|

市场调查报告书

商品编码

1844661

生物酒精:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Bio-alcohols - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

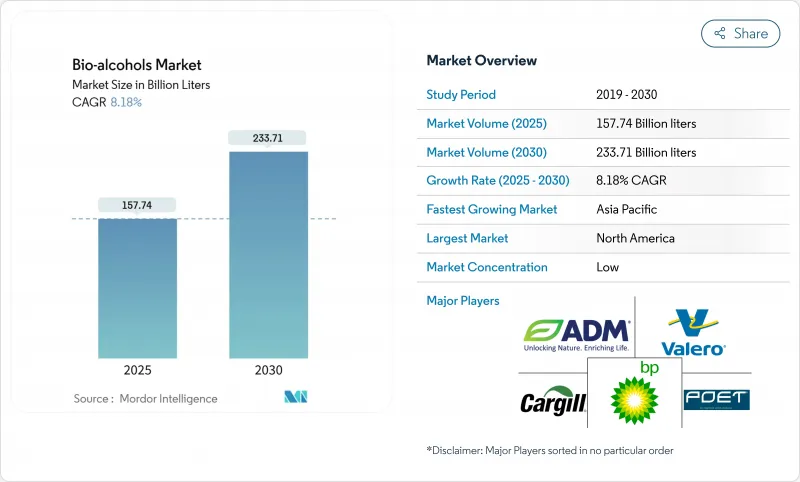

预计 2025 年生物酒精市场规模为 1,577.4 亿公升,到 2030 年将达到 2,337.1 亿公升,预测期内(2025-2030 年)的复合年增长率为 8.18%。

这一增长反映了可再生燃料法规的加强、酒精转航空认证的快速进展,以及商业化碳转酒精系统的出现,这些系统在减少排放的同时,为炼油厂创造了新的收益。永续船用燃料走廊、消费品中高端化学品的应用以及投资者对低碳供应链日益增长的兴趣也在影响着需求。在北美老牌製造商维持规模经济的同时,亚太地区在政策利好和成本优化技术的推动下,产能正在迅速扩张。与航空公司和船运商签订的策略性承购协议也为投资者提供了清晰的现金流。

全球生物酒精市场趋势与洞察

强制乙醇混合

强制混合燃料可确保需求,降低投资者风险,并加速工厂扩张。印度的目标是到2030年将乙醇混合比例提高到30%,目前已达到20%,彰显了雄心勃勃的政策带来的正面影响。欧盟的ReFuel欧盟航空法规将从2025年开始将SAF比例从2%提高到2050年的70%。巴西的E27计画可作为在物流障碍消除后实现更高混合比例的模板。强制混合燃料可使生产免受大宗商品波动的影响,允许生产商签订长期原料合约并降低资金筹措成本。

酒精转航空航线快速航空公司 SAF 认证

航空业对净零排放的推动正在迅速加速酒精转化为航空燃料的测试。 LanzaJet位于乔治亚的Freedom Pines燃料工厂目前年产量已达900万加仑,这让投资者对大型工厂的可靠运作充满信心。 Accens的Jetanol计划目前计画年产量超过10亿加仑,证实了该技术的可行性。由于SAF的售价通常是传统喷射机燃料的两到三倍,生质乙醇生产商在转向航空公司时可以获得更高的利润。长期的航空公司承购协议,例如西南航空与美国生物能源公司(USA BioEnergy)达成的协议,进一步降低了计划现金流风险。

高混合酒精的管道相容性较差

由于腐蚀和吸湿,大多数石油管线无法输送高混合度的醇类,因此只能依赖卡车和铁路运输。额外的物流成本使得运输价格缺乏竞争力,尤其是在远离混合终端的地区。管道升级需要多家业主的合作,这需要高昂的资本支出,而这在某些市场尚不合理。

細項分析

预计到2024年,生质乙醇的市占率将达到68.05%。生质乙醇的转化成本优势和全球供应链巩固了其领先地位。预计生物乙醇市场规模将随着国家混合燃料限制措施的实施而稳定扩大,即使汽油达到峰值,绝对产量仍将保持成长。然而,生质乙醇卓越的能量密度和直接相容性正在推动对高端化学品的需求,复合年增长率高达9.40%。

酒精转化为喷射燃料的突破为乙醇开闢了更高价值的出路。 LanzaJet 的早期营运数据证实,低成本的农业乙醇可以升级为 SAF,售价可提高两到三倍。同时,生物甲醇正在进入船用燃料和塑胶领域,而生物 BDO 则填补了医药和工程材料领域的空白。整体而言,特种酒精使生物酒精市场更加多元化,降低了对道路燃料波动的敏感度。

生物酒精市场报告按产品类型(生物甲醇、生质乙醇、生物丁醇、生物BDO等)、原料(淀粉作物、糖作物、木质纤维素生物质等)、应用(运输、建筑、电子等)和地区(亚太地区、北美、欧洲、南美、中东和非洲)细分。市场预测以产量(公升)计算。

区域分析

北美2024年将占比39.44%,这反映了其密集的玉米製乙醇走廊、充足的铁路物流以及维持基准产量的可再生燃料标准。加拿大2025年无污染燃料法规将扩大美国以外地区对低碳混合燃料的需求。墨西哥对新麵粉厂的投资将使该大陆融入自我强化的供应链。 Summit Next Gen公司在德克萨斯州投资16亿美元的乙醇-SAF综合体有资格获得JETI拨款,这表明地方补贴与联邦税额扣抵如何相结合,以吸引大型企划。

亚太地区是成长引擎,复合年增长率达9.55%,这得益于印度快速转向30%的混合燃料以及对大米原料创纪录的需求。中国正透过资助与其2060年零排放计画相关的二氧化碳-酒精混合燃料试点项目,获得成长动力;而日本和韩国则正在向炼油厂和机场推出绿色燃料奖励。包括菲律宾在内的东协市场也正在取消混合燃料限制,维持了该地区的广泛需求。这些政策趋势正在吸引将本地原料与进口技术结合的合资企业,加速产能扩张。

在欧洲,严格的碳排放价格和永续燃料(SAF)强制规定正在迅速扩大高端市场。 ReFuelEU 规则手册为投资者明确了未来永续燃料(SAF)的扩张方向,德国和英国正在实施国家补贴以确保国内生产。原料灵活性,包括甜菜和废弃物物质,有助于缓衝供应衝击。南美洲继续利用先进的第二代工厂加工廉价的甘蔗和甘蔗渣,支持向亏损地区稳定出口。作为多元化策略的一部分,中东和非洲正在进行规模较小的试点计划。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 强制性乙醇混合目标

- 酒精转航空航线快速航空公司 SAF 认证

- 炼油厂中二氧化碳和酒精CCU工厂的整合

- 生物酒精作为CPG低碳化学原料的用途

- 甲醇动力来源运输走廊的出现

- 市场限制

- 原物料价格波动

- 缺乏高混合酒精管道相容性。

- 2027年后全球微型车产量将停滞不前

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测(数量)

- 依产品类型

- 生物甲醇

- 生质乙醇

- 生物丁醇

- 生物BDO

- 其他生物酒精

- 按原料

- 作物作物

- 糖料作物

- 木质纤维素生物质

- 藻类生物量

- 工业废弃物

- 按用途

- 运输

- 建造

- 电子产品

- 製药

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- Abengoa

- ADM

- BASF SE

- BP plc

- Cargill Incorporated

- CropEnergies AG

- Gevo

- Green Plains Inc.

- INEOS

- Mascoma LLC

- POET LLC

- Raizen

- SEKISUI CHEMICAL CO., LTD.

- Valero Energy Corporation

第七章 市场机会与未来展望

The Bio-alcohols Market size is estimated at 157.74 billion liters in 2025, and is expected to reach 233.71 billion liters by 2030, at a CAGR of 8.18% during the forecast period (2025-2030).

This growth reflects tightening renewable-fuel rules, quick progress in alcohol-to-jet certification, and the arrival of commercial carbon-capture-to-alcohol systems that give refiners fresh revenue while cutting emissions. Demand is also being reshaped by sustainable marine-fuel corridors, premium chemical uses in consumer goods, and stronger investor appetite for low-carbon supply chains. Established North American producers keep scale advantages, yet Asia-Pacific is adding capacity faster thanks to policy tailwinds and cost-optimized technologies. Feedstock innovation, especially with algae and industrial off-gases, is helping moderate margin risks linked to crop price swings, while strategic offtake deals with airlines and shippers give investors cash-flow clarity.

Global Bio-alcohols Market Trends and Insights

Mandated Ethanol-Blend Targets

Blend mandates guarantee demand, reduce investor risk, and speed plant expansions. India's goal of 30% blending by 2030, having already reached 20%, shows the upside that ambitious policy can unlock. The EU's ReFuelEU Aviation rule starts with 2% SAF in 2025 and rises to 70% by 2050, offering a clear runway for alcohol-to-jet projects. Brazil's E27 program remains a template for high blend ratios once logistics barriers ease. Because mandates shield volumes from commodity swings, producers can line up long-term feedstock contracts and lower financing costs.

Rapid Airline SAF Certification of Alcohol-to-Jet Pathways

Aviation's net-zero push has sharply accelerated testing of alcohol-to-jet routes. LanzaJet's Freedom Pines Fuels site in Georgia already makes 9 million gallons a year and gives financiers confidence that large plants will run reliably. Axens' Jetanol projects now top 1 billion gallons per year of planned capacity, underlining the technology's bankability. SAF often sells at two to three times the price of conventional jet fuel, so bio-ethanol producers enjoy wider margins when they pivot toward aviation customers. Long-term airline offtake deals, such as Southwest's agreement with USA BioEnergy, further derisk project cash flows.

Insufficient Pipeline Compatibility for High-Blend Alcohols

Most petroleum pipelines cannot handle high alcohol blends due to corrosion and water uptake, forcing reliance on truck or rail. The extra logistics cost erodes delivered-price competitiveness, especially in regions far from blending terminals. Upgrading lines needs cooperation between many owners and warrants high capital that some markets cannot justify yet.

Other drivers and restraints analyzed in the detailed report include:

- Integration of CO2-to-Alcohol CCU Plants at Refineries

- Bio-Alcohol as Low-Carbon Chemical Feedstock in CPG

- Stagnant Global Light-Vehicle Production Post-2027

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bio-ethanol kept a 68.05% 2024 Bio-alcohol market share, underpinned by mature plants, standardized specs, and supportive mandates. Its conversion cost edge and global supply chain reinforce leadership. The Bio-alcohol market size for bio-ethanol is expected to expand steadily in line with nationwide blend limits that increase absolute volume even as gasoline peaks. Yet bio-butanol's superior energy density and drop-in compatibility are propelling its 9.40% CAGR and a rising slice of premium chemical demand.

Alcohol-to-jet breakthroughs provide a higher-value outlet for ethanol. LanzaJet's early operating data confirm that low-cost agricultural ethanol can be upgraded into SAF that sells at a 2-3X price multiple. Meanwhile, bio-methanol is carving room in marine fuels and plastics, and bio-BDO caters to pharmaceutical and engineered-material niches. Collectively, specialty alcohols diversify the Bio-alcohol market and lessen sensitivity to road-fuel swings.

The Bio-Alcohol Market Report is Segmented by Product Type (Bio-Methanol, Bio-Ethanol, Bio-Butanol, Bio-BDO, and More), Feedstock (Starch-Based Crops, Sugar-Based Crops, Lignocellulosic Biomass, and More), Application (Transportation, Construction, Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Liters).

Geography Analysis

North America's 39.44% 2024 share mirrors its dense corn-to-ethanol corridor, ample rail logistics, and the Renewable Fuel Standard that keeps baseline volumes. Canada's 2025 Clean Fuel Regulation widens demand for low-carbon blends beyond the United States. Mexico's new mill investments knit the continent into a self-reinforcing supply chain. Summit Next Gen's USD 1.6 billion Texas ethanol-to-SAF complex, eligible for JETI subsidies, underlines how local grants align with federal tax credits to lure mega-projects.

Asia-Pacific is the growth engine, tracking a 9.55% CAGR on the back of India's fast-tracked 30% blend agenda and record rice-feedstock pull. China adds momentum by funding CO2-to-alcohol pilots that dovetail with its 2060 neutrality plan, while Japan and South Korea channel green-fuel incentives at refineries and airports. ASEAN markets, including the Philippines, are lifting blending rules too, keeping regional demand broad-based. This policy updraft attracts joint ventures that stitch together local feedstock with imported technology, accelerating capacity rollout.

Europe moves with stringent carbon-pricing and SAF mandates that jump-start premium niches. The ReFuelEU rulebook gives investors clarity on future SAF ramp-ups, while Germany and the UK run national subsidies to ensure domestic production. Feedstock flexibility, including sugar beet and waste biomass, helps buffer supply shocks. South America continues leveraging cheap sugarcane and advanced second-generation mills that process bagasse, supporting steady export flows to deficit regions. The Middle East and Africa, though smaller, are piloting projects as part of diversification strategies.

- Abengoa

- ADM

- BASF SE

- BP p.l.c.

- Cargill Incorporated

- CropEnergies AG

- Gevo

- Green Plains Inc.

- INEOS

- Mascoma LLC

- POET LLC

- Raizen

- SEKISUI CHEMICAL CO., LTD.

- Valero Energy Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandated ethanol-blend targets

- 4.2.2 Rapid airline SAF certification of Alcohol-to-Jet pathways

- 4.2.3 Integration of CO2 to alcohol CCU plants at refineries

- 4.2.4 Bio-alcohol use as low-carbon chemical feedstock in CPG

- 4.2.5 Emerging methanol-powered shipping corridors

- 4.3 Market Restraints

- 4.3.1 Feedstock price volatility

- 4.3.2 Insufficient pipeline compatibility for high-blend alcohols

- 4.3.3 Stagnant global light-vehicle production post-2027

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Bio-Methanol

- 5.1.2 Bio-Ethanol

- 5.1.3 Bio-Butanol

- 5.1.4 Bio-BDO

- 5.1.5 Other Bio-Alcohols

- 5.2 By Feedstock

- 5.2.1 Starch-based Crops

- 5.2.2 Sugar-based Crops

- 5.2.3 Lignocellulosic Biomass

- 5.2.4 Algal Biomass

- 5.2.5 Industrial Off-gases and MSW

- 5.3 By Application

- 5.3.1 Transportation

- 5.3.2 Construction

- 5.3.3 Electronics

- 5.3.4 Pharmaceuticals

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abengoa

- 6.4.2 ADM

- 6.4.3 BASF SE

- 6.4.4 BP p.l.c.

- 6.4.5 Cargill Incorporated

- 6.4.6 CropEnergies AG

- 6.4.7 Gevo

- 6.4.8 Green Plains Inc.

- 6.4.9 INEOS

- 6.4.10 Mascoma LLC

- 6.4.11 POET LLC

- 6.4.12 Raizen

- 6.4.13 SEKISUI CHEMICAL CO., LTD.

- 6.4.14 Valero Energy Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

生物醇市场:依产品类型、原料、技术、应用和最终用途产业划分-2026-2032年全球市场预测

生物醇市场:依产品类型、原料、技术、应用和最终用途产业划分-2026-2032年全球市场预测 2025-2033 年生物酒精市场报告(按产品类型、原料、应用和地区)

2025-2033 年生物酒精市场报告(按产品类型、原料、应用和地区) 生物酒精市场 - 成长、未来展望、竞争分析,2025-2033 年

生物酒精市场 - 成长、未来展望、竞争分析,2025-2033 年