|

市场调查报告书

商品编码

1846143

绿色涂料:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Green Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

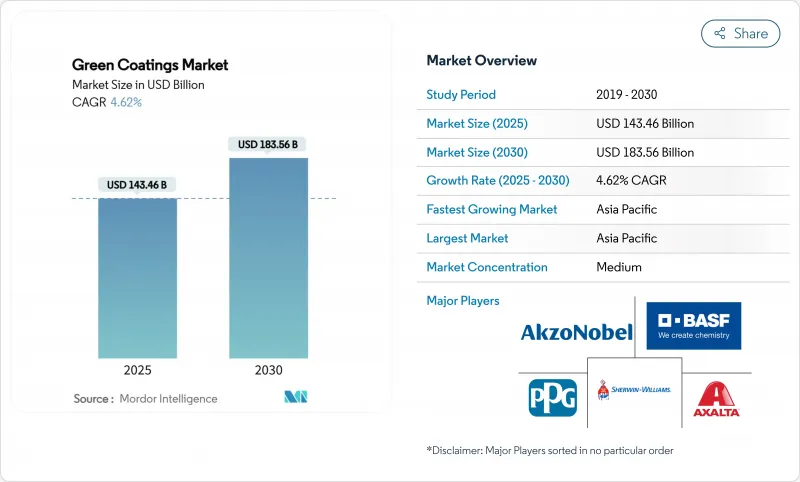

预计2025年绿色涂料市场规模将达到1,464.6亿美元,到2030年将达到1,835.6亿美元,复合年增长率为4.62%。

监管部门对挥发性有机化合物 (VOC) 限值要求的严格化、水性化学品和粉末技术的快速发展及其在汽车和建筑应用领域的渗透,仍然是绿色涂料市场的主要成长动力。加州南海岸空气品质管理区已根据第 1151 号修正案降低了汽车修补漆产品的 VOC 允许含量,并计划在 2033 年实施更严格的标准。同时,欧盟 (EU) 将从 2026 年 8 月起禁止在食品接触包装中使用全氟和多氟烷基物质 (PFAS),这将推动包装配方师转向生物基阻隔技术。此外,目前用于提高水性树脂耐久性的技术已可与溶剂型树脂相媲美。

全球绿色涂料市场趋势与洞察

有关VOC排放的严格环境法规

新的VOC法规正在重新定义绿色涂料市场可接受的配方界线。南海岸空气品质管理区(AQMD)的第1151号规则将从2025年5月起逐步降低汽车补漆产品的VOC限值,到2033年达到最严格的阈值,推动汽车修理厂转向水性系统。欧盟的《包装和包装废弃物法规》将PFAS的单一物质含量限制为25 ppb,总合限制为250 ppb,这促使包装供应商从含氟化合物转向生物基被覆剂。拥有合规产品组合的公司将享有先发优势,而局限于传统溶剂型产品的製造商将面临更高的合规成本和潜在的市场排斥。

低VOC建筑涂料需求不断成长

房屋维修、商业维修和绿色建筑标准持续推动建筑价值链向低VOC替代品靠拢。据宣伟公司称,住宅重涂订单正明显转向更易于回收、体积碳足迹更低的涂料。如今,水性涂料的保光性和耐刮擦性已与溶剂型涂料不相上下。阿克苏诺贝尔的RUBBOL WF 3350正是这种转变的典范,它结合了20%的生物基成分,并保证了室内外木器涂料的耐久性。

与溶剂型系统相比,在恶劣环境下的性能差异

船体、海上平台、化学品储存槽等仍需要含溶剂、高固态环氧树脂的长期耐污性和阻隔强度。自修復硅氧烷杂化材料和无铬缓蚀剂正在兴起,但由于认证週期长以及船东对未经测试的化学品的抵触情绪,商业性应用进展缓慢。

細項分析

水性体系将在绿色涂料市场保持主导,到2024年将占据55.16%的市场。其主导地位源自于良好的合规性和持续的树脂升级,可提供与溶剂型涂料相当的机械强度。马自达将整个工厂改用先进的水性面漆,将挥发性有机化合物(VOC)排放减少了57%,同时保持了展示室的光泽度。然而,粉末涂料的发展速度最快,到2030年的复合年增长率将达到6.51%。现在,催化剂辅助红外线炉只需2-3分钟即可在约225°C的温度下固化厚涂层,从而提高了生产能力并降低了公用事业成本。剪切机的Powdura ECO展示了一种循环设计,将相当于16个半升瓶的再生PET嵌入一磅粉末中。粉末基绿色涂料市场规模预计将随着150°C低温固化配方的出现而扩大,这将为热敏塑胶和中密度纤维板家具等应用开闢新的应用领域。另一方面,紫外光固化流体在电子产业占据特殊的市场地位,因为该产业需要近乎即时的固化。

绿色涂料产业也受惠于高固含醇酸树脂和丙烯酸混合涂料。这些系统的溶剂含量可达250克/公升或更低,且不会影响湿边或对金属基材的附着力。总而言之,这强化了人们的认知,即永续化学品能够达到甚至超越传统基准。

区域分析

亚太地区确立了主导地位,2024年占销售额的44.05%,并将在2030年实现5.56%的最快复合年增长率。预计到2024年,印尼的产量将超过100万吨,其中水性装饰涂料将占当地产量的67%。中国《快递包装方法》(GB 43352-2023)将进一步刺激该地区的绿色涂料市场,该法将强制电商仓库改用合规涂料。印度食品安全与标准局(FSSAI)加强食品包装监管的措施也刺激了需求。持续的都市化、汽车产量的成长以及对OEM涂料厂的外国直接投资将为该地区的绿色涂料市场提供长期发展动力。

受加州VOC标准和强劲的住宅重涂週期的推动,北美正处于復苏之路。通用汽车的「三湿」技术凸显了其低能耗生产线的竞争力,而多家一级供应商正在转向简化颜色转换的水性底漆。加拿大也取得了类似的进展,家电製造商正在投资粉末喷涂房,而墨西哥的线圈涂布产能正在进行360万美元的升级,为该地区提供了一个经济高效的供应基地。

欧洲对全氟烷基化合物(PFAS)实施了全面的限制,并考虑了碳边界问题,在激励快速再製造方面仍发挥重要作用。成员国已对高溶剂二氧化钛的进口征收反倾销税,间接推动负责人转向低溶剂或水溶性工艺,从而减少颜料用量。德国和法国持续孵化生物基树脂新兴企业,并与现有企业集团加强技术合作。

南美、中东和非洲等新兴地区的应用速度虽然放缓,但正在加速。巴西的工业产出和沙乌地阿拉伯的「2030愿景」大型企划正在提升永续涂料在防护铁製品和装饰生产线中的重要性。然而,监管执法的碎片化以及可再生原料取得管道的有限性,正在减缓一些区域市场的步伐。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 有关VOC排放的严格环境法规

- 低VOC建筑涂料需求不断成长

- 汽车原始设备製造商转向节能喷漆车间

- 水性树脂化学的进步增强了耐久性

- 利用农业废弃物生产生物基树脂

- 市场限制

- 与溶剂型产品相比,在恶劣环境下的性能差异

- 最终用户的总涂层成本更高

- 生物基原料供应受限

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按类型

- 水性

- 粉末

- 高固体

- UV固化涂料

- 按用途

- 建筑涂料

- 工业漆

- 汽车涂料

- 木材涂料

- 包装涂料

- 其他用途(电子电气涂料等)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率(%)/排名分析

- 公司简介

- AkzoNobel NV

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India Ltd.

- DAW SE

- Eastman Chemical Company

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

第七章 市场机会与未来展望

The green coatings market size stands at USD 146.46 billion in 2025 and is forecast to reach USD 183.56 billion by 2030, translating into a 4.62% CAGR.

Regulatory pressure that tightens limits on volatile organic compounds (VOC), rapid progress in water-borne chemistries and powder technologies, and higher penetration in automotive and architectural uses remain the central growth engines of the green coating market. California's South Coast Air Quality Management District has already cut allowable VOC content in automotive refinish products under amended Rule 1151 and will enforce even stricter levels by 2033. In parallel, the European Union will prohibit per- and polyfluoroalkyl substances (PFAS) in food-contact packaging from August 2026, redirecting packaging formulators toward bio-based barriers. OEMs seeking lower energy paint shops and builders pursuing green certifications are expanding the addressable pool for sustainable solutions, while technology that lifts the durability of water-based resins now rivals solvent-borne systems.

Global Green Coatings Market Trends and Insights

Stringent Environmental Regulations on VOC Emissions

New VOC limits are redefining acceptable formulation windows for the green coating market. South Coast AQMD's Rule 1151 phases in lower VOC ceilings for automotive refinish products beginning May 2025 and culminates in the strictest thresholds by 2033, pushing body shops toward water-borne systems. On another front, the EU Packaging and Packaging Waste Regulation caps PFAS at 25 ppb per individual substance and 250 ppb total, steering packaging suppliers to bio-based coatings that avoid fluorinated chemistries. Businesses already holding portfolios of compliant products gain a first-mover advantage, whereas producers tied to legacy solvent-borne lines face incremental compliance cost and potential market exclusion.

Growing Demand for Low-VOC Architectural Coatings

Home repairs, commercial retrofits, and green-building standards continue to draw the construction value chain toward low-VOC alternatives. Sherwin-Williams reports a noticeable shift in residential repaint orders toward paints designed for easy recycling and lower embodied carbon. Water-borne formulations now deliver the same gloss retention and scrub resistance as solvent-borne equivalents. AkzoNobel's RUBBOL WF 3350 exemplifies this transition, pairing 20% bio-based content with warranty-backed durability in indoor and outdoor wood finishes.

Performance Gaps Versus Solvent-Borne in Harsh Environments

Marine hulls, offshore platforms, and chemical storage tanks still demand the long-term fouling resistance and barrier strength of high-solids epoxies rich in solvents. Although self-healing siloxane hybrids and chrome-free inhibitors are emerging, their commercial adoption is gradual because certification cycles are lengthy and shipowners resist untested chemistries.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift Toward Energy-Efficient Paint Shops

- Advances in Water-Based Resin Chemistry Enhancing Durability

- Higher Total Applied Cost for End-Users

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems preserved leadership in 2024 with a 55.16% share of the green coating market. Their dominance is rooted in favorable compliance footprints and constant resin upgrades that yield mechanical strength on par with solvent-borne counterparts. Mazda's plant-wide switch to advanced water-based topcoats alone lowered VOC output by 57% while retaining showroom-grade gloss. Powder coatings, however, offer the most rapid trajectory, advancing at 6.51% CAGR to 2030. Catalyst-assisted infrared ovens now cure thick films in just 2-3 minutes at roughly 225 °C, elevating production throughput and slashing utility bills. Sherwin-Williams' Powdura ECO illustrates circular design, embedding every pound of powder with recycled PET equal to sixteen half-liter bottles. The green coating market size for powder lines is projected to expand in tandem with low-temperature formulations that harden at 150 °C, opening doors to heat-sensitive plastics and MDF furniture. Meanwhile, UV-curable liquids occupy specialized niches in electronics where near-instant cure is mandatory.

The green coating industry also benefits from higher-solids alkyd and acrylic hybrids. These systems cut the solvent fraction below 250 g/L without sacrificing wet edge or adhesion to metallic substrates. Collectively, such variants reinforce the perception that sustainable chemistries can meet or exceed conventional benchmarks.

The Green Coatings Market Report is Segmented by Type (Water-Borne, Powder, and More), Application (Architectural Coatings, Industrial Coatings, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific confirmed its dominance with 44.05% of 2024 revenue while charting the fastest 5.56% CAGR through 2030. Indonesian output surpassed 1 million tons in 2024, with waterborne decorative paints taking a striking 67% share of local production. The region's green coating market is further stimulated by China's express-packaging law GB 43352-2023 that forces e-commerce warehouses to switch to compliant coatings. India's move to tighten food-container rules under the Food Safety and Standards Authority (FSSAI) also underpins demand. Continued urbanization, automotive build-outs, and foreign direct investment into OEM paint shops present long-run momentum.

North America enjoys a resilient path powered by California's VOC benchmarks and robust residential repaint cycles. General Motors' three-wet technique underscores the competitive edge of low-energy lines, and multiple Tier 1 suppliers pivot to water-borne primers that simplify color changeover. Canada mirrors this progress through appliance manufacturers investing in powder booths, whereas Mexico's coil-coating capacity staking USD 3.6 million in upgrades provides the region a cost-efficient supply hub.

Europe remains a heavyweight courtesy of sweeping PFAS restrictions and carbon-border considerations that motivate rapid reformulation. Member states impose antidumping duties on high-solvent titanium dioxide imports, indirectly steering formulators toward lower-solids or water-borne routes that require less pigment. Germany and France continue to incubate bio-based resin start-ups, fostering technical collaborations with existing conglomerates.

Emerging geographies in South America, the Middle East, and Africa post moderate yet accelerating uptake. Brazil's industrial output and Saudi Arabia's Vision 2030 mega-projects heighten the relevance of sustainable coatings in protective steelwork and decorative lines. However, fragmented regulatory enforcement and limited access to renewable feedstocks temper pace in several local markets.

- AkzoNobel N.V.

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India Ltd.

- DAW SE

- Eastman Chemical Company

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent environmental regulations on VOC emissions

- 4.2.2 Growing demand for low-VOC architectural coatings

- 4.2.3 Automotive OEM shift toward energy-efficient paint shops

- 4.2.4 Advances in water-based resin chemistry enhancing durability

- 4.2.5 Adoption of bio-based resins from agricultural waste

- 4.3 Market Restraints

- 4.3.1 Performance gaps versus solvent-borne in harsh environments

- 4.3.2 Higher total applied cost for end-users

- 4.3.3 Supply constraints of bio-based feedstocks

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Water-borne

- 5.1.2 Powder

- 5.1.3 High-solids

- 5.1.4 UV-cured coatings

- 5.2 By Application

- 5.2.1 Architectural Coatings

- 5.2.2 Industrial Coatings

- 5.2.3 Automotive Coatings

- 5.2.4 Wood Coatings

- 5.2.5 Packaging Coatings

- 5.2.6 Other Applications (Electronics and Electrical Coatings, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Arkema

- 6.4.3 Asian Paints Ltd.

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Beckers Group

- 6.4.7 Berger Paints India Ltd.

- 6.4.8 DAW SE

- 6.4.9 Eastman Chemical Company

- 6.4.10 Evonik Industries AG

- 6.4.11 Hempel A/S

- 6.4.12 Jotun

- 6.4.13 Kansai Paint Co., Ltd.

- 6.4.14 Nippon Paint Holdings Co., Ltd.

- 6.4.15 PPG Industries Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Sika AG

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

绿色涂料市场报告:按类型、应用和地区划分(2026-2034年)

绿色涂料市场报告:按类型、应用和地区划分(2026-2034年) 全球绿色涂料市场规模、份额、趋势和成长分析报告(2026-2034)

全球绿色涂料市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球绿色涂料市场报告

2026年全球绿色涂料市场报告 绿色涂料市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年全球绿色涂料市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034年)日本绿色涂料市场报告(按类型(水性、粉末、高固含量、UV固化)、应用(建筑涂料、工业涂料、汽车涂料、木器涂料、包装涂料及其他)和地区划分,2026-2034)

绿色涂料市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年全球绿色涂料市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034年)日本绿色涂料市场报告(按类型(水性、粉末、高固含量、UV固化)、应用(建筑涂料、工业涂料、汽车涂料、木器涂料、包装涂料及其他)和地区划分,2026-2034) 绿色涂料市场规模、份额和成长分析(按技术、最终用户和地区划分)—2026-2033年产业预测

绿色涂料市场规模、份额和成长分析(按技术、最终用户和地区划分)—2026-2033年产业预测