|

市场调查报告书

商品编码

1844733

低温涂料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Low Temperature Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

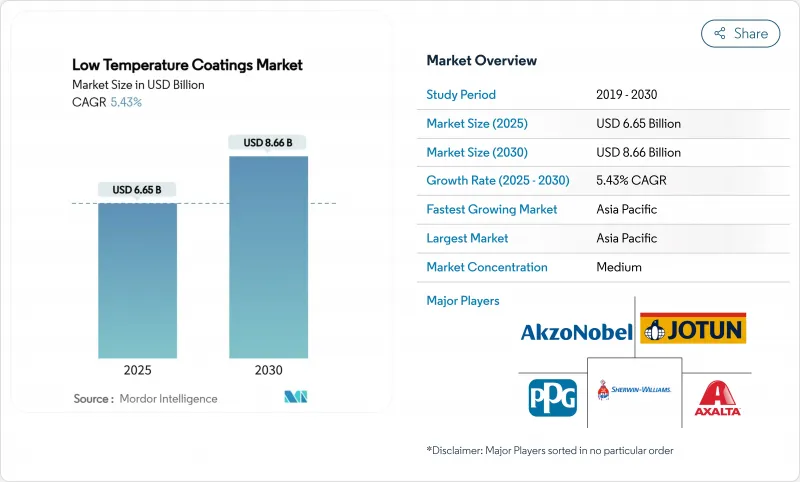

低温涂料市场规模预计在 2025 年为 66.5 亿美元,预计到 2030 年将达到 86.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.43%。

这项稳步进展反映了减少製程热排放的监管压力、允许使用较低固化温度的能源价格上涨,以及能够在接近 120°C 的温度下充分发挥性能的技术进步。随着工厂从 375°F 的烘烤週期过渡到在 285°F 下固化的配方,通常可节省高达 25% 的能源,从而提高产量并减少碳足迹。需求受到塑胶、复合材料和 3D 列印零件使用的增加以及电动车 (EV) 生产的快速增长的推动,这些零件在传统烤箱条件下会变形,这需要热稳定但固化缓慢的电池机壳。竞争适中,主要供应商利用树脂化学、雷射辅助固化和策略性收购来捍卫市场份额,而利基市场参与者则瞄准超低烘烤领域,例如离岸风力发电维护和积层製造。原料成本(尤其是二氧化钛)的变化以及沉积 25µm 以下超薄膜的技术挑战仍然是主要阻力。

全球低温涂料市场趋势与洞察

固化温度较低,节省能源

这一数字已在生产线上得到证实,在生产线上,固化峰值温度从400°F(约220°C)降至325°F(约170°C),同时仍保持了耐腐蚀性。更短的炉内停留时间也提高了生产线速度并提升了资产利用率。加州和德国等能源成本较高的地区是首批采用此类配方的地区之一。由于水电费减少和过滤器维护频率降低,通常一年内即可收回成本。减少范围一排放有助于为未来的碳边境定价做好准备。

电动车和电子设备中热感基板的应用日益增多

电动车电池外壳和电子模组无法承受传统烘烤过程固有的热衝击。在 130 度C下聚合的涂层可保护电介质、保留黏合层,并达到绝缘电阻目标,而不会破坏电池单元的化学性质。由于热界面材料在 35°C 下粘合,因此涂装车间现在在电池组装下游加入了整合式低温烘烤区。半导体封装线也反映了这一趋势,要求循环温度不超过 150°C,以避免细间距基板翘曲。亚太地区凭藉其密集的电动车供应链处于领先地位,但北美超级工厂正在迅速指定相同的固化窗口。

我们实现超薄膜的能力受到限制

当粒径低于25微米时,许多粉末化学品容易出现橘皮和孔隙,因为降低的烘箱温度会限制流动和流平性。因此,汽车清漆工程不愿将整个车型改装,而是保留低温烘烤生产线,用于能够保持更高厚度的中涂。在135°C下提高交联密度的催化剂组合虽然有帮助,但会增加配方成本。混合聚酯和奈米填充树脂的研究仍在继续,但距离取得重大突破仍需两到四年。

細項分析

得益于其在建筑耐久性方面的长期业绩和极具竞争力的价格,聚酯体系将在2024年占据40.12%的销售额。聚酯与建筑领域广泛使用的镀锌钢也具有良好的附着力,这巩固了其在建筑领域的主导地位。然而,在低温涂料市场,聚氨酯在兼具柔韧性和耐化学性的应用领域中更具优势。双组分和封闭型异氰酸酯体係可在120°C下固化,从而开启了聚酯无法企及的塑胶和复合材料类别。

由于电动车製造商指定电池盖采用柔性介电层,聚氨酯的产量预计将以7.18%的复合年增长率成为所有树脂中最快的。墨西哥聚氨酯消费量年增率高达5-7%,证实了全球聚氨酯消费量的强劲成长动能。水性双组分聚氨酯混合材料符合VOC(挥发性有机化合物)法规,同时提供家电边框所需的附着力。这些因素共同推动了聚氨酯在低温涂料市场的崛起。

受规模经济和製程熟悉度的推动,粉末技术在2024年的销售额中占比将达到72.14%。配方製造商已将固化阈值从十年前的180°C提高到今天的140°C,从而将每平方公尺的能耗降低了约三分之一。目前,最大的粉末供应商提供的雷射固化系统可在室温下三分钟内达到最佳物理性能,这项创新可望进一步提高生产线的生产效率。

UV/EB 固化技术发展迅速,预计到 2030 年复合年增长率将达到 7.45%。其无溶剂操作特性,加上 110°C 的低固化温度,对中密度纤维板 (MDF) 家俱生产线和乙烯基地板材料工厂极具吸引力。当操作员需要立即处理物料以适应即时组装区时,UV/EB 固化技术的应用将加速。这些特性拓宽了技术选择,并促进了低温涂料市场规模细分领域的良性竞争。

区域分析

预计到2024年,亚太地区将占全球粉末涂料总收入的46.15%,复合年增长率为7.27%。中国庞大的粉末涂料丛集正受惠于家电和电动车的大规模生产,而印度的汽车生产和印尼的家电出口也将进一步拉动这个产业的发展。能源价格上涨以及各大城市VOC法规的收紧,进一步推动了低温固化化学品的普及。

北美以以金额为准计算位居第二,其成长受到政策和技术领先地位的推动。美国能源局对雷射硬化粉末研究的资助加速了商业化进程,而加州的工艺热法规则将实验室突破转化为实际购买。墨西哥正在投资360万美元扩建其捲材涂层生产线,以加强其跨境供应链。

欧洲在创新方面与北美竞争,同时也引入了积极的碳定价政策。欧盟的《工业碳管理战略》设定了明确的储存目标,并且正在引导工业涂料製造商走向节能减排的方案。同时,在中东、非洲和南美洲,跨国客户正在强制执行统一的规范,逐渐推动製造商采用低温烘烤系统,从而扩大了整体低温涂料的市场规模。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 固化温度较低,节省能源

- 扩大热敏基板在电动车和电子设备的应用

- 製程热碳定价加速采用

- 需要超低烘烤涂层的 3D 列印零件

- 离岸风力塔维护转向低温固化

- 市场限制

- 我们实现超薄膜的能力受到限制

- 与常温固化UV/EB系统的竞争

- 复合基板上的热衝击缺陷

- 价值链分析

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场规模及成长预测

- 按树脂

- 聚酯纤维

- 环氧树脂

- 聚氨酯

- 丙烯酸纤维

- 其他树脂

- 依技术

- 粉末

- 液体溶剂型

- 液体 - 水基

- UV/EB固化型

- 按基材

- 金属

- 塑胶和复合材料

- 木头

- 其他基材

- 按最终用户产业

- 建筑学

- 工业的

- 车

- 木头

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- Akzo Nobel NV

- Allnex GmbH

- APV Engineered Coatings

- Asian Paints Limited

- Axalta Coating Systems LLC

- BASF

- Beckers Group

- Covestro AG

- Hempel A/S

- IGP Pulvertechnik AG

- Jotun

- Kansai Paint Co. Ltd.

- Nippon Paint Holdings Co. Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- TCI Powder

- Teknos Group

- The Sherwin-Williams Company

- Tiger Coatings GmbH and Co. KG

第七章 市场机会与未来展望

The Low Temperature Coatings Market size is estimated at USD 6.65 billion in 2025, and is expected to reach USD 8.66 billion by 2030, at a CAGR of 5.43% during the forecast period (2025-2030).

The steady advance reflects regulatory pressure to trim process-heat emissions, rising energy prices that reward cooler cure profiles, and technological progress that now allows full performance at temperatures close to 120 °C. Energy savings of up to 25% have become common when plants shift from 375 °F bake cycles to formulations that cure at 285 °F, improving throughput and lowering carbon footprints. Demand is also boosted by the growing use of plastics, composites, and 3-D-printed parts that deform under conventional oven conditions, as well as the surge in electric vehicle (EV) production that requires thermally stable but gently cured battery enclosures. Competitive intensity is moderate: leading suppliers leverage resin chemistry, laser-assisted curing, and strategic acquisitions to defend share while niche players target ultra-low-bake segments such as offshore wind maintenance and additive manufacturing. Raw-material cost swings, notably titanium dioxide, and the technical difficulty of depositing ultra-thin films below 25 µm remain the principal headwinds.

Global Low Temperature Coatings Market Trends and Insights

Energy Savings from Reduced Cure Temperatures

Plants that retrofit to low-temperature powder systems save up to 25% in gas or electricity consumption, a figure confirmed by production lines that dropped cure peaks from 400 °F to 325 °F while maintaining corrosion resistance. Shorter oven residence also pushes line speeds higher, improving asset utilization. Regions with high energy tariffs such as California and Germany adopt these formulations first, yet the payoff is now similar elsewhere because carbon charges are widening. Payback is often achieved within one year thanks to slimmer utility bills and fewer filter-maintenance cycles. The move lowers scope 1 emissions, positioning users for future carbon-border fee regimes.

Growing Adoption for Heat-Sensitive Substrates in Electric Vehicles and Electronics

EV battery housings and electronic modules cannot tolerate the thermal shock typical of legacy bakes. Coatings that polymerize at 130 °C protect dielectrics, preserve adhesive layers, and meet insulation resistance targets without disturbing battery cell chemistries. Thermal interface materials are bonded at 35 °C, so paint shops now integrate integrated low-bake zones downstream of cell assembly. Semiconductor packaging lines mirror the trend by asking for sub-150 °C cycles that avoid warpage in fine-pitch boards. Asia-Pacific leads because of its EV supply-chain density, but North American gigafactories are rapidly specifying identical cure windows.

Limited Ability to Achieve Ultra-Thin Films

Below 25 µm, many powder chemistries suffer orange-peel and pore formation because lower oven temperatures restrict flow and leveling. Automotive clearcoat programs therefore hesitate to convert entire fleets, instead reserving low-bake lines for mid-coat layers where film build can remain thicker. Catalyst packages that accelerate crosslink density at 135 °C help but add formulation cost. Research into hybrid polyesters and nanofilled resins continues, yet large-scale breakthroughs remain two to four years away.

Other drivers and restraints analyzed in the detailed report include:

- Process-Heat Carbon Pricing Accelerating Adoption

- 3-D-Printed Parts Requiring Ultra-Low-Bake Coatings

- Competition from Ambient-Cure UV/EB Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester systems accounted for 40.12% of 2024 revenue, supported by a long record of architectural durability and competitive pricing. Polyesters also bond well to galvanized steel, a high-volume substrate in construction, which cements their baseline position. The low temperature coatings market nevertheless favors polyurethane for applications demanding both flexibility and chemical resistance. Two-component and blocked isocyanate chemistries cure at 120 °C, opening plastic and composite categories that polyesters cannot reach.

Polyurethane volumes are projected to expand at a 7.18% CAGR, the fastest among resins, as EV makers specify flexible dielectric layers for battery covers. Mexico's 5-7% annual growth in polyurethane consumption underscores global momentum. Water-borne 2K-PUR hybrids meet VOC caps yet still deliver the adhesion required for consumer electronics bezels. These factors together reinforce polyurethane's rise within the low temperature coatings market.

Powder technology held 72.14% of 2024 revenue owing to scale economics and process familiarity. Formulators have driven cure thresholds from 180 °C a decade ago to 140 °C today, slashing energy intake per square meter by roughly one-third. The largest powder suppliers now offer laser-cured systems that reach full properties in three minutes at room temperature, an innovation poised to lift line productivity further.

UV/EB curing is the sprinter, forecast at a 7.45% CAGR to 2030. It merges solvent-free operation with cure temperatures as low as 110 °C, which appeals to MDF furniture lines and vinyl flooring plants. Adoption accelerates whenever operators need instant handling to feed just-in-time assembly zones. These capabilities broaden technological choice and stimulate healthy rivalry inside the low temperature coatings market size segment, where UV/EB solutions already command double-digit shares in industrial wood.

The Low Temperature Coatings Market Report is Segmented by Resin (Polyester, Epoxy, and More), Technology (Powder, Liquid - Solvent-Borne, Liquid - Water-Borne, UV/EB-cured), Substrate (Metals, Plastics and Composites, Wood, Other Substrates), End-User Industry (Architectural, Industrial, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the landscape with 46.15% of 2024 revenue and is projected to compound at 7.27% CAGR, the fastest regional clip. China's vast powder coating clusters benefit from high-volume appliance and EV production, while India's automotive buildouts and Indonesia's appliance exports supply additional pull. Rising energy tariffs and intensifying VOC rules in major cities further encourage the adoption of cooler-cure chemistries.

North America ranks second in value; its growth rests on both policy and technology leadership. The U.S. Department of Energy's funding for laser-cured powder research shortens commercialization timelines, and California's process-heat regulations translate lab breakthroughs into real purchasing commitments. Mexico adds momentum by expanding coil-coat lines with USD 3.6 million in new capacity, strengthening cross-border supply chains.

Europe matches North America for innovation yet differs by wielding aggressive carbon pricing. The EU Industrial Carbon Management strategy sets explicit storage targets, nudging industrial coaters toward energy-lean options. Meanwhile, manufacturers across the Middle East, Africa, and South America gradually migrate to low-bake systems as multinational customers enforce uniform specifications, enlarging the overall low temperature coatings market footprint.

- Akzo Nobel N.V.

- Allnex GmbH

- APV Engineered Coatings

- Asian Paints Limited

- Axalta Coating Systems LLC

- BASF

- Beckers Group

- Covestro AG

- Hempel A/S

- IGP Pulvertechnik AG

- Jotun

- Kansai Paint Co. Ltd.

- Nippon Paint Holdings Co. Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- TCI Powder

- Teknos Group

- The Sherwin-Williams Company

- Tiger Coatings GmbH and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy savings from reduced cure temperatures

- 4.2.2 Growing adoption for heat-sensitive substrates in electronic vehicles and electronics

- 4.2.3 Process-heat carbon pricing accelerating adoption

- 4.2.4 3-D printed parts requiring ultra-low-bake coatings

- 4.2.5 Offshore wind tower maintenance shift to low-temp cures

- 4.3 Market Restraints

- 4.3.1 Limited ability to achieve ultra-thin films

- 4.3.2 Competition from ambient-cure UV/EB systems

- 4.3.3 Thermal-shock defects on composite substrates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Polyester

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Acrylic

- 5.1.5 Other Resins

- 5.2 By Technology

- 5.2.1 Powder

- 5.2.2 Liquid - Solvent-borne

- 5.2.3 Liquid - Water-borne

- 5.2.4 UV / EB-cured

- 5.3 By Substrate

- 5.3.1 Metals

- 5.3.2 Plastics and Composites

- 5.3.3 Wood

- 5.3.4 Other Substrates

- 5.4 By End-User Industry

- 5.4.1 Architectural

- 5.4.2 Industrial

- 5.4.3 Automotive

- 5.4.4 Wood

- 5.4.5 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Allnex GmbH

- 6.4.3 APV Engineered Coatings

- 6.4.4 Asian Paints Limited

- 6.4.5 Axalta Coating Systems LLC

- 6.4.6 BASF

- 6.4.7 Beckers Group

- 6.4.8 Covestro AG

- 6.4.9 Hempel A/S

- 6.4.10 IGP Pulvertechnik AG

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co. Ltd.

- 6.4.13 Nippon Paint Holdings Co. Ltd.

- 6.4.14 PPG Industries, Inc.

- 6.4.15 RPM International Inc.

- 6.4.16 TCI Powder

- 6.4.17 Teknos Group

- 6.4.18 The Sherwin-Williams Company

- 6.4.19 Tiger Coatings GmbH and Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment