|

市场调查报告书

商品编码

1844720

去氧剂:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030)Oxygen Scavengers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

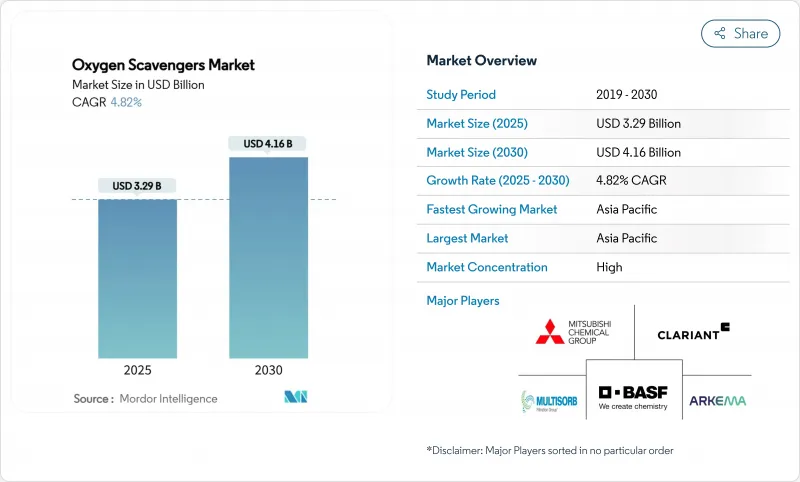

去氧剂市场规模预计在 2025 年达到 32.9 亿美元,预计到 2030 年将达到 41.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.82%。

需求正从传统的铁粉转向聚合物整合和基于酶的系统,以帮助品牌所有者满足更严格的保质期、纯度和可回收性目标。亚太地区是多层包装薄膜的生产中心,而北美则是高价值医药应用的领导者。美国食品药物管理局(FDA)的人类食品计画和欧盟法规2025/40等法规正在加速向避免金属离子迁移的非金属配方的转变。在终端用途方面,电子商务的蓬勃发展正鼓励品牌所有者选择即使在数週复杂的履约网路中也能保持有效的氧气管理技术,从而维持去氧剂市场的中期成长。

全球去氧剂市场趋势与洞察

新鲜即食食品和冷藏包装食品快速成长

消费者习惯向便利食品的转变,推动了主动氧气管理技术在肉类、海鲜和熟食类别中的广泛应用。品牌商正在将无袋空气清除层融入热成型托盘中,以确保产品在长期冷藏和零售保质期内保持颜色稳定。区域超级市场表示,减少废弃物和提高商品行销弹性是其主要优势,这促使代加工商指定能够在低温下快速启动的解决方案。因此,设备供应商正在改进高速托盘封口线,以适应预先装载空气清除树脂的多层薄膜,这些树脂不会损害密封的完整性。这种采用为美国和德国的薄膜挤出机带来了稳定的订单,巩固了去氧剂市场的基准成长。

药典对药品包装中残留氧气的规定日益严格

最新的 USP 和 EMA 指南设定了肠外和固态剂量包装中残留氧气的上限,鼓励药品製造商检验在规定的保质期内保持低于 0.5% 氧气的屏障系统。聚合物为基础的清除剂(如 Colorcon 的 PharmaKeep 系列)可在 10-90% 的相对湿度下发挥作用,解决药品的湿度敏感性问题,同时避免金属离子的风险。欧洲法规的发展轨迹类似,修订后的欧盟食品接触材料法规于 2025 年 3 月生效,引入了影响药品包装材料的更高的纯度要求和迁移限值。这些进步对于生技药品尤其明显,因为微量的氧气可以催化蛋白质降解,而对湿度敏感的小分子疗法则需要多年的稳定性数据。

对金属离子和官能基污染的担忧

铁基小袋会释放微量离子,这些离子会催化敏感膳食补充剂中的氧化反应,或导致高檔茶和咖啡中出现金属异味。监管审核现在要求在最恶劣的湿度条件下进行迁移测试,这促使一些品牌商在高价值SKU中完全淘汰铁基系统。聚合物封装降低了直接接触风险,但增加了原料成本,小型製造商难以承受。这种权衡阻碍了传统小袋包装在短期内渗透到药品和特殊食品管道,并在一定程度上抑制了去氧剂市场的发展。

細項分析

受成熟供应链、快速吸收率和低单位成本的推动,预计到 2024 年金属系统将占据去氧剂市场的 57.89%。该细分市场的规模优势,加上与全球肉类加工商和零嘴零食製造商的批量合同,支撑了入门级去氧剂的市场规模。然而,非金属系统预计将以 8.60% 的复合年增长率成长,是所有材料组中成长最快的。聚合物整合系统无需在生产线末端插入包装袋,从而减少了高速灌装封口生产线的转换时间。酵素和抗坏血酸配方进一步扩大了限制金属添加剂的清真、犹太洁食和洁净标示品牌的选择范围。製药审核越来越强调聚合物系统与控湿仓库的兼容性,鼓励泡壳膜挤出机采用 Amosorb 和 PharmaKeep 浓缩液。奈米复合催化剂的持续研究和开发表明,非金属解决方案可能在 2030 年后取代铁铅。总之,这些动态增强了去氧剂市场材料部分的多样性。

第二代化学品也符合回收法规的要求,将清除功能融入单晶片 PET 或 PP 结构而非贴合加工铝箔中,这种方法支持欧盟法规 2025/40 的循环经济目标。树脂供应商正在展示瓶到瓶的可回收性,同时将雾度增加降至最低,从而实现了饮料品牌到 2030 年回收率达到 30% 的承诺。同时,金属袋製造商正在透过优化粉末粒度和添加吸湿缓衝剂来延缓海运过程中的过早活化。因此,材料平台之间的竞争集中在平衡活化抑制、单位经济性和下游可回收性上,这种竞争将影响去氧剂市场中转化商和全球快速消费品买家的采购决策。

全球去氧剂市场报告按类型(金属去氧剂和非金属去氧剂)、最终用户行业(食品饮料、製药、石油天然气、电力等)以及地区(北美、南美、欧洲、中东和非洲)对该行业进行了细分。市场预测以美元计算。

区域分析

预计到2024年,亚太地区将占全球38.05%的需求,到2030年,复合年增长率将达到7.50%,这得益于中国不断扩大的医药出口基地和印度软膜转化产能的快速扩张。该地区各国政府持续补贴低温运输物流,并设定减少食品废弃物的国家目标,刺激了主动阻隔解决方案的采用。该地区受益于成熟的原材料供应链和食品加工行业日益增长的需求,满足了国内和出口市场的需求。三菱去氧剂化学透过其子公司——日本的MGC Ageless和泰国的Ageless——在该地区拥有强大的影响力,展现出其完善的基础设施,以支持脱氧剂的生产和分销。

北美是一个成熟且技术先进的去氧剂市场。严格的FDA监管要求进行全面的迁移测试,这推动了对完整记录的聚合物配方的需求。品牌所有者优先考虑符合州级「生产者责任延伸」法规规定的机械回收目标的解决方案。加拿大肉类加工商指定使用大容量包装袋和自动装填设备,以满足对亚洲的出口需求,从而维持稳定的替换需求。在墨西哥,新兴的便利食品产业进一步支撑了区域成长,但成本压力也造成了一系列被动和主动的障碍。

欧洲的监管驱动力与北美相似,但也进一步拥抱循环经济的野心。欧盟法规 2025/40 要求到 2030 年所有包装都必须可回收,这刺激了对具有内建回收功能的整体结构的投资。法国和德国的主要饮料集团正在试用含有非金属添加剂的 宝特瓶瓶坯,以使氧气保护与押金返还系统保持一致。东欧薄膜挤出机製造商正在从西方供应商进口聚合物浓缩物,以缩小技术差距并推动应用。虽然中东/非洲和南美洲在绝对数量上落后,但随着现代食品零售业态的扩张,人们的兴趣正在加速成长。在这些新兴市场,开发银行资助的示范计划已经证明了活性氧管理在减少食品腐败方面的益处,预示着去氧剂市场在中期的需求将稳定成长。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 新鲜即食食品和冷藏包装食品快速成长

- 药典对药品包装中残留氧气的规定更加严格

- 扩大无菌低温运输邮件套件物流

- 奈米复合聚合物清除剂的商业化

- 电子商务导致运送时间延长

- 市场限制

- 对金属离子污染和感官污染的担忧

- 经济高效、阻隔性薄膜替代品

- 铁矿石和特殊催化剂价格波动剧烈

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 按类型

- 金属去氧剂

- 非金属去氧剂

- 按最终用户产业

- 饮食

- 製药

- 石油和天然气

- 电力

- 化学

- 纸浆和造纸

- 其他终端用户产业(水处理、污水处理等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 印尼

- 越南

- 马来西亚

- 菲律宾

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 土耳其

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- Accepta Water Treatment

- Arkema

- Avient Corporation

- BASF

- Clariant

- Desiccare Inc.

- Ecolab

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Multisorb

- Solenis

- Veolia

第七章 市场机会与未来展望

The Oxygen Scavengers Market size is estimated at USD 3.29 billion in 2025, and is expected to reach USD 4.16 billion by 2030, at a CAGR of 4.82% during the forecast period (2025-2030).

Demand pivots from conventional iron powders toward polymer-integrated and enzyme-based systems that help brand owners satisfy stricter shelf-life, purity and recyclability targets. Asia-Pacific represents the core production base for multilayer packaging films while North America drives high-value pharmaceutical applications, and both regions influence raw-material sourcing strategies for global suppliers. Regulations such as the FDA's Human Foods Program and EU Regulation 2025/40 are amplifying the shift toward non-metallic formulations that avoid metal-ion migration. Across end-uses, the e-commerce boom forces brand owners to choose oxygen management technologies that remain effective during weeks-long journeys through complex fulfilment networks, sustaining medium-term growth for the oxygen scavengers market.

Global Oxygen Scavengers Market Trends and Insights

Rapid Growth in Fresh-Ready & Chilled Packaged Meals

Shifts in consumer habits toward convenience foods have widened deployment of active oxygen management across meat, seafood and deli categories. Brand owners integrate sachet-free scavenging layers into thermoformed trays so products remain color-stable throughout extended chilled storage and retail display. Regional supermarket chains cite reduced waste and improved merchandising flexibility as key benefits, prompting co-packers to specify solutions that activate rapidly at low temperatures. Equipment suppliers are therefore adapting high-speed tray-sealing lines to accommodate multilayer films pre-loaded with scavenging resins that do not compromise seal integrity. This adoption dynamic feeds a steady order pipeline for film extruders located in the United States and Germany, reinforcing baseline growth for the oxygen scavengers market.

Stricter Pharmacopeia Limits on Residual Oxygen in Drug Packs

The latest USP and EMA guidelines cap residual oxygen in parenteral and solid-dose packs, urging drug makers to validate barrier systems that sustain <=0.5% oxygen throughout the stated shelf life. Polymer-based scavengers such as Colorcon's PharmaKeep series can function across 10-90% relative humidity, addressing drug-product moisture sensitivity while avoiding metal-ion risks. the European regulations are following similar trajectories, with the EU's revised food contact material regulations effective March 2025 introducing enhanced purity requirements and migration limits that affect pharmaceutical packaging materials .Contract development organizations embed such additives directly into polyolefin blisters, which simplifies line qualification versus separate sachets. These advances are most visible in biologics, where trace oxygen can catalyze protein degradation, and in moisture-reactive small-molecule therapies that require multi-year stability data.

Metal-Ion Contamination & Sensory-Taint Concerns

Iron-based sachets release trace ions that can catalyze oxidative reactions in sensitive nutraceuticals and lead to metallic off-notes in premium teas and coffees. Regulatory auditors now require migration testing under worst-case humidity, prompting some brand owners to exclude ferrous systems entirely for high-value SKUs. Polymer encapsulation methods lower direct contact risk, yet they raise raw-material costs that smaller manufacturers struggle to absorb. This trade-off tempers near-term penetration of traditional sachets in pharmaceutical and specialty-food channels, restraining a portion of the oxygen scavengers market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Aseptic Cold-Chain Meal-Kit Logistics

- Commercialization of Nanocomposite Polymer Scavengers

- Cost-Effective and High-Barrier Film Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic formulations retained 57.89% oxygen scavengers market share in 2024 thanks to established supply chains, rapid absorption kinetics and low unit cost. The segment's scale advantage translates into volume contracts with global meat processors and snack producers, anchoring the oxygen scavengers market size for entry-level applications. However, non-metallic systems are growing at an 8.60% CAGR, the fastest among all material groups. Polymer-integrated variants eliminate the need for end-of-line sachet insertion, which shortens changeover time on high-speed fill-and-seal lines. Enzyme and ascorbic-acid formulations further widen options for halal, kosher and clean-label brands that restrict metallic additives. Pharmaceutical audits increasingly cite polymer systems' compatibility with humidity-controlled warehouses, encouraging blister-film extruders to adopt Amosorb and PharmaKeep concentrates. Continuous R-&D around nanocomposite catalysts suggests non-metallic solutions could erode iron's lead beyond 2030, especially if unit prices align with mainstream snack food budgets. Collectively, these dynamics reinforce material-segment diversity within the oxygen scavengers market.

Second-generation chemistries also align with recycling mandates because they embed scavenging capacity in mono-material PET or PP structures rather than laminated foil, an approach that supports circular-economy targets under EU Regulation 2025/40. Resin suppliers have demonstrated bottle-to-bottle recyclability with minimal haze increase, satisfying beverage-brand commitments to 30% recycled content by 2030. Meanwhile, metallic sachet makers counter by optimizing powder particle size and adding moisture-absorbing buffers that delay premature activation during ocean transit. Competition across material platforms therefore centers on balancing activation control, unit economics and downstream recycling performance, a contest that will shape procurement decisions for both converters and global CPG buyers in the oxygen scavengers market.

The Global Oxygen Scavenger Market Reports Segments the Industry by Type (Metallic Oxygen Scavengers and Non-Metallic Oxygen Scavengers), End-User Industry (Food and Beverage, Pharmaceutical, Oil and Gas, Power and More), and Geography (Asia-Pacific, North America, South America, Europe, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 38.05% of 2024 demand and is projected to deliver a 7.50% CAGR to 2030, underpinned by China's expanding pharmaceutical export base and India's rapid capacity additions in flexible-film conversion. Governments across the region continue to subsidize cold-chain logistics and set national targets for food-waste reduction, stimulating adoption of active barrier solutions. The region benefits from established supply chains for raw materials and growing demand from food processing industries that serve both domestic and export markets. Mitsubishi Gas Chemical's strong presence in the region through subsidiaries like MGC AGELESS Co., Ltd. in Japan and AGLESS (THAILAND) CO., LTD. demonstrates the established infrastructure supporting oxygen scavenger production and distribution.

North America represents a mature but technically advanced arena for the oxygen scavengers market. Stringent FDA oversight mandates exhaustive migration testing and drives demand for fully documented polymer formulations. Brand owners prioritize solutions compatible with mechanical recycling targets under state-level extended producer responsibility rules. Canadian meat processors, dealing with export voyages toward Asia, specify high-capacity sachets and automated insertion equipment, sustaining steady replacement demand. Mexico's rising convenience-food sector further supports regional growth, although cost pressures favour a mix of passive and active barriers.

Europe mirrors North American regulatory drivers but layers additional circular-economy ambitions. EU Regulation 2025/40 will require all packaging to be recyclable by 2030, spurring investments in mono-material structures with embedded scavenging capability. Large beverage groups in France and Germany pilot PET bottle preforms containing non-metallic additives, aligning oxygen protection with deposit-return systems. Eastern European film extruders increasingly import polymer concentrates from Western suppliers, bridging technology gaps and spreading adoption. The Middle East & Africa and South America trail in absolute volume yet show accelerating interest as modern grocery retail formats expand. Across these emerging regions, demonstration projects funded by development banks illustrate the spoilage-reduction benefits of active oxygen management, pointing toward steady medium-term demand inflows for the oxygen scavengers market.

- Accepta Water Treatment

- Arkema

- Avient Corporation

- BASF

- Clariant

- Desiccare Inc.

- Ecolab

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Multisorb

- Solenis

- Veolia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth in Fresh-Ready and Chilled Packaged Meals

- 4.2.2 Stricter Pharmacopeia Limits on Residual Oxygen in Drug Packs

- 4.2.3 Expansion of Aseptic Cold-Chain Mealkit Logistics

- 4.2.4 Commercialisation of Nanocomposite Polymer Scavengers

- 4.2.5 E-commerce Demand for Longer Transit Shelf-Life

- 4.3 Market Restraints

- 4.3.1 Metal-Ion Contamination & Sensory-Taint Concerns

- 4.3.2 Cost-Fffective and High-Barrier Film Substitutes

- 4.3.3 Volatile Iron-Ore and Specialty Catalyst Price Swings

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Metallic Oxygen Scavengers

- 5.1.2 Non-metallic Oxygen Scavengers

- 5.2 By End-user Industry

- 5.2.1 Food and Beverage

- 5.2.2 Pharmaceutical

- 5.2.3 Oil and Gas

- 5.2.4 Power

- 5.2.5 Chemical

- 5.2.6 Pulp and Paper

- 5.2.7 Other End-user Industries (Water and Waste-Water Treatment, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Indonesia

- 5.3.1.7 Vietnam

- 5.3.1.8 Malaysia

- 5.3.1.9 Philippines

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Accepta Water Treatment

- 6.4.2 Arkema

- 6.4.3 Avient Corporation

- 6.4.4 BASF

- 6.4.5 Clariant

- 6.4.6 Desiccare Inc.

- 6.4.7 Ecolab

- 6.4.8 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.9 Multisorb

- 6.4.10 Solenis

- 6.4.11 Veolia

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

氧气吸收剂包装市场预测至2034年—按类型、形式、整合方法、材料、应用、最终用户和地区分類的全球分析

氧气吸收剂包装市场预测至2034年—按类型、形式、整合方法、材料、应用、最终用户和地区分類的全球分析 氧气吸收剂市场:按类型、形式、包装和最终用户划分 - 2026-2032年全球预测脱氧剂市场:依产品类型、等级、应用、最终用途产业和通路划分-全球预测,2026-2032年

氧气吸收剂市场:按类型、形式、包装和最终用户划分 - 2026-2032年全球预测脱氧剂市场:依产品类型、等级、应用、最终用途产业和通路划分-全球预测,2026-2032年 全球去氧剂包装市场:市场规模、份额、成长和行业分析:按类型、最终用途和地区预测(至2034年)

全球去氧剂包装市场:市场规模、份额、成长和行业分析:按类型、最终用途和地区预测(至2034年) 2026年全球氧气吸收剂市场报告

2026年全球氧气吸收剂市场报告 除氧剂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测,2026-2033年

除氧剂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测,2026-2033年 去氧剂市场-2026-2031年预测

去氧剂市场-2026-2031年预测 氧气清除剂市场规模、份额和成长分析(按类型、配方、剂型、最终用户和地区划分)—2026-2033年产业预测金属清除剂市场(按材料类型、金属类型、技术、分销管道和最终用户产业)—2025-2030 年全球预测

氧气清除剂市场规模、份额和成长分析(按类型、配方、剂型、最终用户和地区划分)—2026-2033年产业预测金属清除剂市场(按材料类型、金属类型、技术、分销管道和最终用户产业)—2025-2030 年全球预测 铝脱氧剂市场报告:趋势、预测和竞争分析(至 2031 年)

铝脱氧剂市场报告:趋势、预测和竞争分析(至 2031 年)