆房必须配备自动灭火系统和专用通风设备。欧盟指令持续降低允许的溶剂含量,促使建筑商转向低VOC有机硅-丙烯酸混合物。随着业主要求其资产符合法规要求,高层建筑建筑幕墙和交通枢纽的维修正在推动需求激增。认证其产品达到或超过新基准值的製造商将获得规范优先权,并减少昂贵的返工需求。

硅胶和环氧树脂价格不稳定

美国国际贸易委员会的裁决发现,某些环氧树脂的进口价格低于公允价值,导致国内供应紧张,成本上涨。亚洲主要有机硅工厂同时关闭,加剧了价格波动。没有长期合约的小型配方製造商面临两位数的成本成长,利润率下降,产品被迫重新定价。生产商透过复製前体或扩大内部单体产能进行对冲,但资本支出推迟了立即缓解压力的措施。虽然原材料波动具有周期性,但它会在短期内给现金流带来压力,并阻碍研发支出。

細項分析

到2024年,硅胶树脂将占据耐热涂料市场份额的38.16%,这得益于其优异的化学特性,使其能够承受600°C以上的高温而不会失去附着力。到2030年,硅树脂的复合年增长率将达到8.90%,是耐热涂料市场的关键成长引擎。其需求涵盖排气管、火炬管、烘烤炉、航太零件以及其他不允许故障的零件。环氧树脂在中温范围内仍保持其重要性,但面临成本方面的阻力以及双酚A衍生物的监管审查。丙烯酸树脂非常适合价格敏感型消费品应用,这些应用的峰值表面温度较低。

耐热涂料报告按树脂类型(有机硅、环氧树脂、丙烯酸、其他树脂)、技术类型(溶剂型、水基、粉末、UV/EB 固化)、最终用户行业类型(建筑和施工、石油和天然气、电力部门、运输、木工和家具、消费品、其他最终用户行业)和地区类型(亚太地区、北美、欧洲、南美、中东和非洲)行业。

区域分析

到2024年,亚太地区将占全球总收入的47.81%,复合年增长率为7.50%。中国的「一带一路」走廊需要用于桥樑和隧道的耐热底漆,因为这些桥樑和隧道面临野火和化学品洩漏的风险。印度正在「印度製造」计划下扩大国内炉灶、锅炉和工业烤箱的生产,所有这些产品都要求使用耐热薄膜。

北美仍然是技术创新的中心。美国和加拿大的顶级航太公司指定使用军用级金属和陶瓷阻隔涂层。联邦基础设施投资,例如更换老化桥樑和改善能源网,要求每个计划都采用低VOC、耐高温的涂层。

欧洲正在优先考虑永续性。欧盟挥发性有机化合物(VOC)的限值逐年严格,鼓励建商采用水性硅胶和粉末涂料。德国、法国和义大利的汽车平台正在整合涂有奈米结构陶瓷薄膜的轻质金属零件,以实现热管理。虽然南美洲、中东和非洲的市场规模较小,但技术转移和国际安全标准的采用正在扩大整体可利用的耐热涂料市场。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 全球基础设施支出激增

- 加强世界各地的消防安全法规

- 航太业的需求不断成长

- 提高防火设备意识

- 可重复使用的太空船和太空旅游船

- 市场限制

- 硅胶和环氧树脂价格波动

- 溶剂型系统的VOC法规

- 缺乏多层涂层系统的涂层技术

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 按树脂

- 硅酮

- 环氧树脂

- 丙烯酸纤维

- 其他树脂(聚氨酯、醇酸树脂等)

- 依技术

- 溶剂型

- 水性

- 粉末

- UV/EB固化型

- 按最终用户产业

- 建筑/施工

- 石油和天然气

- 电力业

- 运输

- 木工和家具

- 消费品

- 其他终端用户产业(工业加工设备等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- 3M

- Advanced Industrial Coatings

- AkzoNobel NV

- Aremco

- Arkema

- Axalta Coating Systems LLC

- BASF

- Belzona International Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd.

- KCC Corporation

- Momentive

- PPG Industries Inc.

- Teknos Group

- The Sherwin-Williams Company

- Wacker Chemie AG

第七章 市场机会与未来展望

The Heat-Resistant Coatings Market size is estimated at USD 6.91 billion in 2025, and is expected to reach USD 8.86 billion by 2030, at a CAGR of 5.09% during the forecast period (2025-2030).

Rising global infrastructure investments, tighter fire-safety rules and the aerospace sector's push for reusable spacecraft continue to widen demand. Asia-Pacific retains scale advantages through government-led building programs and manufacturing expansion, while North America and Europe emphasize high-performance solutions that meet stricter environmental rules. Technology adoption shows two clear tracks: water-borne systems hold volume leadership owing to lower VOC emissions, and UV/EB-curable chemistries post the fastest gains by combining rapid cure with minimal environmental impact. Silicone-based resins dominate both scale and growth because of unmatched stability above 600 °C, and emerging power-generation projects are shifting volume toward energy infrastructure where thermal management is critical. Raw-material price swings and a shortage of certified applicators remain counterweights, yet sustained innovation in sustainable formulations and automated spray systems keeps the long-term outlook positive.

Global Heat-Resistant Coatings Market Trends and Insights

Surge in Global Infrastructure Spending

Governments are funding record levels of infrastructure aimed at climate resilience and urban growth. The United States Infrastructure Investment and Jobs Act earmarked USD 225 million for updated energy codes that influence coating specifications. Emerging Asia-Pacific economies add momentum as Indonesia, India, and China accelerate airport, bridge, and smart-city projects that specify high-temperature barrier films. Public-private partnerships in transport tunnels and district-heating lines further widen demand for long-cycle thermal coatings.

Stricter Global Fire-Safety Regulations

Fire-code revisions raise minimum performance thresholds for ignition resistance, smoke toxicity, and end-use surface temperature. The International Fire Code 2024 introduces updated flame-spread benchmarks that immediately affect coating formulations. California's Fire Code Chapter 24 mandates automatic extinguishing systems and specialized ventilation for coating booths handling heat-resistant products. EU directives continue to shrink allowed solvent content, pushing builders toward low-VOC silicone-acrylic hybrids. Retrofits of high-rise facades and transportation hubs create demand spikes as owners bring assets into compliance. Manufacturers that certify products above the new baseline win specification priority and reduce the need for costly rework.

Volatile Silicone and Epoxy Prices

A United States International Trade Commission ruling found certain epoxy imports were sold below fair value, tightening domestic supply and raising costs. Simultaneous outages in key Asian silicone plants amplified volatility. Smaller formulators lacking long-term contracts faced double-digit cost spikes that eroded margins and triggered product repricing. Producers hedge by dual-sourcing precursors and expanding in-house monomer capacity, but capital outlays delay immediate relief. Although raw-material swings are cyclical, they compress cash flow and hinder research and development spending in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand from the Aerospace Industry

- Rising Awareness Toward Fire Protection Equipment

- VOC Limits on Solvent-Borne Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone resins accounted for 38.16% of the 2024 heat-resistant coatings market share, reflecting the chemistry's ability to tolerate temperatures above 600 °C without losing adhesion. That leadership is matched by the fastest segment CAGR of 8.90% through 2030, making silicone the pivotal growth engine of the heat-resistant coatings market. Demand spans exhaust stacks, flare stacks, bake ovens, and aerospace parts where failure is unacceptable. Epoxies retain relevance in mid-temperature zones but face cost headwinds and regulatory scrutiny on bisphenol-A derivatives. Acrylics fill price-sensitive applications in consumer goods where surface temperature peaks are lower.

The Heat-Resistant Coatings Report is Segmented by Resin (Silicone, Epoxy, Acrylic, Other Resins), Technology (Solvent-Borne, Water-Borne, Powder, UV/EB-curable), End-User Industry (Building and Construction, Oil and Gas, Power Sector, Transportation, Woodworking and Furniture, Consumer Goods, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific led with 47.81% of 2024 revenue and advances at 7.50% CAGR, powered by megaprojects in transport, housing, and energy. China's Belt and Road corridors require heat-resistant primers for bridges and tunnels exposed to wildfire and chemical spill risks. India, under its Make in India vision, expands domestic manufacturing of cookstoves, boilers, and industrial ovens that all specify heat-stable films.

North America remains an innovation center. Aerospace primes in the United States and Canada specify metallic and ceramic barrier coats qualified to MIL standards. Federal infrastructure outlays replace aging bridges and improve energy grids, each project mandating low-VOC, high-temperature finishes.

Europe emphasizes sustainability. EU VOC ceilings tighten yearly, pushing builders to waterborne silicones and powder options. Automotive platforms in Germany, France, and Italy integrate lightweight metal components coated with nano-structured ceramic films for thermal regulation. Markets in South America, the Middle East and Africa grow from a smaller base yet benefit from technology transfer and the adoption of international safety codes, widening the total addressable heat-resistant coatings market.

- 3M

- Advanced Industrial Coatings

- AkzoNobel N.V.

- Aremco

- Arkema

- Axalta Coating Systems LLC

- BASF

- Belzona International Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd.

- KCC Corporation

- Momentive

- PPG Industries Inc.

- Teknos Group

- The Sherwin-Williams Company

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Global Infrastructure Spending

- 4.2.2 Stricter Global Fire-safety Regulations

- 4.2.3 Growing Demand from the Aerospace Industry

- 4.2.4 Rising Awareness Toward Fire Protection Equipment

- 4.2.5 Re-usable Spacecraft and Space-tourism Vehicles

- 4.3 Market Restraints

- 4.3.1 Volatile Silicone and Epoxy Prices

- 4.3.2 VOC Limits on Solvent-borne Systems

- 4.3.3 Applicator Skill Shortage for Multi-layer Systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Silicone

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Other Resins (Polyurethane, Alkyd, etc.)

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Powder

- 5.2.4 UV/EB-curable

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Oil and Gas

- 5.3.3 Power Sector

- 5.3.4 Transportation

- 5.3.5 Woodworking and Furniture

- 5.3.6 Consumer Goods

- 5.3.7 Other End-user Industries (Industrial Processing Equipment, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Advanced Industrial Coatings

- 6.4.3 AkzoNobel N.V.

- 6.4.4 Aremco

- 6.4.5 Arkema

- 6.4.6 Axalta Coating Systems LLC

- 6.4.7 BASF

- 6.4.8 Belzona International Ltd.

- 6.4.9 Hempel A/S

- 6.4.10 Jotun

- 6.4.11 Kansai Paint Co. Ltd.

- 6.4.12 KCC Corporation

- 6.4.13 Momentive

- 6.4.14 PPG Industries Inc.

- 6.4.15 Teknos Group

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

二氧化硅防腐颜料市场依等级类型、产品形态、应用、终端用户产业及通路划分-2026-2032年全球预测工业高温耐火涂料市场按类型、技术、温度范围、应用方法、应用领域和最终用途行业划分,全球预测(2026-2032年)高温航太涂料市场:按化学成分、飞机类型、涂层厚度、最终用途和应用方法划分-全球市场预测(2026-2032 年)

二氧化硅防腐颜料市场依等级类型、产品形态、应用、终端用户产业及通路划分-2026-2032年全球预测工业高温耐火涂料市场按类型、技术、温度范围、应用方法、应用领域和最终用途行业划分,全球预测(2026-2032年)高温航太涂料市场:按化学成分、飞机类型、涂层厚度、最终用途和应用方法划分-全球市场预测(2026-2032 年) 2018-2034年全球耐热涂料市场需求及预测分析

2018-2034年全球耐热涂料市场需求及预测分析 全球耐热涂料市场成长、规模及趋势分析(按类型、技术及应用)-区域展望、竞争策略及2034年细分市场预测

全球耐热涂料市场成长、规模及趋势分析(按类型、技术及应用)-区域展望、竞争策略及2034年细分市场预测 全球耐热涂料市场规模(依技术、树脂类型、应用、地区、范围和预测)

全球耐热涂料市场规模(依技术、树脂类型、应用、地区、范围和预测)