|

市场调查报告书

商品编码

1844676

高性能纤维:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)High-Performance Fibers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

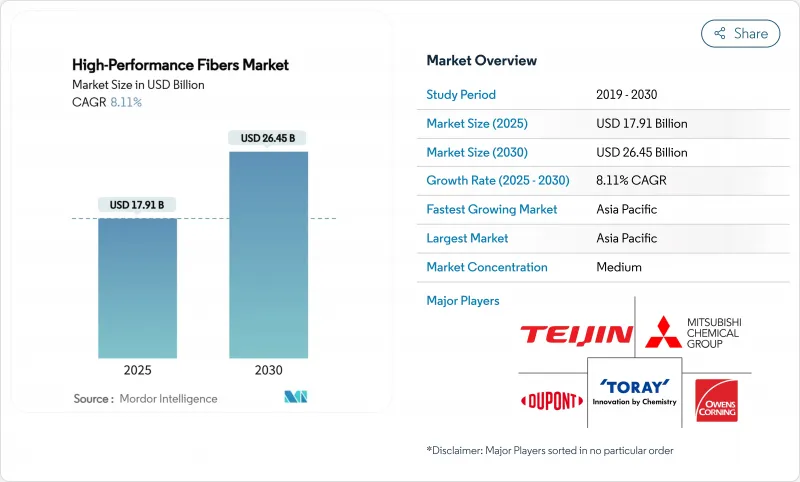

高性能纤维市场规模预计在 2025 年达到 179.1 亿美元,预计到 2030 年将达到 264.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.11%。

碳纤维、酰胺纤维、玻璃纤维和特殊纤维的使用正在加速,它们正从利基航太应用转向可再生能源硬体、零排放汽车和数据丰富的通讯网路的主流应用。如今,超过100公尺长的商用风力发电机叶片、IV型氢气压力容器和5G光纤电缆都需要具有卓越强度重量比和热稳定性的材料。中国积极的产能扩张正在给平均售价带来压力,但不断增长的销售量和新兴应用继续推动收益。政策制定者的脱碳指令,加上北美和欧洲的供应链在地化倡议,进一步支持了长期成长。

全球高性能纤维市场趋势与洞察

轻型离岸风电叶片需求激增

如今,长度超过100公尺的涡轮叶片使用的碳纤维数量远超以往型号,自动化纤维铺放技术也降低了製造成本,使风电成为一些製造商最大的单一销售量,甚至超过了航太。碳玻复合材料正被用来平衡刚性、耐腐蚀性和抗雷击性。随着北海和东海产能的快速扩张,中国和欧洲的叶片製造商正透过确保纤维生产线获得成本优势。

航太和国防工业的需求很高

战斗机队、无人机系统和航太运载火箭的现代化持续推动国防预算对超高模量碳纤维和陶瓷纤维的投资。在商用航空领域,复合材料宽体平台的订单正在反弹,「更电动化」的飞机架构引入了电磁屏蔽要求,这有利于碳纤维-芳香聚酰胺混合积层法。

挥发性聚丙烯腈 (PAN) - 前驱物供应链

到2024年,聚丙烯腈的价格波动可能达到30-40%,这将挤压缺乏后后向整合的独立纺纱厂的净利率。东丽和控制原丝产能的中国本土主要企业已保护自己免受价格上涨的影响,一些欧美製造商已推迟扩张计划,直至原材料供应更加稳定。美国的先导计画预计将实现原料多元化,但商业化生产仍需数年时间。

細項分析

到 2024 年,碳纤维将占据高性能纤维市场份额的 43.18%,预计到 2030 年的复合年增长率将达到 9.08%。中復神鹰等亚洲製造商正在江苏省增加新产能,年产能为 3 万吨,价值 8.66 亿美元,以进军成本敏感的工业领域。帝人在荷兰的工业规模回收工厂将芳香聚酰胺纱重新加工成新纤维,减少生命週期排放。玻璃纤维仍然是建筑和标准汽车面板的低成本支柱,而聚苯硫(PPS) 则因电动车电池组所需的耐热和耐化学性而经历两位数增长。超高分子量聚乙烯和陶瓷纤维分别在低温储存和高超音速平台中发挥特殊作用。

工业碳成本的快速下降正在重塑筹资策略。汽车製造商正在签署多年期合约以确保供应,风电原始设备製造商正在谈判代加工协议,以价格上限换取产量承诺。材料製造商正在将碳丝束与低黏度环氧树脂结合,以满足高产量叶片的生产目标。同时,高性能纤维市场对木质素衍生碳的风险投资正在增加,以减轻对PAN的依赖并提高环保资格。虽然尚未商业化,但试验生产线正在生产模量值超过35 Msi的纤维,适用于体育用品层压板,这预示着十年内现有供应链的颠覆潜力。

区域分析

受中国可再生能源应用和积极的汽车电气化计画的推动,到2024年,亚太地区将以40.25%的市场份额占据高性能纤维市场份额的主导地位。中国政府的五年规划支持离岸风力发电每年增加100吉瓦以上,使大直径叶片的纤维用量增加一倍。国内製造商打破了西方国家对T1000级碳纤维的垄断,使国内原始设备製造商能够满足先进战斗机的国防和航太规格要求。日本的东丽和帝人继续在高端市场占据主导地位,而韩国则为电池外壳和电子电路基板提供聚苯硫醚(PPS)和玻璃纤维。

受通膨控制法和「购买美国货」政策的推动,北美正在优先发展国内碳纤维生产。预计到2027年,华盛顿州、阿拉巴马州和魁北克省的新生产线每年将新增1.5万吨以上产能,从而减少对亚洲前驱体的依赖,并满足战斗机计画和航太发射器的国家安全目标。墨西哥不断增长的电动车组装能正在吸引边境以南的芳香聚酰胺和玻璃纤维进口,从而鼓励区域加工商在最终组装中心附近落户。

欧洲市场不断发展,强调永续性和循环经济原则,法律规范越来越倾向于生物基和可回收纤维解决方案,而非传统材料。该地区的风电产业是碳纤维需求的主要驱动力,而汽车应用则专注于支援排放目标的轻量化解决方案。德国汽车製造商正在检验易于重熔的热塑性碳纤维结构,北欧能源开发商正在海上原型机中测试生物基环氧树脂基质。该地区的成长速度落后于亚洲,但严格的品质和环境标准意味着更高的平均售价。南美和中东地区新兴的需求与基础设施和可再生能源计划相关,但受到外汇波动和技术短缺的限制,仍然充满机会。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 轻型离岸风电叶片需求激增

- 航太和国防工业的需求很高

- 4级氢气压力容器的商业化部署

- 5G光纤电缆将采用芳香聚酰胺纱

- 运动和防护产品需求旺盛

- 市场限制

- 挥发性聚丙烯腈 (PAN) 前驱物供应链

- 多材料复合材料的回收基础设施有限

- 中国产能过剩导致价格压缩

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 按类型

- 碳纤维

- 复合材料

- 碳纤维增强聚合物(CFRP)

- 增强碳(RCC)

- 纺织产品

- 微电极

- 催化剂

- 酰胺纤维

- 间芳香聚酰胺

- 对芳香聚酰胺

- 玻璃纤维

- 聚苯硫(PPS)

- 其他类型(超高分子量聚乙烯(UHMWPE)、聚苯并咪唑(PBI)、聚对苯基-2,6-苯并双噁唑(PBO)、碳化硅(SiC)、玄武岩)

- 碳纤维

- 按最终用户产业

- 航太/国防

- 车

- 体育用品

- 替代能源

- 电子和通讯

- 建筑和基础设施

- 其他终端使用者产业(医疗保健、医疗设备等)

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- Avient Corporation

- Bally Ribbon Mills

- China Jushi Co., Ltd.

- DuPont

- Hexcel Corporation

- Honeywell International Inc.

- Huvis Corp

- Kolon Industries, Inc.

- Kureha Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Owens Corning

- PBI Performance Products, Inc.

- Sarla Performance Fibers Limited

- Solvay

- Teijin Limited

- Toray Industries Inc.

- Toyobo Co., Ltd.

- TOYOBO MC Corporation

- Weihai Guangwei Group Co., Ltd.

- WL Gore & Associates

- Yantai Tayho Advanced Materials Co., Ltd.

第七章 市场机会与未来展望

The High-Performance Fibers Market size is estimated at USD 17.91 billion in 2025, and is expected to reach USD 26.45 billion by 2030, at a CAGR of 8.11% during the forecast period (2025-2030).

Uptake is accelerating as carbon, aramid, glass, and specialty fibers move from niche aerospace uses to mainstream roles in renewable-energy hardware, zero-emission vehicles, and data-rich telecom networks. Commercial wind-turbine blades that now exceed 100 m lengths, Type-IV hydrogen pressure vessels, and 5G fiber-optic cabling all require materials with exceptional strength-to-weight ratios and thermal stability. Aggressive capacity additions in China have pressured average selling prices, yet rising volumes and new applications continue to lift revenue. Policymakers' decarbonization mandates, combined with supply-chain localization initiatives in North America and Europe, further anchor long-term growth.

Global High-Performance Fibers Market Trends and Insights

Surging Demand for Lightweight Offshore-Wind Blades

Turbine blades topping 100 m now consume far greater volumes of carbon fiber than earlier models, and automated fiber placement is lowering production costs, allowing wind to surpass aerospace as the single largest volume outlet for some manufacturers. Hybrids that combine carbon and glass are being adopted to balance stiffness, corrosion resistance, and lightning-strike protection. Chinese and European blade makers with captive fiber lines gain cost advantages during rapid capacity build-outs in the North Sea and East China Sea.

High Demand from Aerospace and Defense Industry

Modernization of fighter fleets, uncrewed aerial systems, and space-launch vehicles keeps defense budgets invested in ultra-high-modulus carbon and ceramic fibers. Commercial aviation recovery has renewed orders for composite-rich wide-body platforms, while "more-electric" aircraft architectures introduce electromagnetic-shielding requirements that favor hybrid carbon-aramid lay-ups.

Volatile Polyacrylonitrile (PAN)-Precursor Supply Chain

Polyacrylonitrile price swings of 30-40% in 2024 curtailed margins for independent spinners lacking backward integration. Toray and domestic Chinese majors that control precursor capacity insulated themselves from spikes, while several Western producers postponed expansion plans pending more stable feedstock visibility. Bio-based acrylonitrile pilot projects in the United States could diversify inputs, yet commercial output remains years away.

Other drivers and restraints analyzed in the detailed report include:

- Commercial Rollout of Type-IV Hydrogen Pressure Vessels

- 5G Fiber-Optic Cabling Shift to Aramid Yarn

- Limited Recycling Infrastructure for Multi-Material Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbon fiber captured 43.18% of the high-performance fibers market share in 2024 and is forecast to climb at a 9.08% CAGR to 2030, underpinned by automotive lightweighting mandates and renewable-energy infrastructure roll-outs. Asia-based producers such as Zhongfu Shenying are injecting fresh capacity-USD 866 million for 30,000 t/y in Jiangsu-to penetrate cost-sensitive industrial segments. Aramid continues to dominate ballistic and telecom applications; Teijin's industrial-scale recycling plant in the Netherlands now reprocesses aramid yarn into new fiber, lowering lifecycle emissions. Glass fiber remains the low-cost mainstay for construction and standard automotive panels, while polyphenylene sulfide (PPS) enjoys double-digit growth as electric-vehicle battery packs require thermal and chemical resilience. UHMWPE and ceramic fibers fill niche roles in cryogenic storage and hypersonic platforms, respectively.

Rapid cost erosion across industrial-grade carbon is reshaping procurement strategies. Automakers are locking multiyear contracts to assure supply, while wind OEMs negotiate tolling arrangements that exchange volume commitments for price ceilings. Material formulators are coupling carbon tow with low-viscosity epoxy resins to meet high-throughput blade production targets. Concurrently, the high-performance fibers market is witnessing growing venture investment in lignin-derived carbon to ease PAN dependence and improve environmental credentials. Although still pre-commercial, pilot lines have produced 35+ Msi modulus fibers suitable for sporting-goods laminates, signaling potential to disrupt incumbent supply chains later in the decade.

The Global High Performance Fibers Market is Segmented by Type (Carbon Fiber, Aramid Fiber, Glass Fiber, Polyphenylene Sulfide (PPS), and More), End-User Industry (Aerospace and Defense, Automotive, Sporting Goods, Alternative Energy, Electronics & Telecommunications, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific dominates with 40.25% of the high-performance fibers market share in 2024, propelled by China's renewable-energy deployment and aggressive vehicle-electrification timelines. Beijing's Five-Year Plan backs >100 GW/year of offshore-wind additions, doubling fiber usage in large-diameter blades. Domestic producers have broken Western monopoly on T1000-class carbon, enabling local OEMs to meet defense and aerospace specifications for advanced fighter jets. Japan's Toray and Teijin continue to command premium niches, while South Korea channels PPS and glass fiber into battery housings and electronic substrates.

North America, supported by the Inflation Reduction Act and Buy-American policies, is prioritizing domestic carbon-fiber output. New lines in Washington State, Alabama, and Quebec will add >15,000 t/y by 2027, mitigating reliance on Asian precursors and aligning with national-security objectives for fighter programs and space launchers. Mexico's growing EV assembly capacity is pulling aramid and glass imports south of the border, prompting regional converters to co-locate near final assembly hubs.

Europe's market evolution emphasizes sustainability and circular economy principles, with regulatory frameworks that increasingly favor bio-based and recyclable fiber solutions over conventional materials. The region's wind energy sector drives significant carbon fiber demand, while automotive applications focus on lightweight solutions that support emission reduction targets . German automakers validate thermoplastic carbon architectures that allow easier re-melt, while Nordic energy developers test bio-based epoxy matrices in offshore prototypes. Regional growth lags Asia's pace yet commands higher average selling prices due to stringent quality and environmental standards. Emerging demand in South America and the Middle East remains opportunistic, tied to infrastructure and renewable-energy megaprojects but tempered by currency volatility and skills shortages.

- Avient Corporation

- Bally Ribbon Mills

- China Jushi Co., Ltd.

- DuPont

- Hexcel Corporation

- Honeywell International Inc.

- Huvis Corp

- Kolon Industries, Inc.

- Kureha Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Owens Corning

- PBI Performance Products, Inc.

- Sarla Performance Fibers Limited

- Solvay

- Teijin Limited

- Toray Industries Inc.

- Toyobo Co., Ltd.

- TOYOBO MC Corporation

- Weihai Guangwei Group Co., Ltd.

- W. L. Gore & Associates

- Yantai Tayho Advanced Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Lightweight Offshore-Wind Blades

- 4.2.2 High Demand from Aerodpace and Defense Industry

- 4.2.3 Commercial Rollout of Type-IV Hydrogen Pressure Vessels

- 4.2.4 5G fiber-optic Cabling Shift to Aramid Yarn

- 4.2.5 High Demand for Sporting and Protective Products

- 4.3 Market Restraints

- 4.3.1 Volatile Polyacrylonitrile (PAN)-Precursor Supply Chain

- 4.3.2 Limited Recycling Infrastructure for Multi-Material Composites

- 4.3.3 Chinese Over-Capacity Driving Price Compression

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Carbon Fiber

- 5.1.1.1 Composite Materials

- 5.1.1.1.1 Carbon Fiber Reinforced Polymer (CFRP)

- 5.1.1.1.2 Reinforced Carbon Carbon (RCC)

- 5.1.1.2 Textiles

- 5.1.1.3 Microelectrodes

- 5.1.1.4 Catalysis

- 5.1.2 Aramid Fiber

- 5.1.2.1 Meta-Aramid

- 5.1.2.2 Para-Aramid

- 5.1.3 Glass Fiber

- 5.1.4 Polyphenylene Sulfide (PPS)

- 5.1.5 Other Types (Ultra-High Molecular Weight Polyethylene (UHMWPE), Polybenzimidazole (PBI), Poly(p-phenylene-2,6-benzobisoxazole)(PBO), Silicon Carbide (SiC), Basalt)

- 5.1.1 Carbon Fiber

- 5.2 By End-user Industry

- 5.2.1 Aerospace & Defense

- 5.2.2 Automotive

- 5.2.3 Sporting Goods

- 5.2.4 Alternative Energy

- 5.2.5 Electronics & Telecommunications

- 5.2.6 Construction & Infrastructure

- 5.2.7 Other End User Industries (Healthcare & Medical Devices, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Avient Corporation

- 6.4.2 Bally Ribbon Mills

- 6.4.3 China Jushi Co., Ltd.

- 6.4.4 DuPont

- 6.4.5 Hexcel Corporation

- 6.4.6 Honeywell International Inc.

- 6.4.7 Huvis Corp

- 6.4.8 Kolon Industries, Inc.

- 6.4.9 Kureha Corporation

- 6.4.10 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.11 Owens Corning

- 6.4.12 PBI Performance Products, Inc.

- 6.4.13 Sarla Performance Fibers Limited

- 6.4.14 Solvay

- 6.4.15 Teijin Limited

- 6.4.16 Toray Industries Inc.

- 6.4.17 Toyobo Co., Ltd.

- 6.4.18 TOYOBO MC Corporation

- 6.4.19 Weihai Guangwei Group Co., Ltd.

- 6.4.20 W. L. Gore & Associates

- 6.4.21 Yantai Tayho Advanced Materials Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Emerging of Nanofibers and Ceramic Fibers

全球变色纺织品市场按技术、材料、产品类型、应用、分销管道和最终用途分類的预测(2026-2032年)高性能塑胶光纤市场:按类型、应用、最终用户和分销管道划分,全球预测(2026-2032年)

全球变色纺织品市场按技术、材料、产品类型、应用、分销管道和最终用途分類的预测(2026-2032年)高性能塑胶光纤市场:按类型、应用、最终用户和分销管道划分,全球预测(2026-2032年) 按材料类型、应用、最终用途产业、地理区域和预测分類的全球高性能纤维市场规模

按材料类型、应用、最终用途产业、地理区域和预测分類的全球高性能纤维市场规模 高性能织物滤袋市场报告:趋势、预测和竞争分析(至 2031 年)

高性能织物滤袋市场报告:趋势、预测和竞争分析(至 2031 年) 高性能纤维市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区、竞争细分,2020-2030 年

高性能纤维市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区、竞争细分,2020-2030 年 全球高性能纤维市场,2025-2029

全球高性能纤维市场,2025-2029 到 2030 年高性能纤维的市场预测:按类型、应用、最终用户和地区进行的全球分析全球高性能纤维市场 - 全球产业分析、规模、占有率、成长、趋势、预测(2031)- 依产品、依应用、依地区

到 2030 年高性能纤维的市场预测:按类型、应用、最终用户和地区进行的全球分析全球高性能纤维市场 - 全球产业分析、规模、占有率、成长、趋势、预测(2031)- 依产品、依应用、依地区 高性能纺织品市场:依地区:全球产业分析、规模、占有率、成长、趋势,2024-2032年预测

高性能纺织品市场:依地区:全球产业分析、规模、占有率、成长、趋势,2024-2032年预测