|

市场调查报告书

商品编码

1844718

有机酸:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Organic Acids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

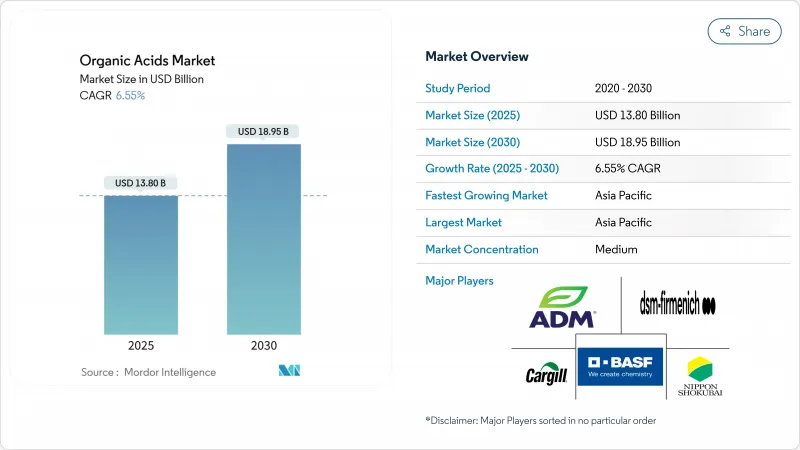

预计有机酸市场规模到 2025 年将达到 138 亿美元,到 2030 年将扩大到 189.5 亿美元,复合年增长率为 6.55%。

这种成长主要得益于从石化方法到生物发酵製程的重大转变,以及食品、聚合物和製药业对洁净标示产品的需求不断增加。

有机酸,包括乙酸、柠檬酸和乳酸,在食品保鲜、增味和pH值调节等各种应用中发挥至关重要的作用。环境问题和对永续替代品的需求正在推动向生物基生产方式的转变。此外,消费者对天然和清洁标籤产品的偏好日益增长,促使製造商在食品和饮料配方中加入有机酸。在聚合物和製药行业,有机酸因其功能特性而日益应用,例如用作化学合成的中间体并提升产品性能。预计有机酸在各个价值链中的应用将支持市场在预测期内的强劲成长。

全球有机酸市场趋势与洞察

乙酸作为太阳能 EVA 薄膜的醋酸乙烯单体的快速应用

太阳能光伏 (PV) 产业的快速发展显着增加了醋酸乙烯单体(VAM) 生产中对醋酸的需求。这项需求主要源自于 EVA封装膜,它对于提高太阳能板的耐用性和效率至关重要。如今,生产商可以利用大豆油的非催化分解,以可再生原料生产商业级 VAM。这种创新製程生产的醋酸是一种高价值产品,能够满足太阳能光电产业严格的品质要求。透过采用这种生物基生产路线,製造商可以履行永续性义务,同时实现供应链多元化,并减少对石化衍生 VAM 的依赖。此外,将生物基醋酸与可再生乙醇衍生乙烯结合,可以建立一条完全永续的VAM 生产路线。这项进步使有机酸製造商能够在快速扩张的太阳能市场中抓住溢价机会。

注射剂型对药用级乳酸的需求

药用级乳酸的需求是有机酸市场的主要驱动力,尤其是由于其在註射剂中的应用日益广泛。乳酸以其良好的生物相容性和生物降解性而闻名,在製药行业中被广泛用于增强药物传输系统。根据美国食品药物管理局(FDA) 的数据,在药物製剂中使用乳酸符合严格的安全性和有效性标准,使其成为注射剂的首选。此外,世界卫生组织 (WHO) 强调了此类生物相容性化合物在改善患者预后方面的重要性,尤其是在重症监护药物方面。此外,糖尿病和心血管疾病等慢性疾病的日益普及导致注射剂需求激增,进一步推动了对药用级乳酸的需求。根据美国疾病管制与预防中心 (CDC) 的数据,到 2023 年,美国成年人糖尿病的盛行率将达到 15.8%,这凸显了对有效药物输送系统日益增长的需求。预计这种成长将直接影响製药应用对乳酸的需求。

严格的VOC指令限製石油基丙烯酸和己二酸

针对石油基丙烯酸和己二酸的严格挥发性有机化合物 (VOC) 指令严重阻碍了有机酸市场的发展。这些指令旨在透过限制使用会导致 VOC排放的石化衍生物来减少环境污染并促进永续性。众所周知,VOC 对人类健康和环境都有不利影响,包括导致地面臭氧层的形成和空气品质恶化。因此,包括北美、欧洲和亚太地区在内的各个地区的监管机构正在实施严格的 VOC排放控制指南,这直接影响了石油基丙烯酸和己二酸的生产和使用。有机酸市场的製造商在遵守这些法规方面面临挑战,这可能导致生产成本增加,因为需要先进的技术和流程来满足合规标准。此外,这些法规鼓励业界探索和采用替代原料,例如生物基原料,这些原料更环保,但通常成本更高且扩充性较差。

細項分析

2024 年,乙酸在有机酸市场保持主导地位,占据 34.16% 的主导市场。这种主导地位归因于其在纺织、食品饮料和製药等各行业的广泛应用。乙酸在醋酸乙烯单体(VAM) 的生产中起着关键作用,而 VAM 是製造黏合剂、油漆和被覆剂的关键前驱物。乙酸也用于製造乙酸酐、对苯二甲酸和乙酸酯,进一步推动了需求。该化合物的多功能性和在终端用户行业的广泛需求继续推动其成长并巩固其作为市场领导的地位。预计新兴国家对工业应用的日益关注和对 VAM 需求的不断增长将在未来几年进一步推动乙酸的成长。

同时,琥珀酸已成为有机酸市场中成长最快的细分市场。预计在2025-2030年的预测期内,琥珀酸的复合年增长率将达到9.67%。这一增长主要源于其作为可生物降解聚合物基本成分的日益普及,这得益于日益增长的环保意识以及对永续材料的监管支持。琥珀酸也用于製造树脂、被覆剂和个人保健产品,进一步提升了其市场占有率。此外,生物基生产技术的进步使琥珀酸成为一种经济高效、可再生的石油基化学品替代品。

石化原料将主导有机酸市场,到2024年将占61.52%的显着份额。这些来源将继续在满足食品饮料、製药和化学品等各行各业对有机酸的高需求方面发挥关键作用。完善的石化生产基础设施和相对较低的生产成本使其占据了强大的市场地位。然而,对环境永续性的担忧和原油价格的波动可能会在未来几年对石化基有机酸的成长构成挑战。

同时,生物基有机酸预计在预测期内将以惊人的11.07%的复合年增长率成长。这一成长的驱动力在于消费者对永续环保产品的日益增长的偏好,以及鼓励使用可再生资源的严格环境法规。生物基有机酸源自玉米、甘蔗和其他生物质等可再生原料,使其成为石化原料的永续替代品。生物技术和发酵过程的进步进一步提高了生物基有机酸生产的效率和扩充性,使其成为市场的关键成长动力。

区域分析

2024 年,亚太地区将在全球有机酸市场中占据主导地位,占据最大的区域市场份额 30.42%,并以预计 9.41% 的复合年增长率成为增长最快的地区,到 2030 年。这种双重领导地位归功于该地区强大的製造业生态系统和不断壮大的中产阶级人口不断转变的消费模式。受都市化进程加速和消费者偏好变化的推动,食品、製药和工业应用对有机酸的需求尤其强劲。中国是该地区最大的有机酸生产国,但面临产能过剩和持续的贸易争端等挑战,这些挑战可能会影响市场动态。然而,在快速的经济发展、有利的政府政策和与全球永续性标准的接轨的支持下,印度和东南亚国家正在成为重要的成长贡献者。

由于生物基生产技术的进步以及优先考虑永续性和高品质标准的监管框架,北美在有机酸市场继续保持稳固地位。该地区正在大力投资发酵产能,以弥补现有的基础设施缺口并实现更有效率的生产流程。食品饮料、製药和农业等各行各业对生物基替代品的日益普及,进一步提振了北美对有机酸的需求。该地区对创新和永续性的关注,使其成为开发先进有机酸解决方案的领导者,服务于国内和国际市场。这些因素使北美在全球市场继续占据关键地位。

欧洲有机酸市场成熟,注重高端应用和严格的合规性。随着各行各业日益转向永续和环保的解决方案,该地区严格的环境标准为生物基製造商创造了机会。欧洲对有机酸的需求主要来自食品保鲜、製药和工业流程等领域的应用,这些领域对品质和永续性至关重要。同时,南美、中东和非洲代表着全球有机酸市场的新兴机会。这些地区经济发展迅速,农业资源丰富,为有机酸的生产和消费提供了坚实的基础。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 醋酸醋酸乙烯单体中醋酸的快速采用,用于太阳能EVA薄膜

- 注射药用乳酸的需求

- 柠檬酸类天然防腐剂在洁净标示饮品的兴起

- 琥珀酸作为 BioPBS 和 BioBDO 的基石的开发

- 饲料级甲酸和丙酸在无非洲猪瘟猪饲料中的应用

- 在饲料中用作抗生素的替代品

- 市场限制

- 严格的VOC指令限製石油基丙烯酸和己二酸

- 中国低纯度柠檬酸产能过剩及价格压缩

- 合成酸的环境问题阻碍了市场成长

- 阻碍市场成长的技术和基础设施障碍

- 供应链分析

- 监理展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场规模和成长预测(数量和金额)

- 按类型

- 醋酸

- 柠檬酸

- 乳酸

- 琥珀酸

- 苹果酸

- 丙酸

- 甲酸

- 富马酸和马来酸

- 其他(苯甲酸、葡萄糖酸、己二酸等)

- 按原料

- 生物基

- 石化

- 混合/副产品

- 按用途

- 饮食

- 动物饲料和营养

- 製药和医疗保健

- 个人护理和化妆品

- 工业化学品和中间体(VAM、PTA、丙烯酸酯等)

- 聚合物和生质塑胶(PLA、PBS、PHA)

- 其他(纺织品、润滑剂、电子产品)

- 按形式

- 液体

- 干/晶体/粉末

- 区域分析

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 其他北美地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲国家

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 其他亚太地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市场排名分析

- 公司简介

- BASF SE

- Cargill, Incorporated

- Archer Daniels Midland Company

- Royal DSM(Reverdia)

- Nippon Shokubai Co., Ltd.

- DSM-Firmenich AG

- Roquette Freres

- Celanese Corporation

- Corbion NV

- Thermo Fisher Scientific

- Bartek Ingredients Inc.

- Fuso Chemical Co., Ltd.

- Inner Mongolia

- Mitsubishi Chemical Group

- Fengchen Group Co.,Ltd

- RZBC GROUP CO., LTD

- TINNAKORN CHEMICAL & SUPPLY

- Shandong Feiyang Chemical

- Jinan Finer Chemical Co., Ltd

- Anhui BBCA Biochemical

第七章 市场机会与未来展望

The organic acids market size reached USD 13.80 billion in 2025 and is forecast to advance to USD 18.95 billion by 2030 at a 6.55% CAGR.This growth is largely driven by a notable transition from petrochemical methods to bio-based fermentation processes, alongside an increasing demand for clean-label products across food, polymer, and pharmaceutical sectors.

Organic acids, which include acetic acid, citric acid, lactic acid, and others, play a crucial role in various applications such as food preservation, flavor enhancement, and pH regulation. The shift toward bio-based production methods is gaining traction due to environmental concerns and the need for sustainable alternatives. Additionally, the rising consumer preference for natural and clean-label products is pushing manufacturers to adopt organic acids in food and beverage formulations. In the polymer and pharmaceutical industries, organic acids are increasingly used for their functional properties, such as acting as intermediates in chemical synthesis and enhancing product performance. This growing adoption across diverse value chains underscores the market's robust expansion during the forecast period.

Global Organic Acids Market Trends and Insights

Rapid Uptake of Acetic Acid in Vinyl-Acetate-Monomer for Solar-EVA Films

The rapid growth of the photovoltaic industry has significantly increased the demand for acetic acid in the production of vinyl acetate monomers (VAM). EVA encapsulant films, which are essential for improving the durability and efficiency of solar panels, drive this demand. Producers can now manufacture commercial-grade VAM from renewable feedstocks by utilizing the non-catalytic cracking of soybean oil. This innovative process generates acetic acid as a valuable co-product that complies with the stringent quality requirements of the solar industry. By adopting this bio-based production pathway, manufacturers address sustainability mandates while diversifying supply chains to reduce reliance on petrochemical-derived VAM. Additionally, integrating ethylene derived from renewable ethanol with bio-based acetic acid establishes a fully sustainable VAM production route. This advancement enables organic acid producers to capitalize on premium pricing opportunities in the rapidly expanding solar market.

Pharmaceutical-grade Lactic Acid Demand for Injectable Drug Formulations

The demand for pharmaceutical-grade lactic acid is a significant driver in the organic acids market, particularly due to its increasing application in injectable drug formulations. Lactic acid, known for its biocompatibility and biodegradability, is widely used in the pharmaceutical industry to enhance drug delivery systems. According to the U.S. Food and Drug Administration (FDA), the adoption of lactic acid in drug formulations aligns with stringent safety and efficacy standards, making it a preferred choice for injectable drugs . Additionally, the World Health Organization emphasizes the importance of such biocompatible compounds in improving patient outcomes, especially in critical care medications. Moreover, the increasing prevalence of chronic diseases such as diabetes and cardiovascular disorders has led to a surge in demand for injectable drugs, further driving the need for pharmaceutical-grade lactic acid. According to the Centers for Disease Control and Prevention (CDC), the prevalence of total diabetes was 15.8% in all adults in the United States in 2023, highlighting the growing need for effective drug delivery systems. This growth is expected to directly impact the demand for lactic acid in pharmaceutical applications.

Stringent VOC Directives Limiting Petro-based Acrylic and Adipic Acids

The organic acid market is experiencing significant restraint due to stringent Volatile Organic Compound (VOC) directives imposed on petro-based acrylic and adipic acids. These directives aim to reduce environmental pollution and promote sustainability by limiting the use of petrochemical derivatives that contribute to VOC emissions. VOCs are known to have adverse effects on both human health and the environment, including contributing to ground-level ozone formation and air quality degradation. As a result, regulatory bodies across various regions, including North America, Europe, and Asia-Pacific, have implemented strict guidelines to curb VOC emissions, directly impacting the production and usage of petro-based acrylic and adipic acids. Manufacturers in the organic acid market are facing challenges in complying with these regulations, which may lead to increased production costs due to the need for advanced technologies and processes to meet compliance standards. Additionally, the restrictions are driving the industry to explore and adopt alternative raw materials, such as bio-based feedstocks, which are more environmentally friendly but often come with higher costs and scalability issues.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Citric-acid-based Natural Preservatives in Clean-Label Beverages

- Growth of Succinic Acid as a Building Block for Bio-PBS and Bio-BDO

- Environmental Concerns with Synthetic Acids Hindering the Market Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, acetic acid holds a dominant 34.16% market share in the organic acids market, maintaining its leadership position. This dominance is attributed to its extensive applications across various industries, including textiles, food and beverages, and pharmaceuticals. Acetic acid plays a critical role in the production of vinyl acetate monomer (VAM), which is a key precursor for manufacturing adhesives, paints, and coatings. Additionally, its use in the production of acetic anhydride, terephthalic acid, and acetate esters further enhances its demand. The compound's versatility and widespread demand across end-user industries continue to drive its growth and solidify its position as a market leader. The increasing focus on industrial applications and the rising demand for VAM in emerging economies are expected to further bolster the growth of acetic acid in the coming years.

Succinic acid, on the other hand, is emerging as the fastest-growing segment in the organic acids market. It is projected to register a robust CAGR of 9.67% during the forecast period of 2025 to 2030. This growth is primarily fueled by its increasing adoption as a building block for biodegradable polymers, which are gaining traction due to rising environmental concerns and regulatory support for sustainable materials. Succinic acid is also used in the production of resins, coatings, and personal care products, further contributing to its expanding market presence. Moreover, advancements in bio-based production technologies have made succinic acid a cost-effective and renewable alternative to petroleum-based chemicals.

In 2024, petrochemical sources dominated the organic acids market, holding a significant 61.52% share. These sources continue to play a crucial role in meeting the high demand for organic acids across various industries, including food and beverages, pharmaceuticals, and chemicals. The established infrastructure for petrochemical production and the relatively lower production costs contribute to their strong market position. However, concerns regarding environmental sustainability and fluctuating crude oil prices may pose challenges to the growth of petrochemical-based organic acids in the coming years.

On the other hand, bio-based sources of organic acids are expected to grow at an impressive CAGR of 11.07% during the forecast period. This growth is driven by increasing consumer preference for sustainable and eco-friendly products, along with stringent environmental regulations encouraging the adoption of renewable resources. Bio-based organic acids are derived from renewable feedstocks such as corn, sugarcane, and other biomass, making them a more sustainable alternative to petrochemical sources. Advancements in biotechnology and fermentation processes are further enhancing the efficiency and scalability of bio-based organic acid production, positioning this segment as a key growth driver in the market.

The Organic Acids Market Report is Segmented by Type (Acetic Acid, Citric Acid, and More), Source (Bio-Based, Petro-Chemical, Hybrid/Co-product Streams), Application (Food and Beverages, Animal Feed and Nutrition, and More ), Form (Liquid, Dry/Crystal/Powder), and Geography (North America, South America, Europe, Middle East and Africa, Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

In 2024, Asia-Pacific dominated the global organic acids market, holding the largest regional market share of 30.42% and registering the fastest growth with a projected CAGR of 9.41% through 2030. This dual leadership stems from the region's robust manufacturing ecosystem and the rising consumption patterns of its expanding middle-class population. The demand for organic acids is particularly strong in food, pharmaceutical, and industrial applications, driven by increasing urbanization and changing consumer preferences. China, as a key producer in the region, faces challenges such as overcapacity and ongoing trade disputes, which could impact its market dynamics. However, India and Southeast Asian countries are emerging as significant growth contributors, supported by rapid economic development, favorable government policies, and alignment with global sustainability standards.

North America continues to maintain a strong foothold in the organic acids market, underpinned by its technological advancements in bio-based production and a regulatory framework that prioritizes sustainability and high-quality standards. The region has witnessed substantial investments in fermentation capacity, addressing previous infrastructure gaps and enabling more efficient production processes. The demand for organic acids in North America is further bolstered by the growing adoption of bio-based alternatives across various industries, including food and beverages, pharmaceuticals, and agriculture. The region's focus on innovation and sustainability has positioned it as a leader in the development of advanced organic acid solutions, catering to both domestic and international markets. These factors ensure North America's continued prominence in the global market landscape.

Europe, with its mature organic acids market, emphasizes premium applications and strict regulatory compliance. The region's stringent environmental standards create opportunities for bio-based producers, as industries increasingly shift towards sustainable and eco-friendly solutions.The demand for organic acids in Europe is driven by their applications in food preservation, pharmaceuticals, and industrial processes, where quality and sustainability are paramount. Meanwhile, South America and the Middle East & Africa represent emerging opportunities in the global organic acids market. These regions benefit from economic development and abundant agricultural resources, which provide a strong foundation for organic acid production and consumption.

- BASF SE

- Cargill, Incorporated

- Archer Daniels Midland Company

- Royal DSM (Reverdia)

- Nippon Shokubai Co., Ltd.

- DSM-Firmenich AG

- Roquette Freres

- Celanese Corporation

- Corbion N.V.

- Thermo Fisher Scientific

- Bartek Ingredients Inc.

- Fuso Chemical Co., Ltd.

- Inner Mongolia

- Mitsubishi Chemical Group

- Fengchen Group Co.,Ltd

- RZBC GROUP CO., LTD

- TINNAKORN CHEMICAL & SUPPLY

- Shandong Feiyang Chemical

- Jinan Finer Chemical Co., Ltd

- Anhui BBCA Biochemical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Uptake of Acetic Acid in Vinyl-Acetate-Monomer for Solar-EVA Films

- 4.2.2 Pharmaceutical-grade Lactic Acid Demand for Injectable Drug Formulations

- 4.2.3 Expansion of Citric-acid-based Natural Preservatives in Clean-Label Beverages

- 4.2.4 Growth of Succinic Acid as a Building Block for Bio-PBS and Bio-BDO

- 4.2.5 Feed-grade Formic & Propionic Acids Adoption for ASF-Free Swine Diets

- 4.2.6 Use in Animal Feed as Antibiotic Alternatives

- 4.3 Market Restraints

- 4.3.1 Stringent VOC Directives Limiting Petro-based Acrylic and Adipic Acids

- 4.3.2 Over-capacity and Price Compression in Chinese Low-purity Citric Acid

- 4.3.3 Environmental Concerns with Synthetic Acids Hindering the Market Growth

- 4.3.4 Technological and Infrastructural Barriers Hampering the Market Growth

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Acetic Acid

- 5.1.2 Citric Acid

- 5.1.3 Lactic Acid

- 5.1.4 Succinic Acid

- 5.1.5 Malic Acid

- 5.1.6 Propionic Acid

- 5.1.7 Formic Acid

- 5.1.8 Fumaric and Maleic Acids

- 5.1.9 Others (Benzoic, Gluconic, Adipic, etc.)

- 5.2 By Source

- 5.2.1 Bio-based

- 5.2.2 Petro-chemical

- 5.2.3 Hybrid/Co-product Streams

- 5.3 By Application

- 5.3.1 Food and Beverages

- 5.3.2 Animal Feed and Nutrition

- 5.3.3 Pharmaceuticals and Healthcare

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Industrial Chemicals and Intermediates (VAM, PTA, Acrylates, etc.)

- 5.3.6 Polymers and Bioplastics (PLA, PBS, PHA)

- 5.3.7 Others (Textiles, Lubricants, Electronics)

- 5.4 By Form

- 5.4.1 Liquid

- 5.4.2 Dry/Crystal/Powder

- 5.5 Geographic Analysis

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 India

- 5.5.5.3 Japan

- 5.5.5.4 Australia

- 5.5.5.5 Rest of Asia-Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Cargill, Incorporated

- 6.4.3 Archer Daniels Midland Company

- 6.4.4 Royal DSM (Reverdia)

- 6.4.5 Nippon Shokubai Co., Ltd.

- 6.4.6 DSM-Firmenich AG

- 6.4.7 Roquette Freres

- 6.4.8 Celanese Corporation

- 6.4.9 Corbion N.V.

- 6.4.10 Thermo Fisher Scientific

- 6.4.11 Bartek Ingredients Inc.

- 6.4.12 Fuso Chemical Co., Ltd.

- 6.4.13 Inner Mongolia

- 6.4.14 Mitsubishi Chemical Group

- 6.4.15 Fengchen Group Co.,Ltd

- 6.4.16 RZBC GROUP CO., LTD

- 6.4.17 TINNAKORN CHEMICAL & SUPPLY

- 6.4.18 Shandong Feiyang Chemical

- 6.4.19 Jinan Finer Chemical Co., Ltd

- 6.4.20 Anhui BBCA Biochemical

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

全球有机酸市场规模、份额、趋势和成长分析报告(2026-2034年)

全球有机酸市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球有机酸市场报告

2026年全球有机酸市场报告 全球氢碘酸市场,2025-2029年

全球氢碘酸市场,2025-2029年 氢碘酸市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、最终用途产业、应用、地区和竞争格局划分,2021-2031年)

氢碘酸市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、最终用途产业、应用、地区和竞争格局划分,2021-2031年) 有机酸市场规模、份额和成长分析(按产品、应用、来源、形态和地区划分)—产业预测(2026-2033 年)

有机酸市场规模、份额和成长分析(按产品、应用、来源、形态和地区划分)—产业预测(2026-2033 年) 全球有机酸市场按来源、类型、形态、应用、功能和地区划分-预测至2030年

全球有机酸市场按来源、类型、形态、应用、功能和地区划分-预测至2030年 2025-2033年有机酸市场报告(按类型、来源、最终用户和地区)有机酸市场-全球产业规模、份额、趋势、机会与预测,按类型、最终用途、地区和竞争细分,2020-2030 年夫西地酸市场-全球产业规模、份额、趋势、机会和预测,按销售管道(直接、间接)、最终用途(脓疱病、蜂窝性组织炎、割伤和伤口、眼部感染、其他)、按地区和竞争情况划分,2020 年至 2030 年预测

2025-2033年有机酸市场报告(按类型、来源、最终用户和地区)有机酸市场-全球产业规模、份额、趋势、机会与预测,按类型、最终用途、地区和竞争细分,2020-2030 年夫西地酸市场-全球产业规模、份额、趋势、机会和预测,按销售管道(直接、间接)、最终用途(脓疱病、蜂窝性组织炎、割伤和伤口、眼部感染、其他)、按地区和竞争情况划分,2020 年至 2030 年预测 鹅去氧胆酸原料药市场:依产品种类、等级、销售管道、最终用户 - 2025-2030 年全球预测

鹅去氧胆酸原料药市场:依产品种类、等级、销售管道、最终用户 - 2025-2030 年全球预测