|

市场调查报告书

商品编码

1844712

硅油:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Silicone Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

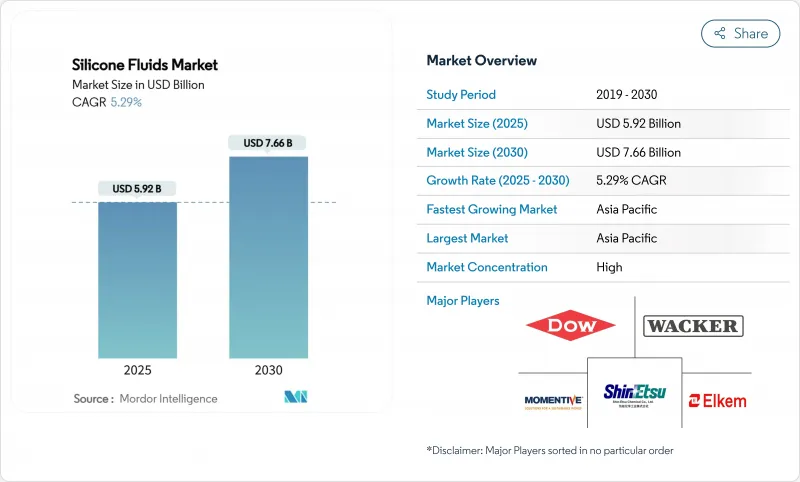

预计 2025 年硅油市场规模为 59.2 亿美元,到 2030 年将达到 76.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.29%。

随着原始设备製造商 (OEM) 和改性商寻求能够在极端温度下保持稳定、抗氧化并绝缘电子设备的流体——这些性能是传统矿物和合成碳氢化合物无法比拟的——对这些高性能聚合物的需求日益增长。电动车的加速发展、超大规模资料中心的兴起以及推动製造商转向更安全、更永续化学的监管趋势,进一步推动了硅油市场的成长。儘管原材料波动和更严格的环保标准抑制了成长势头,但硅油市场仍将继续受益于垂直整合努力、回收投资以及利基应用的技术创新。预计未来五年,硅油市场将以中等个位数的速度稳定成长。

全球硅油市场趋势与洞察

个人护理和化妆品的需求不断增长

配方师正竞相用兼具感官吸引力和可持续性的新一代材料取代限制性环状有机硅。 Siltech 的生物基烷基聚二甲基Dimethicone提高了延展性,同时减少了对原始化石原料的永续性。 CHT 集团的 BeauSil RE-AMO 919 EM 采用超过 94% 的再生单体配製而成,且不牺牲润肤剂的含量,从而实现了循环经济目标。亚太地区不断增长的中等收入人群正在青睐高端多功能护肤和护髮产品,这刺激了对能够在单一配方中提供调理、阻隔和光泽功效的硅油的需求。随着各大品牌不断强化其产品系列,多功能性已成为关键的差异化因素,能够证明减少碳足迹的供应商正获得青睐。

电动汽车温度控管液的应用日益广泛

液冷电池组需要能够高效传热并限制热失控的介电流体。路博润的Lifetime Fill硅酮冷却液反映了这一转变,能够在电动车电池组的整个使用寿命中保持稳定的状态。中国即将推出的GB 29743.2电导率基准值设定了高标准,传统的乙二醇-水混合物无法满足这一标准,这促使汽车製造商转向硅基配方。不仅电池,宽能带隙逆变器、电动马达和充电系统也受益于硅油的宽动作温度范围。上游方面,受电动车成长推动的硅金属需求预计将在2030年之前以每年4.56%的速度成长,这将使拥有稳定原材料供应的垂直整合製造商受益。

金属硅及单体价格不稳定

中国控制着全球约四分之三的硅金属产量,这为硅油市场带来了连锁风险。能源价格上涨、产量限制以及地缘政治摩擦导致现货价格波动,并扰乱了下游硅料生产商的预算规划。儘管美国根据《通膨削减法案》为国内冶炼计划提供奖励,但新产能要到2030年才能全面运作。同时,生产商正在透过签订长期供应合约进行对冲,并评估后向整合。

細項分析

改质等级的扩张速度快于未改性等级,复合年增长率为 6.84%。这得归功于配方师指定具有独特侧链、反应位点或交联基团的硅氧烷。这些客製化分子可选择性地与基材键结、增强附着力或形成疏水錶面,使最终用户无需过度设计即可实现性能目标。电动车灌封胶、三防胶和高柔韧性纺织油墨的需求尤其强劲。然而,纯聚二甲基硅氧烷凭藉其成本效益和满足各种规格的能力,仍占据销售领先地位。供应链日趋成熟,持续的製程瓶颈消除将进一步降低单位成本。

永续生产的竞争日益激烈。陶氏公司和Circusil的合资企业将创造一个回收循环,可将PDMS的碳足迹减少50%以上。瓦克将于2025年5月在中国运作一条新的流体和乳液生产线,为下一代电子产品增加高纯度生产能力。 KCC将于2024年收购迈图,将业务范围从上游硅氧烷单体扩展到下游特种流体。随着循环经济目标的不断推进,拥有闭合迴路能力的製造商将优先获得渴望获得范围3减排认证的全球原始设备製造商的供应奖励。

硅油市场报告按产品类型(直链硅油、改性硅油)、应用(润滑剂和油脂、减震材料、液体电介质、液压油、消泡剂、个人护理、油漆和涂料添加剂、纺织品、药品和其他应用)和地区(亚太地区、北美、欧洲、南美和中东和非洲)细分。

区域分析

亚太地区主导硅油市场,其供应链从金属硅冶炼开始,一直延伸到最终产品。中国凭藉着成本优势和75%的原料控制能力,在该地区占据领先地位;而日本和韩国则在微型电子和储存半导体领域处于领先地位,这些领域需要超高纯度的介电流体。东南亚正在成为製造业的避险天堂,越南和泰国正在吸引外国对特种化学品综合体的直接投资。在印度国内汽车製造和个人保健部门扩张的推动下,印度的本土销售额实现了两位数成长。

北美的表现有所不同。美国引领关键矿产的陆上供应链,而资料中心和电动车的建设正在推动特种流体的需求。陶氏公司正在扩大在硅橡胶能,以支持寻求快速交付的区域客户。埃克森美孚正在德克萨斯增加高黏度合成基料能,这表明优质功能性流体在工业领域的广泛接受度。加拿大供应以水基为基础的冶金级有机硅,而墨西哥的加工出口走廊正在吸引用于电子组装和汽车线束製造的流体。

欧洲仍然是创新中心,儘管它面临最严峻的监管障碍。瓦克预测,到2025年,由于特种级有机硅的销售量将抵销通用级有机硅销量的下滑,其收益将成长10%。德国工程公司指定使用用于工具机的有机硅减震材料,而法国化妆品製造商则率先采用升级再造的有机硅成分,以满足即将出台的包装和碳足迹法规。北欧公用事业公司的绿色能源矩阵增强了循环製造概念的可信度,有助于硅油製造商在推销其技术性能的同时,也兼顾环境价值。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 个人护理和化妆品的需求不断增长

- 电动汽车温度控管液的应用日益广泛

- 工业自动化高性能润滑剂的成长

- 超大规模资料中心的浸入式冷却

- 用于生物刺激素混合物的精密农业消泡剂

- 市场限制

- 金属硅及单体价格波动

- 严重的VOC和REACH合规成本

- 原料硅氧烷供应商集中度高

- 价值链分析

- 五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 依产品类型

- 直链硅油

- 聚二甲基硅油

- 甲基苯基硅油

- 甲基含氢硅油

- 其他直硅胶

- 改质硅油

- 反应性硅油

- 非反应性硅油

- 直链硅油

- 按用途

- 润滑油和润滑脂

- 阻尼介质

- 液体电介质

- 油压

- 消泡剂

- 个人护理

- 油漆和涂料添加剂

- 纺织品整理加工剂

- 製药

- 其他用途

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- BRB International BV

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- GELEST Inc.

- Innospec Inc.

- IOTA silicone

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- Wacker Chemie AG

- Zhejiang Zhongtian Fluorine Silicon Material Co., Ltd.

第七章 市场机会与未来展望

The Silicone Fluids Market size is estimated at USD 5.92 billion in 2025, and is expected to reach USD 7.66 billion by 2030, at a CAGR of 5.29% during the forecast period (2025-2030).

Demand for these high-performance polymers is climbing as OEMs and formulators look for fluids that stay stable under extreme temperatures, resist oxidation, and insulate electronics-capabilities that conventional mineral or synthetic hydrocarbons cannot match. Growth is further reinforced by the accelerating shift to electric mobility, the rise of hyperscale data centers, and regulatory moves that push manufacturers toward safer, more sustainable chemistries. Although raw-material volatility and tightening environmental standards temper momentum, the silicone fluids market continues to benefit from vertical integration initiatives, recycling investments, and niche-application innovation. Collectively, these forces position the silicone fluids market for steady mid-single-digit expansion over the next five years.

Global Silicone Fluids Market Trends and Insights

Rising Demand from Personal Care and Cosmetics

Formulators are moving quickly to replace restricted cyclic silicones with next-generation materials that marry sensory appeal and sustainability. Bio-based alkyl dimethicones from Siltech improve spreadability while cutting reliance on virgin fossil feedstocks. CHT Group's BeauSil RE-AMO 919 EM incorporates over 94% recycled monomers to meet circular-economy targets without sacrificing emolliency. Expanding middle-class populations in Asia-Pacific are embracing premium multifunctional skin- and hair-care products, spurring demand for silicone fluids that deliver conditioning, barrier, and gloss benefits in a single blend. As brands tighten product portfolios, multifunctionality becomes a critical differentiator, and suppliers able to document lower carbon footprints gain preferred-supplier status.

Increasing Adoption in Electric Vehicle Thermal-Management Fluids

Liquid-cooled battery packs need dielectric fluids that suppress thermal runaway yet transfer heat efficiently. Lubrizol's lifetime-fill silicone coolant exemplifies this shift by remaining stable for the full service life of an EV battery pack. China's forthcoming GB 29743.2 conductivity threshold sets a high bar that conventional glycol-water blends cannot meet, steering automakers toward silicone-based formulations. Beyond batteries, wide-bandgap inverters, e-motors, and charging systems also benefit from the broad operating-temperature band of silicone fluids. Upstream, silicon metal demand tied to EV growth is rising 4.56% annually through 2030, rewarding vertically integrated producers that can secure raw supply.

Volatile Silicon Metal and Monomer Prices

China controls roughly three-quarters of the world's silicon metal output, creating a single-country risk that cascades through the silicone fluids market. Energy-price spikes, production curbs, and geopolitical frictions swing spot quotes, disrupting budgeting for downstream formulators. The United States is incentivizing domestic smelter projects under the Inflation Reduction Act, yet new capacity will not meaningfully come onstream before 2030. In the meantime, producers hedge with long-term supply contracts and evaluate backward integration, actions that demand capital many mid-sized players cannot muster.

Other drivers and restraints analyzed in the detailed report include:

- Growth in High-Performance Lubricants for Industrial Automation

- Liquid-Immersion Cooling of Hyperscale Data Centres

- Stringent VOC and REACH Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modified grades are expanding faster than unmodified counterparts, charting a 6.84% CAGR as formulators specify siloxanes with tailored side-chains, reactive sites, or crosslinkable groups. These custom molecules bond selectively to substrates, boost adhesion, or create hydrophobic surfaces, letting end-users hit performance targets without over-engineering. Demand is prominent in EV potting, conformal coatings, and high-flex textile inks. Straight polydimethyl-silicone grades nevertheless maintain volume leadership due to cost efficiency and broad spec inclusion. Their supply chains are mature, and continuous-process debottlenecking further reduces unit cost.

Competition is intensifying around sustainable production. Dow's joint venture with Circusil brings a recycling loop able to cut PDMS carbon footprint by more than 50%. Wacker commissioned new Chinese fluid and emulsion lines in May 2025, adding high-purity capacity aimed at next-gen electronics. KCC's 2024 purchase of Momentive broadens vertical reach from upstream siloxane monomers to downstream specialty fluids. As circular-economy targets harden, producers with closed-loop capabilities gain supply-award preference from global OEMs keen to certify Scope 3 reductions.

The Silicone Fluids Market Report is Segmented by Product Type (Straight Silicone Fluid and Modified Silicone Fluid), Application (Lubricants and Greases, Damping Media, Liquid Dielectrics, Hydraulic Fluids, Defoamers, Personal Care, Paints and Coating Additives, Textile, Pharmaceuticals, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific dominates the silicone fluids market, leveraging integrated supply chains that begin with silicon metal smelting and culminate in finished formulations. China's cost advantage and 75% raw-material control anchor the region's leadership, while Japan and South Korea champion miniaturized electronics and memory semiconductors that require ultra-pure dielectric fluids. Southeast Asia is emerging as a manufacturing hedge, with Vietnam and Thailand courting foreign direct investment for specialty-chemical complexes. India, supported by domestic automotive build-out and an expanding personal-care sector, records double-digit local sales increases.

North America presents a different dynamic. The United States orchestrates supply-chain onshoring for critical minerals, while datacenter and EV build-outs propel specialty-fluid demand. Dow's capacity expansion for silicone elastomers in Michigan supports regional customers seeking short lead times. ExxonMobil added high-viscosity synthetic base-stock capacity in Texas, signaling wider industrial acceptance of premium functional fluids. Canada supplies hydro-based metallurgical-grade silicon, and Mexico's maquiladora corridor pulls in fluids for electronics assembly and automotive wiring harness production.

Europe contends with the strictest regulatory hurdles yet remains an innovation epicenter. Wacker forecasts 10% revenue growth in its Silicones division for 2025 as specialty grades offset lower commodity volumes. Germany's engineering companies specify silicone damping media for machine tools, while France's cosmetic houses pioneer upcycled silicone ingredients to meet imminent packaging and carbon-footprint rules. Nordic utilities' green-power matrices lend credibility to circular-manufacturing claims, helping silicone fluid makers sell environmental value alongside technical performance.

- BRB International B.V.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- GELEST Inc.

- Innospec Inc.

- IOTA silicone

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co., Ltd.

- Siltech Corporation

- Supreme Silicones India Pvt. Ltd.

- Wacker Chemie AG

- Zhejiang Zhongtian Fluorine Silicon Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from personal care and cosmetics

- 4.2.2 Increasing adoption in electric vehicle thermal-management fluids

- 4.2.3 Growth in high-performance lubricants for industrial automation

- 4.2.4 Liquid-immersion cooling of hyperscale data centres

- 4.2.5 Precision agriculture anti-foam agents for biostimulant mixtures

- 4.3 Market Restraints

- 4.3.1 Volatile silicon metal and monomer prices

- 4.3.2 Stringent VOC and REACH compliance costs

- 4.3.3 High supplier concentration in raw siloxanes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Straight Silicone Fluids

- 5.1.1.1 Poly-dimethyl Silicone Fluid

- 5.1.1.2 Methylphenyl Silicone Fluid

- 5.1.1.3 Methylhydrogen Silicone Fluid

- 5.1.1.4 Other Straight Silicone Fluids

- 5.1.2 Modified Silicone Fluids

- 5.1.2.1 Reactive Silicone Fluid

- 5.1.2.2 Non-reactive Silicone Fluid

- 5.1.1 Straight Silicone Fluids

- 5.2 By Application

- 5.2.1 Lubricants and Greases

- 5.2.2 Damping Media

- 5.2.3 Liquid Dielectrics

- 5.2.4 Hydraulic Fluids

- 5.2.5 Defoamers

- 5.2.6 Personal Care

- 5.2.7 Paints and Coating Additives

- 5.2.8 Textile Finishes

- 5.2.9 Pharmaceuticals

- 5.2.10 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BRB International B.V.

- 6.4.2 CHT Germany GmbH

- 6.4.3 Dow

- 6.4.4 DuPont

- 6.4.5 Elkem ASA

- 6.4.6 GELEST Inc.

- 6.4.7 Innospec Inc.

- 6.4.8 IOTA silicone

- 6.4.9 KCC SILICONE CORPORATION

- 6.4.10 Momentive

- 6.4.11 Shin-Etsu Chemical Co., Ltd.

- 6.4.12 Siltech Corporation

- 6.4.13 Supreme Silicones India Pvt. Ltd.

- 6.4.14 Wacker Chemie AG

- 6.4.15 Zhejiang Zhongtian Fluorine Silicon Material Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

硅油市场:2026-2032年全球市场预测(依产品类型、黏度、应用、终端用户产业及通路划分)

硅油市场:2026-2032年全球市场预测(依产品类型、黏度、应用、终端用户产业及通路划分) 全球硅油市场规模、份额、趋势和成长分析报告(2026-2034年)

全球硅油市场规模、份额、趋势和成长分析报告(2026-2034年) 硅油市场规模、份额、趋势及预测(按类型、应用、终端用户产业及地区划分),2026-2034年

硅油市场规模、份额、趋势及预测(按类型、应用、终端用户产业及地区划分),2026-2034年 硅油市场规模、份额及成长分析(依产品类型、应用、终端用户产业及地区划分)-2026-2033年产业预测

硅油市场规模、份额及成长分析(依产品类型、应用、终端用户产业及地区划分)-2026-2033年产业预测 甲基含氢硅胶全球市场报告:趋势、预测及竞争分析(至2031年)硅油市场,按类型、按功能、按应用、按最终用户、按国家和地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

甲基含氢硅胶全球市场报告:趋势、预测及竞争分析(至2031年)硅油市场,按类型、按功能、按应用、按最终用户、按国家和地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 全球硅胶市场按类型、最终用途行业和地区划分 - 预测至 2032 年2024 年至 2031 年硅油市场(按应用、最终用户和地区划分)

全球硅胶市场按类型、最终用途行业和地区划分 - 预测至 2032 年2024 年至 2031 年硅油市场(按应用、最终用户和地区划分) 硅胶市场规模、份额、趋势分析报告:按应用、最终用途、地区、细分市场预测,2024-2030

硅胶市场规模、份额、趋势分析报告:按应用、最终用途、地区、细分市场预测,2024-2030 全球硅油市场规模、份额和趋势分析:按应用、类型、最终用户和地区分類的展望和预测(2024-2031)

全球硅油市场规模、份额和趋势分析:按应用、类型、最终用户和地区分類的展望和预测(2024-2031)